Surgical Robots Market Report Scope & Overview:

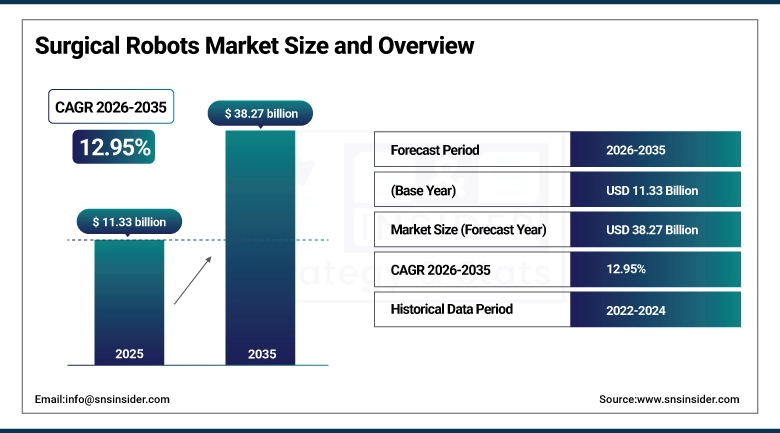

The Surgical Robots Market size was estimated at USD 11.33 billion in 2025 and is expected to reach USD 38.27 billion by 2035 and grow at a CAGR of 12.95% over the forecast period of 2026-2035.

The surgical robots market is witnessing robust growth owing to the rising adoption of minimally invasive procedures, innovations in technology among robotic surgery systems and demand for accurate surgical outcomes. Robotics have clearly made great strides in orthopedic, urological, gynecological and neurological surgeries; resulting in increased surgical efficiency, fewer complications and decreased recovery times.

Robotic technology is being increasingly adopted by hospitals and health organizations to create more accurate medical procedures while minimizing waste in the operating room. Furthermore, the growing number of chronic diseases, an aging population and a digitalization of surgery have all played an important role in driving up the adoption of robotics within healthcare markets on a global scale.

For instance, in June 2024, a study published in The Lancet Digital Health analyzing over 1,800 cases reported that robotic-assisted surgeries improved precision by 85% and reduced intraoperative variability by nearly 30%, highlighting enhanced procedural consistency

Surgical Robots Market Size and Forecast:

-

Market Size in 2025: USD 11.33 billion

-

Market Size by 2035: USD 38.27 billion

-

CAGR: 12.95% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Surgical Robots Market - Request Free Sample Report

Surgical Robots Market Trends

-

Increasing adoption of robotic-assisted surgical systems driven by growing demand for minimally invasive procedures and improved patient outcomes across multiple specialties.

-

Continuous advancements in robotic technology, including enhanced visualization, haptic feedback, and AI-enabled decision support systems, improving surgical precision and efficiency.

-

Rising integration of robotic platforms with imaging technologies and navigation systems to enable real-time surgical guidance and accuracy.

-

Expansion of robotic-assisted procedures beyond traditional applications into complex surgeries such as oncology, cardiothoracic, and neurosurgical interventions.

-

Growing investment by hospitals and healthcare providers in next-generation robotic systems to streamline workflows and enhance operating room productivity.

-

Increasing focus on surgeon training programs and simulation platforms to improve proficiency and accelerate adoption of robotic surgical techniques.

-

Strengthening regulatory approvals and product innovations by key market players contributing to broader accessibility and commercialization of surgical robotics.

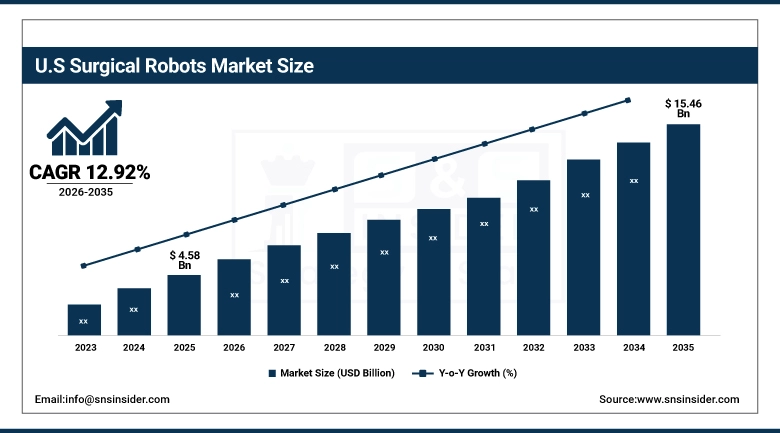

The U.S. Surgical Robots Market was valued at USD 4.58 billion in 2025 and is projected to reach USD 15.46 billion by 2035, growing at a CAGR of 12.92% from 2026–2035. The USA is leading in the surgical robots industry across the globe due to the developed healthcare infrastructure in the nation and the high level of use of minimally invasive surgical procedures.

Factors contributing to the growth include rapid adoption by leading robotic system providers, good payment systems and high demand in precision surgery. Moreover, a solid hospital framework already exists, and robotic surgical systems are gaining in significance as an avenue for providing patient safety and enhanced functional results.

Surgical Robots Market Growth Drivers:

-

Increasing Preference for Minimally Invasive Procedures is Accelerating the Surgical Robots Market Expansion

The adoption of minimally invasive surgical procedures is seen as one of the major structural drivers in the robotics surgery market. The use of robotic technology in surgery is associated with a decline in complications ranging from 15% to 30%, a decrease in hospital stays of up to 20% to 50%, and faster recovery periods than conventional surgery methods.

Robots enhance the skills of the surgeon by reducing tremors, amplifying motion, and offering high-resolution stereoscopic images, all of which enable efficient functioning in confined anatomical areas. This is particularly true for surgery in urology, such as prostatectomy, in gynecology, and complex orthopedic procedures. In addition, increased patient knowledge and expectations have resulted in a trend toward robotic surgery as an edge over other facilities.

For instance, in July 2024, a multi-center randomized clinical study published in JAMA Surgery reported that robotic-assisted procedures reduced complication rates by over 22% compared to conventional open surgeries, while also improving postoperative recovery metrics.

Surgical Robots Market Restraints:

-

High Acquisition Costs and Operational Complexities are Limiting the Surgical Robots Market Penetration

The deployment of robotic systems in surgery remains hindered primarily by expensive upfront payments ranging between USD 1.5 million and USD 3 million, coupled with maintenance and disposables costs on an annual basis. Such prohibitive costs remain a huge challenge in particular for mid-sized facilities in pricing-sensitive markets.

In addition to limitations imposed by finances, practical issues also hinder the adoption process. The need for extensive training for the surgeons, who require up to 20 to 50 supervised operations, and problems with incorporating new processes, and longer surgery times in the beginning, are some of the factors that contribute to the delay.

The interrelated problems of funding and implementation continue to prevent widespread acceptance, particularly in developing countries with under-resourced health care systems.

Surgical Robots Market Opportunities:

-

Technological Advancements and Expansion into Emerging Markets are Creating New Growth Avenues for the Surgical Robots Market

The next step in market growth is expected to be driven by technological advances and geographic diversification. Technologies such as AI-based autonomy, real-time tissue discrimination, and haptic feedback (force-feedback) have increased accuracy in surgery and lessened the dependence on human skill.

Simultaneously, the organizations are exercising cost-optimization strategies such as modular robots and reusable instruments to make them more affordable and useful for implementation in developing countries that comprise India, China, and Southeast Asia. The growth of ambulatory surgical centers and outpatient surgery is another reason for the demand for these cost-effective robotic devices.

For instance, in May 2024, a leading medical device manufacturer introduced a modular robotic platform that reduced system costs by approximately 30%, enabling deployment across secondary hospitals and outpatient surgical facilities.

Surgical Robots Market Segment Analysis

-

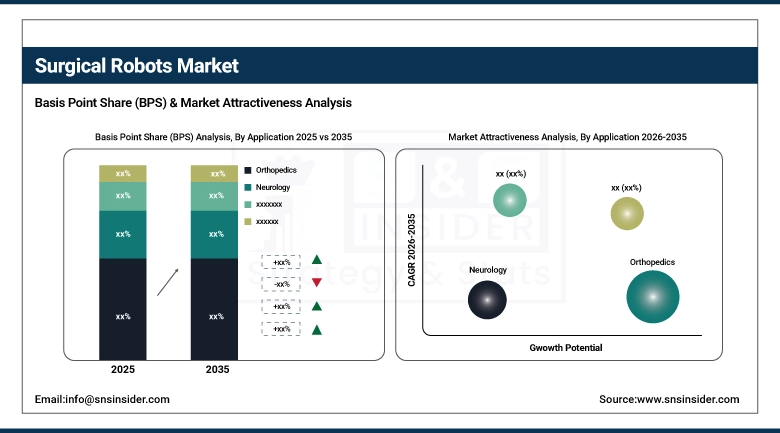

By application, orthopedics accounted for the largest share of approximately 41.62% in 2025, while the neurology segment is expected to register the fastest growth with a CAGR of 13.48%.

-

By end-use, inpatient settings dominated the market with nearly 63.85% share in 2025, whereas outpatient settings are anticipated to witness the highest growth with a CAGR of 13.21%.

By Application, Orthopedics Leads the Market, While Neurology Emerges as the Fastest Growing Segment

Orthopedics stands out due to the high number of joint replacement operations and the criticality of implant placement precision. Orthopedic robotic systems facilitate the planning of the operation based on the individual anatomy of the patient and adjusting the implant placement during surgery.

On the other hand, the neurology submarket is witnessing a surge in demand owing to the increasing need for accurate brain and spinal surgery treatments. This has been made possible by the integration of robotics and imaging technology in neurosurgery operations.

By End-Use, Inpatient Segment Dominates, While Outpatient Segment Registers Rapid Growth

These facilities remain at the forefront due to their capability of accommodating expensive capital investments, managing intricate surgeries, and coordinating multi-specialty surgical teams. Moreover, a positive payment model and high number of patients contribute to greater acceptance within inpatient facilities.

There are growing numbers of outpatient centers due to increasing demand for surgeries that release patients within the same day and also cost-effective surgical systems. It is also believed that the introduction of smaller robots for ambulatory centers will increase acceptance in this sector even more.

Surgical Robots Market Regional Highlights:

North America Surgical Robots Market Insights:

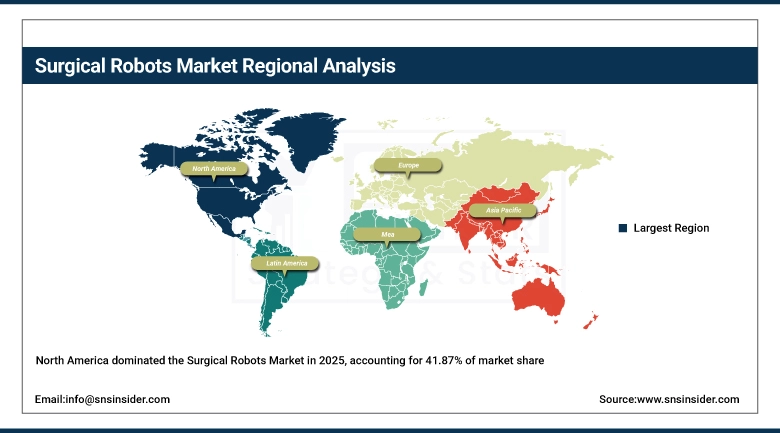

North America had the leading position within the surgical robots market in 2025, capturing around 41.87% of the total market value. That domination is predicated on not only an advanced healthcare infrastructure and significant capital investment but also rapid adoption of the latest robotic-assisted surgical technology. From North America perspective, due to presence of advanced types of equipment suppliers, affirmative insurance policies and high number of minimally invasive procedures the USA is recognized as the most prominent growth engine. Underpinned by an equally strong regulatory and clinical research environment within this treatment space, North America will continue to lead over the 2026-2035 forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Surgical Robots Market Insights:

Asia Pacific is expected to exhibit the fastest CAGR of 12.95%. The rapid development of healthcare infrastructure, increased expenditure on healthcare services and increase in the demand for advanced surgical solutions in developing economies such as China, India, Japan and South Korea are some of the key factors that are expected to fuel the growth. Digital health initiatives promoted by governments, and the building of advanced hospitals, are driving the adoption rate of robots in surgeries. More patients, medical tourism and heightened awareness about minimal invasion surgery are also contributing to strong regional momentum.

Europe Surgical Robots Market Insights:

Europe constitutes the second largest market due to its robust healthcare systems and constant improvement of surgical technologies. Countries in Europe are adopting more robotics technology, with the top countries in this sector being Germany, the UK, France and Italy for use of these systems including urology, gynecology and orthopedics. Decentralization of the EU has been marked with further growth potential, namely through the formation of a consolidated healthcare system via aligning regulations, investing in medical innovation and modernizing hospitals.

Latin America (LATAM) and Middle East & Africa (MEA) Surgical Robots Market Insights:

LATAM and MEA are developing economies that demonstrate steady growth due to consistent investments in healthcare facilities and surgical capacity. Prominent among such adoption efforts are the ones taking place in Brazil, Mexico, UAE, and Saudi Arabia, supported by increased availability of quality health care and greater investments from both the public and private sides. Private hospital chains along with a focus on superior surgical practices play significant roles. Moreover, the rise of medical tourism along with government-led efforts toward healthcare reforms will positively affect revenues until 2035.

Surgical Robots Market Competitive Landscape:

Intuitive Surgical Inc., which was incorporated in 1995, is still dominating the market in robotically-assisted surgical systems. The Da Vinci surgical system by Intuitive Surgical sets the trend for the whole industry due to its sophisticated imaging, precision instruments, and information management capabilities.

-

In February 2025: Intuitive Surgical launched an upgraded da Vinci system featuring enhanced visualization and AI-enabled workflow optimization, improving surgical precision and operational efficiency across North America and Europe.

Stryker Corporation, established in 1941, is one of the key players in the orthopedic surgical robotics industry. The company uses the Mako Smart Robotics technology for executing the data-based, customized joint replacement surgery. In doing so, it strengthens its position in the rapidly growing orthopedic sector through the combination of robotic execution and pre-op analysis.

-

In March 2025: Stryker Corporation enhanced the Mako platform with next-generation software and real-time intraoperative data capabilities, strengthening clinical outcomes and surgeon adoption.

Zimmer Biomet Holdings, Inc., founded in 1927, is a firm player in the market of robotics-assisted orthopedic treatments, providing the ROSA system. This device can be used for surgery in knees, hips, and neurosurgery, which shows the company’s dedication to implementing the technology of big data into surgical processes and expanding.

-

In November 2025: Zimmer Biomet launched the ROSA Knee with OptimiZe upgrade, integrating advanced analytics and real-time surgical insights to improve intraoperative decision-making and procedural accuracy.

Surgical Robots Market Key Players:

-

Intuitive Surgical, Inc.

-

Stryker Corporation

-

Zimmer Biomet Holdings, Inc.

-

Medtronic plc

-

Smith & Nephew plc

-

Johnson & Johnson (Ethicon)

-

Asensus Surgical, Inc.

-

CMR Surgical Ltd.

-

Vicarious Surgical Inc.

-

Moon Surgical

-

Medicaroid Corporation

-

Corindus, Inc. (Siemens Healthineers)

-

Titan Medical Inc.

-

Virtual Incision Corporation

-

Meerecompany Inc.

-

MicroPort Scientific Corporation

-

Think Surgical, Inc.

-

Distalmotion SA

-

Avatera Medical GmbH

-

Hansen Medical (Auris Health)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.33 Billion |

| Market Size by 2035 | USD 38.27 Billion |

| CAGR | CAGR of 12.95% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application [Orthopedics (Knee, Hip, Spine, Others), Neurology, Urology, Gynecology, Others] • By End-use [Inpatient, Outpatient] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Intuitive Surgical, Inc., Stryker Corporation, Zimmer Biomet Holdings, Inc., Medtronic plc, Smith & Nephew plc, Johnson & Johnson (Ethicon), Asensus Surgical, Inc., CMR Surgical Ltd., Vicarious Surgical Inc., Moon Surgical, Medicaroid Corporation, Corindus, Inc. (Siemens Healthineers), Titan Medical Inc., Virtual Incision Corporation, Meerecompany Inc., MicroPort Scientific Corporation, Think Surgical, Inc., Distalmotion SA, Avatera Medical GmbH, Hansen Medical (Auris Health) |

Frequently Asked Questions

Ans: The Surgical Robots Market is expanding due to increasing demand for minimally invasive procedures, rising chronic disease burden, and continuous technological advancements. Improved surgical precision, reduced complications, and faster recovery times are key factors accelerating adoption globally.

Ans: The Surgical Robots Market is expected to grow from USD 11.33 billion in 2025 to USD 38.27 billion by 2035, registering a CAGR of 12.95% during the forecast period from 2026 to 2035.

Ans: In the Surgical Robots Market, orthopedics holds the largest share due to the high volume of joint replacement procedures and the need for precise implant positioning. Meanwhile, neurology is emerging as the fastest-growing segment.

Ans: The Surgical Robots Market faces challenges such as high initial investment costs, expensive maintenance, and the need for extensive surgeon training. These factors can limit adoption, especially in cost-sensitive and developing regions.

Ans: North America leads the Surgical Robots Market, driven by advanced healthcare infrastructure, strong reimbursement systems, and high adoption of robotic-assisted surgeries, particularly in the United States.

Get in Touch