Medical Devices Market Report Scope & Overview:

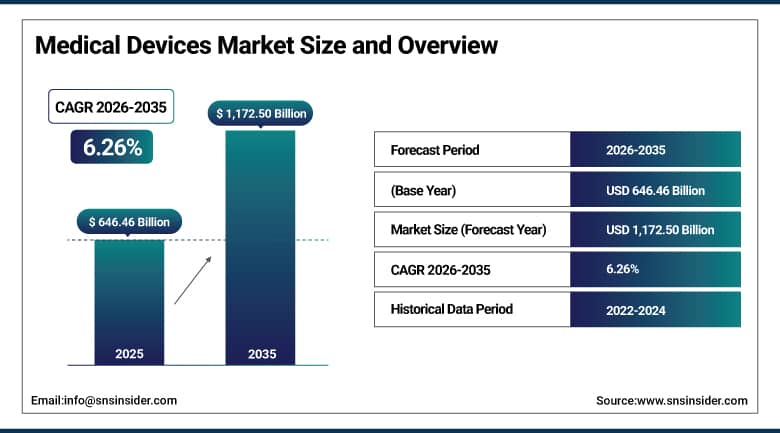

The Medical Devices Market was valued at USD 646.46 Billion in 2025 and is expected to reach USD 1,172.50 Billion by 2035, growing at a CAGR of 6.26% from 2026 to 2035.

The medical devices market plays a hugely important role in the global healthcare economy. It includes everything from basic diagnostic tools and monitoring supplies to complex systems like cardiovascular implants, robotic surgery units, and fancy diagnostic tech. This sector is super crucial because it forms the link between diagnosis and treatment in clinical settings. Medical devices are used in just about every type of medical field and care situation. Nowadays, integrating these devices with digital health, AI, and personalized medicine is really changing how the industry works. This boosts value for everyone healthcare providers, insurers, and patients alike.

Medtronic plc, the world’s largest medical device company by revenue, reported fiscal year 2025 revenues of USD 32 billion, highlighting continued procedure volume recovery across cardiovascular and spine categories and accelerating adoption of its robotics-assisted surgical platform in international markets, with particular emphasis on Asia Pacific and Latin American procedure growth rates outpacing those of established North American and European markets.

Market Size and Forecast:

-

Market Size in 2026E: USD 678.86 Billion

-

Market Size by 2035: USD 1,172.50 Billion

-

CAGR: 6.26% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Medical Devices Market - Request Free Sample Report

Medical Devices Market Trends:

-

AI-enabled diagnostic imaging and patient monitoring systems are improving early disease detection and clinical decision-making.

-

Miniaturized cardiovascular and neurostimulation devices are expanding access to minimally invasive therapies and outpatient procedures.

-

Rising adoption of home healthcare and remote monitoring devices is driven by aging populations and growing connected care models.

-

Robotic-assisted surgical platforms are increasing adoption across orthopedic, urological, and cardiovascular procedures.

-

Expansion of digital procurement and e-commerce channels is streamlining access to monitoring, diagnostic, and therapeutic devices.

U.S. Medical Devices Market Outlook:

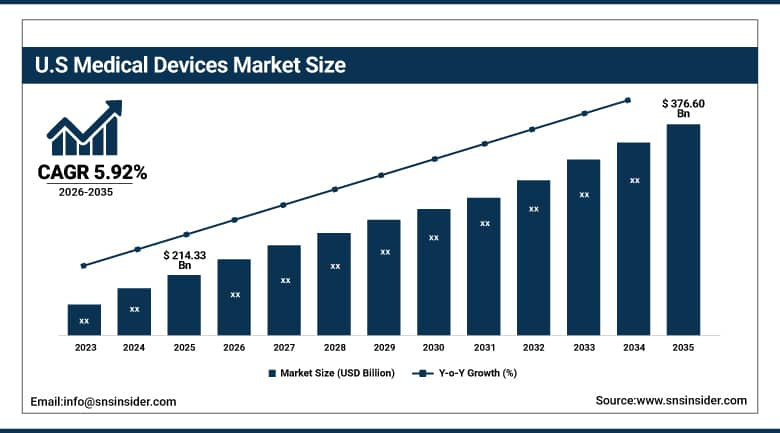

The U.S. Medical Devices Market was valued at USD 214.33 Billion in 2025 and is expected to reach USD 376.60 Billion by 2035, growing at a CAGR of 5.92%.

The United States is clearly at the top in the global medical devices market, raking in around 85.54% of North America's total revenue. It leads thanks to an advanced hospital system, a super innovative manufacturing sector, and the world's biggest network for approving and monitoring medical devices. Plus, their healthcare pays more for cutting-edge tech, boosting the market even further. The US also rocks the globe's largest academic medical center network. This fosters quick take-up of new gadgetry by clinics, getting these innovations into the marketplace faster than anywhere else. So, not only do they pioneer more products, but their systems support a continuous cycle of creation and growth, making their clout seriously solid.

Johnson & Johnson MedTech, in its 2024 results, reported strong U.S. growth driven by orthopedic, electrophysiology, and surgical vision procedures, alongside increasing adoption of its robotic-assisted surgery platform across major hospital systems.

Medical Devices Market Segment Analysis:

-

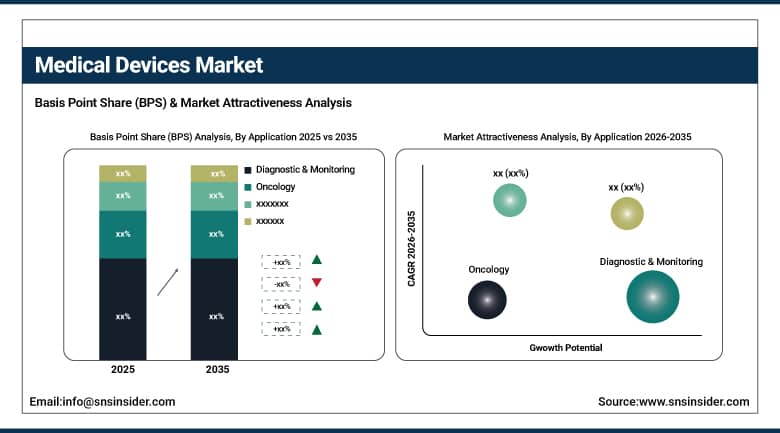

By Application, diagnostic & monitoring dominated the market with a 29.15% share in 2025, while oncology is the fastest growing application with the highest CAGR of 7.88% from 2026 to 2035.

-

By Product Type, in-vitro diagnostic (IVD) devices dominated the market with a 26.15% share in 2025, while patient monitoring devices are the fastest growing product type with the highest CAGR of 7.37% from 2026 to 2035.

-

By End User, hospitals dominated the market with a 48.14% share in 2025, while home healthcare settings are the fastest growing end user segment with the highest CAGR of 8.01% from 2026 to 2035.

-

By Distribution Channel, direct sales dominated the market with a 48.26% share in 2025, while e-commerce platforms are the fastest growing channel with the highest CAGR of 8.52% from 2026 to 2035.

By Application, diagnostic & monitoring dominates the medical devices market, while oncology is the fastest-growing segment.

The Diagnostic & Monitoring segment dominated the medical devices market with the highest revenue share of 29.15% in 2025, rising global demand for early disease detection and routine health checks is pushing the use of diagnostic tools. Now, we see widespread use of things like imaging systems, in vitro devices, and patient monitors. This segment is the biggest in the market because of these technologies and more. Plus, more digitization in healthcare, a rise in chronic diseases, and greater acceptance of remote monitoring gadgets are keeping the demand strong. So, hospitals, clinics, labs, and even homes rely heavily on these diagnostic and monitoring devices, which cements the segment's top spot in the market.

The oncology application segment is projected to witness the fastest CAGR of 7.88% during the forecast period of 2026–2035. The rise in cancer cases worldwide is pushing the use of image-guided radiation therapy and minimally invasive tumor biopsy and ablation devices. Plus, more surgical robots are being integrated into cancer procedures. The increasing accuracy in oncology drug-device combos, along with the bigger role of companion diagnostic devices for targeted treatments, is making things better too. Also, with more investments in radiotherapy and interventional oncology in growing health markets, the commercial success of these devices is soaring across various cancer care options.

By Product Type, in-vitro diagnostic (IVD) devices dominate the medical devices market, while patient monitoring devices are the fastest-growing segment.

The In-Vitro Diagnostic (IVD) Devices segment dominated the market with the highest revenue share of 26.15% in 2025, because lab and point-of-care tests are super important for clinical care they help diagnose diseases, choose treatments, and monitor patients through it all. With more molecular and immunoassay tests coming out, not to mention advances in clinical chemistry and glucose monitoring, the in vitro diagnostics market is getting bigger. There are more patients using these services and clinics are relying on them more too. This is due to higher rates of chronic diseases and the push for broader health screenings.

The Patient Monitoring Devices segment is estimated to register the highest CAGR of 7.37% during the forecast period of 2026–2035 Due to aging populations and advanced remote monitoring tech, we're seeing more continuous health tracking of high-risk folks at home rather than in hospitals. With a bigger push to cut preventable hospital readmissions, there's expanded care for folks with chronic heart, lung, and metabolic issues via connected devices. Plus, increased financial backing for remote monitoring in key healthcare regions is boosting use of these gadgets in hospitals and homes alike.

By End User, hospitals dominate the medical devices market, while home healthcare settings are the fastest-growing segment.

The hospitals segment dominated the medical devices market with the highest revenue share of 48.14% in 2025, because hospitals do high-acuity procedures and complex diagnostics, they use way more medical devices than other care settings. Large academic medical centers and big health systems must buy a lot of this equipment. They need devices for everything from emergency to critical care, including surgery and diagnostics. This makes hospitals the main buyers for the global medical devices market, covering all product levels. So, medical device companies see these big hospitals as crucial for their business.

The home healthcare settings segment is anticipated to record the fastest CAGR of 8.01% throughout the forecast period of 2026–2035, driven by demographic, economic, and technological changes, patient monitoring and chronic disease management are moving from hospitals to home. Healthcare systems need to cut costs for treating chronically ill patients, while people prefer care at home. Plus, digital health tools let doctors keep track of patients remotely. Advances in easy-to-use medical devices for conditions like heart issues and diabetes make home care simpler and safer. So, the home healthcare sector looks set to be the fastest-growing part of the medical device market globally, with robust growth expected throughout the forecast period.

By Distribution Channel, direct sales dominate the medical devices market, while e-commerce platforms are the fastest-growing segment.

The direct sales channel dominated the medical devices market with the highest revenue share of 48.26% in 2025, because big medical device makers need to keep close ties with big hospitals, networked health systems, and purchasing groups, they do this. It lets them place their products well, run clinical training, and set up contracts based on outcomes. The top manufacturers invest in their sales teams to offer special clinical and tech support. This is vital for fancy equipment, implants, and robotic surgery systems. With these, giving education, procedure help, and upkeep is super important for selling their gear.

The E-commerce platforms segment is projected to witness the fastest CAGR of 8.52% during 2026–2035, because smaller healthcare providers and places like diagnostic labs and specialty clinics are adopting digital purchasing, they now enjoy easier access to more options at better prices. Home healthcare product users appreciate this too—online platforms make buying simpler. Sales of devices directly to consumers are growing as well, thanks to approved monitoring, diagnostic, and treatment gadgets now readily available through web-based retailers. Backing this boost in digital selling, regulatory frameworks in key regions support online purchases of medical products.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.54% |

|

Europe |

Germany |

28.46% |

|

Asia Pacific |

China |

40.64% |

|

Middle East & Africa |

UAE |

35.45% |

|

Latin America |

Brazil |

44.29% |

North America Medical Devices Market Insights

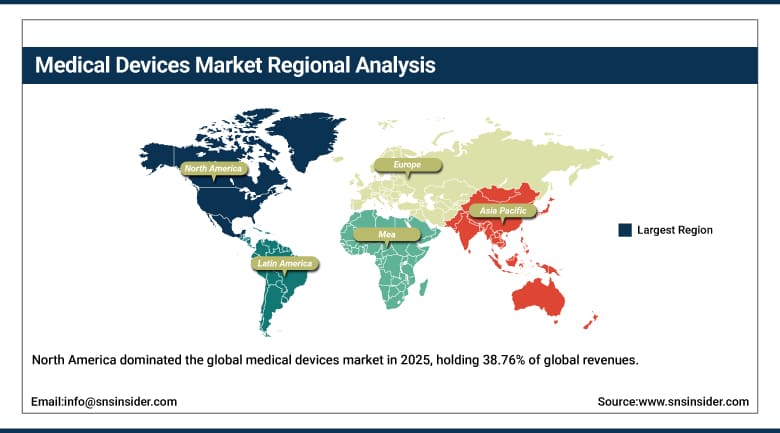

North America dominated the global medical devices market in 2025, holding 38.76% of global revenues, with the United States accounting for 85.54% of regional revenue. The region’s unassailable market leadership position reflects the unprecedented depth of its medical device innovation ecosystem, which encompasses the world’s highest concentration of medical device manufacturers, a uniquely productive clinical research and early commercialization infrastructure anchored by academic medical centers and venture-capital-backed early stage device companies, and a regulatory framework administered by the U.S. Food and Drug Administration that, while rigorous, provides the commercial certainty and international market signal value that enables premium device pricing and rapid post-approval adoption dynamics.

Canada fits well with the regional market because of its healthcare system. They buy medical devices regularly, are close to U.S. manufacturing, and adopt new tech thanks to academic health centers. Cooperation grows between provincial health systems and international device makers too. This teamwork helps create clinical data, supporting wider market access for their products.

The North American medical devices market generates over USD 250 billion annually, supported by the world’s highest per-capita medical device expenditure rates and a healthcare infrastructure encompassing more than 6,000 hospitals, 10,000+ ambulatory surgical centers, and one of the world’s densest networks of diagnostic laboratory and specialty clinic facilities consuming medical devices across virtually every therapeutic category.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Medical Devices Market Insights

European medical devices market is mature and commercially savvy. All major markets use uniform healthcare system procurement rules. Plus, the EU MDR demands solid clinical proof. Also, Europe boasts a strong med device manufacturing sector centered in countries like Germany, Switzerland, France, the Netherlands, and the UK. They make top-notch products used all over for things like imaging, diagnostics, cardiovascular fixes, and orthopedic work. Germany heads up this group and is the biggest European med device market.

It houses giants like Siemens Healthineers, B. Braun Melsungen, and Fresenius Medical Care, as well as many specialized mid-market firms. These businesses back Germany’s leadership with their precision-engineered, clinically advanced products. That's why the country stays atop as a global med device innovator.

Europe’s medical devices sector generates over EUR 140 billion annually in industry revenues, supporting more than 730,000 jobs across manufacturing, distribution, and clinical support functions, and representing one of the world’s most concentrated geographic clusters of medical device innovation capability and regulatory expertise.

Asia Pacific Medical Devices Market Insights

Asia Pacific is the fastest-growing regional medical devices market at a CAGR of 6.87% through 2035. China accounts for 40.64% of Asia Pacific revenues as China invests in healthcare through its infrastructure programs, modernizing hospitals and boosting its domestic medical device industry under initiatives like Made in China 2025, it's creating a big demand for medical devices and improving manufacturing abilities at the same time. In India, rapid expansion of health insurance coverage, growth in domestic device manufacturing via incentive schemes, and the swift growth of private hospitals and diagnostics chains are making the country one of the region's fastest-growing healthcare opportunities. These efforts increase equipment purchases and extend formal healthcare to more people.

China’s medical device market has grown to become the world’s second-largest national market, with government healthcare expenditure exceeding USD 1 trillion annually and a hospital construction and modernization program adding hundreds of new large-scale hospital facilities annually, each representing significant capital medical device procurement opportunities across imaging, surgical, monitoring, and laboratory diagnostic equipment categories.

MEA & Latin America Medical Devices Market Insights

The medical device markets in the Middle East and Latin America show different business potential but share some key traits: expanding health care infrastructures, increasing non-communicable diseases, and a booming middle class. These groups want better healthcare, similar to what developed countries offer. In the Middle East, the UAE dominates the regional market, generating around 30.45% of revenues. This lead is thanks to heavy healthcare investments, top-notch facilities in cities like Dubai and Abu Dhabi, and its role as a hub for medical tourists from all over the Middle East and North Africa. They attract patients with the best tech at international standards.

Brazil leads Latin America's medical devices market, backed by the biggest hospital network in the region. They've got domestic manufacturing for local use and exports too, alongside private health insurance that covers about 25% of Brazilians. This insurance offers better device reimbursement than the public SUS system. Mexico and Colombia are growing fast as well. As their private health sectors expand and government programs push for universal coverage, advanced medical devices become more common. So, these countries are now seen as key markets for expansion.

Latin America’s medical devices market is projected to exceed USD 50 billion by the mid-2030s, supported by Brazil’s dominant market position and growing regional demand from Mexico, Colombia, and Chile, where expanding private insurance coverage and healthcare infrastructure investment are driving premium device adoption beyond traditional public procurement frameworks.

Market Dynamics:

Growth Drivers: Rising chronic disease burden and technological innovation in device platforms

Rising rates of non-communicable diseases in both rich and poor countries are driving up the medical devices market. Dealing with issues like heart disease, diabetes, cancer, and respiratory problems needs constant use of devices, such as those for diagnosis, monitoring, surgery, and therapy. This holds true for decades after diagnosis. Right now, there's a big shift in the health trends of people in Asia Pacific, Latin America, and the Middle East. As these areas become more urban, diets change, and people move less, they start getting more lifestyle-related illnesses. This is leading to an increase in the need for managing chronic conditions in regions with huge populations.

Concurrent tech progress in medical devices is creating way more value than just replacements. It's giving rise to brand new clinical abilities that tackle unmet medical needs. More patients are becoming eligible for procedures too, even those who once weren't suitable for treatment. Plus, care can now happen in cheaper facilities, which is opening up new volumes of procedures.

Restraints: Regulatory compliance complexity and reimbursement environment pressures

The rising complexity and costs of medical device regulations slow down innovation and make it harder for companies to turn their products into profitable ventures. With new EU Medical Device Regulations and stricter FDA requirements, companies need to pour more money into meeting these demands. Smaller firms get hit especially hard compared to big multinationals that can absorb those expenses. These rigorous rules mean more time, money, and effort spent on proving a device’s safety and efficacy. In Europe, it now takes much longer to get devices to market due to extra clinical evidence needs. Patients end up waiting longer for new tech, and manufacturers take huge financial risks funding multi-year studies.

Opportunities: Digital health integration and emerging market healthcare infrastructure expansion

Integrating medical devices into digital health systems is the biggest commercial opportunity in this field. This combo of connected device platforms, cloud management, AI, and interoperable health records lays the groundwork for new ways to deliver care and manage diseases. These methods create steady revenue, moving past the old model of one-time device sales. Manufacturers can gain an edge by linking their physical devices with digital health platforms. By improving patient outcomes and reducing costs, they form networks and analysis tools that clinicians love. This approach gives them major advantages and lets them charge more, setting them apart from competition relying solely on selling devices.

Recent Developments:

-

2026: Abbott Laboratories received CE Mark and FDA Breakthrough Device designation for its next-generation Lingo continuous glucose monitoring system designed for non-diabetic metabolic health management, significantly expanding the addressable consumer and preventive health market for continuous monitoring technology platforms.

-

2026: Boston Scientific Corporation completed its acquisition of a leading cardiac electrophysiology mapping and ablation technology company, strengthening its competitive position in the high-growth pulsed field ablation segment and expanding its integrated electrophysiology procedure system portfolio for atrial fibrillation treatment across global catheter lab environments.

-

2025: Medtronic plc received FDA approval for its next-generation Hugo robotic-assisted surgical system with expanded procedure indications across urological, gynecological, and thoracic surgery categories, accelerating its competitive positioning against the established da Vinci surgical robotic platform in major U.S. and international hospital markets.

-

2025: Siemens Healthineers AG launched its MAGNETOM Terra.X 7-Tesla MRI system with enhanced AI-guided image reconstruction algorithms, establishing a new performance benchmark in neurological and musculoskeletal imaging for academic medical center and research hospital deployments globally.

Medical Devices Market Key Players are:

-

Medtronic plc

-

Johnson & Johnson MedTech

-

Abbott Laboratories

-

GE HealthCare Technologies Inc.

-

Siemens Healthineers AG

-

Stryker Corporation

-

Boston Scientific Corporation

-

Becton Dickinson and Company

-

Philips Healthcare

-

Baxter International Inc.

-

Zimmer Biomet Holdings Inc.

-

Edwards Lifesciences Corporation

-

Olympus Corporation

-

Terumo Corporation

-

Fresenius Medical Care AG

-

Intuitive Surgical Inc.

-

Smith+Nephew plc

-

Align Technology Inc.

-

ResMed Inc.

-

Canon Medical Systems Corporation

Medical Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 646.46 Billion |

| Market Size by 2035 | USD 1172.50 Billion |

| CAGR | CAGR of 6.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (In-Vitro Diagnostic (IVD) Devices, Cardiovascular Devices, Orthopedic Devices, Diagnostic Imaging Devices, Patient Monitoring Devices, Others) • By Application (Diagnostic & Monitoring, Orthopedics, Cardiology, Respiratory Care, Neurology, Oncology) • By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Diagnostic Laboratories, Specialty Clinics, Home Healthcare Settings, Others) • By Distribution Channel (Direct Sales, Medical Device Distributors, Retail Pharmacies, E-commerce Platforms, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic plc, Johnson & Johnson MedTech, Abbott Laboratories, GE HealthCare Technologies Inc., Siemens Healthineers AG, Stryker Corporation, Boston Scientific Corporation, Becton Dickinson and Company, Philips Healthcare, Baxter International Inc., Zimmer Biomet Holdings Inc., Edwards Lifesciences Corporation, Olympus Corporation, Terumo Corporation, Fresenius Medical Care AG, Intuitive Surgical Inc., Smith+Nephew plc, Align Technology Inc., ResMed Inc., Canon Medical Systems Corporation. |

Frequently Asked Questions

The medical devices market is expected to grow at a CAGR of 6.26% from 2026 to 2035.

The medical devices market was valued at USD 646.46 Billion in 2025.

The primary growth factors include the rising global burden of chronic diseases increasing demand for diagnostic, therapeutic, and monitoring devices, rapid innovation in AI-enabled and connected healthcare technologies, and expanding healthcare infrastructure across emerging markets driving new medical device adoption.

Patient monitoring devices is the fastest-growing product type in the Medical Devices Market, with a CAGR of 7.37% from 2026 to 2035.

North America dominated the medical devices market in 2025, holding 38.76% of global revenues, with the United States accounting for 85.54% of North American revenues.

Get in Touch