Window Films Market Report Scope & Overview:

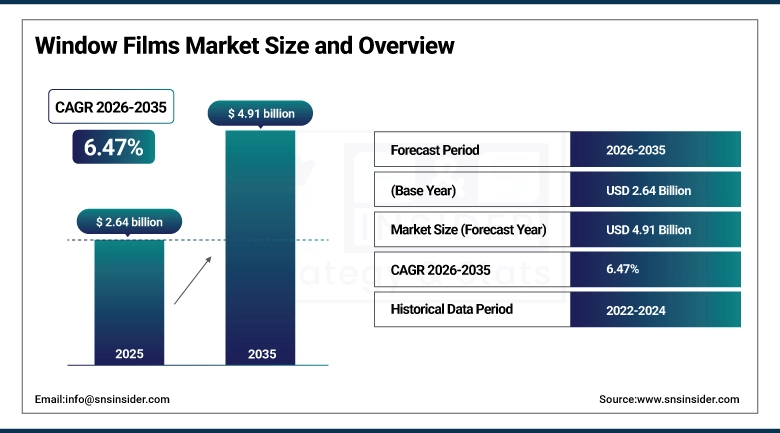

The Window Films Market size was valued at USD 2.64 Billion in 2025 and is projected to reach USD 4.91 Billion by 2035, growing at a CAGR of 6.47% during 2026-2035.

The Window Films Market is expected to experience high growth rates due to several factors. These include higher energy prices encouraging building owners to turn to solar control technologies, stricter vehicle safety laws enforcing the use of laminated glass window films, increased interest in privacy and decoration uses in offices and commercial establishments, and heightened UV protection concerns in both residential and automobile industries. Urbanization in Asia Pacific, along with green building initiatives incentivizing buildings' ability to reduce solar heat gain, is driving the use of ceramic and multi-layer window films in commercial buildings at a rate that countries such as Vietnam and Indonesia have never witnessed before.

Market Size and Forecast:

-

Market Size in 2025: USD 2.64 Billion

-

Market Size by 2035: USD 4.91 Billion

-

CAGR of 6.47% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Window Films Market - Request Free Sample Report

Key Window Films Market Trends

-

Rising adoption of ceramic window films in commercial buildings, replacing older metalized films whose signal interference with mobile networks and vehicle GPS receivers had become an operational liability for building operators and fleet managers.

-

Automotive OEM partnerships with film manufacturers are expanding, with 3M and Eastman Chemical embedding window film technology directly into new vehicle glass specifications rather than relying solely on the aftermarket installation channel.

-

Safety and security film procurement by government buildings, embassies, and critical infrastructure facilities accelerated through 2024 after updated blast mitigation standards in the U.S. and UK made glazing protection a compliance requirement rather than a discretionary upgrade.

-

Smart window film technology, incorporating electrochromic and photochromic switching layers that adjust tint on demand, moved from pilot installation to commercial availability in premium commercial and hospitality building projects across North America and Europe.

-

Growth in decorative and privacy film segments is being driven by interior design trends in corporate offices and retail environments where frosted, patterned, and digitally printed films are replacing physical partition walls and traditional window treatments at lower installed cost with better flexibility for layout changes.

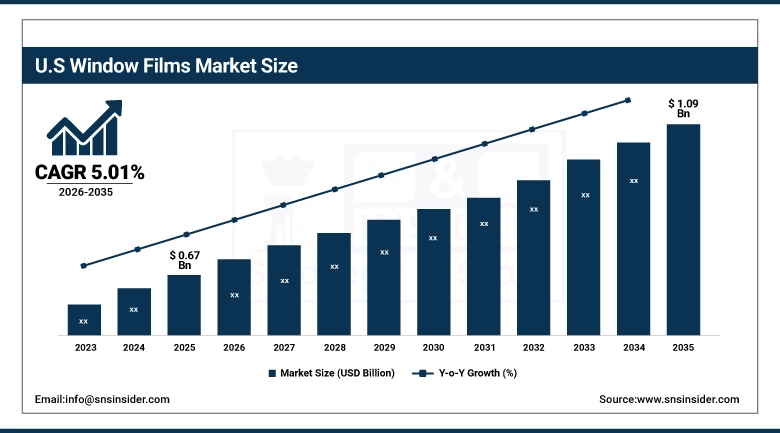

The U.S. Window Films Market size was valued at USD 0.67 Billion in 2025 and is projected to reach USD 1.09 Billion by 2035, growing at a CAGR of 5.01% during 2026-2035. The U.S. market is the largest single national market globally, anchored by a mature automotive aftermarket installation network, state-level energy code requirements that incentivize commercial solar control film retrofits, and sustained demand from federal and state government facilities upgrading window glazing protection under post-2020 security hardening programs.

Window Films Market Growth Drivers:

-

Window Films Market Demand Accelerates as Energy Efficiency Mandates, Automotive Safety Regulations, and Commercial Building Retrofit Programs Drive Adoption Across All Major Segments and Geographies

The commercial building retrofit market is the strongest near-term demand driver in developed economies. Buildings account for roughly 40% of total energy consumption in the U.S. and EU, and solar control window film is one of the few upgrades that delivers measurable reduction in cooling load without requiring structural work or window replacement. A 3M Prestige series or Eastman LLumar ClimatePro installation on a south- and west-facing office block in Phoenix or Singapore can reduce solar heat gain through glass by 60-80%, cutting air conditioning load and qualifying the building for LEED or BREEAM energy performance credits that influence tenant attraction and insurance rates.

Eastman Chemical's LLumar brand, the world's largest window film brand by installed base, reported that its commercial segment revenue grew at a double-digit rate in 2024, with APAC markets including India and Southeast Asia accounting for the fastest regional expansion as new commercial real estate projects incorporated solar control film specifications from design stage rather than as post-occupancy retrofits.

Window Films Market Restraints:

-

Window Films Market Growth Constrained by Installation Quality Variability, Regulatory Complexity Around Visible Light Transmission Limits, and Competition from Alternative Glazing Technologies in New Construction Segments

The window film market's most persistent structural constraint is quality inconsistency in the installer base, particularly in price-sensitive automotive and residential segments where unlicensed low-cost installers using inferior film products have damaged category reputation through premature delamination, bubbling, and colour shift. That reputation damage affects premium product sell-through at retail because buyers conflate bad installation experiences with product quality. Regulatory fragmentation compounds this: visible light transmission limits for automotive window tinting vary by state in the U.S. and by country globally, requiring film manufacturers to maintain multiple product variants and making compliance navigation a deterrent for smaller dealers. In new commercial construction, low-emissivity coated glass and double-glazed units built into the facade from design stage increasingly deliver solar control performance that post-installation films can't materially improve, limiting window film's addressable market in that sub-segment.

Window Films Market Opportunities:

-

Smart Switchable Films, Asia Pacific Building Construction Growth, Safety Film Compliance Mandates, and Decorative Film Adoption in Corporate Interiors Create Meaningful Market Opportunities Through 2035

Smart and switchable window films represent the highest-value growth vector in the product category. PDLC (Polymer Dispersed Liquid Crystal) and SPD (Suspended Particle Device) films, which transition from clear to opaque on electrical command, are moving out of high-end hospitality into corporate office, healthcare, and residential luxury applications as unit costs fall with scale. Saint-Gobain's SageGlass and Eastman's Vision VarioShade products both saw expanded commercial project specification lists in 2024. Asia Pacific's commercial real estate pipeline, which includes India's office park construction in Hyderabad and Bengaluru and Vietnam's export manufacturing zone development, creates a volume opportunity for solar control films that has no historical precedent in those markets.

3M's window films division reported commercial project wins in 2024 that included the retrofit of more than 2 million square feet of commercial glazing across Southeast Asian markets, with building owners citing payback periods of 3-5 years on solar control film investment through air conditioning energy savings alone, a return profile that property managers increasingly present to building owners as a straightforward capital allocation decision rather than a discretionary upgrade.

Window Films Market Segment Analysis

-

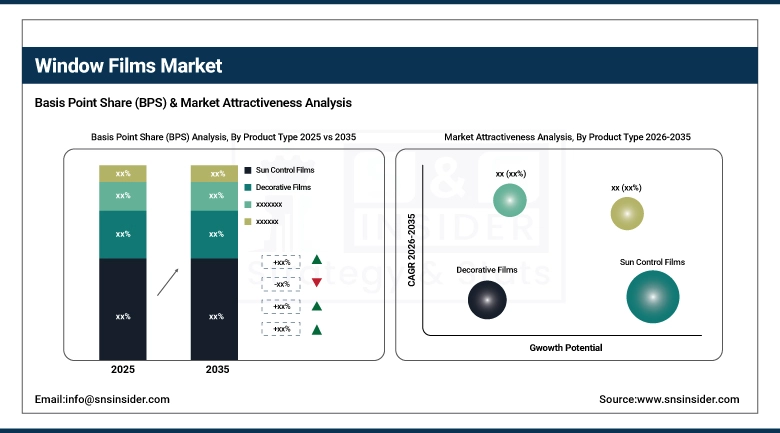

By Product Type, Sun Control Films dominated with 38.26% in 2025, and Safety & Security Films are expected to grow at the fastest CAGR of 7.48% from 2026 to 2035.

-

By Material Type, Polyester (PET) Films dominated with 41.63% in 2025, and Ceramic Films are expected to grow at the fastest CAGR of 7.87% from 2026 to 2035.

-

By Application, Automotive dominated with 36.58% in 2025, and Commercial is expected to grow at the fastest CAGR of 7.22% from 2026 to 2035.

-

By End-User Industry, Building & Construction dominated with 39.18% in 2025, and Building & Construction is also expected to grow at the fastest CAGR of 7.02% from 2026 to 2035.

By Product Type, Sun Control Films Lead Window Films Market While Safety and Security Films Set for Fastest Growth 2026 to 2035

Heat reduction films hold a dominant position owing to their excellent capacity for heat absorption, reduction of glare, and UV filtering. Safety and security films are becoming increasingly popular because of growing consumer concern about security from burglary, accidents, and environmental threats. The contribution of decorative and privacy films is significant as well because of increasing demand for beautification.

By Material Type, Polyester Films Lead While Ceramic Films Set for Fastest Growth in Window Films Market 2026 to 2035

The polyester film type is dominant due to its durability, transparency, and economy, thus rendering it fit for various uses. On the other hand, the ceramic type is gaining popularity as an excellent option due to its heat rejection capability, friendly signaling, and lack of metal. The vinyl and others fall in a niche market based on aesthetic and customization needs.

By Application, Automotive Leads Window Films Market While Commercial Applications Show Fastest Growth 2026 to 2035

Automotive usage remains at the forefront because window film is used extensively in these fields for heat rejection, protection against UV rays, and better driving experience. Commercial uses have witnessed significant growth due to the rising need for energy-saving buildings and infrastructure developments. Usage in the residential sector has also risen because of the rising demand for comfortable interiors.

By End-User Industry, Building and Construction Leads and Maintains Fastest Growth in Window Films Market 2026 to 2035

The dominant player in this market is the building and construction industry because of the extensive use of window films as an important aspect of conserving energy and ensuring efficiency and environmental sustainability in buildings. There will be continued growth in this industry as the green movement picks up pace around the globe. The automotive industry is also an important one when it comes to usage of window films.

Window Films Market Regional Analysis

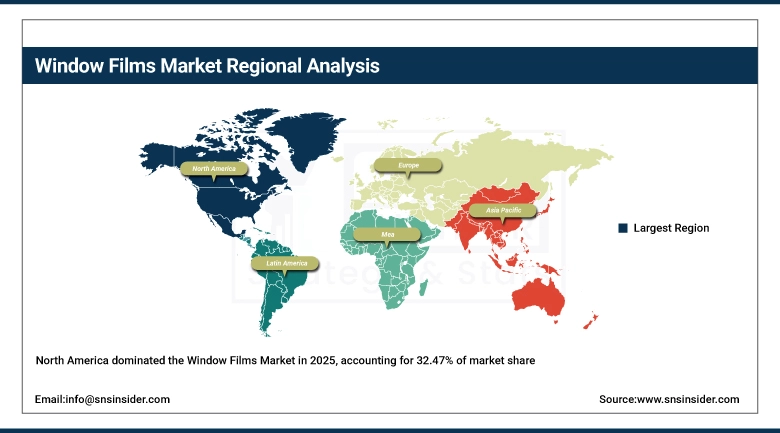

North America Window Films Market Insights

North America held a 32.47% share of the global Window Films Market in 2025 at USD 0.86 Billion, growing at a CAGR of 5.31% through 2035. The region's market is built on the world's most developed professional window film installer network, where IWFA (International Window Film Association) certification programs set installation standards that protect product reputation. Commercial retrofit demand driven by state energy codes in California, New York, and Texas, combined with federal building security upgrade programs across the GSA portfolio, provides a policy-backed demand floor independent of construction cycles.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Window Films Market Insights

The United States dominated North America's window film market at 78.36%, USD 0.67 Billion in 2025. The U.S. remains the global reference market for window film technology development, distribution, and installation practice, with 3M's St. Paul operations and Eastman Chemical's LLumar division in Fieldale, Virginia both headquartered domestically. The aftermarket automotive channel, the commercial building retrofit market, and the government security film program combine to create a buyer base broader and deeper than any other single national market.

Europe Window Films Market Insights

Europe held 27.83% at USD 0.73 Billion in 2025, growing at a CAGR of 5.46% through 2035. The EU's Energy Performance of Buildings Directive, which requires progressive improvement in building energy ratings across member states, creates a compliance-driven retrofit market for solar control films in the existing building stock that runs independently of new construction volume. The UK, Germany, France, and the Benelux countries generate the highest commercial film specification volumes in the region. ORAFOL's German manufacturing base and HEXIS's French operations make Europe one of the few regions with significant domestic window film production capacity.

Germany Window Films Market Insights

Germany was the leading market for window films in Europe in 2025 due to factors such as Germany’s high number of commercial property buildings which required energy retrofitting, the auto sector in Germany producing downstream sales for installed film, and the presence of ORAFOL Europe as the local window film manufacturer.

Asia Pacific Window Films Market Insights

Asia Pacific is the fastest-growing region at 8.84% CAGR through 2035, valued at USD 0.65 Billion in 2025 and projected to reach USD 1.51 Billion by 2035. Japan, South Korea, Australia, and the ASEAN economies between them represent the full spectrum of window film adoption from mature automotive markets in Japan and Korea where ceramic film has displaced metalized film as the standard aftermarket specification, to fast-growing commercial construction markets in Vietnam and Indonesia where solar control film is being specified in new office and retail buildings as a cost-effective alternative to high-performance glazing systems. India's growing automotive fleet and expanding premium commercial real estate market in Bengaluru, Hyderabad, and Pune add a large and accelerating national demand base.

China Window Films Market Insights

China dominated the Asia Pacific Window Films Market in 2025. Domestic manufacturers including FILMTACK and NEXFIL compete alongside 3M, Eastman LLumar, and Saint-Gobain in a market where the automotive aftermarket channel is the largest by volume and the commercial building retrofit channel is the fastest growing. China's green building certification program under MOHURD's three-star standard increasingly credits solar control film installation as part of building energy performance assessments, creating a policy incentive that aligns developer and tenant interests around film specification.

Latin America (LATAM) and Middle East & Africa (MEA) Window Films Market Insights

The Latin American and MEA film window market is growing at a healthy pace due to increased construction activity, urbanization, and energy efficiency consciousness. Hot weather is driving the need for use of solar control films for buildings and automobiles. Growth of the automobile industry and infrastructure development are aiding in market growth. Improving economic performance and emphasis on sustainability are adding to growth potential in the market.

Competitive Landscape for Window Films Market:

3M Company, headquartered in St. Paul, Minnesota, is the global leader in window film technology across automotive, commercial, and safety segments. Its Scotchshield, Prestige, and Ceramic Series product lines cover the full performance spectrum from entry-level dyed films to premium multi-layer ceramic constructions, distributed through a certified dealer network that spans over 100 countries.

-

In 2024, 3M launched its Prestige Series PR 70 ceramic automotive film, achieving 99% infrared rejection at visible light transmission levels that comply with tinting regulations in all 50 U.S. states and key export markets including Australia and the Gulf states, with the product specifically designed to address the signal interference complaints that had pushed automotive fleet operators away from metalized film products.

Eastman Chemical Company, headquartered in Kingsport, Tennessee, operates the world's largest window film brand by installed base through its LLumar and Vista divisions, covering automotive aftermarket, commercial retrofit, and residential applications across a global installer network of over 85,000 professional dealers. Eastman's acquisition of the V-KOOL brand in Southeast Asia and its integration of huper optik's ceramic technology into the LLumar ClimatePro range gave it product and distribution coverage across the full Asia Pacific growth corridor that no other Western window film manufacturer matches at comparable scale.

- In 2024, Eastman expanded its LLumar manufacturing capacity at its Fieldale, Virginia facility to address order backlogs in the commercial retrofit segment, with the expansion specifically targeting the ceramic film production lines where demand growth from APAC commercial projects had stretched delivery timelines beyond the 4-week standard the company had historically maintained for distributor stocking orders.

Window Films Market Key Players:

Some of the Window Films Market Companies are:

-

3M Company

-

Eastman Chemical Company

-

Avery Dennison Corporation

-

Saint-Gobain S.A.

-

Madico Inc.

-

Toray Industries Inc.

-

Garware Hi-Tech Films Ltd.

-

Johnson Window Films Inc.

-

Armolan Window Films

-

Reflectiv

-

American Standard Window Film

-

LINTEC Corporation

-

ORAFOL Europe GmbH

-

HEXIS S.A.S.

-

NEXFIL Co., Ltd.

-

Rayno Window Film

-

Global Window Films Inc.

-

Konica Minolta Inc.

-

FILMTACK PTE Ltd.

-

XPEL Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.64 Billion |

| Market Size by 2035 | USD 4.91 Billion |

| CAGR | CAGR of 6.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Sun Control Films, Decorative Films, Safety & Security Films, and Privacy Films) • By Material Type (Polyester (PET) Films, Vinyl Films, Ceramic Films, and Metalized / Other Specialty Films) • By Application (Automotive, Residential, Commercial, and Marine / Others) • By End-User Industry (Automotive Industry, Building & Construction, Marine & Aerospace, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M Company, Eastman Chemical Company, Avery Dennison Corporation, Saint-Gobain S.A., Madico Inc., Toray Industries Inc., Garware Hi-Tech Films Ltd., Johnson Window Films Inc., Armolan Window Films, Reflectiv, American Standard Window Film, LINTEC Corporation, ORAFOL Europe GmbH, HEXIS S.A.S., NEXFIL Co., Ltd., Rayno Window Film, Global Window Films Inc., Konica Minolta Inc., FILMTACK PTE Ltd., XPEL Inc. |

Frequently Asked Questions

North America led the Window Films Market in 2025 with a 32.47% share.

Sun Control Films dominated the Window Films Market with a 38.26% share in 2025

Key drivers include rising energy efficiency mandates, automotive safety regulations, and increasing demand for UV protection and privacy solutions.

The Window Films Market size was USD 2.64 Billion in 2025 and is projected to reach USD 4.91 Billion by 2035.

The Window Films Market is expected to grow at a CAGR of 6.47% from 2026–2035.

Get in Touch