Wound Gel Market Report Scope & Overview:

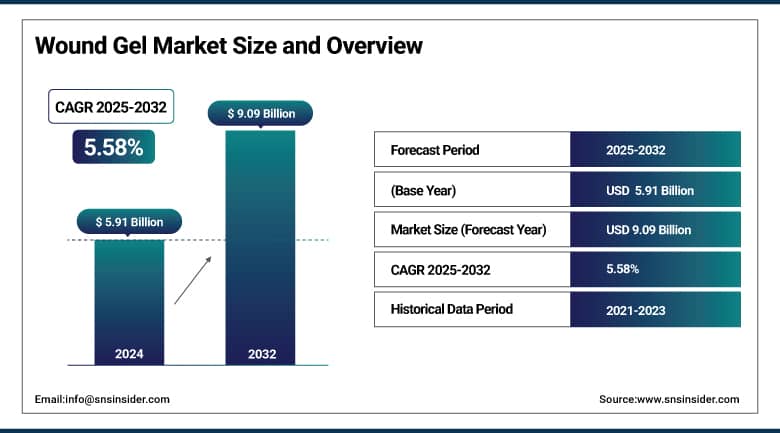

The Wound Gel Market size was valued at USD 5.91 billion in 2024 and is expected to reach USD 9.09 billion by 2032, growing at a CAGR of 5.58% over the forecast period of 2025-2032.

The increase in chronic wounds, burns, diabetic ulcers, and post-surgical infections represents a steady rise in the global wound gel market. The market is being boosted by factors such as increased demand for improved wound care solutions, rising knowledge about infection management, and the increasing number of outpatient and homecare therapies. The adoption is also powered by technological advancements in gel formulations—silver-based and bioactive gels are some of them. Moreover, developed regions possess favorable healthcare infrastructure and reimbursement policies, which further propel the market growth.

For instance, according to NCBI, the global pooled prevalence of diabetic foot ulceration is estimated at 6.3%. Among all regions, North America reports the highest prevalence at 13%, while Oceania records the lowest at 3%. Africa's prevalence stands at 7.2%, slightly higher than Asia's 5.5%. The condition is observed to be more common in male patients with diabetes (4.5%) compared to female patients (3.5%). Additionally, patients with type 2 diabetes mellitus (T2DM) exhibit a higher prevalence of foot ulceration at 6.4%, compared to 5.5% in those with type 1 diabetes mellitus (T1DM).

To Get More Information On Wound Gel Market - Request Free Sample Report

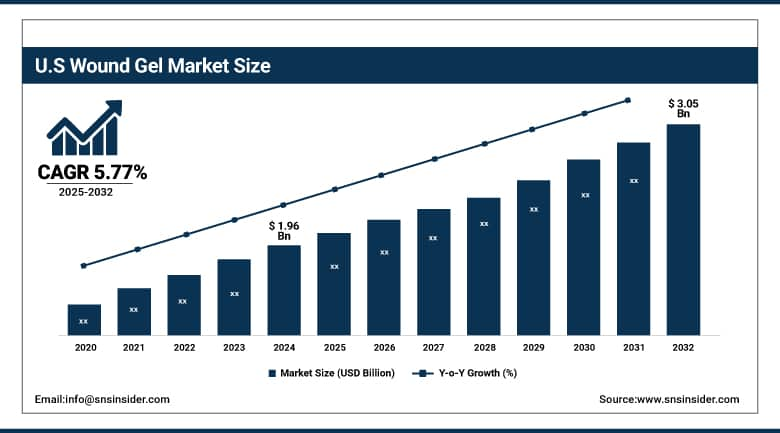

The U.S. Wound Gel Market size was valued at USD 1.96 billion in 2024 and is expected to reach USD 3.05 billion by 2032, growing at a CAGR of 5.77% over the forecast period of 2025-2032.

The wound gel market growth in North America is led by the U.S. owing to its superior healthcare infrastructure, concentration on the management of chronic wounds, and adoption of novel technologies for wound care. This, coupled with a high degree of awareness among healthcare professionals and low reimbursement by insurance companies for other treatment modalities, is expected to drive higher adoption of wound gel products across clinical and homecare settings in the country.

Wound Gel Market Dynamics:

Drivers

-

Rising Prevalence of Chronic Wounds is Driving the Market Growth

Diabetes, obesity, and vascular diseases are on the rise, and thus, chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers are becoming a greater burden on the globe. In contrast, chronic wounds generally require long-term treatment and generally delicate care in the management of the wound, owing to the unavoidable development of infections and gradual restoration of tissue. The absence of these conditions is where the wound gels are especially useful, due to they create a moist environment, facilitate autolytic debridement, and promote expedited healing. The need for clinically effective, easy-to-apply gel-based dressings is steadily increasing, especially as healthcare systems struggle to care for patients requiring long-term wound management, making this one of the key drivers for growth in the market.

Globally, between 1.17 and 2.68 patients are diagnosed with chronic wounds per 1,000 people, with the most frequently affected age groups being older adults. Approximately 2% of the U.S. population has chronic wounds, driven largely by a need for treatment among the nearly 30 million people with diabetes in the United States.

-

Shift toward home-based care and self-treatment is accelerating the Market Growth

Increasing preference for self-managed wound care, especially for minor wounds and chronic wounds that do not need to be hospitalized. With the convenience, affordability, and ease of use of wound gels, more patients and caregivers are resorting to over-the-counter gel products. The transformation is attributed to the penetration of E-commerce platforms, rising health concerns, and the need for a low-cost solution for healthcare costs. Furthermore, development in the formulation of wound gels has made them much safer, with a higher success rate for home use. Consequently, the demand for consumer health segment-based easy-to-use wound gels is growing in the elderly population and remote areas with no medical means.

A dedicated mobile app, WoundAIssist, was recently launched for remote wound assessment and monitoring—a harbinger of speeding digital health advances in homecare wound management

Restraint

-

Availability of Alternative Wound Care Methods is Restraining the Market from Growing

The availability of alternative wound care products such as traditional gauze dressings, ointments, foams, hydrocolloids, and natural remedies is are restraining factor towards the growth of the wound gel market trends. In a number of healthcare systems, specifically in developing and low-resource areas, medical professionals and patients make choices for these substitutes as a result of their low price, common use, and intensive availability. Conventional dressings and local ointments have received a long tradition of use to treat minor wounds and are deeply rooted in local clinical practices. Besides, natural or herbal remedies are still popular in some cultures, thus hampering the advancement of advanced solutions such as wound gels. The competition of substitute products is slowing the market penetration of wound gels, especially in low and middle-income countries.

Wound Gel Market Segmentation Analysis:

By Product

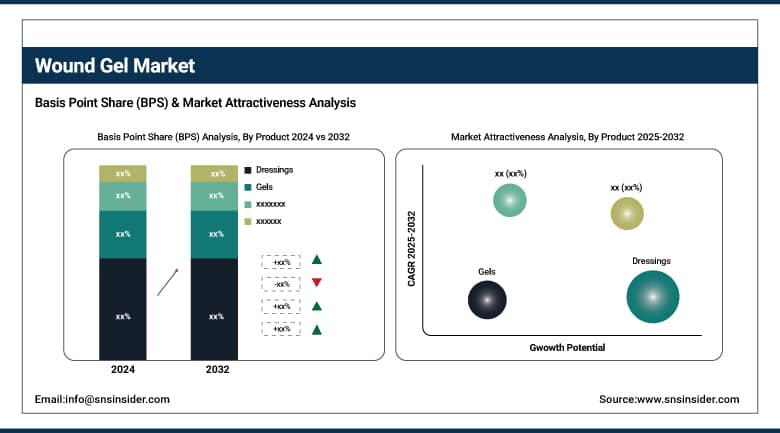

The dressings segment dominated the wound gel market with a 74.10% market share in 2024, owing to their extensive applications in both acute and chronic wound care. Wound gels with /Embedding dressings allow dressings to have improved physical moisture retention and infection control ability, and easy application, which are beneficial not only in clinical conditions but also at home. Their ability to handle different types of wounds, from pressure ulcers and diabetic foot ulcers to post-surgical ones, and special antimicrobial versions has made them a market leader.

During the forecast period, the Gels segment is anticipated to observe the fastest growth. This is due to the rising demand for wound treatment solutions, which promote quick healing and lower the risk of infection, driving this market growth. Wound gels, particularly those with bioactive or silver-based components, are also emerging more widely as they can keep a moist environment and facilitate autolytic debridement. Moreover, increasing awareness regarding wound cleanliness and the migration towards non-surgical treatment are likely to propel the use of standalone products based on gels.

By Antimicrobial Properties

The silver (Ag+) segment dominated the wound gel market with an 82.16% market share in 2024, and this is due to its effectiveness in treating infections and aiding in the healing process. BackgroundSilver-containing wound gels are common in treating chronic and acute wounds in clinical practice, particularly in the case of wounds at high infection risk. Healthcare providers prefer these metals due to their predominant antimicrobial activity against bacteria, fungi, and biofilms. Rising prevalence of chronic wounds, such as diabetic foot ulcers and pressure ulcers, is another high-impact rendering growth growth-driving factor, augmenting demand for silver-infused products in the market targeting the wound care segment.

The non-silver segment is anticipated to witness the fastest growth during the projected period. The increase is due to the rising concern regarding the resistance to silver, cytotoxicity, and the higher cost of silver-based products. Non-silver wound gels, usually containing anti–microbials, enzymes, or synthetic substances, appear to be one of the most secure, inexpensive substitutes for mild to moderate wounds. Moreover, rising preferences for organic and biocompatible wound care solutions (mostly, in homecare environments) are boosting the preference for non-silver wound gels.

By Mode of Purchase

The prescription segment dominated the wound gel market with an 88.50% market share in 2024 due to the advanced wound gels are primarily used for chronic wounds, post-surgical care, and infections, require supervision before using the same; they are allegedly prescribed in nature as observed in the past 4- 5 years period. Wound gels available over the counter are not usually suitable for complicated cases, and healthcare providers usually suggest the use of prescription-grade wound gels containing specific metals such as silver ions, antibiotics, or bioactive compounds for the best results. Moreover, growing reimbursement support for prescribed wound care products in clinical and long-term care settings has also helped this segment maintain its dominance.

High demand for self-care, coupled with increasing consumer awareness, is projected to drive the rapid growth of the Non-prescription segment over the forecast years. Among them, topical wound gels are gaining an increased adoption rate for minor cuts, burns and abrasions, particularly among home users looking for a rapid treatment option that is easy to access. This growth is further propelled by the increasing sales of painless, non-prescription wound gels on e-commerce platforms and retail pharmacies. Furthermore, product innovations with natural or herbal ingredients have broadened the consumer base in this segment.

By Distribution Channel

With the provision of readily accessible wound gel products through hospital pharmacies, retail drugstores, and medical supply stores, the offline segment dominated the wound gel market in 2024 with a 79.3% market share. Loyalty to offline channels is apparent when it comes to prescription wound gels that may require pharmacist guidance or be a controlled item. Wound dressings for chronic and post-operative wounds require timely and consistent availability in clinical environments, and offline distribution allows for tighter inventory management and product authenticity.

The online segment is the fastest-growing during the forecast years. The growth is mainly associated with the rising use of e-commerce platforms, a growing trend of home-based wound care, and the convenience offered by doorstep delivery. Consumers are also able to seek out more online, including over-the-counter products such as wound gels and plant and herbal formulations, often at low prices. Meanwhile, the increasing penetration of digital health platforms and the direct-to-consumer promotional campaigns on the part of manufacturers are driving the surge in online purchases.

By Application

The chronic wounds segment led the wound gel market with a 58.14% market share in 2024, owing to the global rise in long-duration disease conditions, including diabetic foot ulcers, venous leg ulcers, and pressure sores. Such wounds take a long time to heal and need constant hydration, hence the use of wound gels, particularly the antimicrobial or bioactive wound gels, to provide a better solution. Moreover, chronic wound care with wound gels is significantly contributing to the demand for wound gels due to the increasing incidence of lifestyle diseases and the growing geriatric population in developed and developing regions.

The acute wounds segment is projected to witness the fastest growth during the forecast timeframe. Surging number of surgical procedures, traumatic injuries, and burn cases is fuelling demand for fast-acting, effective wound healing solutions. Wound gels are easily applied in Clinical wound management, making them more common in clinical emergency care and clinical post-operative management for accelerating tissue repair. In addition, increasing awareness regarding wound hygiene and self-treatment of minor injuries is propelling the growth of this division, especially through OTC and online sales channels, which is furthering driving its growth at a faster pace.

By End Use

Hospitals segment dominated the wound gel market with a 43.2% market share in 2024 owing to the high number of inpatient and outpatient procedures with the need of wound management Chronic and post-operational wounds, burns, and trauma are treated in hospitals where wound gels are often needed to prevent infections, heal tissues more quickly, and provide ease and comfort to patients. Moreover, hospital settings contain many skilled health care professionals and prescription-grade, high efficacy products, further leading to the increasing preference for advanced wound gels in this segment. Hospitals are the primary end-users of wound gel products, with reimbursement policies and integrated supply chains augmenting their position.

The homecare settings segment is expected to register the highest growth during the forecast period. Market growth is propelled by an increasing demand for self-treatment, a growing elderly population that requires long-term wound care, and greater availability of consumer-friendly, over-the-counter wound gel items. Decentralization of healthcare services, especially for chronic wounds such as diabetic foot ulcer and pressure ulcer, is driving the growth of the home health market. Additionally, growing access to online purchases and the low cost of non-prescription wound gels is causing patients and caregivers to tend to their smaller to moderate wounds at home.

Regional Analysis:

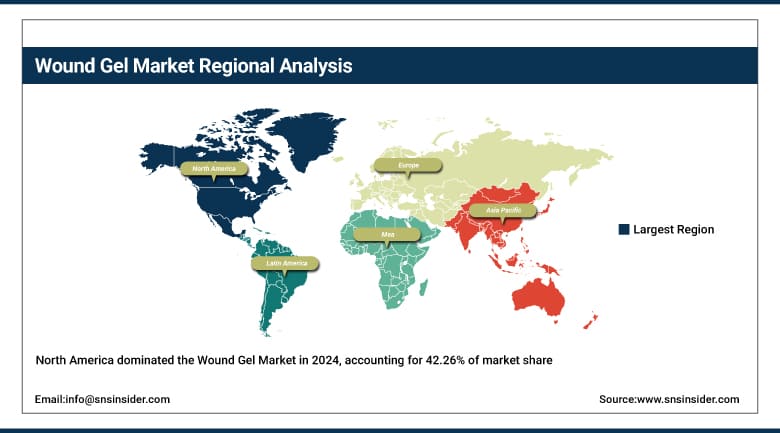

North America dominated the wound gel market with a 42.26% market share in 2024, owing to a well-established healthcare infrastructure, along with a high prevalence rate of chronic wounds and considerable adoption of advanced wound care products. Strong investment dynamics in dispatching and R&D, along with a strong foothold of key market players and favorable reimbursement policy, promote the usage of high-priced wound care products in the region, particularly antimicrobial and bioactive gels. Moreover, an increasing aging population requiring wound care is expected to spur demand in hospitals, clinics, and home care.

Get Customized Report as Per Your Business Requirement - Enquiry Now

The wound gel market in Asia Pacific region is expected to grow at the fastest rate with a 5.66% CAGR over the forecast period due to the increase in healthcare cost, the expanding population preferring various kinds of wound treatment solutions including but not limited to wound gel compositions owing to growing population be affected by wound gel compositions including but not limited to people suffering from diabetes and geriatric populace. China, India, and Japan, for instance, are rapidly improving their healthcare sectors, with increasing coverage and more access to higher-end treatment options. In addition, the increasing number of chronic conditions and surgical procedures is shifting the paradigm toward outpatient care and home care, which, in turn, will fuel the demand for efficient wound gel products in the region.

Europe is experiencing moderate growth in the wound gel market due to mature healthcare systems, rising incidence of chronic and acute wounds, and high R&D investment. Germany, France, and the UK have invested in the development and use of advanced wound management solutions and bioactive materials in healthcare and export innovation and challenges to well-recognized bodies such as the European Wound Management Association (EWMA) that facilitates innovative and educational drive. In addition, the growing geriatric population and increasing surgical volumes in the region are further propelling demand for gel-based products across clinical and home care settings.

The growth of the market in Europe is also driven by innovative initiatives such as smart bioactive gels or more assertive legislation/ grants from the EU (e.g., the 6 million euros European Union Horizon Europe FORCE REPAIR project), developing next-generation gel technologies for wound healing. Moreover, rising adoption as a result of stringent public-private cooperation and increasing focus on infection management will boost the market development, and Europe is anticipated to be a prominent growth pocket for the wound gel market analysis.

The Latin American wound gel market is growing at a significant pace as increasing cases of chronic wounds, such as diabetic foot ulcers and pressure injuries, are expected to be the major factor responsible for the growth of the wound gel market in Latin America. The growing investments in healthcare infrastructure and increasing public awareness about advanced wound therapies, such as hydrogels and antimicrobial gel, are aiding the market space.

Moderate growth in the wound gel market is taking place in the MEA region, backed up by increasing healthcare spending, government influx in the infrastructure, and a growing number of surgical and diabetic wound cases. Even if adoption is uneven, driven by a lack of access to advanced medical products, growing capacity within hospitals and clinics spurs a continued upward trajectory for market adoption.

Key Market Players:

-

3M Company

-

Smith & Nephew plc

-

Mölnlycke Health Care AB

-

Hartmann Group

-

Braun Melsungen AG

-

Medline Industries, Inc.

-

Johnson & Johnson

Recent Developments in the Wound Gel Market:

-

May 2025 – Global medical technology leader Smith+Nephew reported that it has been awarded a single-source, 10-year contract worth up to USD 75 million by the U.S. Department of Defense (DoD) through the Defense Logistics Agency (DLA). The firm will provide its RENASYS◊ TOUCH Negative Pressure Wound Therapy (NPWT) Systems under the agreement to meet military healthcare requirements.

-

January 2024 – The Medical Solutions Business of 3M Health Care, a business expected to spin off as an independent company, was funded with USD 34.2 million by the U.S. Army. The funds will be utilized in the creation of innovative infection prevention solutions, wound management solutions, and wound healing solutions to further extend the company's leadership in advanced wound care.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.91 Billion |

| Market Size by 2032 | USD 9.09 Billion |

| CAGR | CAGR of 5.58% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Dressings, Gels) • By Antimicrobial Properties (Silver (Ag+), Non-Silver) • By Mode of Purchase (Prescription, Non-prescription) • By Distribution Channel (Offline, Online) • By Application (Chronic Wounds, Acute Wounds) • By End Use (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, Homecare Settings, Long-Term Care Facilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Smith & Nephew plc, 3M Company, ConvaTec Group plc, Coloplast A/S, Mölnlycke Health Care AB, Integra LifeSciences Corporation, Hartmann Group, B. Braun Melsungen AG, Medline Industries, Inc., Johnson & Johnson, and other players. |

Frequently Asked Questions

North America dominated the Wound Gel Market in 2024.

The “Silver (Ag+)” segment dominated the Wound Gel Market.

Shift toward home-based care and self-treatment is accelerating the market growth.

The Wound Gel Market was USD 5.91 billion in 2024 and is expected to reach USD 9.09 billion by 2032.

The Wound Gel Market is expected to grow at a CAGR of 5.58% from 2025 to 2032.

Get in Touch