Sovereign Cloud Market Report Scope & Overview:

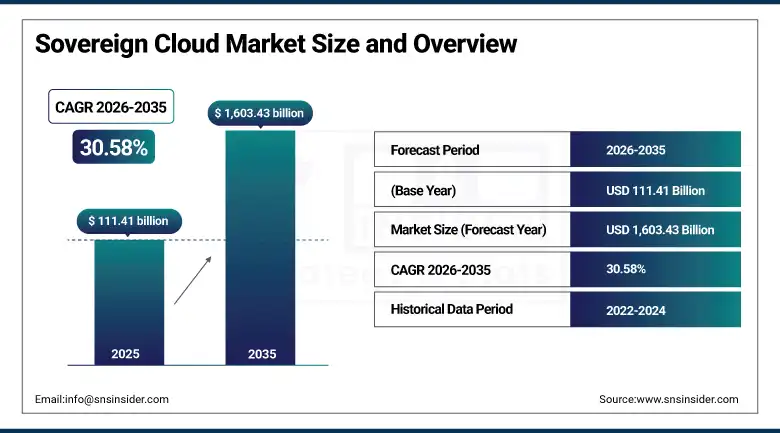

The Sovereign Cloud Market was valued at USD 111.41Billion in 2025 and is expected to reach USD 1,603.43 Billion by 2035, growing at a CAGR of 30.58% from 2026–2035.

The global sovereign cloud market is experiencing extraordinary commercial momentum driven by the convergence of government data localisation mandates, enterprise data sovereignty requirements, and the recognition that standard public cloud architectures built on foreign-headquartered hyperscaler infrastructure do not provide the jurisdictional control, operational independence, and regulatory compliance assurance that governments and regulated enterprises require for their most sensitive data and critical operational systems.

Microsoft launched its Cloud for Sovereignty initiative in 2023-2024, tailored to meet government-specific data residency and operational control requirements, enabling public sector organisations to deploy Azure workloads with enhanced sovereignty controls including encrypted data management, confidential computing, and government-controlled cryptographic key management. The initiative has been adopted by multiple European government agencies seeking to meet EU data sovereignty requirements while retaining access to Azure’s enterprise cloud capabilities and global compliance certification portfolio.

Market Size and Forecast

-

Market Size in 2026E: USD 145.46 Billion

-

Market Size by 2035: USD 1,603.43 Billion

-

CAGR: 30.58% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Sovereign Cloud Market - Request Free Sample Report

Sovereign Cloud Market Trends

-

Rising government data localisation legislation across the EU, India, Saudi Arabia, and Southeast Asia is creating compliance-driven sovereign cloud procurement mandates.

-

Growing enterprise adoption of confidential computing technology including secure enclaves and trusted execution environments is enabling sovereign cloud providers.

-

Increasing defence and intelligence community investment in sovereign cloud platforms is creating the most commercially demanding and technically sophisticated sovereign cloud use cases.

-

Expanding hyperscaler partnerships with national sovereign cloud operators is enabling governments to access global cloud scale and AI capability.

-

Rising SME adoption of sovereign cloud services through cost-effective shared sovereign infrastructure is democratising regulatory-compliant cloud access.

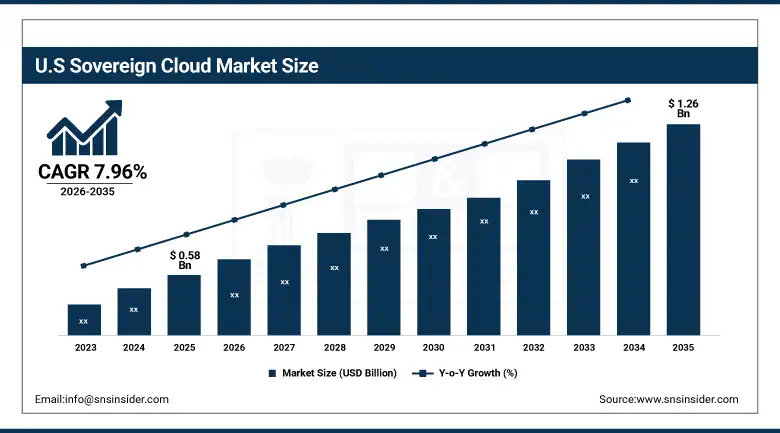

U.S. Sovereign Cloud Market Outlook

The U.S. Sovereign Cloud Market was valued at approximately USD 0.58 Billion in 2025 and is expected to reach approximately USD 1.26 Billion by 2035, growing at a CAGR of approximately 7.96%.

Demand in the U.S. market is driven by federal government cloud security requirements including FedRAMP High authorisation, IL4 and IL5 classified data handling standards, and the intelligence community’s IC-compliant cloud infrastructure requirements whose procurement defines the most demanding national sovereign cloud standards in any market globally. State and local government sovereign cloud adoption is growing as jurisdictions implement their own data localisation policies for citizen data, public safety records, and critical infrastructure management systems.

E2E Cloud announced the launch of its Sovereign Cloud Platform in March 2025, giving enterprises, governments, and data centres full control over their digital infrastructure. This development signals the growing commercial market for sovereign cloud solutions beyond the hyperscaler ecosystem as specialist providers build niche sovereign infrastructure that addresses the specific control and operational independence requirements that standard hyperscaler sovereign offerings do not fully satisfy for the most demanding regulated enterprise and government customers.

Sovereign Cloud Market Segment Analysis

-

By Deployment, the Cloud segment dominated the Sovereign Cloud Market with 57.40% share in 2025, while the On-Premise segment is the fastest growing at a CAGR of 32.10%.

-

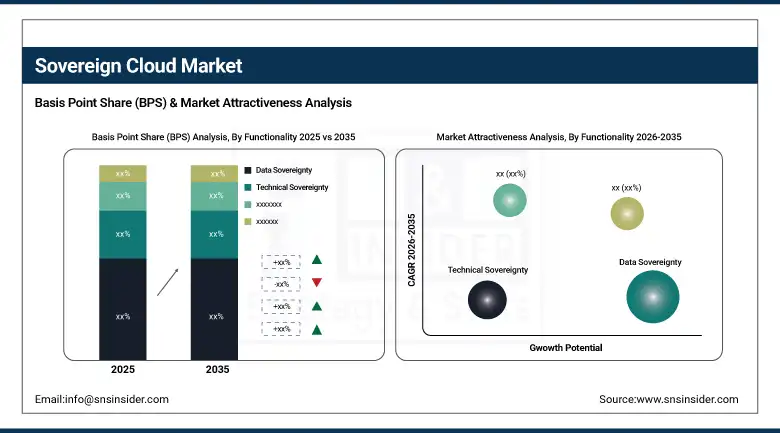

By Functionality, the Data Sovereignty segment dominated the Sovereign Cloud Market with 48.90% share in 2025, while the Technical Sovereignty segment is the fastest growing at a CAGR of 30.50%.

-

By Enterprise Size, the Large Enterprises segment dominated the Sovereign Cloud Market with 53.60% share in 2025, while the SMEs segment is the fastest growing.

-

By End Use, the Government & Public Sector segment dominated the Sovereign Cloud Market in 2025, while the Healthcare segment is the fastest growing.

By Functionality, data sovereignty dominates, technical sovereignty grows fastest

Data sovereignty retained the dominant functionality position with 48.90% of the sovereign cloud market in 2025. The commercial primacy of data sovereignty reflects its foundational legal and regulatory standing as the baseline requirement that every sovereign cloud deployment must satisfy before any additional technical or operational sovereignty consideration becomes commercially relevant. Data sovereignty ensures that data is stored, processed, and governed within a specific national jurisdiction under that nation’s legal framework, making it directly accessible to domestic legal authorities and inaccessible to foreign governments without the host nation’s consent.

Technical sovereignty is the fastest-growing functionality at a CAGR of 30.50% through 2035 because the most sophisticated government and enterprise customers are progressively recognising that data sovereignty alone is insufficient for achieving genuine independence from foreign cloud vendor control.

By End Use, government dominates, healthcare grows fastest

Government and public sector retained the dominant end use position in the sovereign cloud market in 2025, reflecting the foundational truth that sovereign cloud as a product category exists primarily to address the unique data governance, jurisdictional control, and operational independence requirements that national governments impose on their own critical systems and on the regulated entities operating under their jurisdiction. Government agencies across defence, intelligence, tax administration, welfare services, and national security operate with data sensitivity levels and sovereignty requirements that standard public cloud architectures cannot contractually satisfy, creating both the original commercial demand for sovereign cloud and the procurement specifications that define the category’s technical standards.

Healthcare is the fastest-growing end use segment in the sovereign cloud market because the convergence of digital health transformation, personal health information sensitivity, and progressive healthcare data regulation is creating sovereign cloud requirements in a sector that previously relied on on-premises data centres for sensitive workload isolation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

India |

32.6% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Sovereign Cloud Market Insights

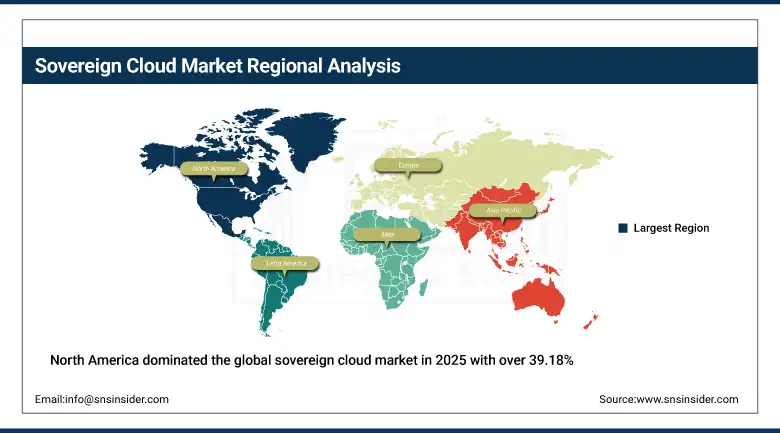

North America dominated the global sovereign cloud market in 2025 with over 39.18% of global revenues, with the United States accounting for approximately 87.4% of North American revenues. The region’s market leadership is anchored by the federal government’s sophisticated cloud security certification infrastructure, the concentration of the world’s leading hyperscaler companies whose sovereign cloud product lines define global technical standards, and the defence and intelligence community’s sovereign cloud investment whose procurement requirements drive the most technically demanding sovereign cloud platform development.

Canada contributes approximately 12.6% of North American revenues through its federal government’s Protected B data classification requirements, provincial government data residency policies for citizen information, and the RCMP and national security community’s sovereign cloud requirements whose combined procurement is creating growing commercial demand for Canadian-controlled cloud infrastructure that meets the government’s evolving data sovereignty standards.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Sovereign Cloud Market Insights

Europe is the most commercially sophisticated sovereign cloud market outside North America, where the GDPR’s data protection requirements, the EU AI Act’s governance framework, and national data localisation policies across France, Germany, the UK, and the Nordic countries collectively create the most comprehensive regulatory environment for sovereign cloud procurement in any global region.

Germany accounts for approximately 22.3% of European revenues through its Bundescloud programme for federal government agencies, BSI’s C5 cloud security certification framework, and the Deutsche Telekom-Microsoft partnership that created the sovereign T-Systems managed cloud whose contractual model provides Azure capabilities within a German-controlled operational entity.

Asia Pacific Sovereign Cloud Market Insights

Asia Pacific is the fastest-growing regional sovereign cloud market, driven by India’s Digital Personal Data Protection Act’s data localisation requirements, China’s comprehensive data security and cross-border data transfer regulations, Singapore’s financial sector data governance framework, and Southeast Asian nations’ progressive adoption of cloud data sovereignty policies that increasingly restrict sensitive data processing to nationally controlled cloud infrastructure.

India accounts for approximately 32.6% of Asia Pacific revenues through its combination of a massive public sector digital transformation programme whose data sovereignty requirements are creating large-scale sovereign cloud procurement, the private sector’s compliance with DPDPA localisation requirements, and Civo’s launch of India’s first sovereign cloud based in Mumbai in December 2024.

MEA & Latin America Sovereign Cloud Market Insights

The Middle East and Africa and Latin America are growing sovereign cloud markets where government digitisation investment, national data protection legislation, and sovereign nations’ strategic interest in controlling the digital infrastructure underlying their critical government and economic systems are creating structured demand for sovereign cloud platforms whose data residency and operational control credentials satisfy national sovereignty requirements.

Saudi Arabia leads MEA revenues at approximately 38.4% of the regional total through Vision 2030’s ambitious digital government transformation programme, the National Data Management Office’s data localisation requirements, and NEOM’s smart city infrastructure whose cloud foundation requires sovereign-compliant architecture operated under Saudi jurisdictional control.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its LGPD data protection legislation’s data localisation implications, the federal government’s Governo Digital programme whose sovereign cloud requirements are shaping public sector cloud procurement, and the financial sector’s BACEN data residency requirements for financial data processed within Brazilian jurisdiction.

Market Dynamics

Growth Drivers: Government data localisation legislation creating compliance-driven procurement

Government data localisation legislation is the most structurally certain commercial growth driver in the sovereign cloud market, as each national data protection law enacted creates a compliance-driven procurement requirement that organisations operating in the relevant jurisdiction must satisfy regardless of their preference for standard public cloud cost and simplicity advantages. The progressive proliferation of data localisation requirements across the EU, India, China, Saudi Arabia, and Southeast Asia is collectively creating an expanding addressable sovereign cloud market whose geographic scope grows with each legislative development. Unlike discretionary technology investment decisions, compliance-driven cloud procurement is mandated rather than elective, creating demand that persists through economic cycle variation.

Restraints: Higher cost of sovereign cloud infrastructure relative to standard public cloud and technical complexity of sovereign cloud migration from legacy on-premises environments

Sovereign cloud infrastructure’s higher unit cost relative to standard public cloud alternatives is the most commercially significant adoption barrier for cost-sensitive enterprise and government customers whose procurement decisions must balance compliance requirements against total technology investment budgets. The dedicated or partitioned infrastructure that genuine sovereignty requires cannot achieve the same unit economics as the massively shared global infrastructure whose scale advantages define standard public cloud cost leadership. This premium can be 20 to 40% above standard cloud pricing depending on sovereignty depth, creating procurement approval complexity in budget-constrained government departments and SMEs.

The limited depth of AI, analytics, and developer platform services available in sovereign cloud environments relative to standard public cloud alternatives creates a capability gap that constrains the advanced workloads that sovereign cloud customers can run within their compliance boundary. Governments and enterprises that require both sovereignty compliance and access to cutting-edge AI capabilities face a genuine trade-off whose resolution requires either accepting capability limitations within sovereign boundaries or developing hybrid architectures that separate sovereign and non-sovereign workloads across different cloud environments with associated integration complexity.

Opportunities: Defence and intelligence community sovereign AI investmentmand emerging market government digital transformation creating first-time sovereign cloud programmes

Defence and intelligence community sovereign AI represents the most commercially valuable near-term sovereign cloud opportunity as governments globally recognise that AI systems trained on and operating across classified and sensitive national security data require the most stringent sovereign cloud controls that standard hyperscaler environments cannot provide. The U.S. DoD’s classified AI infrastructure investment, NATO alliance members’ sovereign AI programme development, and India’s defence technology modernisation are each creating specialist sovereign cloud requirements whose technical specifications and procurement values substantially exceed standard government cloud contracts.

Emerging market government digital transformation is creating a large and growing first-time sovereign cloud programme development opportunity as governments in Southeast Asia, Africa, and Latin America execute public sector digitisation investments whose data sovereignty requirements from inception provide sovereign cloud providers with greenfield opportunities to build national cloud infrastructure rather than competing to displace established alternative approaches. These greenfield deployments represent the most commercially accessible sovereign cloud market entry opportunities for both regional providers and global hyperscalers seeking to establish early sovereign market position.

Recent Developments:

-

2025: Microsoft extended its Cloud for Sovereignty initiative across additional European government markets in 2025, adding enhanced confidential computing capabilities, locally managed encryption key infrastructure, and government-specific compliance documentation that enables EU public sector organisations to deploy Azure services with verifiable data sovereignty controls satisfying national regulatory requirements including France’s SecNumCloud and Germany’s BSI C5 frameworks.

-

2025: E2E Cloud launched its Sovereign Cloud Platform in March 2025, providing enterprises, governments, and data centre operators with full control over digital infrastructure through an operator-independent sovereign architecture that addresses data sovereignty concerns without dependence on hyperscaler contractual commitments, targeting the enterprise segment seeking absolute operational control beyond what hyperscaler sovereign programme offerings provide.

-

2024: Civo launched India’s dedicated sovereign cloud platform in December 2024, based in Mumbai, providing Indian enterprises and government customers with cloud services operated exclusively within Indian jurisdiction under Indian legal governance, directly addressing the Digital Personal Data Protection Act’s data localisation requirements and establishing a commercially significant specialist sovereign infrastructure alternative to hyperscaler India region deployments for the most compliance-sensitive Indian data workloads.

Sovereign Cloud Market Key Players

-

Microsoft

-

Amazon Web Services

-

Google Cloud

-

IBM

-

Oracle

-

SAP

-

OVHcloud

-

T-Systems

-

Atos

-

Thales

-

Orange Business Services

-

Capgemini

-

Alibaba Cloud

-

Huawei Cloud

-

E2E Cloud

-

Civo

-

Rackspace Technology

-

VMware

-

Accenture

-

Deutsche Telekom

Sovereign Cloud Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 111.41 Billion |

| Market Size by 2035 | USD 1603.41 Billion |

| CAGR | CAGR of 30.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment (Cloud, On-Premise) • By Functionality (Data Sovereignty, Technical Sovereignty, Operational Sovereignty) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By End Use (Government & Public Sector, Defense & Intelligence, BFSI, Healthcare, Telecommunications, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Microsoft, Amazon Web Services, Google Cloud, IBM, Oracle, SAP, OVHcloud, T-Systems, Atos, Thales, Orange Business Services, Capgemini, Alibaba Cloud, Huawei Cloud, E2E, Cloud, Civo, Rackspace Technology, VMware, Accenture, Deutsche Telekom |

Frequently Asked Questions

Get in Touch