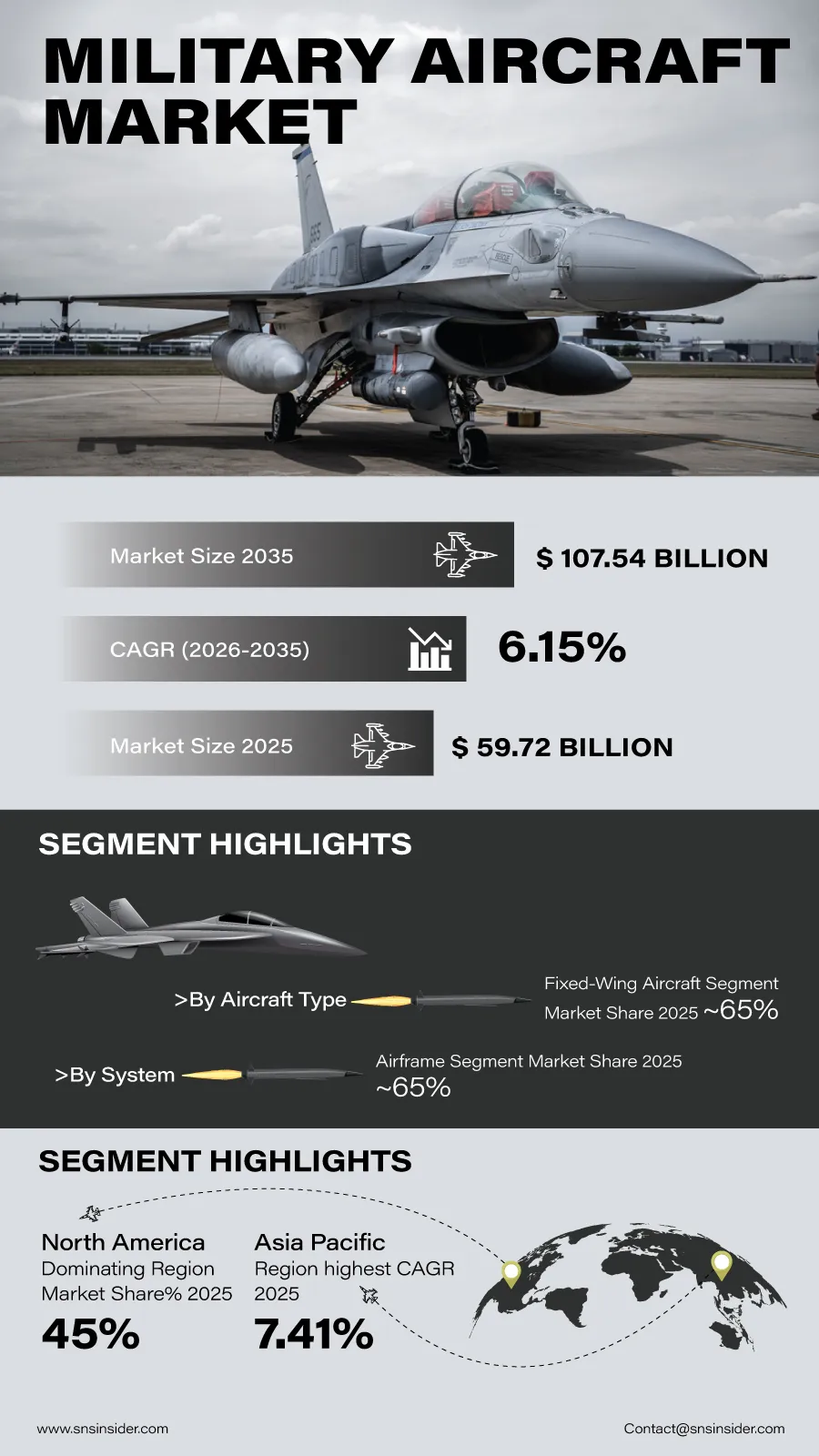

Military Aircraft Market globally is set to witness substantial growth as countries continue to improve their defense strategies by investing in futuristic aircraft systems. According to a recent study by SNS Insider, the global Military Aircraft Market size valued at USD 59.72 billion in 2025, is anticipated to grow to USD 107.54 billion by 2035, registering a CAGR of 6.15% over the 2026–2035 forecast period.

The governments in the major economies have recognized the need to upgrade their air forces in order to meet security needs, ensure better efficiency, and keep up their strategic dominance. The need for advanced fighter jets, military transport planes, surveillance systems, and unmanned aerial vehicles is growing.

The continuous development of technology in terms of stealth, intelligent electronics, propulsion systems, weapons that use precision guidance, and mission management software is changing the face of military aviation. In addition to this, defense contractors have taken up the development of multi-role aircraft that can undertake a variety of tasks.

Air Force Modernization Programs Continue to Unlock New Growth Opportunities

The military services are pouring money into next-generation aircraft fleets to retire ageing platforms and increase their operational capabilities for combat, reconnaissance, transport and humanitarian missions. The requirement for fast deployment, longer operating range and greater situational awareness on the battlefield drives global demand for high technology aircraft.

Greater cooperation between defense agencies, aerospace manufacturers and technology providers is driving innovation across the sector. AI, advanced sensor fusion, autonomous flight technologies and secure communications systems are becoming a requirement for next generation military aviation platforms.

Moreover, multinational defense partnerships and collaborative aircraft development programs provide manufacturers with opportunities to increase production capacities, share technological know-how and secure long-term procurement channels in global markets.

Key Market Insights Highlight Shifting Demand Patterns

By aircraft type, fixed-wing aircraft segment accounted for approximately 65% of global market revenue in 2025 due to their widespread deployment across combat, transport, surveillance, and long-range operational missions. Rotorcraft are expected to register the fastest growth through 2035 as military forces increase investments in helicopters for troop mobility, medical evacuation, and tactical support operations.

Based on application, combat aircraft are anticipated to contribute around 42% of market revenue in 2025, reflecting continued investment in maintaining air superiority and strategic strike capabilities. Reconnaissance and surveillance are forecast to emerge as the fastest-growing application segment as defense organizations expand intelligence gathering and real-time battlefield monitoring capabilities.

By propulsion type, turbofan-powered aircraft segment held nearly 38% of market revenue in 2025 owing to their high performance, operational efficiency, and extensive deployment in fighter and transport aircraft. Fully electric and hybrid-electric propulsion technologies are projected to witness the fastest growth as military research programs explore more efficient and lower-maintenance propulsion systems for future aerial platforms.

In terms of systems, airframes segment dominated with around 28% share of market revenue in 2025 owing to the continuous investments in lightweight materials, structural durability, and advanced composite technologies. Avionics are expected to register the fastest growth through 2035 as armed forces increasingly prioritize sophisticated navigation, communication, electronic warfare, and mission management capabilities.

An Infographic Representation of the Global Military Aircraft Market

Advanced Aviation Technologies Strengthen Mission Effectiveness

The rapid development of digital technologies is revolutionizing military aviation through higher operational performance, survivability and mission coordination. Artificial intelligence, sensor fusion, autonomous capabilities, predictive maintenance and advanced electronic warfare systems are making aircraft more efficient in more demanding operational environments.

In addition, manufacturers are investing in modular aircraft architectures that allow for future upgrades to meet evolving mission requirements. These technology advances are expected to improve aircraft readiness, reduce maintenance complexity and extend service life across military fleets globally.

Regional Markets Demonstrate Strong Defense Investment Momentum

North America is estimated to account for 45% of the total market revenue worldwide in 2025, owing to increased defence spending, ongoing aircraft modernization projects, and the existence of leading aerospace manufacturers. Ongoing procurement of next generation fighter aircraft, transport platforms and unmanned systems continue to bolster the region's leadership position.

Asia Pacific region is anticipated to be the fastest growing regional market with a CAGR of 7.41% through 2035. Increased defense budgets, heightened geopolitical tensions and wide-ranging military modernization programs in countries such as India, Japan, South Korea and parts of South-east Asia are fueling major procurement activity in the region.

As governments continue strengthening national security strategies and investing in advanced air combat capabilities, demand for modern military aircraft is expected to remain resilient over the coming decade.

Industry Participants Focus on Innovation and Next-Generation Airpower

The competitive landscape remains highly dynamic as aerospace companies continue advancing stealth technologies, autonomous systems, intelligent avionics, advanced propulsion solutions, and integrated mission capabilities. Strategic defense partnerships, research investments, and long-term procurement contracts remain central to maintaining technological leadership in the evolving military aviation sector.

Key companies operating in the global Military Aircraft Market include Lockheed Martin Corporation, The Boeing Company, Airbus Defence and Space, BAE Systems plc, Northrop Grumman Corporation, General Dynamics Corporation, Raytheon Technologies (RTX), Leonardo S.p.A., Dassault Aviation SA, Saab AB, Embraer S.A., Textron Inc., Hindustan Aeronautics Limited (HAL), Korea Aerospace Industries (KAI), Sukhoi (United Aircraft Corporation), Rheinmetall AG, Thales Group, Rolls-Royce Holdings plc, GE Aerospace, and Elbit Systems Ltd.

An SNS Insider analyst Santosh Bhul commented, “Growing investments in air force modernization, advanced aerospace technologies, and multi-domain defense capabilities are creating strong momentum for the military aircraft market. Manufacturers that emphasize innovation, operational versatility, and next-generation mission systems will be well positioned to capitalize on expanding global defense procurement opportunities.”

About the Author

Get in touch