Wood Fiber Insulation Market Report Scope & Overview:

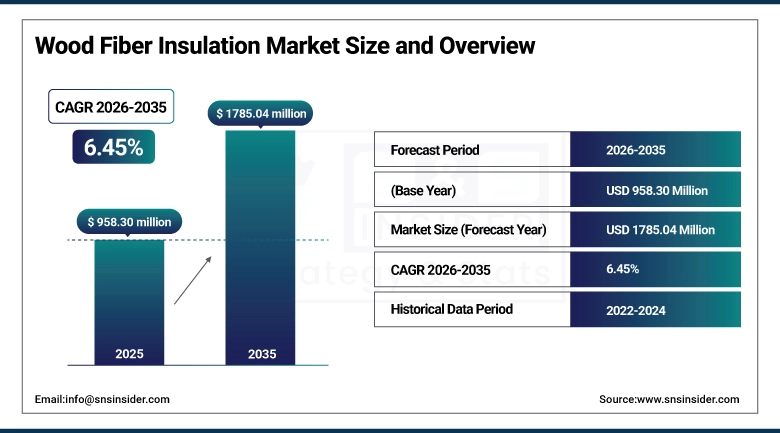

The Wood Fiber Insulation Market size was valued at USD 958.30 Million in 2025 and is projected to reach USD 1,785.04 Million by 2035, growing at a CAGR of 6.45% during 2026-2035.

The Wood Fiber Insulation market is expected to exhibit strong growth over the forecast period on the back of several trends that include stricter building energy regulations, the increasing trend towards using low-carbon building materials within the construction industry, and consumer demand for natural and breathable insulation products. Building owners in Europe have been faced with increasing regulations surrounding the Energy Performance of Buildings Directive and are thus investing in more efficient insulation systems for existing buildings, making wood fiber insulation increasingly competitive against mineral wool and foam insulation alternatives.

Market Size and Forecast:

-

Market Size in 2025: USD 958.30 Million

-

Market Size by 2035: USD 1,785.04 Million

-

CAGR of 6.45% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Wood Fiber Insulation Market - Request Free Sample Report

Key Wood Fiber Insulation Market Trends

-

Rising demand for recycled and waste wood fiber products as construction firms seek to meet embodied carbon targets under procurement policies and green certification frameworks, with the recycled fiber segment growing at a faster pace than virgin fiber across all major markets.

-

European manufacturers including STEICO SE and Gutex are scaling production capacity to address order backlogs in the commercial retrofit segment, with demand from the EU renovation wave initiative outpacing installed production across Germany, France, and Austria.

-

Mats, rolls, and batts formats are gaining market share against rigid boards in residential applications, driven by contractor preference for products that fit between standard stud and rafter spacings without cutting and that handle site moisture more tolerantly than foam alternatives.

-

E-commerce and online distribution platforms are the fastest-growing channel for wood fiber insulation, as homeowner-led renovation activity and self-build housing projects generate direct-to-site purchasing demand that traditional builder merchant networks were not structured to serve efficiently.

-

Industrial building insulation specifications are increasingly including wood fiber products for interior lining applications where thermal mass, acoustic performance, and diffusion-open construction are project requirements, particularly in food processing, agricultural, and cold-storage facilities where humidity management inside the building envelope matters.

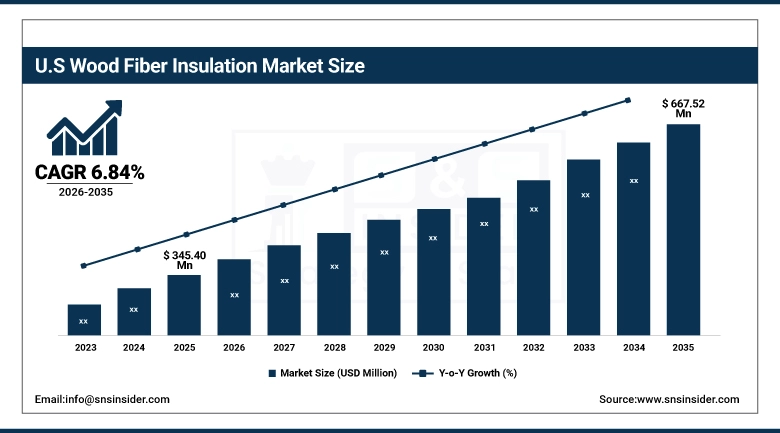

The U.S. Wood Fiber Insulation Market size was valued at USD 345.40 Million in 2025 and is projected to reach USD 667.52 Million by 2035, growing at a CAGR of 6.84% during 2026-2035. The U.S. market is the dominant national market within North America, underpinned by residential construction activity in the Pacific Northwest and New England where architects and specifiers have a longer history with natural fiber building products, combined with growing commercial building retrofit demand tied to state-level energy benchmarking and disclosure programs in California, New York, and Massachusetts that put pressure on building owners to improve thermal performance.

Wood Fiber Insulation Market Growth Drivers:

-

Wood Fiber Insulation Market Demand Advances as Building Energy Efficiency Mandates, Bio-Based Material Preferences, and Commercial Retrofit Programs Broaden Adoption Across Residential, Commercial, and Industrial Applications

The commercial building retrofit market represents one of the more durable demand drivers for wood fiber insulation in developed economies. Buildings consume roughly 40% of total energy in the U.S. and European Union, and wall, roof, and floor insulation upgrades remain among the highest-impact retrofit measures available to building owners without structural intervention. Wood fiber insulation products in board and batt formats are increasingly competitive in these applications because they offer hygrothermal performance advantages over closed-cell alternatives, allowing walls to dry inward and outward in climates where moisture management is a structural durability concern rather than a comfort issue alone.

Wood Fiber Insulation Market Restraints:

-

Wood Fiber Insulation Market Expansion Constrained by Higher Unit Cost Relative to Mineral Wool and Foam Alternatives, Limited Manufacturing Scale Outside Europe, and Contractor Familiarity Gaps in North American and Asia Pacific Markets

The most persistent constraint facing wood fiber insulation manufacturers is cost competitiveness against established mineral wool and extruded polystyrene products, particularly in price-sensitive residential renovation and low-cost commercial construction segments where specification decisions are driven by installed cost per R-value rather than whole-life or environmental performance considerations. Wood fiber products carry material cost premiums relative to glasswool and rockwool that are difficult to close at current production volumes, and the manufacturing infrastructure required to process wood fiber into consistent insulation boards, batts, and loose fill is concentrated in Germany, Austria, Switzerland, and France, leaving North American and Asia Pacific markets dependent on imports that add logistics cost and lead time uncertainty. Contractor installation familiarity is an additional friction point: wood fiber insulation handling, fastening, and detailing requirements differ from mineral wool and foam in ways that slow adoption in markets where tradesperson training is organized around conventional product categories.

Wood Fiber Insulation Market Opportunities:

-

Recycled Wood Fiber Product Development, Asia Pacific Commercial Construction Growth, Renovation Wave Policy Mandates in Europe, and E-Commerce Channel Expansion Create Measurable Market Opportunities Through 2035

Insulated materials produced from recycled and waste wood fibers present a highly promising product development prospect among such insulation products, since many construction projects in Europe, including the public sector in North America, have procurement policies that take into account the constraints on embodied carbon and require bio-based materials content, conditions that cannot be met by the virgin mineral fiber insulation products. Producers with verifiable recycled content percentages and low Global Warming Potential values in their Environmental Product Declarations enjoy the preference when specifying such building projects, which must comply with strict sustainability procurement criteria. In Asia Pacific, commercial real estate construction in India is on the rise, with Hyderabad, Pune, Bengaluru, and the National Capital Region leading the construction of offices and logistics facilities.

Wood Fiber Insulation Market Segment Analysis

-

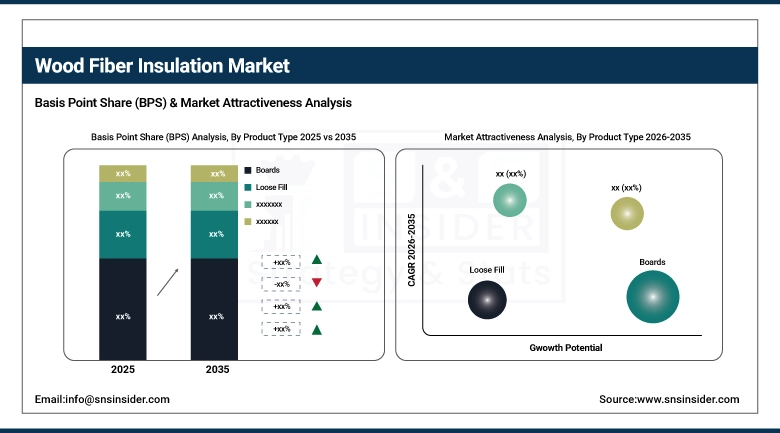

By Product Type, Boards dominated with 42.56% in 2025, and Mats & Rolls / Batts are expected to grow at the fastest CAGR of 7.73% from 2026 to 2035.

-

By Material Source, Virgin Wood Fiber dominated with 55.78% in 2025, and Recycled/Waste Wood Fiber is expected to grow at the fastest CAGR of 7.28% from 2026 to 2035.

-

By Application, Residential Construction dominated with 48.36% in 2025, and Commercial & Institutional Buildings are expected to grow at the fastest CAGR of 7.15% from 2026 to 2035.

-

By Distribution Channel, Direct Sales (B2B) dominated with 38.47% in 2025, and E-Commerce / Online Platforms are expected to grow at the fastest CAGR of 8.86% from 2026 to 2035.

By Product Type, Boards Lead Wood Fiber Insulation Market While Mats & Rolls / Batts Set for Fastest Growth 2026 to 2035

Boards hold the leading share in the wood fiber insulation product type segment because of their structural rigidity, ease of handling in commercial and industrial building applications, and compatibility with external wall insulation systems where dimensional stability under weathering and mechanical fastening loads is a product performance requirement. Mats, rolls, and batts are the fastest-growing format because residential construction and renovation activity generates demand for flexible products that adapt to irregular stud spacings and rafter cavities without the cutting waste associated with rigid boards. Loose fill holds a steady position primarily in attic insulation applications where blown installation methods allow complete coverage of irregular spaces and penetrations.

By Material Source, Virgin Wood Fiber Leads While Recycled/Waste Wood Fiber Shows Fastest Growth in Wood Fiber Insulation Market 2026 to 2035

Virgin wood fiber remains the dominant material source because of its consistent fiber length, moisture content, and density characteristics that allow manufacturers to produce insulation products with predictable thermal performance and mechanical properties at production scale. Recycled and waste wood fiber is the fastest-growing source because of sustainability procurement requirements in commercial and institutional building projects and improving processing technologies that allow manufacturers to achieve consistent product quality from post-industrial and post-consumer wood waste streams. Composite wood fiber blends occupy a middle position, used by manufacturers seeking to optimize cost and performance by combining virgin and recycled fiber content at proportions that meet specification requirements without incurring the full cost premium of all-virgin production.

By Application, Residential Construction Leads Wood Fiber Insulation Market While Commercial & Institutional Buildings Show Fastest Growth 2026 to 2035

Residential construction generates the highest volume demand for wood fiber insulation because wall, roof, and floor insulation requirements in housing affect the largest installed area of any single building type, and wood fiber products have achieved strong specification penetration in the high-performance new-build and deep renovation segments that are growing within the broader residential market. Commercial and institutional buildings are the fastest-growing application segment because energy performance benchmarking requirements, green building certification targets, and net-zero carbon commitments from public sector and institutional building owners are driving insulation upgrade activity in the existing commercial stock at rates that residential renovation alone does not match. Industrial buildings represent a stable and growing application as facility operators in food processing, agriculture, and logistics seek diffusion-open insulation solutions that manage condensation risk in production environments.

By Distribution Channel, Direct Sales (B2B) Leads and E-Commerce / Online Platforms Show Fastest Growth in Wood Fiber Insulation Market 2026 to 2035

Direct B2B sales remain the largest distribution channel because the predominant buyers of wood fiber insulation are construction contractors, insulation installers, and building product distributors who purchase on account, require technical product support, and place orders large enough to justify direct manufacturer or regional distributor relationships. E-commerce and online platforms are the fastest-growing channel because homeowner-led renovation activity, self-build housing, and the growing availability of technical product information through manufacturer and third-party websites have made direct purchasing practical for non-trade buyers who previously depended on builder merchants. Retail and home improvement chains maintain a steady share in markets where wood fiber insulation has achieved sufficient consumer brand recognition to sit alongside conventional insulation products on shelf.

Wood Fiber Insulation Market Regional Analysis

North America Wood Fiber Insulation Market Insights

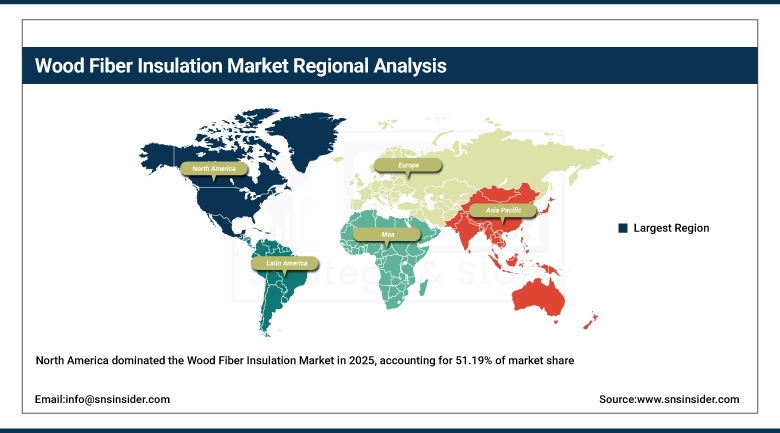

North America held a 51.19% share of the global Wood Fiber Insulation Market in 2025 at USD 490.55 Million, growing at a CAGR of 7.06% through 2035. The region's market is anchored by residential construction activity in markets where high-performance and Passive House building standards have gained traction among architects and custom home builders, combined with commercial retrofit demand generated by state and municipal energy benchmarking programs that create financial incentive for building owners to improve thermal envelope performance. The presence of domestic production in North America, including TimberHP's manufacturing facility in Maine, reduces import dependency for U.S. and Canadian buyers and has supported regional market development by lowering the logistics cost barrier that previously limited wood fiber insulation adoption outside specialty building circles.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Wood Fiber Insulation Market Insights

The United States dominated North America's wood fiber insulation market at 70.41%, USD 345.40 Million in 2025. The U.S. is the largest single national market in North America and the primary driver of regional growth, with demand concentrated in the residential high-performance construction segment in the Northeast and Pacific Northwest, supplemented by commercial retrofit activity in states with active energy benchmarking and disclosure programs. U.S. market development has been supported by green building certification adoption, where LEED, WELL, and Living Building Challenge projects frequently specify bio-based insulation materials to meet material health and embodied carbon criteria that conventional mineral fiber and foam products do not address.

Europe Wood Fiber Insulation Market Insights

Europe held 26.37% at USD 252.70 Million in 2025, growing at a CAGR of 5.37% through 2035. The EU's Energy Performance of Buildings Directive and national renovation wave programs create a policy-driven retrofit market that provides consistent demand for insulation upgrade activity independent of new construction volume cycles. Germany, Austria, France, and Switzerland generate the highest commercial and residential wood fiber insulation specification volumes in the region, supported by a domestic manufacturing base that includes STEICO, Gutex, Homatherm, and Pavatex among others. European consumers and building professionals have historically shown greater willingness to pay material cost premiums for natural fiber insulation products relative to North American and Asian markets, a purchasing culture that sustains premium product positioning for established European brands.

Germany Wood Fiber Insulation Market Insights

Wood Fiber Insulation was the leading wood fiber insulation market in Germany in 2025, considering the heavy activities taking place in the building sector due to KfW energy efficiency programs funding, the high number of Passive House constructions requiring wood fiber insulation layers installed continuously in the exterior walls of buildings, and the fact that STEICO SE and other wood fiber insulation manufacturers operate in Germany, making it the largest consuming country and the largest producer country of this insulation type in the world.

Asia Pacific Wood Fiber Insulation Market Insights

Asia Pacific is the fastest-growing region at a CAGR of 7.37% through 2035, valued at USD 133.40 Million in 2025 and projected to reach USD 270.97 Million by 2035. Japan, South Korea, Australia, and the ASEAN economies represent a spectrum of wood fiber insulation adoption from more developed markets in Australia and Japan where timber construction and natural building material preferences create a receptive environment for wood fiber products, to earlier-stage growth markets in Vietnam, India, and Indonesia where commercial construction activity is scaling faster than insulation product specification sophistication has historically required. India's expanding premium residential and commercial construction market in Bengaluru, Hyderabad, and Pune is generating demand for higher-performance insulation solutions as building energy codes tighten and developer differentiation through green building certification becomes a marketing priority.

China Wood Fiber Insulation Market Insights

China is the leading player in the Asia Pacific wood fiber insulation market owing to the large construction industry, high demand for sustainable materials, and government’s emphasis on energy efficiency in infrastructure. Urbanization and growth in construction projects have also helped China maintain its market leadership.

Latin America (LATAM) and Middle East & Africa (MEA) Wood Fiber Insulation Market Insights

Latin America and Middle East and Africa together represent the smallest but steadily growing portions of the global wood fiber insulation market, at USD 48.97 Million and USD 32.68 Million respectively in 2025. Latin America's market is growing at a CAGR of 3.76% through 2035, with Brazil and Mexico providing the largest national demand bases within the region as residential construction activity and growing awareness of thermal comfort requirements in both hot and temperate climate zones expand the addressable insulation market beyond the conventional mineral wool and foam products that dominate current specification. MEA is growing at a CAGR of 4.31% through 2035, with Gulf construction markets and South Africa representing the most active early adopters of natural fiber insulation materials in a region where the category is still in early market development stages.

Competitive Landscape for Wood Fiber Insulation Market:

STEICO SE, headquartered in Feldkirchen near Munich, Germany, is the global market leader in wood fiber insulation by production capacity and revenue, manufacturing a full range of wood fiber insulation boards, flexible batts, and loose fill products distributed through building merchant and specialty insulation distributor networks across Europe and increasingly into North American and export markets. STEICO's manufacturing operations in Germany and Poland give it cost and logistics advantages in the European market that smaller regional producers have difficulty matching at scale.

-

In 2024, STEICO SE expanded production throughput at its Czarna Woda facility in Poland to address rising demand from the French and UK commercial renovation markets, with the expansion focused on flexible wood fiber batt production lines where order backlogs had extended delivery lead times for distributor partners beyond their standard stocking cycle targets.

Gutex Holzfaserplattenwerk H. Henselmann GmbH & Co. KG, located in Waldshut-Tiengen, Germany, has the longest tradition, having a wide range of products such as wood fiber rigid boards, rolls, and special facade insulation panels that serve as insulation composite materials for the external walls of buildings. The focus on natural resin binders and diffusion-open constructions of the company allows placing Gutex's products in the high-end category in the European market due to the constant demand for natural fiber insulation created by architects' specification for energy renovation projects.

- In 2024, Gutex launched its Thermowall UD-Q product line into the UK market through a specialist natural building materials distributor partnership, targeting the growing segment of self-builders and retrofit contractors working on Passivhaus and EnerPHit certified projects where the combination of thermal performance and diffusion-open construction is a core design requirement rather than a product preference.

Wood Fiber Insulation Market Key Players:

Some of the Wood Fiber Insulation Market Companies are:

-

STEICO SE

-

Gutex Holzfaserplattenwerk H. Henselmann GmbH & Co. KG

-

TimberHP

-

Knauf Insulation

-

Soprema (Pavatex)

-

Saint-Gobain ISOVER

-

Pavatex SA

-

Natufiber Insulation Manufacturing Company LLC

-

Thermofloc

-

Cellulose Works

-

Unger-Diffutherm Holzwerkstoffe GmbH

-

Homatherm GmbH

-

Finsa

-

HOMANIT GmbH & Co. KG

-

Kronospan

-

Greenfiber International

-

Celenit S.p.A.

-

Best Wood Schneider GmbH

-

Sonae Arauco

-

Masonite International Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 958.30 Million |

| Market Size by 2035 | USD 1785.04 Million |

| CAGR | CAGR of 6.45% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Boards, Loose Fill, Mats & Rolls / Batts, and Others (e.g., Pellets, Molded Shapes)) • By Material Source (Virgin Wood Fiber, Recycled/Waste Wood Fiber, and Composite Wood Fiber Blends) • By Application (Residential Construction, Commercial & Institutional Buildings, Industrial Buildings, and Retrofit & Renovation Projects) • By Distribution Channel (Direct Sales (B2B), Distributors & Dealers, E-Commerce / Online Platforms, and Retail/Home Improvement Chains) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | STEICO SE, Gutex Holzfaserplattenwerk H. Henselmann GmbH & Co. KG, TimberHP, Knauf Insulation, Soprema (Pavatex), Saint‑Gobain ISOVER, Pavatex SA, Natufiber Insulation Manufacturing Company LLC, Thermofloc, Cellulose Works, Unger‑Diffutherm Holzwerkstoffe GmbH, Homatherm GmbH, Finsa, HOMANIT GmbH & Co. KG, Kronospan, Greenfiber International, Celenit S.p.A., Best Wood Schneider GmbH, Sonae Arauco, Masonite International Corporation. |

Frequently Asked Questions

North America led the Wood Fiber Insulation Market in 2025 with a 51.19% share.

Boards dominated the Wood Fiber Insulation Market with a 42.56% share in 2025.

Key drivers include rising building energy efficiency mandates, increasing preference for bio-based and sustainable construction materials, and growing commercial building retrofit activity in both developed and emerging markets.

The Wood Fiber Insulation Market size was USD 958.30 Million in 2025 and is projected to reach USD 1,785.04 Million by 2035.

The Wood Fiber Insulation Market is expected to grow at a CAGR of 6.45% from 2026-2035.

Get in Touch