Thermometer Market Report Scope & Overview:

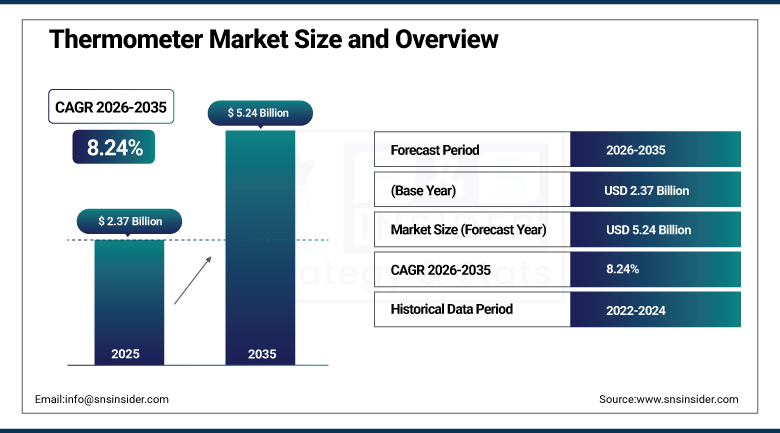

The Thermometer Market was valued at USD 2.37 Billion in 2025 and is expected to reach USD 5.24 Billion by 2035, growing at a CAGR of 8.24% from 2026–2035.

The global thermometer market is growing at a sustained and commercially broad-based pace. Thermometers are temperature measuring instruments whose diverse product types span clinical body temperature measurement, industrial process temperature monitoring, food safety temperature verification, and laboratory precision temperature control across mercury-free glass, digital electronic, infrared non-contact, and smart connected device categories. The market is driven by increasing incidence and prevalence of fever conditions fueling need for advanced temperature-measuring devices, innovations in smart and AI-based thermometers providing real-time monitoring, mobile app connectivity, and improved accuracy, and expanding industrial and food safety temperature monitoring requirements.

In 2024, Withings launched the Thermo Smart Temporal Thermometer 2nd generation with enhanced AI-based fever tracking, multi-user family health monitoring through the Withings Health Mate app, and pediatric fever chart integration that provides parents with context-aware temperature trend analysis alongside absolute temperature readings. The product’s connected health platform integration, represents the commercial direction of consumer thermometer development toward health intelligence platforms whose data value sustains premium device pricing above standalone temperature measurement alternatives.

Market Size and Forecast:

-

Market Size in 2026E: USD 2.56 Billion

-

Market Size by 2035: USD 5.24 Billion

-

CAGR: 8.24% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Thermometer Market- Request Free Sample Report

Thermometer Market Trends:

-

Smart thermometers with smartphone connectivity, cloud tracking, and AI insights are creating premium connected health monitoring device segments.

-

Non-contact infrared thermometers remain widely adopted post-COVID, sustaining strong demand in clinical and consumer hygiene-focused applications.

-

Wearable continuous temperature monitoring in smartwatches and health patches is expanding thermometer use into real-time health tracking systems.

-

Mercury thermometer phase-out under global regulations is accelerating replacement with digital and mercury-free alternatives across healthcare systems.

-

Industrial IoT integration is transforming thermometers into networked sensors enabling real-time process monitoring and predictive maintenance applications.

U.S. Thermometer Market Outlook:

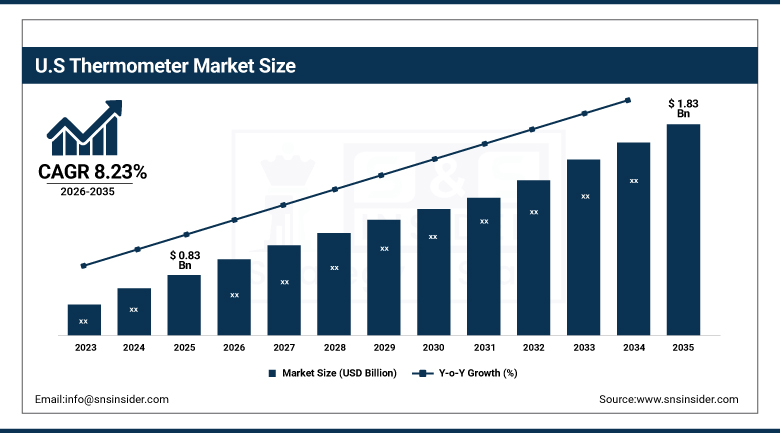

The U.S. Thermometer Market was valued at approximately USD 0.83 Billion in 2025 and is expected to reach approximately USD 1.83 Billion by 2035, growing at a CAGR of approximately 8.23%.

The U.S. is the most commercially sophisticated thermometer market within North America’s dominant revenue position. Becton Dickinson, Exergen Corporation, Omron Healthcare, and Welch Allyn’s U.S. operations serve the domestic clinical market, while Fluke, FLIR, and Testo serve the industrial segment. The post-COVID household thermometer ownership normalization, the growing home health monitoring trend, and the aging population’s chronic disease management temperature monitoring requirement collectively sustain U.S. consumer thermometer procurement. FDA’s OTC market clearance infrastructure for consumer thermometers creates commercial accessibility that sustains robust domestic product innovation and launch activity.

Omron Healthcare launched the EvenTemp Digital Thermometer in 2024 with patented measurement technology providing consistent accurate readings regardless of ambient temperature conditions whose clinical accuracy at home settings creates specification confidence for consumer and clinical procurement. The product’s 10-second measurement speed and colour-coded fever indicator create ease-of-use attributes whose convenience drives adoption in household and clinical settings where measurement speed and result clarity create practical value.

Thermometer Market Segment Analysis:

-

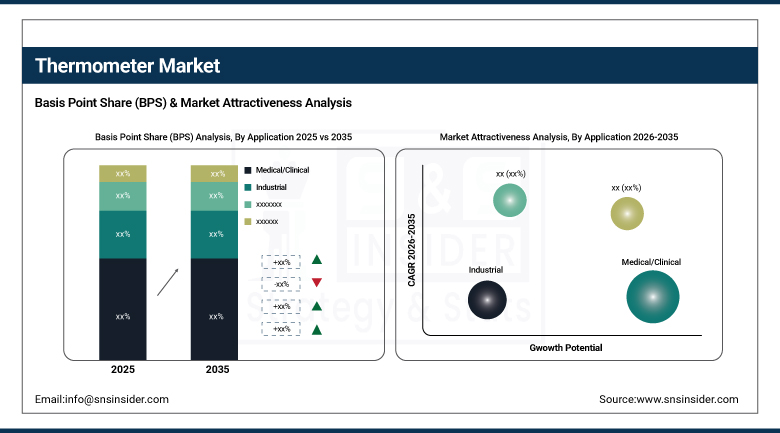

By Application, the medical/clinical segment dominated the market with 27.1% share in 2025, driven by growing incidence of infectious diseases, higher hospital visits, and extensive use of thermometers in home, while the industrial segment is the fastest growing as manufacturing process temperature monitoring, HVAC maintenance, electrical maintenance, and food production quality control create above-average demand growth.

-

By Product Type, the digital/electronic thermometer segment dominated the market with approximately 45% share in 2025 as the most widely adopted clinical and consumer temperature measurement device, while the infrared/non-contact thermometer segment is the fastest growing as contactless measurement’s hygiene advantage, speed convenience, and pediatric ease-of-use create above-average adoption in consumer, clinical, and food service settings.

-

By Technology, the contact thermometer segment dominated the market with approximately 58% share in 2025 as lower cost relative to infrared alternatives, and patient compliance in cooperative clinical settings create contact measurement’s continued dominance in hospital and routine clinical temperature assessment, while the non-contact/infrared segment is the fastest growing as temporal artery, tympanic, and forehead infrared measurement’s convenience, speed, and hygiene advantages create adoption growth across pediatrics and infection-control-sensitive clinical environments.

-

By End User, the hospitals & clinics segment dominated the market with approximately 38% share in 2025 as inpatient and outpatient clinical temperature assessment’s consistent procurement creates the most commercially established thermometer end-user category, while the home care/consumer segment is the fastest growing as smart home health monitoring adoption, connected thermometer platform engagement, and the growing consumer health awareness create consumer thermometer procurement.

By Application, medical dominates, industrial grows fastest

Medical and clinical applications retained the dominant position with 27.1% of the thermometer market in 2025. The clinical thermometer’s role as the primary patient assessment tool in every healthcare encounter creates the most commercially consistent thermometer procurement category whose aggregate across global hospital, clinic, and emergency department settings sustains medical’s dominant application share. Each hospital’s regular thermometer replacement programme, infection control procurement for single-use disposable clinical thermometers, and the nursing staff’s institutional device specification creates consistent commercial relationships whose volume sustains medical application’s market leadership.

Industrial is the fastest-growing application because the convergence of manufacturing quality control, food safety regulation, electrical maintenance, and building management system integration creates multiple simultaneous above-average growth vectors in non-medical thermometer procurement. Each food processing facility whose HACCP compliance requires temperature verification at multiple critical control points creates industrial thermometer procurement that scales with food production volume. Industrial IoT’s integration of thermometer sensors into connected monitoring networks creates premium specification for smart industrial thermometers whose data connectivity creates process optimization value beyond standalone temperature measurement.

By Product, digital dominates, infrared grows fastest

Digital and electronic thermometers retained the dominant product type position with approximately 45% of the thermometer market in 2025. Digital’s commercial primacy reflects its universal adoption as the replacement standard for mercury glass thermometers whose phase-out under the Minamata Convention creates systematic procurement transition that sustains digital thermometer’s aggregate commercial dominance across clinical, consumer, and food service applications. Each mercury glass thermometer replacement creates digital procurement whose transition compounds with the global mercury phase-out programme’s progressive geographic implementation.

Infrared and non-contact thermometers are the fastest-growing product because the COVID-19 pandemic’s permanent normalization of contactless temperature measurement in healthcare and consumer settings created structural adoption above pre-pandemic baselines. Each hospital infection control protocol that specifies non-contact measurement for screening purposes creates institutional procurement whose clinical hygiene motivation sustains specification. Pediatric thermometry’s preference for non-contact forehead measurement, whose child comfort advantage over oral or rectal contact alternatives creates parental specification motivation, sustains consumer infrared thermometer’s above-average household adoption growth.

By End User, hospitals dominate, home care grows fastest

Hospitals and clinics retained the dominant end-user position with approximately 38% of the thermometer market in 2025. The clinical setting’s temperature assessment frequency, encompassing patient admission assessment, routine vital sign monitoring, post-operative surveillance, and emergency department triage, creates consistent per-facility thermometer consumption whose aggregate across the global hospital infrastructure creates the most commercially concentrated thermometer procurement environment. Each hospital’s disposable probe cover programme, shared-device sanitation protocol, and nursing station thermometer inventory create institutional procurement relationships whose replacement cycle and infection control consumable dimension sustain consistent commercial volume.

Home care and consumer is the fastest-growing end user because smart thermometer platform adoption, connected health monitoring ecosystem engagement, and the growing consumer investment in home health management are creating above-average consumer thermometer procurement that compounds with smart home health device ecosystem expansion. Each consumer who upgrades from a basic digital thermometer to a smart connected device creates premium procurement whose app-based fever tracking, family health data management, and telehealth consultation integration create ecosystem value that sustains above-commodity pricing. The home care sector’s expansion as healthcare systems progressively shift toward community-based chronic disease management creates thermometer procurement that sustains the segment’s fastest-growing status.

By Technology, contact dominates, non-contact grows fastest

Contact thermometers retained the dominant technology position with approximately 58% of the thermometer market in 2025. Contact measurement’s clinical accuracy at oral, axillary, and rectal measurement sites creates established clinical confidence whose validated performance in routine temperature assessment sustains specification in cooperative adult patients whose measurement compliance enables accurate contact reading. The lower per-unit cost of digital contact thermometers relative to infrared alternatives creates economic accessibility that sustains contact technology’s dominant commercial position in cost-sensitive consumer and institutional procurement contexts.

Non-contact infrared thermometers are the fastest-growing technology because multiple simultaneous adoption drivers create above-average structural demand growth. The post-COVID healthcare hygiene protocol’s permanent normalization of contactless screening, the pediatrics measurement convenience advantage, and the food safety application’s non-contact verification capability collectively create commercial adoption momentum. Smart temporal artery thermometers’ clinical accuracy studies demonstrating performance equivalent to rectal measurement in pediatrics settings create clinical evidence that sustains professional non-contact specification. The industrial thermometer’s non-contact measurement advantage for high-temperature, moving, or inaccessible measurement targets sustains industrial infrared thermometer above-average adoption.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Thermometer Market Insights

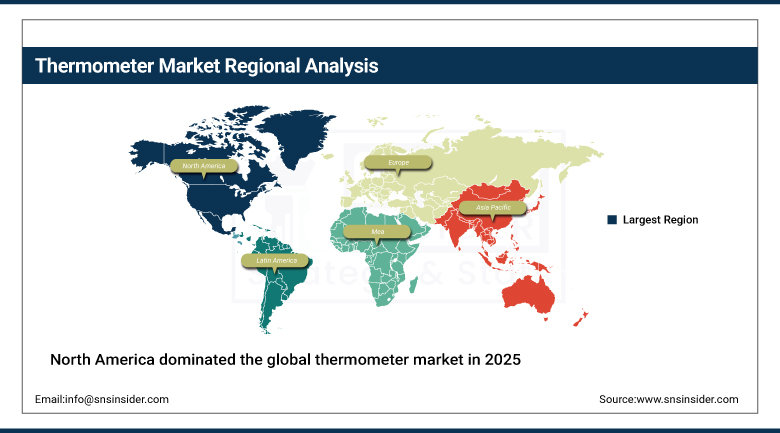

North America dominated the global thermometer market in 2025 as the most commercially sophisticated temperature measurement market. The United States accounts for approximately 87.4% of North American revenues through Becton Dickinson, Exergen, Omron Healthcare, and Welch Allyn’s clinical thermometer leadership, and Fluke, FLIR, and Testo’s industrial thermometer commercial presence. The post-COVID household thermometer ownership normalization and the smart health device ecosystem’s expansion sustain above-average consumer thermometer procurement.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system’s clinical thermometer procurement, the growing home health monitoring sector’s consumer adoption, and the industrial sector’s temperature monitoring investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Thermometer Market Insights

Europe is a technically sophisticated thermometer market where EU Minamata Convention implementation drives mercury thermometer replacement, EU food safety regulation’s HACCP temperature monitoring requirement creates structured industrial procurement, and Braun’s and Hartmann’s German operations define the clinical consumer thermometer standard. Germany accounts for approximately 22.3% of European revenues through its advanced healthcare infrastructure, Braun ThermoScan’s domestic market leadership, and the industrial precision instrument sector’s thermometer procurement.

The United Kingdom, France, and Italy are significant secondary markets where national healthcare system clinical procurement, consumer health monitoring adoption, and the food processing sector’s temperature compliance investment create consistent thermometer demand.

Asia Pacific Thermometer Market Insights

Asia Pacific is the fastest-growing regional thermometer market, driven by China’s extraordinary healthcare infrastructure expansion, India’s growing consumer health awareness, Japan’s advanced smart health device adoption, and Southeast Asia’s expanding clinical procurement. China accounts for approximately 44.8% of Asia Pacific revenues through its hospital network’s clinical procurement, the extraordinary consumer thermometer production and domestic consumption, and the industrial sector’s temperature monitoring investment.

Japan’s premium smart thermometer market, South Korea’s connected health device ecosystem, and India’s rapidly growing consumer healthcare market create significant secondary markets whose combined procurement sustains Asia Pacific’s fastest-growing regional status.

MEA & Latin America Thermometer Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital network’s clinical procurement, the Vision 2030 healthcare infrastructure investment, and the consumer market’s growing health device adoption. Brazil leads Latin American revenues at approximately 44.2% through its large public hospital network, the consumer market’s growing home health monitoring adoption, and the food processing sector’s temperature compliance procurement.

UAE’s advanced private healthcare sector and South Africa’s clinical thermometer procurement create significant MEA secondary markets whose combined demand reflects the progressive adoption of advanced temperature measurement across both national healthcare systems.

Market Dynamics:

Growth Drivers: Infectious disease incidence driving fever monitoring demand and smart health ecosystem creating premium thermometer adoption

Increasing incidence and prevalence of fever conditions is the thermometer market’s most commercially consistent structural demand driver. WHO’s documentation that fever is the most common reason for medical consultation globally, encompassing influenza, COVID-19, malaria, dengue, and other infectious conditions, creates consistent thermometer demand whose volume compounds with infectious disease incidence and healthcare access improvement. The post-COVID-19 pandemic’s permanent elevation of fever monitoring awareness in households, schools, and healthcare facilities creates above-pre-pandemic thermometer procurement whose structural character sustains demand independently of acute pandemic events.

Smart and connected thermometer ecosystem development is creating a premium market category whose health intelligence value sustains above-commodity pricing that basic digital thermometer alternatives cannot command. Each smart thermometer platform that integrates fever history tracking, symptom logging, medication reminder, and telehealth consultation creates per-device annual software and service revenue whose recurring nature sustains commercial relationships beyond hardware replacement cycles.

Restraints: Market saturation in developed markets and competition from low-cost manufacturers moderating pricing

Thermometer market maturity in developed market consumer segments creates saturation where high household penetration reduces net new unit sales to replacement demand. Each household that already owns adequate thermometers creates replacement-only procurement whose lower volume moderates market growth below emerging market adoption trajectory. The basic digital thermometer’s commodity character in cost-competitive retail channels creates downward pricing pressure whose margin compression moderates premium thermometer manufacturers’ revenue growth relative to unit volume growth.

Chinese manufacturing’s competitive pricing in the basic digital and infrared thermometer categories creates market competition that moderates premium Western brand pricing power in cost-sensitive procurement segments. Each low-cost Asian producer that enters retail channels with functional thermometer products at below-premium pricing creates substitution competition that requires innovation investment to sustain differentiation.

Opportunities: Continuous wearable temperature monitoring and emerging market healthcare expansion

Continuous wearable temperature monitoring represents the most commercially innovative thermometer market development whose integration into smartwatches, health patches, and continuous wellness monitoring devices creates persistent body temperature data whose clinical and wellness intelligence value creates new commercial categories. Each wearable device that incorporates continuous temperature sensing creates thermometer sensor procurement that compounds with wearable device shipment volume whose growth trajectory substantially exceeds traditional thermometer replacement cycles.

Emerging market healthcare expansion in Africa, South Asia, and Southeast Asia represents the most commercially scalable volume growth opportunity whose first-time clinical and consumer thermometer adoption creates net new procurement beyond the established market’s replacement cycle. Each new primary healthcare facility commissioned in a developing country creates clinical thermometer procurement, and each new urban household that adopts home health monitoring creates consumer thermometer demand that compounds with middle-class formation.

Recent Developments:

-

2026: Masimo Corporation advanced its non-invasive temperature monitoring ecosystem by integrating continuous wearable-based thermal sensing with hospital monitoring platforms.

-

2025: Braun (Procter & Gamble) expanded its infrared thermometer lineup with enhanced no-touch measurement technology and faster response sensors, improving accuracy in pediatric and clinical screening applications.

-

2025: Omron Healthcare Inc. expanded its connected digital thermometer portfolio in 2025 by integrating AI-enabled fever tracking and Bluetooth-based synchronization with mobile health applications.

Thermometer Market Key Players:

-

Becton, Dickinson and Company (BD)

-

Omron Healthcare Inc.

-

Braun GmbH (Procter & Gamble)

-

Exergen Corporation

-

Baxter International

-

A&D Medical (A&D Company)

-

Microlife Corporation

-

Withings SA

-

iHealth Labs Inc.

-

Masimo Corporation

-

Fluke Corporation (Fortive)

-

Teledyne

-

Testo SE & Co. KGaA

-

Hanna Instruments

-

Traceable Products (Control Company)

-

Paul Hartmann AG

-

Radiant Innovation Inc.

-

American Diagnostic Corporation

-

Helen of Troy

-

Invacare Corporation

Thermometer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.37 Billion |

| Market Size by 2035 | USD 5.24 Billion |

| CAGR | CAGR of 8.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Digital/Electronic Thermometers, Infrared/Non-Contact Thermometers, Mercury-Free/Glass Thermometers, Smart/Connected Thermometers, Disposable Thermometers, Industrial Thermometers) • By Application (Medical/Clinical, Industrial, Food & Beverage, Laboratory & Scientific, Others) • By Technology (Contact, Non-Contact/Infrared) • By End User (Hospitals & Clinics, Home Care/Consumer, Industrial Facilities, Food Processing, Laboratories & Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Becton, Dickinson and Company (BD), Omron Healthcare Inc., Braun GmbH (Procter & Gamble), Exergen Corporation, Baxter International, A&D Medical (A&D Company), Microlife Corporation, Withings SA, iHealth Labs Inc., Masimo Corporation, Fluke Corporation (Fortive), Teledyne, Testo SE & Co. KGaA, Hanna Instruments, Traceable Products (Control Company), Paul Hartmann AG, Radiant Innovation Inc., American Diagnostic Corporation, Helen of Troy, Invacare Corporation |

Frequently Asked Questions

The Thermometer Market is expected to grow at a CAGR of 8.24% from 2026 to 2035.

The Thermometer Market was valued at USD 2.37 Billion in 2025.

Increasing incidence and prevalence of fever conditions fuelling demand for advanced temperature-measuring devices, and smart AI-based thermometer innovation providing real-time monitoring and mobile app connectivity creating premium connected health device procurement.

Medical/Clinical dominated the Thermometer Market with 27.1% share in 2025, driven by growing incidence of infectious diseases, higher hospital visits, and extensive use in home care environments.

North America dominated the Thermometer Market in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch