Solar Inverter Market Report Scope & Overview:

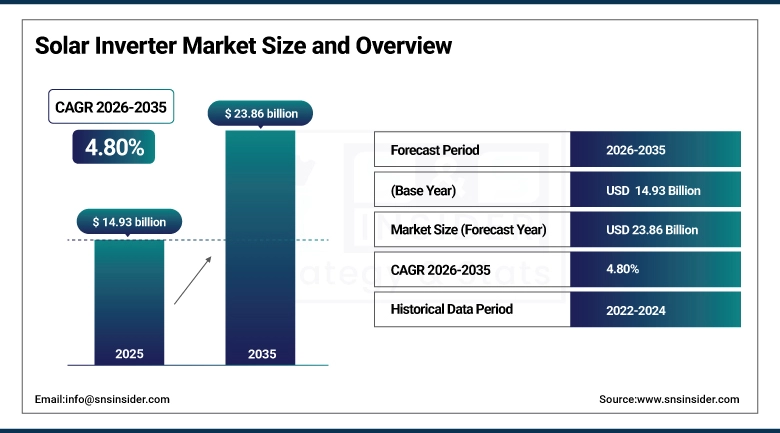

The Solar Inverter Market size was valued at USD 14.93 Billion in 2025 and is projected to reach USD 23.86 Billion by 2035, growing at a CAGR of 4.80% during 2026–2035.

A surge in environmental awareness among people across the globe along with a favourable government attitude towards renewable energy is boosting the Solar Inverter Market. Increasing installation of solar systems in residential, commercial and utility industries is increasing sales. The market growth is also bolstered by technological advancements such as smart inverters and advanced grid integration abilities. Furthermore, a drop in solar component prices, increased energy demand, and investments in infrastructure development in emerging countries, will be playing the key role in market growth during the period of projection.

Solar Inverter Market Size and Growth Forecast:

-

Market Size in 2025: USD 14.93 Billion

-

Market Size by 2035: USD 23.86 Billion

-

CAGR: 4.80% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Solar Inverter Market - Request Free Sample Report

Solar Inverter Market Key Trends:

-

Smart and hybrid inverters are driving the fastest-growing segment due to enhanced grid interaction and energy management capabilities.

-

String inverters are gaining popularity for commercial and industrial installations, while central inverters remain dominant in large utility-scale projects.

-

Increasing demand for grid stability is accelerating the adoption of smart inverters with advanced monitoring and control features.

-

Rising integration of energy storage systems is boosting demand for hybrid solar inverters across residential and commercial sectors.

-

High dependence on imports of electronic components, especially from Asia, poses supply chain and pricing risks.

-

Growing demand for compact, efficient, and lightweight inverters to support rooftop solar installations and distributed energy systems.

-

Advanced inverters are increasingly required for applications such as microgrids, rural electrification, and critical infrastructure, ensuring high reliability and performance.

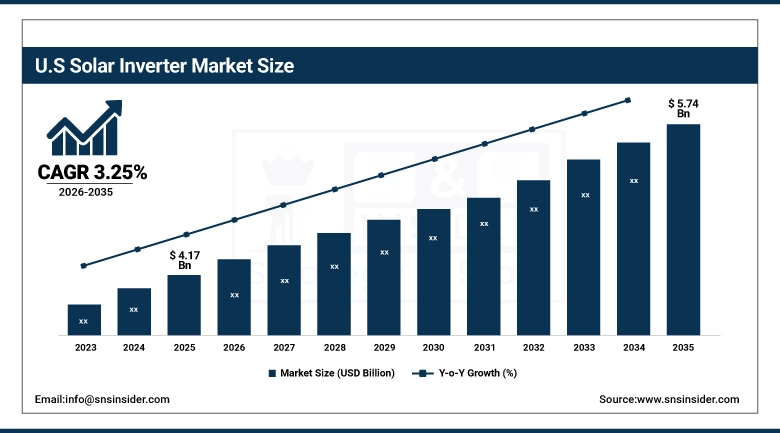

U.S. Solar Inverter Market Size Outlook:

The U.S. Solar Inverter Market was valued at approximately USD 4.17 Billion in 2025 and is projected to reach around USD 5.74 Billion by 2035, growing at a CAGR of about 3.25% during 2026–2035. Growth in the U.S. solar inverter market is driven by rising residential and commercial solar adoption, supportive government incentives, increasing grid modernization efforts, and demand for smart inverters. Expanding energy storage integration and focus on clean energy transition further support steady market growth.

Solar Inverter Market Key Drivers:

-

Rising adoption of solar energy systems across residential, commercial, and utility-scale sectors is driving demand for solar inverters.

Encouraging government regulations, subsidies, and renewable energy targets are speeding up solar installations around the globe. The adoption of advanced inverters such as string and hybrid inverters, is further propelled by rising demand for efficient energy conversion, grid stability, and smart energy management solutions. At the same time, cost effusion of solar elements as well as the constant urbanization in developing economies is furthermore contributing considerably to market growth.

Solar Inverter Market Key Restraints:

-

High initial costs and technical complexities associated with advanced solar inverter systems are restraining market growth.

Reliance on electronic component imports and vulnerability to supply chain disruptions, particularly from Asia, pose pricing and availability issues. Other reasons for the hindrance of adoption include incompatibility with existing grid infrastructure, as well as the high maintenance and replacement costs. Additionally, the fast pace of technological shifts necessitates constant upgrades, leading to additional operational costs for end-users and hindering adoption in price-sensitive areas.

Solar Inverter Market Key Opportunities:

-

Integration of energy storage systems and smart grid technologies is creating significant growth opportunities for the solar inverter market.

In addition-growing adoption of hybrid inverter in residential and commercial sector would syphon, new opportunity for the market along-with-increasing investment in the sectors such as microgrids and rural electrification project. Another avenue of innovation is opened up by upcoming trends including digital monitoring, Artificial Intelligence-based automated energy management and IoT-based inverters. Many parts of the world are also funneling more investment into next gen solar infrastructure due to greater focus on sustainable energy and decarbonization.

Solar Inverter Market Segments:

-

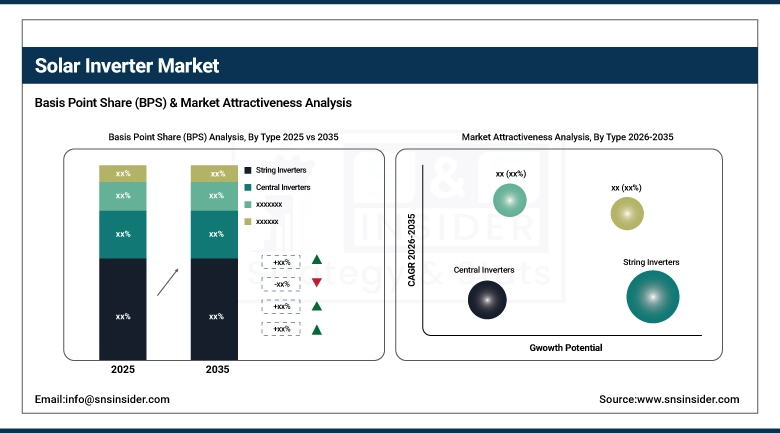

By Type: In 2025, String Inverters dominated with 46% share; Micro Inverters fastest growing segment during 2026–2035

-

By System Type: In 2025, Grid-Tied Inverters dominated with 62% share; Hybrid Inverters fastest growing segment during 2026–2035

-

By Application: In 2025, Utility-Scale dominated with 48% share; Residential fastest growing segment during 2026–2035

-

By End User: In 2025, Utilities dominated with 50% share; Residential Users fastest growing segment during 2026–2035

By Type, String Inverters Dominate While Micro Inverters Grow Rapidly:

Solar inverters of the string type accounted for the largest share of the global solar inverter market as they are the most economical, easy to install, and appropriate for use in commercial and utility projects. This combination of performance and affordability makes them an extremely popular option for many installations.

Micro inverters are the fastest-growing segment owing to their module-level optimization, improved energy efficiency, and enhanced monitoring capabilities. They are more and more used in residential systems with importance on their performance and flexibility.

By System Type, Grid-Tied Inverters Dominate While Hybrid Inverters Grow Rapidly:

Grid-tied inverters are primarily used for residential and large-scale solar systems as they are grid-connected, thus providing homeowners the opportunity to save on bills by drawing electricity from the utility grid. This makes them a great option for many users since they are so simple and inexpensive.

Hybrid inverters are experiencing the fastest growth amongst inverter types, due to growing battery storage system integration adoption and energy backup demand. Such inverters are flexible as they merge solar generation along with storage functions, making them preferable for a modern energy system.

By Application, Utility-Scale Dominates While Residential Grows Rapidly:

Utility-scale applications remained the key contributor to the solar inverter market as installations of solar farms and power generation needs became larger. The advantages of scale, centralized infrastructure, and continued government support for renewable energy deployment are benefiting these projects.

Rising electricity prices, accelerating rooftop solar installations, and enabling net metering regulations are the growth drivers behind residential being the fastest-growing segment. And the increasing consumer awareness coupled with the demand for energy independence is accelerating growth in this segment.

By End User, Utilities Dominate While Residential Users Grow Rapidly:

Their extensive investments in big solar projects and development of grid infrastructure have contributed to the bulk share of the utility sector in the solar inverter market. It’s what will help the nation bash renewable energy targets.

It is the fastest-growing segment owing to the growing installation of rooftop solar systems, more incentives and initiatives to implement home solar systems, and the need for electricity bill savings. The explainable delay can also be attributed to the growing interest in sustainable living

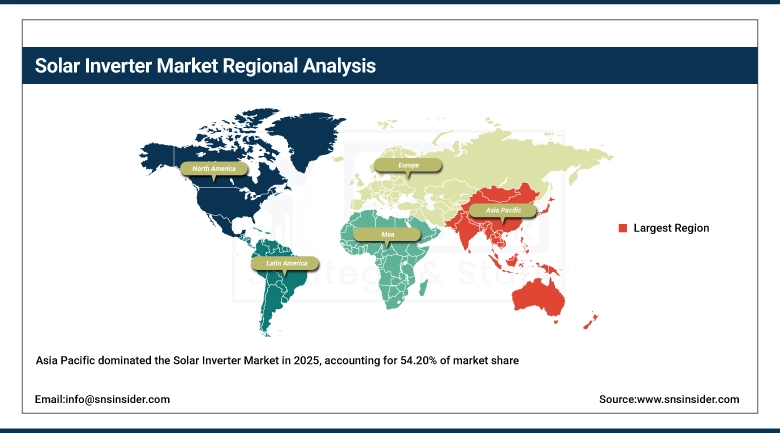

Solar Inverter Market Regional Analysis:

Asia-Pacific Solar Inverter Market Insights:

The solar inverter market is dominated by Asia-Pacific where the value hold by the region is 54.20% while it is the fastest growing region at 5.85% during the study period. The high non-life insurance adoption rates in countries such as Chinese, Indian, Japan, and South-Korea etc. mainly due to extensive large-scale solar PV installations, rapid industrialization, and a strong government policy to boost renewable energy sector. Low manufacturing cost, strong supply chains and major inverter manufacturers are advantages of the region, and that is the reason it is the most well-accessed world for solar energy.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Solar Inverter Market Insights:

North America is a developed market with technological plasticity driven by high-level home and business solar system acceptance, particularly in the United States and Canada. Positive policies along with tax reforms, and rising investment in smart grid infrastructure are primarily fueling the market growth. Moreover, increasing acceptance of energy storage systems also, smart inverters, is supporting the market growth in the region.

Europe Solar Inverter Market Insights:

Supportive targets for renewables, environmental regulations, and rising investments in sustainable infrastructure predominantly drive the solar inverter market in Europe. Top market nations such as Germany, Spain, and Italy have obscene numbers of solar uptake. With a strong emphasis on energy efficiency, grid stability, and renewable energy integration, the region represents a key driver for global market growth.

Latin America Solar Inverter Market Insights:

The Latin American region, with nascent solar installations in places such as Brazil and Mexico, is also an emerging market but is also slightly less predictable. The growth of the market can be attributed to the growing energy demand, favorable climatic conditions, and government initiatives. Solar inverters drive consistent demand across the region as utility-scale solar investments gains pace in the region.

Middle East & Africa (MEA) Solar Inverter Market Insights:

The Middle East & Africa Market being a developing region, it is poised to benefit from the availability of a large solar resource pool and increasing investments in renewables projects is well placed as well. UAE, Saudi Arabia, South African automakers are leading the charge, powered by diversification of energy sources + some government initiative Demand for solar inverters in the region is being propelled through growing utility-scale solar projects and rural electrification initiatives.

Solar Inverter Market Competitive Landscape:

Huawei Digital Power is a China-based global leader in solar inverters. The Company offers advanced smart PV solutions to achieve energy efficiency and reliability for the systems using AI, cloud monitoring, and smart grid technologies. Focusing on its role in utility-scale and commercial solar projects, Huawei uses high-efficiency string inverters and energy storage integration solutions to position itself as a top player in the global solar inverter market.

-

In 2024, Huawei expanded its smart PV portfolio with enhanced AI-powered diagnostics and grid-forming inverter technologies to support large-scale renewable integration.

Sungrow Power Supply with headquarters in China is one of the world's largest manufacturer of Solar Inverters, with products ranging from String, central to hybrid inverters. With ongoing R&D investments and a global expansion, the company has a solid footing in the utility-scale solar and energy storage sectors. Sungrow solutions enjoy leading market shares for their efficiency, scalability, and cost competitiveness.

-

In 2025, Sungrow announced the expansion of its inverter manufacturing capacity and launched next-generation modular inverters to cater to growing global solar demand.

Solar Inverter Companies are:

-

Sungrow Power Supply

-

SolarEdge Technologies

-

Enphase Energy

-

SMA Solar Technology

-

GoodWe Power Supply Technology

-

Ginlong Technologies (Solis)

-

Growatt New Energy Technology

-

TMEIC (Toshiba Mitsubishi-Electric)

-

Delta Electronics

-

Schneider Electric SE

-

ABB Ltd.

-

Mitsubishi Electric Corporation

-

Siemens AG

-

Power Electronics S.L.

-

SofarSolar

-

KACO New Energy GmbH

-

TBEA Co., Ltd.

-

Chint Power Systems (CPS)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.93 Billion |

| Market Size by 2035 | USD 23.86 Billion |

| CAGR | CAGR of 4.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type: (Central Inverters, String Inverters, Micro Inverters) • By System Type: (Grid-Tied Inverters, Off-Grid Inverters, Hybrid Inverters) • By Application: (Residential, Commercial & Industrial, Utility-Scale) • By End User: (Utilities, Residential Users, Commercial & Industrial Users) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Huawei Technologies, Sungrow Power Supply, SolarEdge Technologies, Enphase Energy, SMA Solar Technology, Fronius International, GoodWe Power Supply Technology, Ginlong Technologies (Solis), Growatt New Energy Technology, TMEIC (Toshiba Mitsubishi-Electric), Delta Electronics, Schneider Electric SE, ABB Ltd., Mitsubishi Electric Corporation, Siemens AG, Power Electronics S.L., SofarSolar, KACO New Energy GmbH, TBEA Co., Ltd., Chint Power Systems (CPS) |

Frequently Asked Questions

Ans: The Solar Inverter Market is expected to grow at a CAGR of 4.8% during 2026–2035.

Ans: The Solar Inverter Market size was valued at USD 14.93 Billion in 2025 and is projected to reach USD 23.86 Billion by 2035.

Ans: The key drivers of the Solar Inverter Market include increasing adoption of solar energy, supportive government policies and incentives, advancements in inverter technologies, rising demand for efficient energy management systems, and growing investments in renewable energy infrastructure.

Ans: The String Inverters segment dominated the Solar Inverter Market during the projected period.

Ans: North America dominated the Solar Inverter Market in 2025.

Get in Touch