Smart Insulin Pens Market Report Scope & Overview:

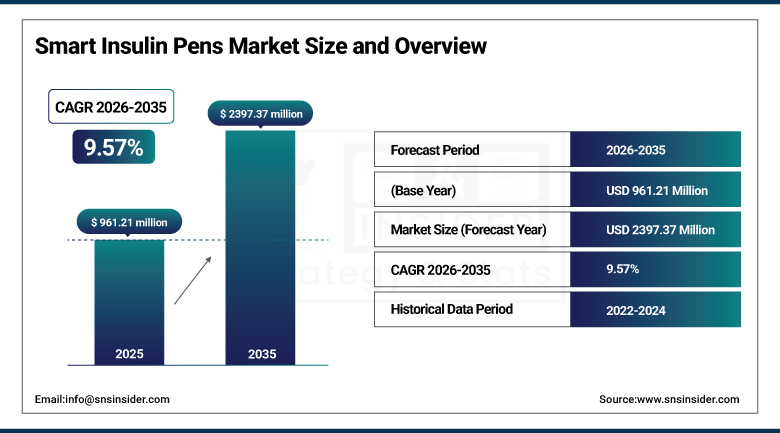

The Smart Insulin Pens Market was estimated at USD 961.21 Million in 2025 and is expected to reach USD 2397.37 Million by 2035 and grow at a CAGR of 9.57% over the forecast period of 2026-2035.

The smart insulin pens market is experiencing robust and accelerating growth, driven by the escalating global burden of diabetes with the International Diabetes Federation reporting over 537 Million adults living with diabetes worldwide as of 2024, a figure projected to exceed 783 Million by 2045. Smart insulin pens represent a transformative evolution in insulin delivery technology, integrating Bluetooth connectivity, dose memory, real-time tracking, and seamless data synchronisation with smartphone applications and continuous glucose monitors (CGMs) to deliver unprecedented precision and patient empowerment in insulin therapy management. Unlike conventional insulin pens that provide no digital feedback or dose-logging capability, smart pens enable automatic dose capture, missed-dose alerts, bolus calculators, and data sharing with healthcare providers transforming episodic diabetes management into a continuous, data-driven therapeutic relationship. The convergence of digital health platforms, expanding home healthcare trends, rising telemedicine adoption, and strong reimbursement programmes across North America and Europe is accelerating smart pen adoption across both Type 1 and Type 2 diabetes patient populations.

As healthcare systems globally transition away from reactive, insulin management-dependent approaches to diabetes care and research focus intensifies on optimising therapy through digital health connectivity; a stunning acceleration of convergence amongst precision medicine, digital health connectivity and the global diabetes epidemic appears inevitable – augmenting adoption rates such that smart insulin pens are rapidly evolving from premium niche devices into the new standards of care for insulin-dependent patients and compounding demand growth across every major geography through the entirety of our long-term forecasts.

Market Size and Forecast:

-

Market Size in 2025: USD 961.21 Million

-

Market Size by 2035: USD 2397.37 Million

-

CAGR: 9.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022–2024

To Get more information on Smart Insulin Pens Market - Request Free Sample Report

Smart Insulin Pens Market Trends:

-

Accelerating integration of Bluetooth-enabled dose tracking with third-party CGM platforms including Dexcom G7 and Abbott FreeStyle Libre 3, enabling closed-loop insulin management insights without requiring a dedicated insulin pump.

-

Rising demand for reusable smart insulin pens that reduce long-term device costs while delivering full digital connectivity, appealing to cost-conscious healthcare systems and value-oriented patients across both developed and emerging markets.

-

Expansion of telehealth and remote diabetes management platforms that enable endocrinologists to review smart pen dose data, time-in-range metrics, and adherence patterns during virtual consultations, improving clinical outcomes.

-

Growing adoption of AI-powered insulin dose recommendation algorithms embedded in diabetes management apps connected to smart pens, enabling personalised bolus suggestions based on meal data, physical activity, and historical glucose patterns.

-

Increasing regulatory approvals across the FDA, EMA, and emerging market agencies for next-generation smart pen platforms incorporating missed-dose detection, temperature monitoring, and integrated healthcare provider data sharing.

-

Expansion of manufacturer-pharma company collaborations including partnerships between smart pen OEMs and insulin manufacturers such as Novo Nordisk and Eli Lilly creating bundled therapy-device solutions that simplify patient adoption.

-

Rising smartphone penetration across Asia Pacific and Latin America enabling broader adoption of app-connected smart pen platforms in markets where digital health infrastructure was previously a barrier to connected device adoption.

U.S. Smart Insulin Pens Market Outlook:

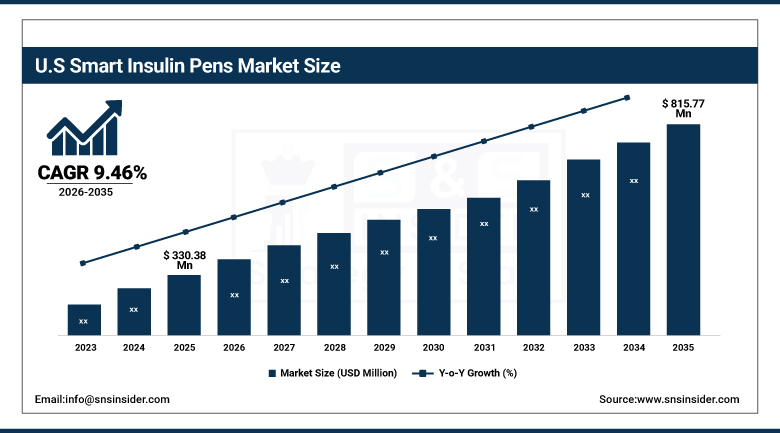

U.S. Smart Insulin Pens Market was valued at USD 330.38 Million in 2025 and is expected to reach USD 815.77 Million by 2035, registering a CAGR of 9.46% during 2026-2035.

The U.S. is the largest single national market for smart insulin pens worldwide, supported by the highest per-capita health care expenditures, a large target addressable patient population estimated at approx. 38 Million Americans with diabetes, established FDA regulatory pathways for connected medical devices and comprehensive insurance reimbursement frameworks increasingly viewing smart pen platforms as routine diabetes care devices. Rapid adoption of digital technologies by patients, combined with an advanced consumer-driven demand for integrated digital health, and broad clinical endorsement (ADA and AACE) are the hallmarks of the U.S. market for diabetes care smart pens. Among the action elements driving individual market dynamics include growth in the CGM installed base looking for smart pen connectivity compatibility, and physician familiarity with smart pen data platforms due to prior integrations into EMR systems as well as commercial momentum from offerings such as Medtronic's InPen, Novo Nordisk's NovoPen 6, Ypsomed's SmartPilot system.

The 2025 FDA 510(k) clearance of Ypsomed's SmartPilot add-on device, which transforms the standard YpsoMate autoinjector into a fully connected smart device with dose tracking and therapy management features is just one example of the innovation pipeline powering the U.S. smart insulin pens market as manufacturers continue to compete to deliver digital connectivity upgrades that are compatible with the current installed base of insulin delivery devices without requiring full device replacement.

Smart Insulin Pens Market Segment Analysis:

-

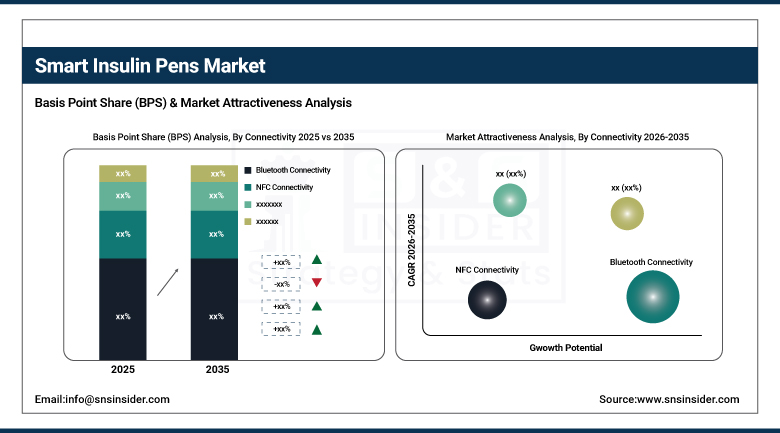

Based on Connectivity, Bluetooth accounted for the largest market share (73%) in 2025; NFC expected to be the fastest-growing segment.

-

Based on Indication, Type 1 Diabetes accounted for the largest market share in 2025; Type 2 Diabetes expected to be the fastest-growing indication segment.

-

Based on Product Type, Smart Connected Pens accounted for the largest market share in 2025; Reusable Pens expected to be the fastest-growing segment.

-

Based on Distribution Channel, Hospital Pharmacy accounted for the largest market share in 2025; Online Pharmacy expected to be the fastest-growing distribution channel.

By Connectivity: Bluetooth dominates, NFC expected to grow fastest

The Bluetooth segment accounted for more than 73% share of total market revenue in 2025 and is anticipated to dominate the global Smart Insulin Pens Market during the forecast period. Bluetooth insulin pens eliminate the need for manual pen reading and patient data entry by providing seamless wireless bridging to insulin tracking apps and connected diabetes management devices to capture doses in real time, populate logbooks automatically, and enable immediate sharing of data with healthcare providers. Bluetooth technology is found in all newly purchased consumer electronic devices that are either sold or used, and with the rapid growth of dedicated diabetes management applications operational via Bluetooth smart pens on both the iOS and Android platforms—establishing Bluetooth as the de facto connectivity standard. The biggest pen platforms (Medtronic InPen, NovoPen 6, Biocorp Mallya) are all already Bluetooth-enabled, locking patients and providers deeper into the ecosystem of diabetes management workflows that repurpose Bluetooth for integrated clinical recommendations.

NFC (Near Field Communication) segment is anticipated to have the highest CAGR throughout 2035, owing to its convenience in contactless data exchange and connectivity between devices such as smart pens, which creates a new pool of patients due to the increase of smartphone penetration and digital health adoption within emerging economies with affordable connectivity. NFC pens have no battery contained within the pen cap to transmit dose data via contactless transfer, enabling patients to tap the pen against their NFC-enabled smartphone, which reduces device complexity, maintenance requirements and manufacturing costs compared with active Bluetooth modules. That being said, the NFC cost advantage makes NFC an appealing technology pathway for smart pen entry in developing markets with more constrained healthcare budgets.

By Indication: Type 1 Diabetes dominates, Type 2 Diabetes grows fastest

Type 1 Diabetes (T1D) represented the dominant indication segment in the Smart Insulin Pens Market in 2025, owing to the complete insulin dependency of T1D patients who need MDI for life — and because precise dosing accuracy is crucial to circumvent hypoglycaemia and hyperglycaemia crises in the high-acuity patient population comprising these patients. Patients with T1D and their care partners have the most engagement with digital diabetes management tools, and are among the first to adopt smart pen technology that supports monitoring of insulin delivery via time-sensitive dosing patterns, enabling patients to share full data streams with their endocrinology teams.

Type 2 Diabetes is anticipated to be the fastest growing indication segment in the forecast period 2035 backed by a considerably larger and faster-paced annual global T2D patient population, approximately 30% of which are expected to require insulin therapy. With health economic advantages, greater user friendliness as a result of interface implementation that appeals to older patient demographics characteristic of the Type 2 diabetes (T2D) population and increasing clinical support for smart pen-related improvements in glycaemic control reductions in HbA1c levels) and treatment adherence among T2D patients, adoption is currently gathering pace ahead of general practitioners; diabetologists and primary care providers who manage most insulin-treated T2D patients worldwide.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

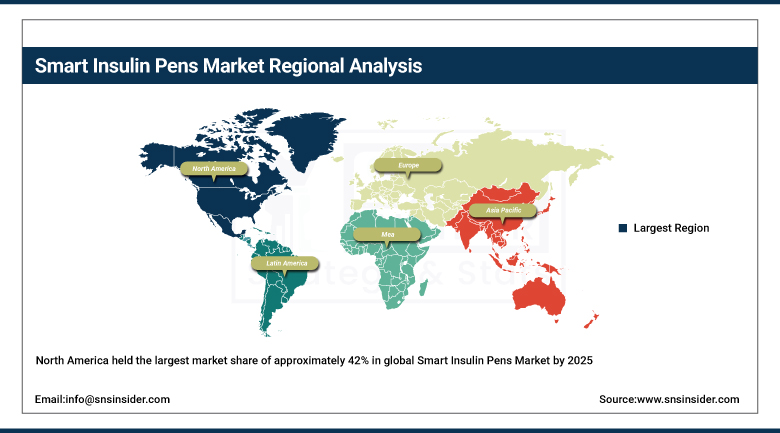

North America |

United States |

42% |

|

Europe |

Germany |

31% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

45% |

North America Smart Insulin Pens Market Insights

North America held the largest market share of approximately 42% in global Smart Insulin Pens Market by 2025 The United States anchors regional leadership with the worlds highest per-capita healthcare expenditure, aligned regulatory frameworks supporting connected medical device innovation via a robust FDA continuum of evidence and reimbursement pathways that increasingly encompass smart pen platforms for insulin-dependent patients. Over half of the regional smart pen OEMs also have U.S. commercial operations, including leading manufactures such as Medtronic, Companion Medical and Biocorp, further confirming the region's technology leadership. In Canada, meaningful contributions emerge from provincial health authority endorsement of digital diabetes management tools and increasing up-take among those insulin-requiring patients who are covered by provincial formulary programmes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Smart Insulin Pens Market Insights

Asia Pacific is set to register the largest regional CAGR during 2026-2035, spurred on by the unprecedented burden of the regional diabetes epidemic (China and India together contain over 200 Million diabetes patients), Digital health infrastructure improving rapidly alongside increasing smartphone connectivity Conrad global solution The role COVID in changing digital wellbeing investment levels and more US exports of Sino Indian management programmes. National informatisation strategies in China, sophisticated digital healthcare infrastructure in Japan, an advanced medical technology industry backed by policy incentives in South Korea, and growing middle-class demand for quality diabetes care in India provide a tectonically capable addressable market for smart insulin pen technology.

Europe Smart Insulin Pens Market Insights

Europe continues to be at the forefront of the Global Smart Insulin Pens Market, as almost all countries in the region have well-established national health systems that facilitate the integration of digital diabetes management tools into national standard care pathways, multiple advanced smart pen platforms have received regulatory approval from authorities using EMA's Medical Device Regulation (MDR) framework, and high patient health literacy are driving demand for sophisticated diabetes management solutions. Germany, France, the UK and the Netherlands are Europe's largest regional diabetes markets characterised by advanced diabetes clinical networks, broad reimbursement of approved insulin delivery devices and increasing integration between smart pen data platforms and national electronic health record systems.

Middle East & Africa and Latin America Smart Insulin Pens Market Insights

The MEA and Latin America markets are expected to progress at a high growth rate throughout the forecast period owing to increasing prevalence of diabetes, rapid population growth in these regions along with continuously evolving middle-class societies with increased investments in the healthcare sector. The UAE is the most advanced geography within MEA to its sophisticated healthcare infrastructure, concentration of high-income patients and government backed digital health initiatives. Brazil is the largest regional revenue contributor in Latin America driven by its significant diabetes population, expanding private healthcare sector and improving physician knowledge of connected diabetes management platforms.

Smart Insulin Pens Market Dynamics

Drivers: Surging global diabetes prevalence creating irreversible structural demand for precision insulin delivery and digital management solutions

The primary structural growth driver for the Smart Insulin Pens Market is the relentless expansion of the global diabetes epidemic with approximately 537 Million adults currently living with diabetes worldwide creating tens of Millions of new insulin-requiring patients annually who represent addressable demand for smart pen platforms. As healthcare systems globally intensify diabetes management quality goals including HbA1c targets, time-in-range optimisation, and hypoglycaemia reduction the clinical superiority of smart pens over conventional pens in enabling precision dosing, adherence tracking, and provider data review is creating a compelling upgrade incentive across the entire insulin-pen user base.

The 2024 FDA clearance of Medtronic's new InPen app featuring missed-dose detection enabling the upcoming Smart MDI system's integration with the Simplera CGM for real-time dosing insights exemplifies the accelerating innovation cycle in smart pen technology that is transforming standalone connected pens into core components of integrated digital diabetes management ecosystems, creating premium differentiation and reinforcing adoption momentum across both T1D and T2D patient populations through the forecast period.

Restraints: High device cost, reimbursement gaps, and digital health literacy barriers limiting adoption in price-sensitive and underserved markets

A significant restraint on the Smart Insulin Pens Market is the premium cost of smart pen devices and associated app subscriptions relative to conventional insulin pens, which creates meaningful affordability barriers in price-sensitive emerging markets and for uninsured or underinsured patient populations even in developed economies. Reimbursement coverage for smart pen platforms varies substantially across insurance systems and geographic markets — with comprehensive coverage established in select European markets and certain U.S. insurance plans, but significant gaps remaining across many markets — limiting adoption to patients who can self-fund device costs. Digital health literacy requirements for effective smart pen utilisation, including smartphone ownership, app navigation proficiency, and willingness to engage with diabetes data, also constrain adoption among older T2D patient demographics who represent a significant share of the insulin-requiring population.

Opportunities: CGM integration, AI-powered dosing algorithms, and emerging market expansion

The growing oral integration between smart insulin pens with continuous glucose monitoring platforms represents, arguably, the biggest commercial growth opportunity in the near future as patients and healthcare providers alike continue to call for seamless data transfer connectivity between insulin delivery technology and glucose sensing solutions allowing for closed loop insulin management insights without the complexity (and price) of a dedicated insulin pump solution. Software features utilising AI-bolus calculation and dose recommendation capabilities in smart pen connected apps are generating a premium quality software component which is able to charge subscription revenues while positively influencing patient outcomes. Smart pen manufacturers that are able to devise cost-optimised smart pen solutions fit-for the emerging market business case and health system characteristics are likely to find appealing expansion opportunities in Asia Pacific, Latin America, and Middle East where the diabetes population is growing rapidly combined with decreasing smart pen manufacturing costs as volume scales.

Recent Developments:

-

2025: Ypsomed received FDA 510(k) clearance for SmartPilot, an innovative add-on that transforms the YpsoMate autoinjector into a connected smart device, enabling seamless dose tracking and therapy management — broadening smart connectivity to the existing autoinjector installed base without requiring full device replacement.

-

2024: Medtronic received FDA clearance for a new InPen app featuring missed-dose detection capability, enabling its upcoming Smart MDI system's integration with the Simplera CGM to provide patients and clinicians with real-time dosing insights and enhanced glucose management visibility.

-

2024: Novo Nordisk expanded commercial availability of its NovoPen 6 smart insulin pen — featuring dose memory and NFC connectivity — across additional European and Asia Pacific markets, reinforcing its leadership in connected insulin delivery device technology.

-

2025: Biocorp extended the Mallya smart cap's compatibility to additional insulin pen models and launched a dedicated clinical data platform enabling healthcare providers to access aggregated smart pen dose data across their diabetes patient populations through a single integrated dashboard.

-

2024: Companion Medical (Medtronic subsidiary) expanded the InPen ecosystem with enhanced bolus calculator algorithms incorporating personalised insulin-to-carbohydrate ratio adjustments and improved hypoglycaemia prediction alerts driven by real-time CGM data integration.

Smart Insulin Pens Market Key Players:

-

Medtronic plc

-

Novo Nordisk A/S

-

Eli Lilly and Company

-

Ypsomed Group

-

Companion Medical

-

Biocorp

-

Smiths Medical

-

Sanofi S.A.

-

Cambridge Consultants Ltd.

-

NIPRO Medical Corporation

-

Roche Diabetes Care

-

Dexcom, Inc.

-

Abbott Laboratories

-

AgaMatrix, Inc.

-

InjexUK

-

Jiangsu Delfu Medical Device Co., Ltd.

-

Ascensia Diabetes Care

-

Bayer AG

-

Tandem Diabetes Care

-

Emperra GmbH

Smart Insulin Pens Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 961.21 Million |

| Market Size by 2035 | USD 2397.37 Million |

| CAGR | CAGR of 9.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Connectivity (Bluetooth Connectivity, NFC Connectivity, Others) • By Indication (Type 1 Diabetes, and Type 2 Diabetes) • By Product Type (Smart Connected Pens, Reusable Pens, Disposable Pens) • By Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic plc, Novo Nordisk A/S, Eli Lilly and Company, Ypsomed Group, Companion Medical, Biocorp, Smiths Medical, Sanofi S.A., Cambridge Consultants Ltd., NIPRO Medical Corporation, Roche Diabetes Care, Dexcom Inc., Abbott Laboratories, AgaMatrix Inc., InjexUK, Jiangsu Delfu Medical Device Co. Ltd., Ascensia Diabetes Care, Bayer AG, Tandem Diabetes Care, Emperra GmbH. |

Frequently Asked Questions

North America dominated the Smart Insulin Pens Market in 2025 with approximately 42% of global market revenue, driven by the highest per-capita healthcare expenditure, robust FDA regulatory frameworks, comprehensive insurance reimbursement coverage for smart pen platforms, and the concentration of leading smart pen manufacturers and digital diabetes management technology innovators.

The Bluetooth segment dominated the Smart Insulin Pens Market in 2025, capturing over 73% of global revenue, driven by seamless wireless connectivity with diabetes management apps, real-time dose tracking, and compatibility with major CGM platforms across the leading smart pen ecosystems.

The escalating global diabetes epidemic — affecting over 537 million adults worldwide — combined with the clinical superiority of smart pens in enabling precision dosing, adherence tracking, and CGM integration, and accelerating digital health adoption across healthcare systems globally, is the primary structural growth driver for the market.

The Smart Insulin Pens Market was valued at USD 961.21 million in 2025.

The Smart Insulin Pens Market is expected to grow at a CAGR of 9.57% from 2026 to 2035.

Get in Touch