Synchro-to-Digital Converter Market Report Scope & Overview:

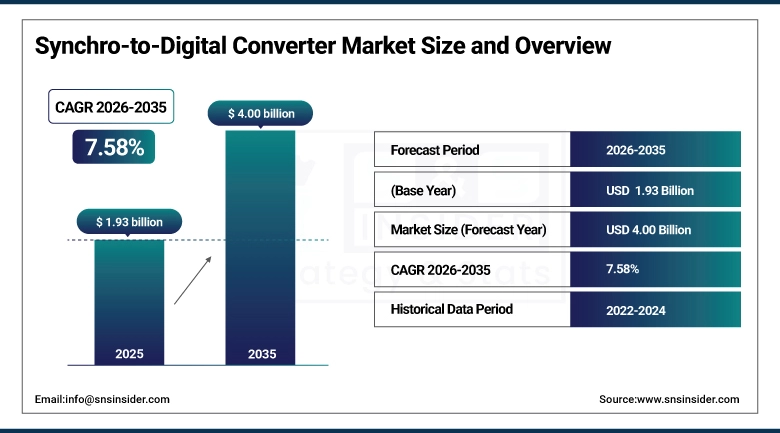

The Synchro-to-Digital Converter Market Size is valued at USD 1.93 Billion in 2025 and is projected to reach USD 4.00 Billion by 2035, growing at a CAGR of 7.58% during the forecast period 2026–2035.

The Synchro-to-Digital Converter Market analysis report provides an in-depth analysis of market trends, focusing on technological innovations, converter types, and aerospace, defense and industrial applications. Rising demand for precision control systems and automation solutions will propel market growth throughout the forecast period.

Synchro-to-Digital Converter shipments reached 245K units in 2025, driven by aerospace, defense, and industrial automation demand for precise motion control.

Market Size and Growth Forecast:

-

Market Size in 2025: USD 1.93 Billion

-

Market Size by 2035: USD 4.00 Billion

-

CAGR: 7.58% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Synchro-to-Digital Converter Market - Request Free Sample Report

Synchro-to-Digital Converter Market Trends:

-

Growing demand for precision motion control is driving innovation in high-accuracy synchro-to-digital converters.

-

Integration with advanced automation and robotics systems is expanding market adoption across industrial applications.

-

Rising aerospace and defense modernization programs are boosting investments in reliable and ruggedized SDC solutions.

-

Miniaturization and hybrid technologies are enabling compact, energy-efficient converter designs for complex systems.

-

Increasing focus on digitalization and smart factory implementations is accelerating SDC deployment in industrial automation.

-

Enhanced signal processing and noise reduction technologies are improving performance and reliability in critical applications.

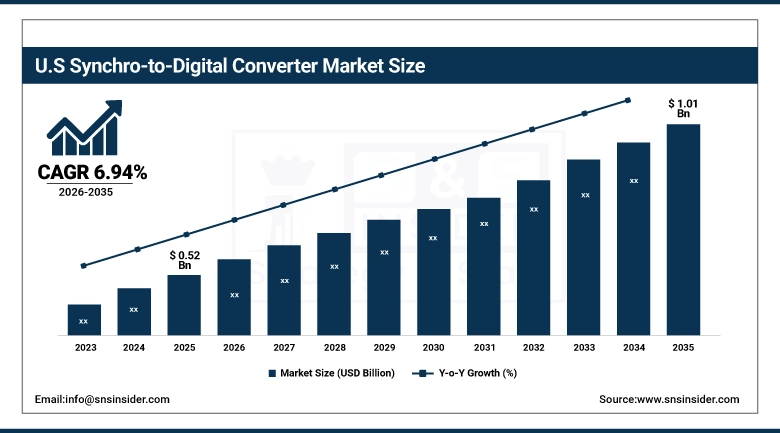

U.S. Synchro-to-Digital Converter Market Size Outlook:

The U.S. Synchro-to-Digital Converter Market is projected to grow from USD 0.52 Billion in 2025E to USD 1.01 Billion by 2035, at a CAGR of 6.94%. Growth is driven by strong defense modernization, rising aerospace electronics upgrades, and expanding automation investments across industrial manufacturing and robotics applications.

Synchro-to-Digital Converter Market Growth Drivers:

-

Rising demand for precision motion control in aerospace, defense and industrial automation driving SDC adoption.

Rising demand for precision motion control is a key driver of the Synchro-to-Digital Converter Market Growth. As aerospace, defense, and industrial automation systems become increasingly complex, reliable and accurate position feedback solutions are critical. Synchro-to-digital converters provide high-precision angular data to optimize system performance, enhance safety, and improve automation efficiency. Growing adoption of robotics and smart manufacturing further fuels market expansion, supporting advanced control and operational accuracy.

Synchro-to-Digital Converter shipments grew 8.1% in 2025, driven by rising adoption in aerospace, defense, and industrial automation applications.

Synchro-to-Digital Converter Market Restraints:

-

High costs, complex integration, and strict industry standards are limiting widespread adoption of Synchro-to-Digital Converters.

High costs, complex integration, and strict industry standards are major restraints for the Synchro-to-Digital Converter Market. Manufacturers face significant design and testing requirements to meet aerospace, defense, and industrial safety standards, delaying product deployment and increasing development expenses. Integration into existing automation or control systems can be technically challenging and costly, limiting adoption, particularly among smaller OEMs. These factors collectively constrain market expansion and create barriers for new entrants seeking to offer innovative SDC solutions.

Synchro-to-Digital Converter Market Opportunities:

-

Expanding automation, robotics, and smart factory adoption creates opportunities for advanced, high-precision Synchro-to-Digital Converters.

Expanding adoption of automation, robotics, and smart manufacturing presents a significant opportunity for the Synchro-to-Digital Converter Market. Advances in precision sensing, digital signal processing, and compact design enable development of highly accurate, reliable converters. Manufacturers can capitalize on growing demand for advanced motion control and system optimization across aerospace, defense, and industrial sectors. This trend supports technological innovation, enhances operational efficiency, and drives sustained market growth.

High-precision Synchro-to-Digital Converters accounted for 32% of new automation system integrations in 2025, driven by robotics and smart manufacturing adoption.

Synchro-to-Digital Converter Market Segmentation Analysis:

-

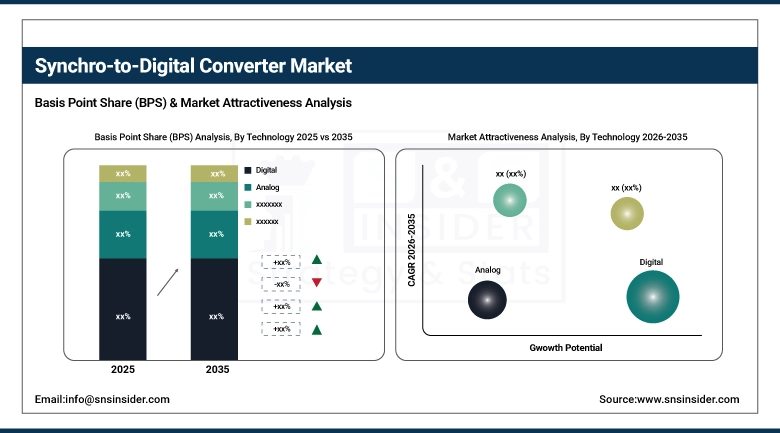

By Technology, Digital held the largest market share of 48.60% in 2025, while Hybrid is expected to grow at the fastest CAGR of 9.37% during 2026–2035.

-

By Converter Type, Multi-Axis accounted for the highest market share of 57.90% in 2025, while Single-Axis is projected to expand at the fastest CAGR of 8.42% during the forecast period.

-

By Output Type, Binary dominated with a 41.30% share in 2025, while Gray Code is anticipated to record the fastest CAGR of 9.11% through 2026–2035.

-

By Application, Aerospace held the largest share of 33.80% in 2025, while Industrial Automation is expected to grow at the fastest CAGR of 10.24% during 2026–2035.

-

By End-User, OEMs accounted for the largest share of 46.50% in 2025, while System Integrators are forecasted to register the fastest CAGR of 9.58% during 2026–2035.

By Technology, Digital Dominates While Hybrid Accelerates Rapidly:

Digital segment dominated the market due to its high precision, signal stability, and compatibility with modern aerospace and defense electronics. Digital converters are widely preferred in mission-critical systems requiring reliable real-time angular measurement and simplified integration. Hybrid is the fastest growing segment, offering a balance of analog signal accuracy and digital processing benefits. Hybrid SDCs are gaining adoption as industries modernize legacy systems, with 500 manufacturers upgrading to mixed-signal platforms in 2025 alone.

By Converter Type, Multi-Axis Leads While Single-Axis Advances Quickly:

Multi-Axis segment dominated the market due to their ability to process multiple synchro signals simultaneously, reducing hardware footprint and improving system efficiency. These converters are widely used in modern aircraft navigation systems, artillery positioning mechanisms, and advanced factory automation machinery. Single-Axis are the fastest-growing segment as they offer a cost-effective solution for compact systems and robotics applications. With miniaturization and embedded design growth, 120,000 Single-Axis converters were deployed across industrial and laboratory systems in 2025.

By Output Type, Binary Takes the Lead While Gray Code Grows Rapidly:

Binary segment dominated the market due to its compatibility with most control processors and its ability to deliver simple, fast and reliable interpretation by digital control systems. It is widely used across legacy and modern aerospace industrial systems, making it the preferred choice for large-scale implementations. Gray Code is the fastest growing segment as it significantly reduces data transition errors and enhances feedback accuracy. 60 new aviation and industrial platforms adopted Gray Code-based converters during 2025 for improved digital resilience.

By Application, Aerospace Dominates While Industrial Automation Expands Swiftly:

Aerospace segment dominated the market as synchro and resolver-based sensors have long been integral in aircraft flight control, engine systems, navigation, and avionics feedback mechanisms. The industry’s strict reliability requirements make Synchro-to-Digital Converters essential for operational safety. Industrial Automation is the fastest growing segment, fueled by investments in smart factories, intelligent robotics, and predictive maintenance infrastructures. In 2025, 1,800 new automation systems globally integrated SDCs to support high-accuracy motion control and system optimization initiatives.

By End-User, OEMs Hold Leadership While System Integrators Accelerate Strongly:

OEMs segment dominated the market as most Synchro-to-Digital Converters are installed at the manufacturing stage of aircraft, defense platforms, and industrial machinery, ensuring system-level standardization. OEMs also benefit from established supply chains and in-house electronics capability. System Integrators are the fastest growing segment as modernization of older military and industrial equipment drives demand for retrofit solutions. 9,500 retrofit and upgrade projects in aerospace and industrial sectors implemented new SDCs in 2025, fueling rapid integrator-led deployment growth.

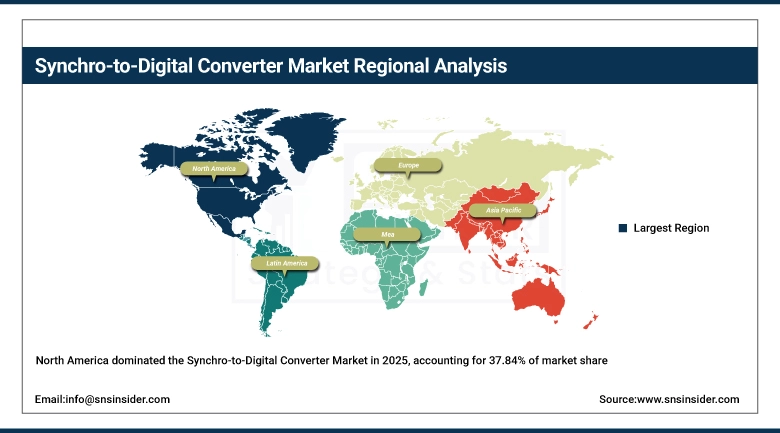

North America Synchro-to-Digital Converter Market Insights:

North America dominated the Synchro-to-Digital Converter Market, accounting for 37.84% market share in 2025. This leadership is driven by strong aerospace and defense manufacturing bases, continuous avionics upgrades, and early adoption of precision motion systems. The region benefits from high R&D spending, strong presence of major OEMs, and rapid modernization of industrial automation infrastructures. Robust defense procurement programs and stringent reliability standards further reinforce North America as the core hub for SDC development and commercialization.

Get Customized Report as Per Your Business Requirement - Enquiry Now

U.S. Synchro-to-Digital Converter Market Insights:

The U.S. Synchro-to-Digital Converter Market is driven by rising investment in aerospace avionics upgrades, advanced defense targeting and navigation systems, and increasing automation deployment across manufacturing. Strong engineering capabilities, extensive R&D funding, and rapid modernization of mission-critical control platforms strengthen the U.S. position as the leading hub for SDC innovation and commercialization.

Asia-Pacific Synchro-to-Digital Converter Market Insights:

The Asia-Pacific Synchro-to-Digital Converter Market is the fastest-growing region, projected to expand at a CAGR of 9.71% during 2026–2035. Growth is driven by rapid industrial automation, expanding aerospace and defense investments, and increasing adoption of robotics and smart manufacturing across China, India, Japan, and South Korea. Government-supported modernization programs, rising localization of high-precision motion control systems, and growing electronics manufacturing output position Asia-Pacific as the most dynamic region for future SDC innovation and deployment.

China Synchro-to-Digital Converter Market Insights:

China’s Synchro-to-Digital Converter Market is driven by rapid expansion of aerospace manufacturing, defense modernization, and large-scale automation upgrades across industrial production. Growing investment in domestic avionics, robotics, and precision motion control technologies strengthens local demand. Increasing localization of advanced electronic components positions China as a major growth contributor within the Asia-Pacific SDC landscape.

Europe Synchro-to-Digital Converter Market Insights:

The Europe Synchro-to-Digital Converter Market is expanding steadily, supported by strong aerospace, defense, and industrial engineering sectors. Increasing investments in advanced avionics, precision navigation, and motion control technologies contribute significantly to market growth. Countries such as Germany, France, the UK, and Italy lead adoption due to robust manufacturing capabilities, stringent performance standards, and strong emphasis on modernizing mission-critical systems. The region’s mature industrial automation landscape and rising deployment of robotics further strengthen Europe’s role as a key market for high-performance SDC solutions.

Germany Synchro-to-Digital Converter Market Insights:

Germany is a key Synchro-to-Digital Converter market supported by strong aerospace, defense, industrial automation and advanced engineering sectors. Growing demand for high-precision motion control, modernization of military avionics, and expansion of Industry 4.0 automation solutions drive adoption. Germany’s technological leadership, stringent quality standards and strong OEM ecosystem reinforce its dominance in the European market.

Latin America Synchro-to-Digital Converter Market Insights:

The Latin America Synchro-to-Digital Converter Market is expanding due to growing investments in aerospace, defense modernization and industrial automation across Brazil, Mexico and Argentina. Increasing demand for precise navigation, motor control and avionics systems, coupled with rising adoption of digital transformation in manufacturing, is driving strong market growth and strengthening regional technological capabilities.

Middle East and Africa Synchro-to-Digital Converter Market Insights:

The Middle East & Africa Synchro-to-Digital Converter Market is expanding due to growing aerospace modernization, rising defense spending and industrial automation initiatives. Investments in advanced navigation, avionics, and motor control systems in Saudi Arabia, the UAE, and South Africa are fueling adoption, while increasing digital infrastructure upgrades strengthen regional technological development and system reliability.

Synchro-to-Digital Converter Market Competitive Landscape:

Analog Devices, headquartered in the U.S., is a leader in precision analog, mixed-signal, and digital signal processing technologies. The company dominates the Synchro-to-Digital Converter market due to its high-performance converter portfolio, advanced sensor interface solutions, and strong focus on aerospace, defense, and industrial automation applications. Leveraging robust R&D, cutting-edge signal processing innovations, and a broad OEM customer base, Analog Devices ensures high reliability, accuracy, and scalability, strengthening its position as a preferred choice for critical motion control and navigation systems.

-

In March 2025, Analog Devices, Inc. launched the “AD2S1210WDSTZ,” a 16-bit high-precision Synchro-to-Digital Converter. It features SPI interface, rugged industrial and automotive-grade design, and accurate angular measurements, reinforcing Analog Devices’ leadership in precision motion control and aerospace.

Texas Instruments, based in the U.S., is a dominant player in the Synchro-to-Digital Converter market owing to its expertise in semiconductor solutions, analog ICs, and precision converters. Its extensive product range addresses aerospace, defense, and industrial automation requirements, offering reliable performance and system compatibility. By investing heavily in R&D, maintaining manufacturing capabilities and collaborating with OEMs and integrators, Texas Instruments provides high-quality, scalable SDC solutions, securing trust, market leadership, and widespread adoption in critical control and automation applications.

-

In February 2025, Texas Instruments, Inc. introduced the “C2000 MCU Resolver Kit (TMDSRSLVR),” enabling developers to integrate resolver-to-digital conversion with SPI for motion-control applications. It enhances precise position feedback, rapid development and strengthens TI’s industrial automation and aerospace presence.

North Atlantic Industries, headquartered in the U.S., specializes in high-reliability aerospace and defense electronic systems, including Synchro-to-Digital Converters. The company dominates the market due to its ruggedized, precision-grade SDC solutions, tailored for avionics, navigation, and military applications. By focusing on innovation, compliance with stringent aerospace standards, and custom OEM solutions, North Atlantic Industries delivers reliable, high-performance converters that integrate seamlessly into mission-critical systems, reinforcing its market leadership and reputation as a trusted provider in high-precision control and motion sensing.

-

In January 2025, North Atlantic Industries, Inc. launched the “SDx Series and 73SD4 Board,” offering multi-channel, high-resolution Synchro-to-Digital conversion with ±1 arc-minute accuracy for avionics and defense systems, reinforcing NAI’s dominance in rugged, high-performance motion sensing solutions.

Synchro-to-Digital Converter Companies are:

-

Analog Devices, Inc.

-

Texas Instruments Incorporated

-

Data Device Corporation

-

Moog Inc.

-

Honeywell International Inc.

-

TE Connectivity Ltd.

-

AMETEK, Inc.

-

General Dynamics Corporation

-

Safran S.A.

-

L3Harris Technologies, Inc.

-

Collins Aerospace (RTX)

-

Raytheon Technologies Corporation

-

BAE Systems plc

-

Thales Group

-

Siemens AG

-

Parker Hannifin Corporation

-

Renishaw plc

-

Indra Sistemas, S.A.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.93 Billion |

| Market Size by 2035 | USD 4.00 Billion |

| CAGR | CAGR of 7.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Analog, Digital, Hybrid) • By Converter Type (Single-Axis, Multi-Axis) • By Output Type (Binary, BCD, Gray Code) • By Application (Aerospace, Defense, Industrial Automation, Robotics, Others) • By End User (OEMs, System Integrators, Research & Development, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Analog Devices, Inc., Texas Instruments Incorporated, North Atlantic Industries, Inc., Data Device Corporation, Moog Inc., Honeywell International Inc., Curtiss-Wright Corporation, TE Connectivity Ltd., AMETEK, Inc., General Dynamics Corporation, Safran S.A., L3Harris Technologies, Inc., Collins Aerospace (RTX), Raytheon Technologies Corporation, BAE Systems plc, Thales Group, Siemens AG, Parker Hannifin Corporation, Renishaw plc, Indra Sistemas, S.A. |

Frequently Asked Questions

North America dominated with a 37.84% market share in 2025, while Asia-Pacific is the fastest-growing region with a CAGR of 9.71% during 2026–2035.

By Technology, Digital dominated with 48.60% market share in 2025, while Hybrid is expected to grow at the fastest CAGR of 9.37% during 2026–2035.

Growth is driven by demand for precision motion control, adoption of automation and robotics, and modernization in aerospace, defense, and industrial sectors.

The market is valued at USD 1.93 Billion in 2025 and is projected to reach USD 4.00 Billion by 2035.

The Synchro-to-Digital Converter Market is expected to grow at a CAGR of 7.58% during the forecast period 2026–2035.

Get in Touch