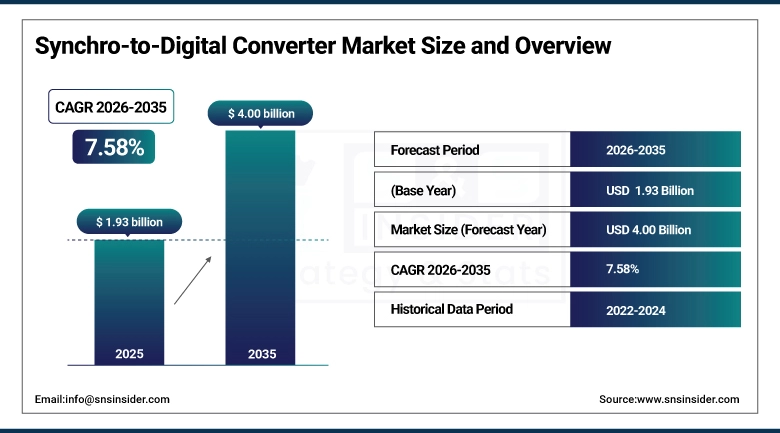

As per the SNS Insider Report titled, Synchro-to-Digital Converter Market Size, Share & Segmentation Analysis, by Technology, by Converter Type, by Output Type, by Application, by End User, and Region | Global Forecast 2026–2035, “The global Synchro-to-Digital Converter Market size was valued at USD 1.93 billion in 2025, is anticipated to grow to USD 4.00 billion by 2035, registering a CAGR of 7.58% during the forecast period 2026–2035.”

Key Takeaways

-

Digital technology dominated the market with a 48.60% revenue share in 2025 owing to rising adoption of high-precision digital signal processing systems across aerospace and defense applications.

-

Hybrid technology is projected to witness the fastest CAGR of 9.37% during 2026–2035 due to increasing demand for enhanced accuracy and flexible conversion architectures.

-

Multi-Axis converters accounted for the largest market share of 57.90% in 2025 driven by their widespread use in advanced navigation, radar, and industrial automation systems.

-

Single-Axis converters are expected to register the fastest CAGR of 8.42% during the forecast period as compact and cost-efficient control systems gain traction across industrial applications.

-

Binary output type held the leading revenue share of 41.30% in 2025 due to its compatibility with conventional digital processing platforms and embedded systems.

-

Gray Code output is anticipated to expand at the fastest CAGR of 9.11% through 2035 owing to its ability to minimize conversion errors in high-precision environments.

-

Aerospace represented the largest application segment with a 33.80% market share in 2025 supported by increasing deployment of synchro-based motion sensing and navigation technologies.

-

Industrial Automation is projected to emerge as the fastest-growing application segment with a CAGR of 10.24% during 2026–2035.

-

OEMs accounted for the largest share of 46.50% in 2025 due to strong integration of synchro-to-digital converters into original equipment manufacturing processes.

-

System Integrators are forecasted to witness the fastest CAGR of 9.58% during the forecast period driven by growing demand for customized automation and control solutions.

-

North America dominated the Synchro-to-Digital Converter Market with a 37.84% revenue share in 2025, while Asia-Pacific is expected to register the fastest CAGR of 9.71% during 2026–2035.

Why Synchro-to-Digital Converter Market is Growing?

The Synchro-to-Digital Converter Market is witnessing substantial growth due to an increase in the adoption of sophisticated precision control system solutions, advanced navigation technology, and high-end signal converters in the aerospace and defense industry, among others. Synchro-to-Digital converters find extensive application in converting the analog output of synchros to digital information.

With rapid technological advancements in avionics systems and radars, and increased use of automated manufacturing systems, the demand for digital and hybrid converters is witnessing a boost. Furthermore, the demand for efficient and accurate motion data acquisition, and feedback systems is contributing to market growth.

The adoption of the fourth industrial revolution or Industry 4.0 technologies, and smart factories is offering lucrative growth prospects in the market. Growing emphasis on operational efficiency and precision engineering, and automated controls is driving the market demand for the same.

Furthermore, defense modernization programs, and investment in aerospace electronics, is expected to drive market growth in the coming years.

Synchro-to-Digital Converter Market Statistics

-

There is constant growth in investments made by the aerospace and defense sector in navigation and positioning systems that have an increased demand for highly accurate synchro converters.

-

The rapid implementation of industrial automation around the globe means more and more intelligent sensors and robotic systems will be employed on the manufacturing floor.

-

The deployment of UAVs and precision-guided systems and devices will result in higher demand for reliable and efficient motion sensors and converters.

-

The switch toward the application of digital avionics and fly-by-wire aircraft technology will lead to increased demand for digital and hybrid synchro-to-digital converters.

-

The rise in automation within factory systems and robotics will lead to greater integration of converters into automated motion control systems within various industries including automotive and heavy manufacturing.

-

The increase in investments in defense-related electronics systems represents future opportunities for the converters' producers.

-

The countries from Asia-Pacific are heavily investing in industrial and aerospace sector development which positively impacts the regional market.

Emerging Trends:

There have been many technological changes in the Synchro-to-Digital Converter market, and some of them include development of high-speed digital converters that deliver more accurate signals with reduced latency. Compactness and energy efficiency are some of the other trends seen in converter technology with the primary target being application in aerospace and embedded industrial environments.

Use of hybrid technologies in conversion solutions has been gaining ground due to their ability to merge the reliability of analogs and the efficiency of digitals. Adoption of artificial intelligence and predictive maintenance features in automated systems is yet another factor fuelling demand for enhanced solutions in signal conversion technologies.

Another significant trend is increased integration of FPGA and software defined architectures into converter systems for greater flexibility and scalability. There is increasing demand for rugged converters that can operate under extreme environmental conditions, particularly in the aerospace and military sectors.

Increasingly, the development of smart factory infrastructures and intelligent industrial systems will spur growth in this sector over the next few years.

Top 10 Companies

-

Analog Devices, Inc.

-

Texas Instruments Incorporated

-

Data Device Corporation

-

Maxim Integrated

-

Renesas Electronics Corporation

-

Broadcom Inc.

-

Moog Inc.

-

Curtiss-Wright Corporation

-

Honeywell International Inc.

-

TE Connectivity

About the Author

Get in touch