STEM Education In K-12 Market Report Scope and Overview:

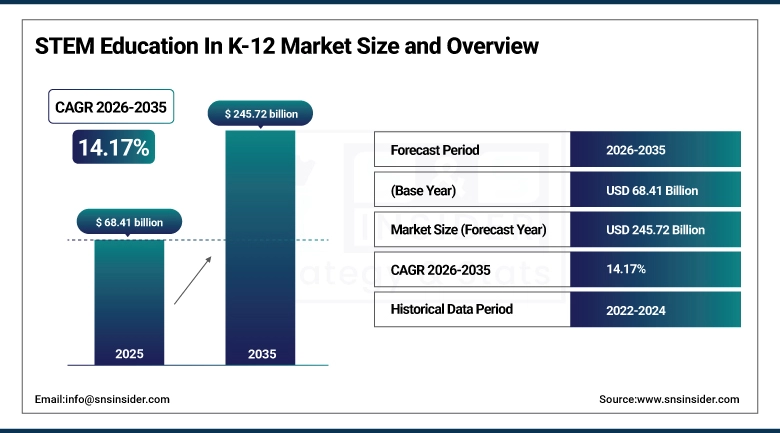

The STEM Education In K-12 Market was valued at USD 68.41 billion in 2025 and is expected to reach USD 245.72 billion by 2035, growing at a CAGR of 14.17% from 2026-2035.

The market growth for STEM Education In K-12 can be witnessed at a very fast pace due to increasing demands for technically adept professionals of the future generation. Moreover, the implementation of technologies such as artificial intelligence and robots is further adding momentum to market growth. Efforts from both educational institutes and governments, along with those by EdTech companies, are aimed at increasing the number of students enrolled in STEM curriculum in primary and secondary schools.

Adaptive learning software programs, virtual lab experiments, gamified learning solutions, coding programs, robotics kits, and so forth have revolutionized the education industry for K-12 students.

STEM Education In K-12 Market Size and Forecast

-

Market Size in 2025: USD 68.41 Billion

-

Market Size by 2035: USD 245.72 Billion

-

CAGR: 14.17% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on STEM Education In K-12 Market - Request Free Sample Report

STEM Education In K-12 Market Trends

-

The development of adaptive learning systems driven by artificial intelligence within the K-12 learning landscape.

-

The utilization of robotics, programming, and computational skills development courses.

-

The incorporation of augmented and virtual reality tools and virtual science labs.

-

The integration of cloud computing and hybrid STEM learning solutions.

-

Government support from the federal government to build smart classrooms and STEM innovation laboratories.

-

The emphasis on creating equal opportunities for females in STEM education.

-

The importance of project-based learning and practical experiences.

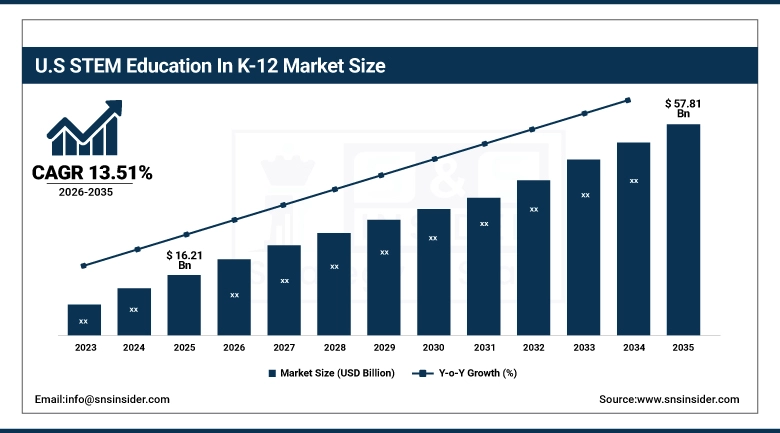

U.S. STEM Education In K-12 Market was valued at USD 16.21 billion in 2025 and is expected to reach USD 57.81 billion by 2035, growing at a CAGR of 13.51%.

The U.S., on the other hand, remains the leader in the market share in the region due to the availability of a well-developed educational technology platform, adoption of advanced learning technologies, and active participation of the government towards the implementation of STEM reforms. There is an increasing demand for engineers, experts in artificial intelligence and robotics, and cyber security specialists.

STEM Education In K-12 Market Segment Analysis

-

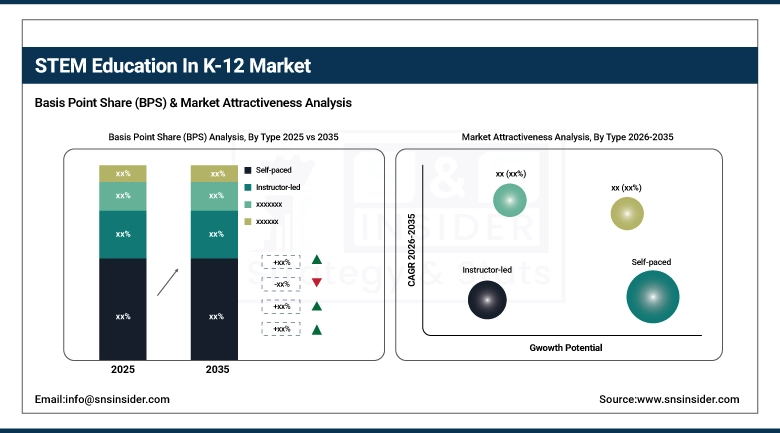

Based on type, Self-paced dominated the market in 2025 with approximately 71.2% revenue share, while Instructor-led are expected to witness the fastest growth during the forecast period.

-

Based on Application, High School (9–12) accounted for nearly 43.1% market share in 2025, while Middle School (6–8) are expected to witness the fastest growth during the forecast period.

By Type, Self-Paced Learning Leads STEM Education in K-12 Market, While Instructor-Led Segment Grows Rapidly

The Self-paced segment captured the largest market share of approximately 71.2% during 2025 in the STEM Education in K-12 market because of its flexibility and scalability. The students learn at their own pace, thus ensuring better comprehension of the subject matter, particularly when dealing with complex subjects like science, technology, engineering, and mathematics. Moreover, it is also adaptable to a variety of e-learning systems, caters to different learning styles, and reduces the reliance on teacher presence. Moreover, the schools have found that self-paced STEM education programs are quite economical and easy to incorporate into the academic schedule.

However, the Instructor-led segment will experience the highest CAGR of about 15.87% from 2026 to 2035 as a result of the personal attention offered by teachers to students and instant feedback. Due to the increasing focus of schools on delivering top-quality STEM education, there has been an increasing need for talented teachers, which makes the demand for instructor-led courses go up.

By Application, High School Segment Dominates STEM Education Market, Middle School Segment Shows Fastest Growth

The High School (9-12) segment was leading the STEM Education in K-12 market with the largest revenue share of around 43.1% in 2025 as the increased emphasis on preparing students for their future career paths and college admission programs was driving the growth of the segment. The students at this level get interested in advanced STEM subjects such as calculus, physics, coding, and other related areas. Moreover, educational institutions are concentrating on students at this level to help them prepare better for their upcoming college education and tech-based careers through dedicated courses and laboratories.

The Middle School (6-8) segment is forecasted to exhibit the fastest CAGR of around 15.60% during the forecast period, 2026-2035, on account of the rising emphasis on the early adoption of STEM education. Educational institutes, policymakers, and teachers are focusing on students at this level as they believe that early exposure to STEM education will play an important role in creating future interest in STEM fields.

STEM Education In K-12 Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~78% |

|

Europe |

United Kingdom |

~22% |

|

Asia Pacific |

China |

~41% |

|

Middle East and Africa |

UAE |

~31% |

|

Latin America |

Brazil |

~45% |

North America STEM Education In K-12 Market Insights

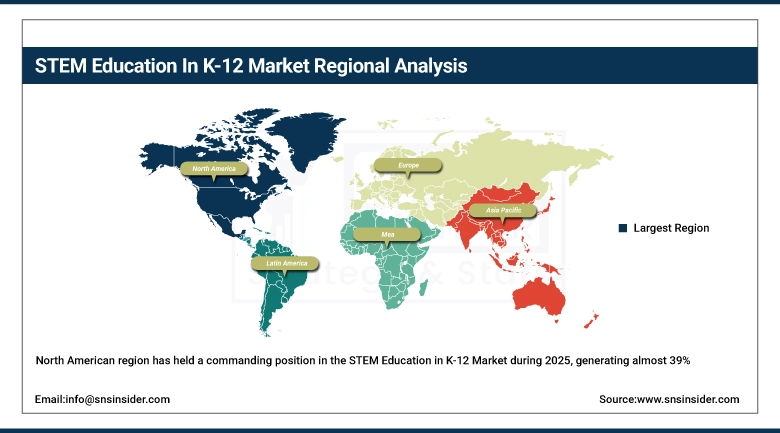

The North American region has held a commanding position in the STEM Education in K-12 Market during 2025, generating almost 39% of total revenue globally, attributed to superior digital learning systems, heavy investments in educational technologies, and active government policies related to STEM workforce development in both the United States and Canada. Growing utilization of AI-powered learning modules, coding training courses, robotics laboratories, and interactive STEM curricula is driving market dynamics in K-12 institutions across both the private and public sectors. National campaigns promoting computer science education, engineering literacy, and future-oriented workforce skills have encouraged greater investments in STEM-oriented learning environments. Growing usage of gamification techniques, virtual laboratories, cloud-based educational services, and practical science lessons is adding fuel to growing participation in K-12 STEM activities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific STEM Education In K-12 Market Insights

The Asia-Pacific region is expected to register the highest CAGR in the Global STEM Education in K-12 Market from 2026 to 2035 owing to widespread acceptance of digital education solutions, STEM education initiatives backed by the government, and increasing investments made in smart classroom infrastructures within China, India, Japan, South Korea, and Southeast Asia. The governments in these countries are focusing on improving literacy in STEM subjects, coding education, robotics instruction, and updating AI-based curricula in order to improve the competiveness of their future labor force. There has been high adoption of digital solutions for STEM education in China and India due to increased availability of the internet, higher expenditure by the middle class on education, and a greater number of jobs in technological fields.

Europe STEM Education In K-12 Market Insights

Europe enjoys a solid standing in the worldwide STEM Education in K-12 Market owing to rising governmental spending on the digital learning revolution, superior public education infrastructure, and a greater emphasis on innovation-oriented skill training in Germany, the UK, France, and Nordic nations. European educational bodies are promoting coding skills, engineering studies, sustainability sciences, and AI-powered learning methods within the K-12 curricula. Digital education projects and smart classroom upgrade programs financed by the EU are facilitating the deployment of STEM-centric e-learning tools, robotics kits, and virtual laboratories. The UK and Germany continue to be important markets in the region thanks to their high penetration of ed-tech products and favorable institutional environment for technical education.

Latin America STEM Education In K-12 Market Insights

The uptake of STEM Education in the K-12 Market is increasing in Latin America on account of the increase in investments made towards digital learning, improved connectivity to the internet, and the improvement in science and technology literacy in countries like Brazil, Mexico, Argentina, and Colombia. Adoption of online STEM platforms, coding education, robotics contests, and other interactive digital learning tools to help engage students and improve their technical capabilities is becoming common practice in educational institutions and schools. Brazil is currently the leading country in the region with regards to the uptake of STEM Education owing to increased adoption of EdTech solutions and digital learning initiatives undertaken by the public sector.

Middle East & Africa STEM Education In K-12 Market Insights

The Middle East and Africa region is witnessing rising demand for the STEM Education in K-12 Market, driven by increased investment from local governments toward digital infrastructure for education, smart learning, and technology-enhanced curriculum development in UAE, Saudi Arabia, and South Africa. The regional governments are increasingly focusing on STEM education to promote economic diversification and foster innovation capabilities in the region. UAE and Saudi Arabia are at the forefront of the regional market owing to the presence of national digital education initiatives and AI-based learning programs, as well as the installation of smart classrooms in both public and private schools in the country. Higher demand for coding classes, robotics training programs, and digital learning platforms that focus on science subjects will contribute to the growing demand in the coming years.Bottom of Form

Market Growth Drivers:

-

Rising demand for digital learning, coding education, and future workforce skill development

With increasing demand for jobs that require proficiency in artificial intelligence, robotics, engineering, data science, and advanced manufacturing, it has become increasingly evident that there is an understanding of the critical role of STEM education on the part of government agencies, educational organizations, and parents. Because of changes brought about by the digital revolution in many sectors, the need for training in coding and computational abilities among young children at elementary, middle, and high schools has skyrocketed. The use of smart classrooms, virtual laboratories, robotics devices, games, and AI-based systems has been incredibly useful in generating interest among students in STEM fields.

Market Restraints:

-

Limited digital infrastructure and shortage of trained STEM educators in developing regions

Even with the advances made by educational technology in recent years, there are many schools that find themselves at a disadvantage due to lack of adequate technological resources, unreliable internet services, and restricted access to advanced methods of STEM education. Insufficient budgetary allocations as well as inadequate distribution of educational materials prevent the full exploitation of robotic laboratories, programming software, and other practical means of teaching science. In addition, the problem of insufficient supply of STEM instructors and training of teachers persists in a number of developing nations.

Market Opportunities:

-

AI-driven personalized learning and virtual STEM platforms creating long-term growth opportunities

The use of artificial intelligence, adaptive learning technologies, and cloud-based e-learning platforms is generating numerous opportunities for the worldwide market for STEM Education in K-12. Artificial intelligence can help in making personalized learning material, student performance analysis, and customized STEM learning paths that match individual strengths. Further innovations in the form of growing adoption of AR, VR, and immersive science simulations are revolutionizing the classroom learning process. Growth in the use of online STEM tutoring services, coding camps, makerspaces, and digital learning ecosystems will drive growth in the global market over the forecast period.

Recent Developments:

-

2026: Google for Education extended its range of AI-based STEM classroom learning tools by incorporating generative AI learning and coding assistance features along with interactive science simulations for the benefit of K-12 organizations across the world.

-

2025: Microsoft Education launched new Copilot-based STEM learning solutions for personalized coding guidance, mathematics coaching via AI, and cloud-based collaborative science learning platforms in schools and digital classrooms.

STEM Education In K-12 Market Key Players

Some of the STEM Education In K-12 Market Companies

• Activate Learning

• Amplify Education, Inc.

• Bedford, Freeman & Worth Publishing Group, LLC

• Carolina Biological Supply Company

• Cengage Learning

• Discovery Education

• EduCo International

• Houghton Mifflin Harcourt

• Kendall Hunt Publishing Company

• Lab-Aids

• McGraw Hill

• OpenSciEd

• PASCO Scientific

• Savvas Learning

• School Specialty, LLC

• Vernier Software & Technology

• LEGO Education

• Pearson Education

• STEMfinity

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 68.41 Billion |

| Market Size by 2035 | USD 245.72 Billion |

| CAGR | CAGR of 14.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Self-paced, Instructor-led) • By Application (Elementary School (K-5), Middle School (6-8), High School (9-12)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Activate Learning, Amplify Education, Inc., Bedford, Freeman & Worth Publishing Group, LLC, Carolina Biological Supply Company, Cengage Learning, Discovery Education, EduCo International, Houghton Mifflin Harcourt, Kendall Hunt Publishing Company, Lab-Aids, McGraw Hill, OpenSciEd, PASCO Scientific, Savvas Learning, School Specialty, LLC, Vernier Software & Technology, LEGO Education, Pearson Education, STEMfinity |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 16.5% in the STEM Education In K-12 Market.

High School (9–12) dominated with approximately 43.1% share in 2025.

Self-paced held approximately 71.2% share in 2025.

The STEM Education In K-12 Market was valued at USD 68.41 Billion in 2025.

The STEM Education In K-12 Market is expected to grow at a CAGR of 14.17% from 2026 to 2035.

Get in Touch