Synthetic Ester Lubricants for the Telecommunications Market Report Scope & Overview:

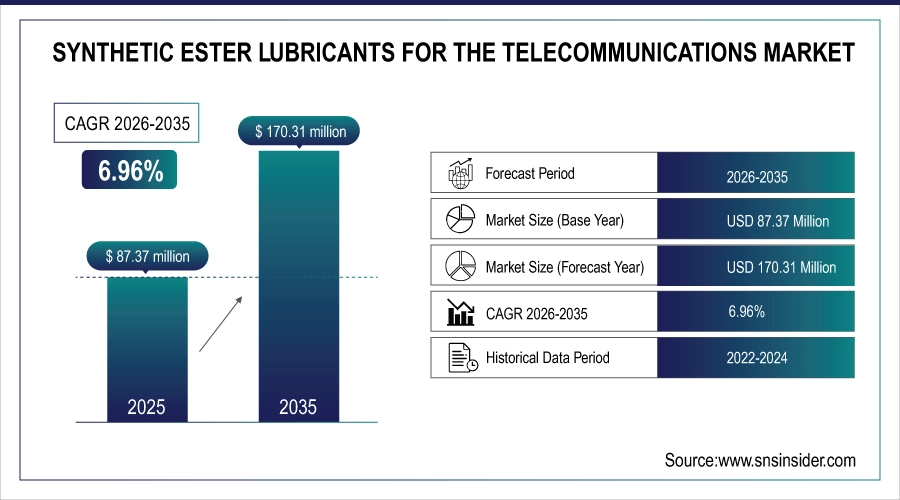

The Synthetic Ester Lubricants for the Telecommunications Market size was valued at USD 87.37 Million in 2025 and is projected to reach USD 170.31 Million by 2035, growing at a CAGR of 6.96% during 2026-2035.

The Synthetic Ester Lubricants for the Telecommunications Market is growing due to rapid expansion of 5G networks, increasing deployment of telecom towers and base stations, and rising demand for reliable thermal management in high-density equipment. Growth in data centers, edge computing, and power backup systems further supports adoption. Synthetic ester lubricants offer superior thermal stability, dielectric performance, long service life, and environmental benefits, making them well-suited for modern telecom infrastructure operating under harsh and continuous conditions.

Market Size and Forecast:

-

Market Size in 2025: USD 87.37 Million

-

Market Size by 2035: USD 170.31 Million

-

CAGR: 6.96% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Synthetic Ester Lubricants for the Telecommunications Market - Request Free Sample Report

Key Synthetic Ester Lubricants for the Telecommunications Market Trends

-

Rapid 5G network deployment and expansion of telecom infrastructure driving higher demand for advanced lubricants.

-

Increasing adoption of synthetic ester lubricants in cooling systems, power backup units, and high-load telecom equipment.

-

Growth of data centers and edge computing facilities fueling the need for thermally stable and dielectric-efficient lubricants.

-

Rising focus on sustainability, biodegradability, and low-toxicity ester formulations in response to environmental regulations.

-

Innovation in lubricant chemistry and strategic partnerships with OEMs enabling tailored solutions for next-generation telecom equipment.

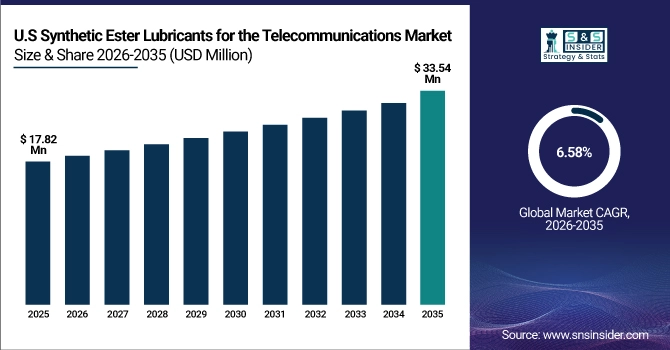

The U.S. Synthetic Ester Lubricants for the Telecommunications Market size was valued at USD 17.82 Million in 2025 and is projected to reach USD 33.54 Million by 2035, growing at a CAGR of 6.58% during 2026-2035. The U.S. Synthetic Ester Lubricants for the Telecommunications Market is growing due to expanding 5G infrastructure, increased data center deployment, and demand for high-performance, thermally stable lubricants that enhance equipment reliability and energy efficiency in telecom networks.

Synthetic Ester Lubricants for the Telecommunications Market Growth Drivers:

-

5G Expansion and Data Center Growth Drive Global Synthetic Ester Lubricant Demand in Telecom Networks

The global Synthetic Ester Lubricants for the Telecommunications Market is primarily driven by the rapid rollout of advanced network technologies such as 5G and the accelerating build-out of telecom infrastructure worldwide. As telecom operators expand base stations, small cells, and edge computing facilities, the demand for high-performance lubricants that offer superior thermal stability, dielectric strength, and oxidation resistance increases. These lubricants are essential for cooling systems, power backup units (UPS and generators), and other critical components that operate under high loads and elevated temperatures. Additionally, the proliferation of data centers to support cloud services, IoT devices, and bandwidth-intensive applications intensifies the need for synthetic ester formulations that maintain performance under continuous operation. Environmental and regulatory pressures are also steering industry preference toward biodegradable, low-toxicity esters over conventional mineral oils, further bolstering market growth.

Global 5G connections reached 2.25 billion worldwide by the end of 2024, growing four times faster than 4G at a similar stage. Total global 5G networks reached 354 commercial deployments by early 2025.

Synthetic Ester Lubricants for the Telecommunications Market Restraints:

-

Awareness Gaps and Compatibility Challenges Limit Synthetic Ester Lubricant Adoption in Telecom Infrastructure

Key restraints include limited awareness of synthetic ester lubricant benefits among smaller telecom operators, compatibility challenges with legacy equipment, and stringent qualification requirements from telecom OEMs. Performance validation timelines are long, slowing adoption. Additionally, supply chain dependency on specialized raw materials and limited standardization across telecom applications can restrict faster market penetration.

Synthetic Ester Lubricants for the Telecommunications Market Opportunities:

-

Emerging Markets and Sustainable Innovations Propel Synthetic Ester Lubricant Demand Across Global Telecom Networks

Significant opportunities lie in emerging economies across Asia Pacific, Latin America, and Africa, where expanding telecommunications networks and digital infrastructure investments are creating new demand pockets. Innovation in lubricant chemistry, including tailored blends for specific telecom equipment and enhanced heat transfer properties, presents avenues for product differentiation and premium positioning. Partnerships between lubricant manufacturers and telecom OEMs can accelerate adoption through co-engineered solutions optimized for next-generation equipment. Furthermore, growing focus on sustainability and circular economy initiatives offers potential for eco-friendly ester products to capture market share, especially among enterprises with stringent environmental goals. As telecom networks evolve toward higher frequencies and greater energy densities, demand for advanced synthetic ester lubricants is expected to strengthen over the next decade.

Asia-Pacific remains a major driver of telecom infrastructure investment, with the region capturing about $117 billion of the $244 billion annual global mobile investment landscape in 2025

Synthetic Ester Lubricants for the Telecommunications Market Segment Analysis

-

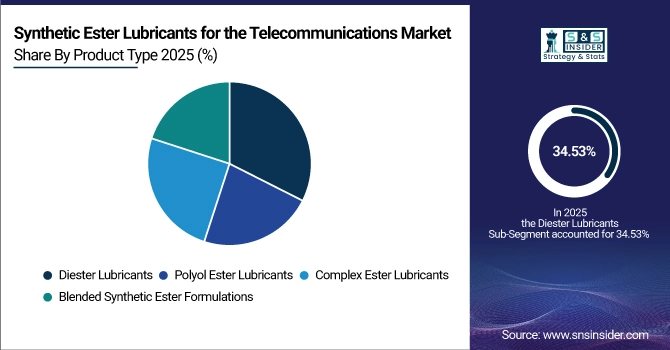

By Product Type, Diester Lubricants dominated with 34.53% in 2025, and Complex Ester Lubricants is expected to grow at the fastest CAGR of 7.62% from 2026 to 2035.

-

By Application, Cooling Systems & Thermal Management dominated with 36.12% in 2025, and it is expected to grow at the fastest CAGR of 7.30% from 2026 to 2035.

-

By Equipment Type, Telecom Towers & Base Transceiver Stations (BTS) dominated with 34.23% in 2025, and Data Centers & Network Switching Equipment is expected to grow at the fastest CAGR of 7.32% from 2026 to 2035.

-

By End-User, Telecom Network Operators dominated with 37.24% in 2025, Data Center Operators is expected to grow at the fastest CAGR of 7.37% from 2026 to 2035.

By Product Type, Diester Lubricants Lead Market While Advanced Ester Formulations Gain Traction in Next Generation Telecom Infrastructure

Diester lubricants remained the leading product type in 2025 due to their proven thermal stability, good lubricity, and compatibility with a wide range of telecom equipment. They are widely used in base stations, power systems, and cooling applications where reliable performance under continuous operation is essential. Moving into the 2026–2035 period, increasing focus on higher-temperature operations, longer drain intervals, and improved oxidative stability is driving interest in advanced ester chemistries. This evolution supports broader adoption of complex ester formulations in next-generation telecom infrastructure.

By Application, Advanced Cooling Solutions Drive Synthetic Ester Lubricant Demand as Telecom Networks Expand Rapidly by 2035

Cooling systems and thermal management applications led demand in 2025, supported by rising heat loads from dense network equipment, 5G radios, and expanding data center operations. Synthetic ester lubricants play a critical role in maintaining temperature stability, improving heat transfer efficiency, and reducing equipment failure risks. From 2026 to 2035, increasing deployment of edge data centers, small cells, and high-frequency network components is expected to further elevate the importance of advanced cooling and thermal management solutions across global telecom networks.

By Equipment Type, Telecom Towers Lead Equipment Lubricant Demand While Data Centers Drive Next Generation Network Growth

Telecom towers and base transceiver stations (BTS) represented the most significant equipment category in 2025, driven by large installed bases and continuous expansion of mobile network coverage. These assets require dependable lubrication for power systems, cooling units, and auxiliary equipment operating in harsh outdoor environments. During the 2026–2035 timeframe, growth momentum is expected to shift toward data centers and network switching equipment, as cloud computing, AI workloads, and high-speed data traffic place greater operational demands on centralized and edge network infrastructure.

By End-User Industry, Telecom Operators Lead Lubricant Demand as Data Centers Drive Growth and Innovation by 2035

Telecom network operators were the primary end users in 2025, reflecting their responsibility for maintaining extensive networks of towers, base stations, and power backup systems. Their focus on uptime, reliability, and long equipment life supports consistent use of high-performance synthetic ester lubricants. Looking ahead to 2026–2035, data center operators are becoming increasingly influential end users as digital transformation accelerates. Rising demand for energy-efficient, thermally stable, and environmentally compliant solutions is strengthening lubricant adoption across large-scale and edge data center facilities.

Synthetic Ester Lubricants for the Telecommunications Market Report Analysis

Asia Pacific Synthetic Ester Lubricants for the Telecommunications Market Insights

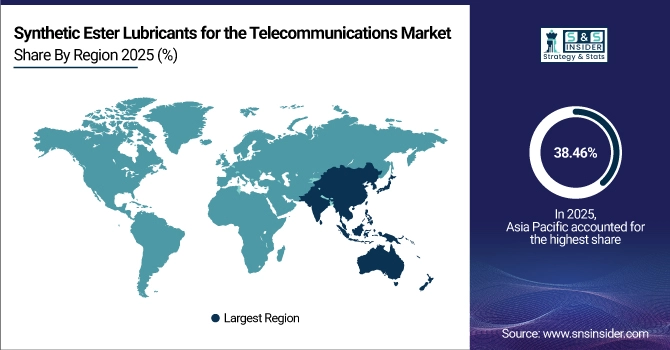

Asia Pacific dominated the global Synthetic Ester Lubricants for the Telecommunications Market with 38.46% share in 2025, driven by rapid expansion of telecom infrastructure across China, India, Japan, and Southeast Asia. Large-scale 5G rollouts, rising mobile data consumption, and increasing deployment of telecom towers and data centers are key growth enablers. The region is also expected to grow at the fastest CAGR of 7.36% from 2026 to 2035, supported by ongoing digitalization, government-backed connectivity initiatives, and growing demand for reliable, high-performance, and thermally stable lubricant solutions in telecom networks.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Synthetic Ester Lubricants for the Telecommunications Market Insights

North America accounted for 26.24% of the global Synthetic Ester Lubricants for the Telecommunications Market in 2025, supported by a well-established telecom infrastructure and early adoption of advanced technologies. The region benefits from widespread deployment of 5G networks, expansion of hyperscale and edge data centers, and strong demand for reliable thermal management and power backup solutions. The presence of major telecom operators, data center providers, and lubricant manufacturers further supports market growth. Stringent environmental regulations are also encouraging the adoption of high-performance, low-toxicity synthetic ester lubricants across telecom applications.

U.S. Synthetic Ester Lubricants for the Telecommunications Market Insights

The United States dominated the North American Synthetic Ester Lubricants for the Telecommunications Market in 2025, driven by extensive 5G deployment, large-scale data center investments, and a high concentration of telecom operators and infrastructure providers requiring advanced thermal management and power system lubrication solutions.

Europe Synthetic Ester Lubricants for the Telecommunications Market Insights

Europe held 21.86% of the global Synthetic Ester Lubricants for the Telecommunications Market in 2025, supported by advanced telecom infrastructure and strong regulatory emphasis on sustainability. Ongoing 5G rollouts, modernization of legacy networks, and increasing deployment of data centers across Western and Northern Europe are driving demand. Telecom operators are increasingly adopting synthetic ester lubricants for improved thermal stability, equipment reliability, and environmental compliance. Strict EU regulations on biodegradability and low toxicity are accelerating the shift toward synthetic ester formulations in telecom cooling systems, power backup units, and network equipment.

Germany Synthetic Ester Lubricants for the Telecommunications Market Insights

Germany dominated the European Synthetic Ester Lubricants for the Telecommunications Market in 2025 due to extensive 5G network deployment, strong industrial and data center presence, and strict environmental regulations encouraging the adoption of high-performance, biodegradable lubricant solutions across telecom infrastructure.

China Synthetic Ester Lubricants for the Telecommunications Market Insights

China dominated the Asia Pacific Synthetic Ester Lubricants for the Telecommunications Market in 2025 due to massive 5G base station deployment, extensive fiber network expansion, strong government support for digital infrastructure, and large-scale investments in data centers and telecom equipment manufacturing.

Latin America (LATAM) and Middle East & Africa (MEA) Synthetic Ester Lubricants for the Telecommunications Market Insights

Latin America and the Middle East & Africa represent emerging markets for synthetic ester lubricants in telecommunications, driven by expanding mobile networks, rising 4G and 5G deployments, and increasing investments in digital infrastructure. Growth is supported by new telecom towers, modernization of legacy networks, and rising demand for reliable power backup systems in remote locations. Increasing data center development, improving connectivity initiatives, and growing awareness of equipment reliability and environmental compliance are further strengthening adoption across both regions.

Competitive Landscape for Synthetic Ester Lubricants for the Telecommunications Market:

Exxon Mobil Corporation is a global leader in energy and specialty chemicals, producing high-performance synthetic ester lubricants used in telecommunications infrastructure. Its products provide superior thermal stability, oxidation resistance, and dielectric performance, supporting reliable operation of base stations, data centers, and power backup systems worldwide.

-

In September 2025, ExxonMobil fires up new lubricant and fuel units at its Singapore complex, expanding production capacity for higher‑value lubricant base stocks, including synthetic products, to meet customer demand in Asia‑Pacific.

Royal Dutch Shell plc is a major global energy and petrochemicals company that develops advanced synthetic lubricant and specialty fluid solutions. Its high‑performance synthetic esters support cooling, thermal management, and reliability in telecommunications infrastructure, addressing demanding network environments and evolving digital connectivity needs worldwide.

-

In June 2025, Shell introduced Shell DLC Fluid S3, a specialized direct liquid cooling solution designed to meet demands of high‑performance computing and data center thermal management.

Synthetic Ester Lubricants for the Telecommunications Market Key Players:

-

Exxon Mobil Corporation

-

Royal Dutch Shell plc

-

Chevron Corporation

-

BP p.l.c.

-

Fuchs SE

-

Sinopec Limited

-

Valvoline Inc.

-

AMSOIL Inc.

-

Phillips 66

-

Idemitsu Kosan Co., Ltd.

-

The Lubrizol Corporation

-

BASF SE

-

Repsol SA

-

Petroliam Nasional Berhad (PETRONAS)

-

ENEOS Corporation

-

NYCO S.A.

-

INEOS Group

-

Savita Oil Technologies Limited

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 87.37 Million |

| Market Size by 2035 | USD 170.31 Million |

| CAGR | CAGR of 6.96% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Diester Lubricants, Polyol Ester Lubricants, Complex Ester Lubricants, and Blended Synthetic Ester Formulations) • By Application (Base Station Equipment Lubrication, Cooling Systems & Thermal Management, Cable & Connector Protection, and Power Backup Systems (Generators, UPS)) • By Equipment Type (Telecom Towers & Base Transceiver Stations (BTS), Data Centers & Network Switching Equipment, Optical Fiber & Cable Infrastructure, and Power and Energy Storage Systems) • By End-User (Telecom Network Operators, Data Center Operators, Telecom Equipment Manufacturers, and Infrastructure Service Providers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Exxon Mobil Corporation, Shell plc, TotalEnergies SE, Chevron Corporation, BP plc, FUCHS SE, Sinopec Limited, Valvoline Inc., AMSOIL Inc., Phillips 66, Idemitsu Kosan Co., Ltd., The Lubrizol Corporation, Croda International Plc, BASF SE, Repsol S.A., PETRONAS, ENEOS Corporation, NYCO S.A., INEOS Group, Savita Oil Technologies Limited |

Frequently Asked Questions

Asia Pacific dominated the Synthetic Ester Lubricants for the Telecommunications Market in 2025.

Diester Lubricants dominated the Synthetic Ester Lubricants for the Telecommunications Market.

The key drivers are rapid 5G network expansion, growing data center deployment, and rising demand for high-performance, thermally stable, and environmentally friendly lubricants in telecom infrastructure.

The Synthetic Ester Lubricants for the Telecommunications Market size was USD 87.37 Million in 2025 and is expected to reach USD 170.31 Million by 2035.

The Synthetic Ester Lubricants for the Telecommunications Market is expected to grow at a CAGR of 6.96% from 2026-2035.

Get in Touch