White Cement Market Report Scope & Overview:

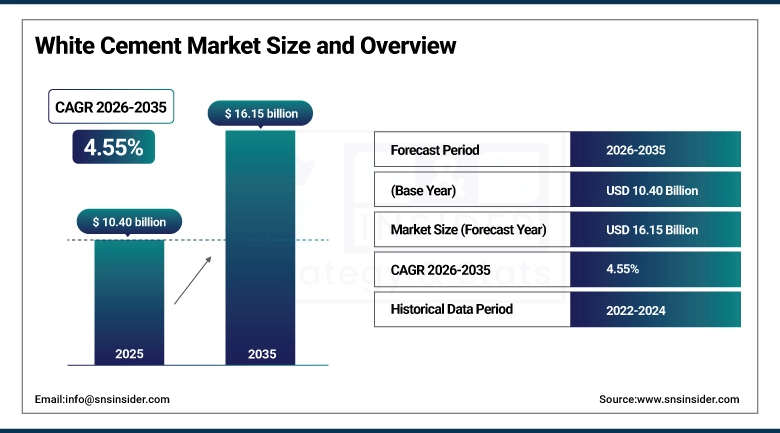

The White Cement Market size was valued at USD 10.40 Billion in 2025 and is projected to reach USD 16.15 Billion by 2035, growing at a CAGR of 4.55% during 2026-2035.

The growth of White Cement Market can be attributed to various factors such as increase in demand for attractive constructions, urbanization, increased construction of residential and commercial properties, usage in decoration purposes, and increased infrastructure expenditure, especially in developing nations that require high-end and eco-friendly construction materials.

White Cement Market Size and Forecast:

-

Market Size in 2025: USD 10.40 Billion

-

Market Size by 2035: USD 16.15 Billion

-

CAGR of 4.55% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on White Cement Market - Request Free Sample Report

Key White Cement Market Trends

-

Rising demand for decorative and architectural applications in residential and commercial construction

-

Increasing adoption of white cement in precast elements, tiles, and façade solutions

-

Growing urbanization and infrastructure development in emerging economies

-

Shift toward sustainable and low-carbon cement production technologies

-

Expansion of premium housing and renovation activities driving aesthetic material usage

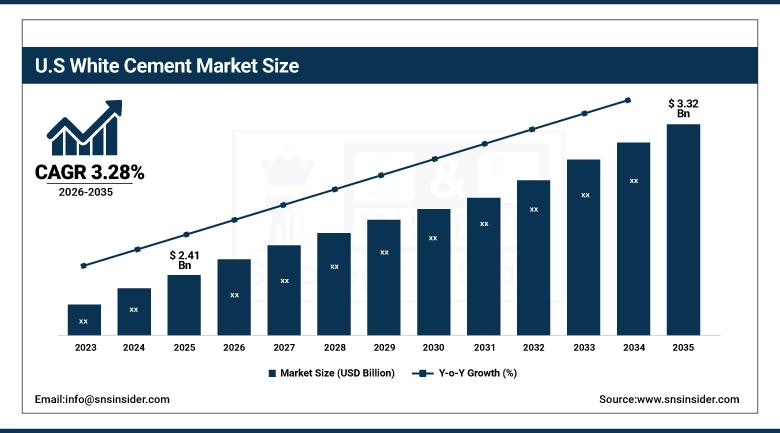

The U.S. White Cement Market size was valued at USD 2.41 Billion in 2025 and is projected to reach USD 3.32 Billion by 2035, growing at a CAGR of 3.28% during 2026-2035. The United States white cement market is gradually growing owing to the demand for decorative construction, infrastructural developments, renovations, and moderate growth attributed to premium construction materials and development of housing and commercial projects.

White Cement Market Growth Drivers:

-

Strong Growth Drivers Accelerating White Cement Demand Across Construction, Infrastructure, and Decorative Building Applications Globally

Growth in the white cement market can be attributed to increasing demand for aesthetics in construction materials for homes and commercial buildings. Growth in urbanization and development of infrastructure is driving up the demand for white cement. Its high reflective nature makes it suitable for use in architecture and decoration. Its use in precast items, tiles, and cladding systems is adding to its increased demand. Moreover, increase in disposable incomes and expensive housing in developing nations has led to rapid growth in the white cement market.

JK Cement's white cement segment reported volumes of approximately 0.72 million tonnes for FY2024, representing 14% year-on-year growth that outpaced both grey cement overall and the broader Indian construction sector growth, with management citing premium residential finishing and exterior putty applications as the primary growth categories and announcing a 0.4 million tonne capacity expansion at Gotan to be completed by FY2026.

White Cement Market Restraints:

-

Key Market Restraints Limiting White Cement Adoption Including High Costs and Raw Material Constraints Globally

The white cement industry faces certain issues due to the high costs associated with the production process, as white cement production costs more than that of grey cement production. The availability of particular raw material with low iron is an issue in the case of white cement since only limited sources are available. In addition to this, energy consumption involved in the process makes it expensive to produce. Apart from this, lack of awareness and competition from other products are also issues.

White Cement Market Opportunities:

-

Emerging Opportunities Driving White Cement Market Expansion Through Innovation, Sustainability, and Premium Construction Demand Globally

There is good potential offered by the market due to rising awareness regarding sustainable construction and environmentally friendly building material. There is an emphasis on research for low carbon footprint and energy efficiency in manufacturing processes. Rising demand for high-end properties, smart city constructions, and city redevelopment projects is generating fresh prospects. Growth in the developing economies and underdeveloped rural markets provides good potential for growth. In addition, innovation in colored as well as value added white cement products can help boost sales going forward.

White Cement Market Segmentation Analysis

-

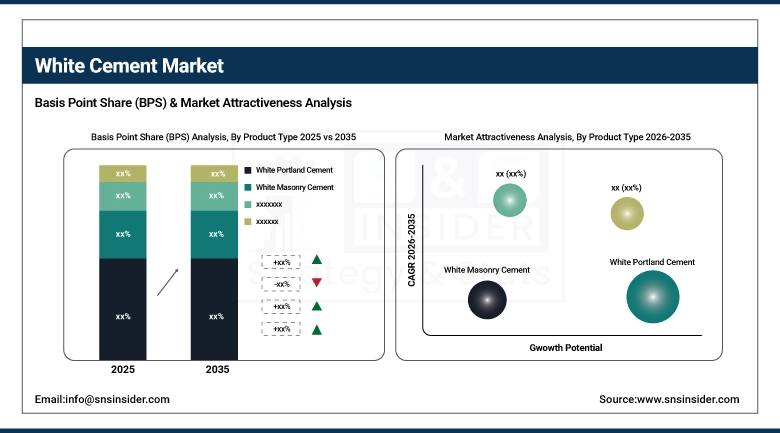

By Product Type, White Portland Cement dominated with 64.28% in 2025, and White Blended Cement is expected to grow at the fastest CAGR of 6.52% from 2026 to 2035.

-

By Application, Residential Construction dominated with 38.62% in 2025, and Infrastructure & Public Works is expected to grow at the fastest CAGR of 5.16% from 2026 to 2035.

-

By End-User Industry, the Residential Sector dominated with 39.15% in 2025, and the Industrial Sector is expected to grow at the fastest CAGR of 5.17% from 2026 to 2035.

-

By Strength / Type Grade, Type I (General Purpose) dominated with 47.36% in 2025, and Type III (High Early Strength) is expected to grow at the fastest CAGR of 5.44% from 2026 to 2035.

By Product Type, White Portland Cement Leads White Cement Market While White Blended Cement Set for Fastest Growth 2026 to 2035

White Portland Cement is dominating the market because of the better strength, durability, and versatility in building and construction purposes. The uniformity of its coloring and appearance makes it suitable for use in premium structures. On the other hand, white blended cement is becoming increasingly popular because of its improved characteristics, economical price, and green features. Growing interest in green building materials and workability is promoting its quicker adoption in modern building trends.

By Application, Residential Construction Leads While Infrastructure and Public Works Shows Fastest Growth in White Cement Market 2026 to 2035

Residential constructions have become prominent with the widespread use of white cement owing to its utilization in beautiful buildings and other decorative surfaces. Urbanization, along with the increasing amount of money that people spend on buying better homes, is driving the growth of this sector. On the other hand, there is also a surge in the infrastructure and public works sectors as governments are now investing more and more in building smart cities and urban infrastructures.

By End-User Industry, Residential Sector Leads While Industrial Sector Poised for Fastest Growth in White Cement Market 2026 to 2035

The residential segment occupies the largest market share due to growing demand for aesthetically pleasing construction material used in residential buildings. With an increase in renovation work and consumers favoring visually pleasing finishes, there will be a positive impact on the growth of the market. On the other hand, the industrial sector is experiencing higher growth because of growing demand for white cement due to its use in special purpose applications like precast, industrial flooring, and structural supports.

By Strength and Type Grade, Type I General Purpose Leads White Cement Market While Type III High Early Strength Shows Fastest Growth 2026 to 2035

The most common white cement type in the market today is the Type I because of its multi-purpose uses and wide applicability from construction to decorations. It has excellent durability and can be used for various purposes. On the other hand, Type III white cement is witnessing faster growth in sales because of its high early strength that leads to faster construction.

White Cement Market Regional Analysis

North America White Cement Market Insights

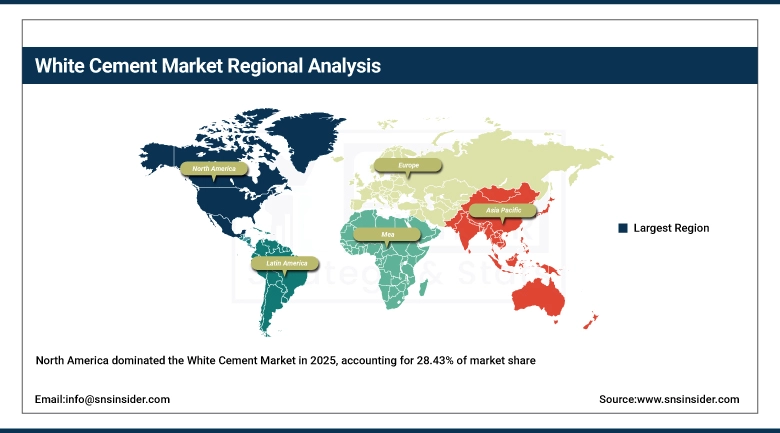

North America held a 28.43% share of the global White Cement Market in 2025 at USD 2.96 Billion, growing at a CAGR of 3.58% through 2035. North America played a notable role in the White Cement Market due to the considerable demand for the purpose of construction with attractive features, renovations, and construction upgrades. North America enjoys a high level of construction technology adoption and utilization along with a greater tendency toward the use of quality construction materials. Moreover, there has been an increase in the number of residential remodeling projects and commercial construction works.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. White Cement Market Insights

The United States dominated North America's white cement market at 81.64%, USD 2.41 Billion in 2025. The US was the leader in the white cement market of North America with an overwhelming market share owing to robust construction activities, renovation needs, and increased usage of decorative elements. Infrastructure development projects and the inclination towards high-quality building materials also fueled the market growth.

Europe White Cement Market Insights

Europe held 24.68% of the global market at USD 2.57 Billion in 2025, growing at a modest CAGR of 3.49% through 2035. The share held by Europe in the world white cement industry was significant due to the presence of established construction sectors as well as a high demand for top quality building materials. Europe enjoys superior technology and stringent policies concerning environmental protection, which make it favor the production of cement using sustainable methods. Factors driving growth include refurbishment of aged buildings, increased emphasis on energy conservation in buildings, and the use of attractive architectural designs.

Germany White Cement Market Insights

Germany dominated the European White Cement Market in 2025 driven by strong construction activity, advanced infrastructure, and high demand for premium and sustainable building materials, supported by renovation projects and energy-efficient building initiatives.

Asia Pacific White Cement Market Insights

Asia Pacific is the fastest-growing region at 5.87% CAGR through 2035, valued at USD 3.28 Billion in 2025 and projected to reach USD 5.79 Billion by 2035 Asia-Pacific is the most rapidly developing region in the White Cement Market, fueled by the fast pace of urbanization, the development of infrastructure projects, and construction activities. The increasing popularity of aesthetically pleasing and high-quality buildings, coupled with initiatives taken by governments to build smart cities and transport infrastructure, has resulted in robust market growth. Furthermore, Asia-Pacific is witnessing an increase in its middle class and disposable income, which is expected to fuel the market in the coming years until 2035.

India White Cement Market Insights

India dominated the Asia Pacific White Cement Market in 2025, driven by rapid urbanization, strong residential construction demand, and increasing use of decorative materials, supported by infrastructure development and rising preference for premium building solutions.

Latin America (LATAM) and Middle East & Africa (MEA) White Cement Market Insights

The emerging markets within the white cement segment are those of Latin America and the Middle East and Africa, fueled by the increase in construction activities and investments in infrastructure. For Latin America, urbanization and development in the residential sector have resulted in a rise in the demand for ornamental products. In the case of the Middle East & Africa market, it enjoys the advantages of infrastructure investment, tourism, and luxury construction trends.

Competitive Landscape for White Cement Market:

Cimsa Çimento Sanayi ve Ticaret A.Ş., headquartered in Istanbul and majority-owned by Cementir Holding since 2017, is the world's largest white cement producer by single-site capacity and one of the most globally active exporters, shipping to 65 countries from its Mersin facility on Turkey's Mediterranean coast. Cimsa produces white Portland cement, white masonry cement, and the LC3 blended white cement products whose commercialisation is potentially the most strategically significant product development in the white cement industry in a decade.

-

In 2024, Cimsa reported record white cement export volumes following the completion of its calcined clay blending line at Mersin, with the new LC3 white blended product accounting for approximately 8% of total white cement dispatches and winning specification approvals at three major European infrastructure projects citing reduced embodied carbon compared to standard white Portland cement.

JK Cement Ltd., headquartered in New Delhi and part of the J.K. Organisation, operates the largest white cement plant in Asia at Gotan in Rajasthan's Nagaur district, where the local limestone's iron oxide content below 0.1% makes it among the best white cement raw material deposits in the world. JK White and Birla White are the two brand franchises the company operates across India's white cement and wall putty segments — a distribution distinction that allows JK to serve both the trade channel and the institutional specification channel through separate sales organisations without cannibalisation.

- In 2024, JK Cement broke ground on its 0.4 million tonne per annum white cement capacity expansion at Gotan, scheduled for commissioning in FY2026, with the management citing sustained double-digit growth in the exterior wall putty category and increasing demand from premium residential projects in Bengaluru, Hyderabad, and the Delhi-NCR corridor as the commercial basis for the investment.

White Cement Market Key Players:

-

Cementir Holding N.V.

-

Çimsa Çimento Sanayi ve Ticaret A.Ş.

-

UltraTech Cement Ltd.

-

CEMEX S.A.B. de C.V.

-

Holcim Ltd.

-

Federal White Cement Ltd.

-

Royal White Cement

-

Saudi White Cement Company

-

Ras Al Khaimah White Cement Co.

-

Italcementi S.p.A.

-

Adana Çimento

-

Cementos Portland Valderrivas S.A.

-

SOTACIB

-

Aalborg Portland A/S

-

Shargh White Cement Co.

-

Fars & Khuzestan Cement Co.

-

Taiheiyo Cement Corporation

-

Siam Cement Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.40 Billion |

| Market Size by 2035 | USD 16.15 Billion |

| CAGR | CAGR of 4.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (White Portland Cement, White Masonry Cement, White Blended Cement, and Others) • By Application (Residential Construction, Commercial Construction, Infrastructure & Public Works, and Architectural & Decorative Applications) • By End-User Industry (Residential Sector, Commercial Real Estate, Industrial Sector, and Institutional & Infrastructure) • By Strength / Type Grade (Type I (General Purpose), Type II (Moderate Resistance), Type III (High Early Strength), and Specialty Grades) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cementir Holding N.V., Çimsa Çimento Sanayi ve Ticaret A.Ş., JK Cement Ltd., UltraTech Cement Ltd., CEMEX S.A.B. de C.V., Holcim Ltd., Federal White Cement Ltd., Royal White Cement, Saudi White Cement Company, Ras Al Khaimah White Cement Co., Italcementi S.p.A., Adana Çimento, Cementos Portland Valderrivas S.A., SOTACIB, Aalborg Portland A/S, Union Cement Company, Shargh White Cement Co., Fars & Khuzestan Cement Co., Taiheiyo Cement Corporation, Siam Cement Group. |

Frequently Asked Questions

Asia Pacific is the largest and fastest-growing region in the White Cement Market.

White Portland Cement dominated the White Cement Market with a 64.28% share in 2025

Rising demand for decorative construction, premium housing, infrastructure projects, and sustainable, aesthetically appealing building materials globally.

The White Cement Market size was USD 10.40 Billion in 2025 and is expected to reach USD 16.15 Billion by 2035.

The White Cement Market is expected to grow at a CAGR of 4.55% from 2026-2035.

Get in Touch