Teleprotection Market Size & Trends:

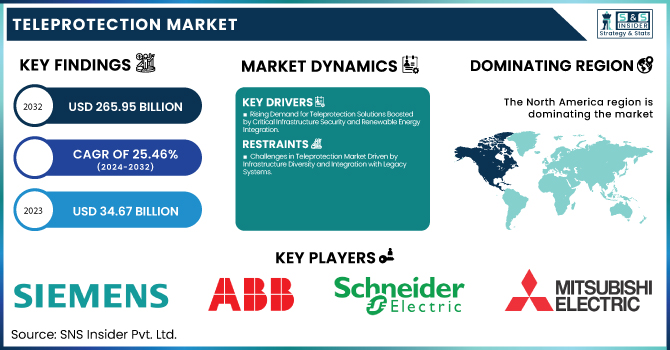

The Teleprotection Market was valued at USD 34.67 billion in 2023 and is expected to reach USD 265.95 billion by 2032, growing at a CAGR of 25.46% over the forecast period 2024-2032.

The integration of teleprotection systems, the increasing adoption of hybrid communication networks, and advanced cybersecurity protocols are all trends that are evolving. Technological trends such as 5G integration, IP-based solutions, and cloud platforms are improving system efficiencies and fault detection sectors.

To Get More information about Teleprotection Market - Request Sample Report

The teleprotection units are now more focused on enhancing reliability and facilitating real-time-based utilization of functionality to rapidly isolate a fault and subsequently restore it. With an increased emphasis on critical infrastructure availability and reliability, remote monitoring solutions enabling centralized control, predictive maintenance, and efficient fault identification and handling are also emerging as very common in both the energy and telecom sectors. The growth of the teleprotection market in the U.S. is mainly due to the advancements in smart grid technologies, the penetration of renewable energy, and the rising need for reliable and secure communication systems. 5G networks and cloud solutions are also making their way and improving the operating experience of the system.

Teleprotection Market Size and Forecast:

-

Market Size in 2023: USD 34.67 Billion

-

Market Size by 2032: USD 265.95 Billion

-

CAGR: 25.46% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

The U.S. Teleprotection Market is estimated to be USD 9.12 Billion in 2023 and is projected to grow at a CAGR of 25.23%. Increasing grid reliability demand, industrial automation adoption, growth of smart cities and resilient power systems, as well as escalated cyber-attack scenarios are further fueling the growth of the U.S. market of teleprotection.

Teleprotection Market Trends:

-

Growing investments in smart grid infrastructure and modern power transmission networks are driving demand for teleprotection systems.

-

Increasing integration of renewable energy sources such as wind and solar is accelerating the need for fast and reliable grid protection technologies.

-

Rising adoption of fiber-optic communication networks is enhancing the speed, reliability, and security of teleprotection solutions.

-

Expansion of high-voltage transmission lines and substations is increasing the deployment of advanced teleprotection equipment.

-

Technological advancements in digital substations, IEC 61850 communication protocols, and intelligent electronic devices (IEDs) are improving system performance.

-

Utilities and power grid operators are focusing on grid reliability, fault detection, and rapid response systems, boosting the adoption of teleprotection technologies globally.

Teleprotection Market Dynamics

Key Drivers:

-

Rising Demand for Teleprotection Solutions Boosted by Critical Infrastructure Security and Renewable Energy Integration

The rising need for reliable and secure communication networks in critical infrastructure segments including power, telecom, and transportation is estimated to spur the demand for teleprotection genres in the market. The importance of fault detection, grid stability, and a fast-disturbance response in the grids necessitates advanced teleportation solutions which have become essential with the rapid penetration of renewable energy systems, mainly in power grids. Moreover, a widespread shift towards digitalization and automation has expedited the need for teleprotection systems for securing communication networks and data transmission, particularly in remote, as well as unsafe environments, such as oil and gas pipelines.

Restrain:

-

Challenges in Teleprotection Market Driven by Infrastructure Diversity and Integration with Legacy Systems

The diversity of the infrastructure is one of the major challenges in the teleprotection market as complexities become high if an integrated platform for advanced telecommunication and protection systems needs to be deployed. Several industries, especially in the developing part of the globe, are still dependent on older systems, and the shift towards new teleportation technologies can be challenging because of compatibility issues. The requirement for seamless integration with existing grid networks and communication systems often demands substantial time and know-how causing delays in project timelines and sub-optimal operational efficiency in the near term.

Opportunity:

-

Teleprotection Market Growth Driven by Smart Grids 5G IoT Investment and Industrialization in Emerging Regions

The uptake within the teleprotection market has likewise grown with the aid of the increasing demand for smart grids, autonomous transportation, and the growing attention to the modernization of infrastructure. Teleprotection Mechanisms and Applications Recent investment by governments and organizations in next-generation communication technologies (such as 5G and IoT) has opened up new opportunities for teleprotection applications. In addition, rapid industrialization in the Asia Pacific and Latin America and the need for improving linear and non-linear control due to smart grid solutions will drive growth. It creates numerous opportunities for various market players to provide a richer range of teleportation systems to coincide with the rapid demand for more robust and secure applications in the regions.

Challenges:

-

Interoperability and Cybersecurity Challenges in Teleprotection Systems Demand Standardization and Enhanced Protection Strategies

Interoperability is another troublesome issue that often comes as a result of not having a common protocol for teleprotection systems. Proprietary solutions are used by different manufacturers and different regions, which makes it hard to ensure effective communication between systems of various vendors and optimal protection. In addition, cybersecurity is another issue in that the growing digitalization of critical infrastructure means systems can be vulnerable to attacks. With teleportation systems communicating with each other, there is a growing threat from cyberattacks on these critical networks, making a continuous investment in hardening the security apparatus required not just for data but also for communication channels. For the long-term success of the teleprotection market, it is therefore vital to address this integration, standardization, and security concerns.

Teleprotection Industry Segmentation Outlook

By Type

The Teleprotection Unit leads the product segment and accounted for a market share of about 40.7% for 2023 due to the rising requirement for fast and reliable fault detection and isolation in critical infrastructure. These units are crucial in safeguarding power grids, telecom networks, and other industrial systems, as they allow for the super-fast relay of protection signals in the case of disturbances. The relevance of teleportation units has prominently increased due to the growing integration of renewable energy sources and the demand for optimal operational periods of power (grid stability), particularly in the power sector.

The Communication Network Technology is anticipated to hold the command for the fastest CAGR growth from 2024 to 2032. The growing penetration of advanced communication networks such as 5G, IoT, and fiber optics concentrates on high data transmission speed and highly improves the efficiency of teleprotection systems. The world is advancing to smarter and automated infrastructure, enhancing the demand for teleprotection over secure, high-speed communication networks, which has huge market potential.

By Components

In 2023, the Intelligent Electronic Device segment accounted for the largest share of 61.4% in the overall teleprotection market. Abstract Intelligent electronic devices (IEDs) are critical elements of real-time monitoring, control, and protection of electrical networks and they have been equipped with advanced functions like fault detection, isolation, and communication with other systems. The need for improving grid reliability and integrating renewable energy sources has fueled their adoption in the power and telecom sectors, which have established them as the dominant market players.

The Interface Device segment is estimated to grow the highest in CAGR over the forecast years from 2024 to 2032. Interface devices are crucial for interfacing teleprotection systems with other devices, such as sensors, relays, and controllers. With an increasing number of industries utilizing automated and integrated systems, the requirement for interface devices that are both efficient and support seamless data exchange within multiple plots will continue to grow. The rise is attributable to the increasing requirement for interface-based and advanced user interface teleprotection systems.

By Application

The teleprotection market was led by the Power sector, which accounted for a share of 38.5% in 2023. The dominance is mainly due to the increasing requirement for trust and secure protection systems in electrical networks, due to the rising deployment of sustainable energy sources. Given the ever-expanding nature of energy networks and the inherent cross-sector interdependence, teleprotection systems in the power industry will become an increasingly important tool to ensure grid stability by quickly detecting faults and isolating disturbances, thus allowing a continuous flow of power.

Information Technology is expected to experience the fastest growth in CAGR from 2024 to 2032. In IT, sectors are advancing with digitalization and automation which are necessitating huge demand for advanced teleportation solutions. With businesses approaching intelligent data centers, cloud networks, and IoT-based systems, the demand for advanced protection and communication technologies increases rapidly. Since the IT sector depends on high-speed, secure, and reliable communication networks, teleprotection systems are vital in ensuring the safety and reliability of digital operations.

Teleprotection Market Regional Analysis

The teleprotection market in North America accounted for the largest share of 35.7% in 2023 Due to the developed infrastructure and presence of top-tier teleprotection enterprises in the region, the leadership of the region is attributed to it. For instance, the United States, not only has made in great shift towards grid modernization and renewable energy deployment but has also witnessed a demand for reliable teleprotection solutions that have encouraged the initiatives, investments as well and policies. GE Grid Solutions, Schneider Electric, and many other companies are engaged in teleportation systems applications to build grid stability. Furthermore, the growing adoption of smart grids and increasing efforts towards cybersecurity concerning telecom and power networks in North America also contribute significantly towards the market growth for the region.

During the period from 2024 to 2032, the Asia Pacific will grow at the highest CAGR. Increasing demand for teleprotection systems due to shifting industrialization/urbanization in China, India, and Japan For example, India is currently witnessing a scenario due to the ongoing impetus for expansion and refurbishment of power grid infrastructure where the growing need for reliable distribution of electricity is creating a need for teleprotection solutions. In Japan too, the use of advanced communication technologies (such as 5G) is enabling Cisco with more efficient and secure telecom and power networks via better and secure teleprotection systems. Such factors emphasize the growing prominence of the Asia Pacific in the global teleprotection market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Siemens (SIPROTEC 5)

-

ABB (Relion 670)

-

Schneider Electric (Sepam Series 20)

-

GE Grid Solutions (Micom P127)

-

Mitsubishi Electric (DECS-300)

-

SEL (SEL-411L)

-

Honeywell (Safety Manager)

-

Toshiba (TOSLINE 10)

-

Eaton (Cooper Power Systems)

-

Omicron (CIBANO 500)

-

RFL Electronics (RFL-2200)

-

S&C Electric (S&C IntelliRupter)

-

Alstom Grid (Grid Automation Solutions)

-

Rockwell Automation (Allen-Bradley PowerMonitor 5000)

-

Nari Technology (TDR-2000)

Teleprotection Market Trends

-

In February 2025, Schneider Electric launched a Smart Power Management solution for homebuilders, helping avoid costly electrical service upgrades by efficiently managing power demands.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 34.67 Billion |

| Market Size by 2032 | USD 265.95 Billion |

| CAGR | CAGR of 25.46% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Teleprotection Unit, Communication Network Technology, Teleprotection Software) • By Components (Intelligent Electronic Device, Interface Device) • By Application (Power, Telecom, Information Technology, Oil & Gas Pipelines, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Siemens, ABB, Schneider Electric, GE Grid Solutions, Mitsubishi Electric, SEL, Honeywell, Toshiba, Eaton, Omicron, RFL Electronics, S&C Electric, Alstom Grid, Rockwell Automation, Nari Technology. |

Frequently Asked Questions

Ans: North America dominated the Teleprotection Market in 2023.

Ans: The Teleprotection Unit segment dominated the Teleprotection Market in 2023.

Ans: The major growth factor of the Teleprotection Market is the increasing demand for reliable and secure communication solutions in smart grids, renewable energy integration, and critical infrastructure protection.

Ans: Teleprotection Market size was USD 34.67 billion in 2023 and is expected to Reach USD 265.95 billion by 2032.

Ans: The Teleprotection Market is expected to grow at a CAGR of 25.46% during 2024-2032.

Get in Touch