Nasal Spray Market Report Scope & Overview:

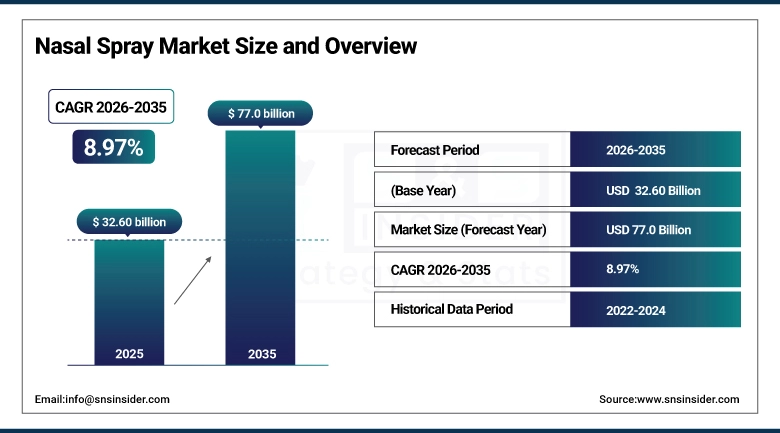

The Nasal Spray Market was estimated at USD 32.60 billion in 2025 and is expected to reach USD 77.0 billion by 2035 and grow at a CAGR of 8.97% over the forecast period of 2026-2035.

The global nasal spray market is experiencing robust and broad-based growth, driven by the convergence of escalating respiratory allergy prevalence, advancing intranasal drug delivery technology, and a structural consumer preference shift toward non-invasive, self-administered therapeutic formats. Nasal sprays have evolved far beyond simple congestion relief to become a versatile, clinically validated delivery platform for corticosteroids, antihistamines, decongestants, saline irrigation, vaccines, hormones, and increasingly for central nervous system (CNS) drugs — with the intranasal route's unique advantages of rapid onset, avoidance of first-pass hepatic metabolism, and direct CNS access positioning it as a premium drug delivery pathway for an expanding range of therapeutic applications. Allergic rhinitis affects more than 400 million people globally and impacts approximately 30% of the U.S. population, establishing a massive chronic patient base with ongoing demand for nasal spray therapy. The post-pandemic era has further heightened consumer awareness for nasal hygiene and respiratory health. This accelerates the adoption of saline irrigation products and contributing to the broader normalisation of regular nasal spray use across all demographic groups.

The Nasal Spray Market's 8.97% CAGR from 2026 to 2035 reflects the structural convergence of a global respiratory disease burden, the intranasal delivery platform's expanding therapeutic application landscape — from allergy management to CNS drug delivery and vaccine administration — and the accelerating consumer preference for convenient, non-invasive, self-administered healthcare solutions that deliver rapid, localised relief without the systemic side effects associated with oral or injectable therapeutic alternatives.

Market Size and Forecast

• Market Size in 2025: USD 32.60 Billion

• Market Size by 2035: USD 77.0 Billion

• CAGR: 8.97% from 2026 to 2035

• Base Year: 2025

• Forecast Period: 2026–2035

• Historical Data: 2022–2024

To Get more information on Nasal Spray Market - Request Free Sample Report

Nasal Spray Market Trends

• Accelerating development of intranasal CNS drug delivery platforms — including nasal naloxone (Narcan), intranasal esketamine (Spravato) for treatment-resistant depression, and pipeline candidates for Alzheimer's disease and Parkinson's — expanding the nasal spray market well beyond traditional respiratory applications into high-value neurological therapeutic categories.

• Rising adoption of preservative-free nasal spray formulations, driven by clinical evidence linking preservatives to nasal mucosa irritation, growing patient preference for well-tolerated long-term therapy formulations, and major manufacturer investment in preservative-free product launches.

• Expanding use of nasal spray as a vaccine delivery route — with intranasal influenza vaccines and pipeline candidates for respiratory syncytial virus (RSV), COVID-19, and other pathogens — offering needle-free administration advantages that improve acceptance rates particularly among paediatric and needle-averse populations.

• Growing market penetration of generic nasal spray products — including Lupin's FDA-cleared generic Atrovent (ipratropium) nasal spray — that are expanding patient access and driving prescription volume growth in established therapeutic categories.

• Rapid expansion of the saline nasal irrigation segment, driven by growing consumer awareness of nasal hygiene, rising use among allergy sufferers and post-surgical patients, and strong OTC sales growth through retail pharmacy and e-commerce channels.

• Increasing innovation in metered-dose pump design, actuator geometry, and particle size engineering that optimise nasal spray deposition profiles, improve drug bioavailability, and reduce oropharyngeal deposition for improved therapeutic efficacy and patient tolerance.

• Rising self-medication trend fuelled by consumer preferences for OTC management of mild-to-moderate nasal allergy and congestion symptoms, supported by the availability of highly effective OTC corticosteroid and antihistamine nasal sprays across pharmacy and online channels.

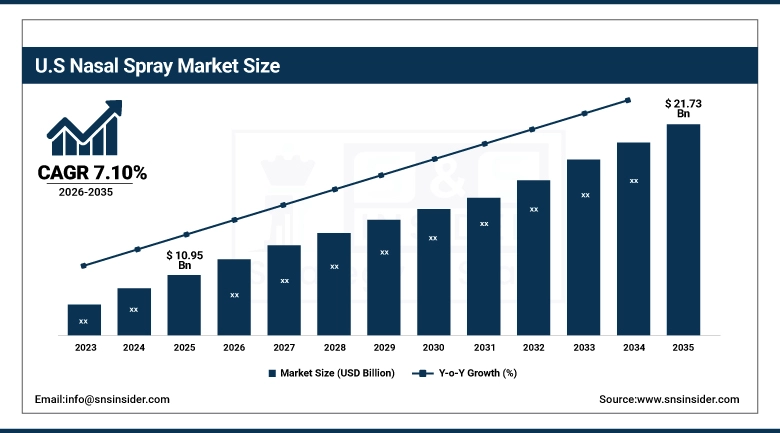

U.S. Nasal Spray Market was valued at USD 10.95 billion in 2025 and is expected to reach USD 21.73 billion by 2035, registering a CAGR of 7.10% during 2026–2035.

The USA is the largest market for nasal sprays due to its high per capita healthcare spending, high incidence of allergic rhinitis in the country where more than 50 million people suffer each year, an advanced market for over-the-counter drugs that makes it possible for patients to obtain nasal sprays with corticosteroids and antihistamines over-the-counter, and a highly dynamic regulatory environment for new nasal drug delivery systems. The U.S. market is favored by high medical support of intranasal corticosteroids as a preferred treatment for allergic rhinitis from leading medical institutions such as Mayo Clinic and Mount Sinai. Important commercial factors influencing the market include patent expirations of key brands resulting in an increase in the share of generics, switching of prescription-only nasal corticosteroid sprays to OTC products, and introduction of innovative intranasal therapies in the areas of central nervous system and vaccines that will provide premium revenues throughout the forecast period.

Lupin's February 2025 FDA clearance for generic Atrovent nasal spray — targeting the prescription anticholinergic rhinitis market — exemplifies the ongoing genericisation wave that is expanding nasal spray market volume by making established therapies more accessible to price-sensitive patient populations, while simultaneously stimulating branded manufacturers to invest in next-generation formulations, novel intranasal delivery systems, and new therapeutic indication development to maintain premium market positioning.

Nasal Spray Market Segment Analysis

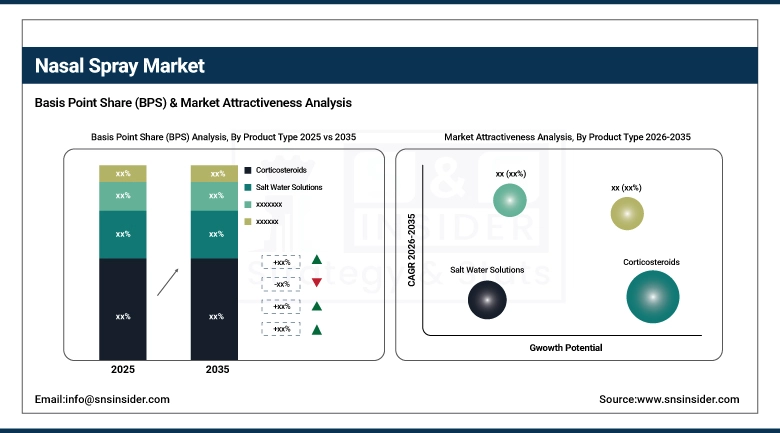

• Based on Product Type, Corticosteroid Nasal Sprays accounted for the largest market share in 2025; CNS/Specialty Intranasal products expected to be the fastest-growing segment (CAGR).

• Based on Application, Allergic Rhinitis accounted for the largest market share in 2025; CNS Disorders expected to be the fastest-growing application segment (CAGR).

• Based on Distribution Channel, Retail Pharmacy/Drug Stores accounted for the largest market share (~48%) in 2025; Online Pharmacy expected to be the fastest-growing distribution channel (CAGR).

By Product Type: Corticosteroids dominate, CNS/Specialty grows at fastest CAGR

In the Nasal Spray Market in 2025, corticosteroid nasal sprays had a commanding market share, owing to their well-established efficacy as the best pharmacological agent in treating allergic rhinitis, chronic sinusitis, and nasal polyps. Intranasal corticosteroids such as fluticasone propionate, mometasone furoate, budesonide, and triamcinolone acetonide offer robust, localized anti-inflammatory effects while having low systemic bioavailability. This has made them the go-to choice of treatment for all major rhinitis guidelines. Over-the-counter formulations of popular corticosteroid products such as Flonase (fluticasone) and Nasacort (triamcinolone) have enabled a large section of patients to treat rhinitis without consulting doctors.

CNS and specialty intranasal therapeutics are projected to register the highest CAGR through 2035, driven by the rapidly expanding clinical validation of intranasal delivery for neurological drug candidates that benefit from the direct nose-to-brain transport pathway. The success story of Spravato (esketamine) nasal spray in treatment-resistant depression and the upcoming intranasal products for Alzheimer’s disease, Parkinson’s disease, migraines, and opioid overdose rescue have proven to be lucrative areas in drug discovery. They are transforming the nasal spray market into a diverse drug delivery platform that is no longer confined to respiratory drugs but commands premium pricing.

By Application: Nasal Congestion dominates, Allergic Rhinitis grows at fastest CAGR

In 2025, Nasal Congestion held the largest share of the Nasal Spray Market due to the widespread occurrence of the common cold, sinusitis, respiratory ailments, and seasonal flu across the globe. Decongestants are commonly used in nasal spray formulations to offer quick relief from blocked nasal passages, improve breathing ease, and relieve sinus pressure. Growing pollution, fluctuating climatic conditions, and increasing cases of respiratory disorders have fueled the demand for this segment. The easy availability of nasal sprays and consumer inclination toward self-treatment have driven market acceptance.

Allergic Rhinitis is expected to witness the fastest CAGR during 2026–2035 owing to the increasing prevalence of allergies triggered by dust, pollen, pollution, and environmental allergens. Rising awareness regarding preventive allergy management and growing use of corticosteroid and antihistamine nasal sprays are accelerating segment growth globally.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

38% |

|

Europe |

Germany |

31% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

UAE |

28% |

|

Latin America |

Brazil |

44% |

North America Nasal Spray Market Insights

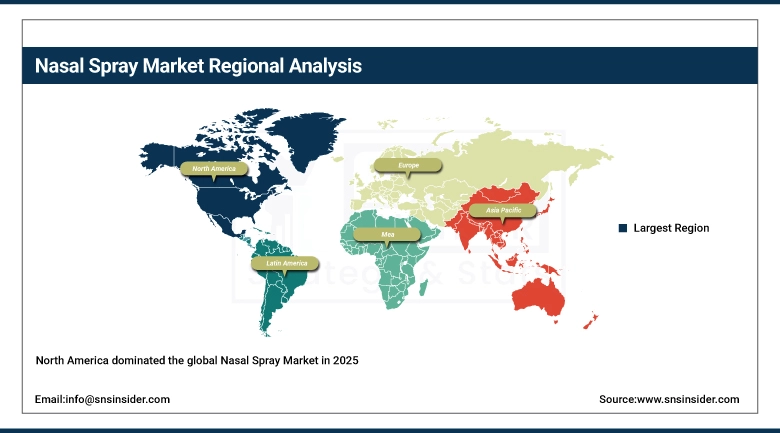

North America dominated the global Nasal Spray Market in 2025, supported by favourable reimbursement frameworks, well-established healthcare infrastructure, and early acceptance of novel intranasal drug delivery systems. The United States is the largest market contributor, underpinned by high allergic rhinitis prevalence, a robust OTC pharmaceutical market, and one of the world's most active regulatory pipelines for intranasal therapeutics. Canada contributes through strong provincial healthcare coverage for prescription nasal spray products and growing OTC market penetration.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Nasal Spray Market Insights

The Asia Pacific region will have the highest regional growth up until 2035, owing to increasing urban pollution and its effects on respiratory allergies, diagnosis of allergic rhinitis and sinusitis in China, India, Japan, and Southeast Asia, and increased access to healthcare and OTC pharmaceuticals in developing nations. The growth in China will be high due to increased local production of pharmaceuticals and investment in healthcare, whereas growth in India will be due to the development of online pharmaceutical companies and children suffering from allergies.

Europe Nasal Spray Market Insights

Europe represents a mature and significant nasal spray market, supported by comprehensive national health system coverage for prescription corticosteroid sprays, sophisticated allergist clinical networks, and strong pharmaceutical manufacturing presence across Germany, France, the UK, and Switzerland. European market growth is being driven by expanding generic nasal spray penetration, growing OTC market development, and increasing clinical adoption of novel intranasal CNS therapeutics.

Middle East & Africa and Latin America Nasal Spray Market Insights

MEA and Latin America are growing nasal spray markets, supported by rising allergic disease prevalence driven by urbanisation, pollution, and climate change, improving pharmacy retail infrastructure, and expanding OTC pharmaceutical market penetration.

Brazil leads Latin American revenues with approximately 44% of regional share, supported by strong domestic pharmaceutical industry capacity and widespread retail pharmacy distribution. The UAE leads MEA adoption through its advanced healthcare system and high-income consumer base with strong OTC pharmaceutical purchasing capacity.

Nasal Spray Market Growth Drivers:

Rising global respiratory allergy burden and expanding intranasal therapeutic application landscape

The primary structural growth driver for the Nasal Spray Market is the escalating global burden of allergic respiratory diseases with allergic rhinitis alone affecting more than 400 million people globally and increasing annually due to climate change extending pollen seasons, rising urban air pollution intensifying allergen exposure, and growing population sensitisation rates combined with the expanding range of therapeutic conditions for which intranasal delivery offers clinical advantages. Each new approved intranasal therapeutic indication from CNS disorders to vaccine delivery broadens the market's total addressable opportunity and creates new high-value commercial frontiers that sustain the market's 8.97% CAGR through 2035.

Bayer and Johnson & Johnson's joint announcement at the World Allergy Organization (WAO) congress of a preservative-free nasal spray formulation for chronic rhinitis, specifically designed to reduce side effects and improve long-term treatment compliance reflects the patient-centric innovation imperative driving nasal spray product development, where improving tolerability and adherence in chronic-use conditions is the key commercial differentiator that sustains branded product market share against accelerating generic competition through the forecast period.

Nasal Spray Market Restraints

Rebound congestion risk, side effect concerns with long-term use, and competition from alternative delivery modalities

A meaningful restraint on the Nasal Spray Market is the well-documented risk of rhinitis medicamentosa rebound nasal congestion from prolonged decongestant nasal spray use. It has led to clinical guidelines recommending decongestant spray use limitations and creates patient hesitancy around extended nasal spray use. The prolonged usage of a corticosteroid nasal spray leads to patients having concerns regarding possible steroid side effects, although there is extensive clinical safety data supporting its efficacy. Competing with other forms of medications such as antihistamine pills, sublingual immunotherapy, and nasal steroid drops offers alternate routes of treatment to certain patients. Moreover, the sophistication involved in engineering nasal sprays and the technique required in administering the spray properly can reduce its efficiency if not explained to the patient properly.

Nasal Spray Market Opportunities

Intranasal CNS therapeutics, nasal vaccine delivery, and emerging market OTC expansion

The development of intranasal CNS therapeutics — leveraging the nose-to-brain delivery pathway for neurological conditions including Alzheimer's disease, Parkinson's disease, anxiety, and depression — represents the most transformative long-term innovation opportunity in the nasal spray market, with the potential to command premium pharmaceutical pricing and access patient populations currently underserved by oral and injectable CNS drug formulations. Intranasal vaccine delivery represents a compelling public health opportunity where needle-free administration, improved mucosal immunity generation, and simpler cold-chain logistics relative to injectable vaccines create a strong case for expanded nasal vaccine development and deployment. The vast and underpenetrated OTC nasal spray market across Asia Pacific, Latin America, and Africa — combined with expanding retail pharmacy and e-commerce distribution networks — offers substantial long-term volume growth opportunities for manufacturers able to develop cost-competitive, locally adapted OTC product portfolios through 2035.

Recent Developments:

• 2026: Hikma Pharmaceuticals expanded its generic nasal spray portfolio in the U.S. market with new approvals targeting allergic rhinitis and nasal congestion treatment segments.

• 2026: Cipla Limited strengthened its respiratory product pipeline by increasing production capacity for corticosteroid and saline nasal spray formulations across emerging markets.

• 2026: Neurelis, Inc. advanced commercialization of its intranasal neurological therapy platforms, supporting broader adoption of precision nasal drug delivery technologies in specialty pharmaceutical applications.

Nasal Spray Market Key Players

• GlaxoSmithKline plc (GSK)

• AstraZeneca PLC

• Novartis AG

• Johnson & Johnson

• Bayer AG

• Viatris Inc.

• Cipla Ltd.

• Procter & Gamble Co.

• Emergent BioSolutions

• Aurena Laboratories AB

• Aytu Health

• Lupin Limited

• Teva Pharmaceutical Industries

• Sanofi S.A.

• Pfizer Inc.

• Merck & Co., Inc.

• NeilMed Pharmaceuticals Inc.

• Neurelis, Inc.

• Hikma Pharmaceuticals PLC

• Bausch Health Companies Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 32.60 Billion |

| Market Size by 2035 | USD 77.0 Billion |

| CAGR | CAGR of 8.97% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Corticosteroid Nasal Sprays, Antihistamine Nasal Sprays, Decongestant Nasal Sprays, Saline/Nasal Irrigation Sprays, Others) • By Application (Allergic Rhinitis, Nasal Congestion, Sinusitis, CNS Disorders, Vaccination, Others) • By Distribution Channel (Retail Pharmacy/Drug Stores, Hospital Pharmacy, Online Pharmacy) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | GlaxoSmithKline plc (GSK), AstraZeneca PLC, Novartis AG, Johnson & Johnson, Bayer AG, Viatris Inc., Cipla Ltd., Procter & Gamble Co., Emergent BioSolutions, Aurena Laboratories AB, Aytu Health, Lupin Limited, Teva Pharmaceutical Industries, Sanofi S.A., Pfizer Inc., Merck & Co., Inc., NeilMed Pharmaceuticals Inc., Neurelis, Inc., Hikma Pharmaceuticals PLC, Bausch Health Companies Inc. |

Frequently Asked Questions

Ans: North America dominated the Nasal Spray Market in 2025, anchored by the United States with its high allergic rhinitis prevalence, well-established OTC pharmaceutical market infrastructure, favourable reimbursement frameworks, and one of the world's most active regulatory pipelines for novel intranasal therapeutic approvals.

Ans: Corticosteroid nasal sprays dominated the market in 2025, driven by their clinical validation as first-line therapy for allergic rhinitis and chronic sinusitis, strong physician prescription rates, and broad OTC availability that collectively drive high prescription and consumer purchase volumes.

Ans: Rising global prevalence of allergic rhinitis affecting over 400 million people, combined with the expanding intranasal drug delivery application landscape encompassing CNS therapeutics, vaccine delivery, and hormonal formulations, and accelerating consumer adoption of OTC nasal spray products, are the primary structural growth drivers through 2035.

Ans: The Nasal Spray Market was valued at USD 32.60 billion in 2025.

Ans: The Nasal Spray Market is expected to grow at a CAGR of 8.97% from 2026 to 2035.

Get in Touch