Action Games Market Report Scope & Overview:

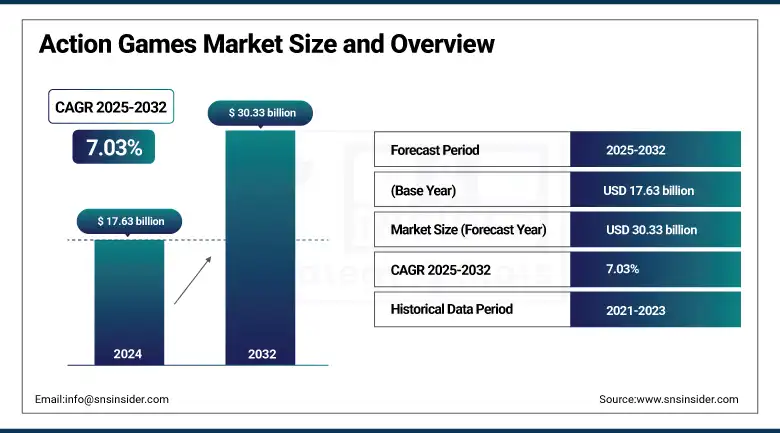

The Action Games Market size was valued at USD 17.63 billion in 2024 and is expected to reach USD 30.33 billion by 2032, expanding at a CAGR of 7.03% over the forecast period of 2025-2032.

The Action Games Market stands out as one of the most vibrant and profitable areas in the global gaming scene, fueled by captivating storytelling, cutting-edge graphics, and adrenaline-pumping gameplay. Genres like first-person shooters, battle royale, and hack-and-slash are drawing in a diverse crowd of players across consoles, PCs, and mobile devices. The growing appetite for lifelike visuals, cross-platform multiplayer experiences, and cloud gaming is driving global adoption. North America takes the lead in market share thanks to its solid infrastructure and top-notch developers, while the Asia Pacific region is experiencing the fastest growth, largely due to the popularity of mobile gaming and eSports. Looking ahead, the future of this market is set to be shaped by advancements in AI, VR, and creative monetization strategies.

According to research, mobile action games now account for 42% of daily gaming sessions in Southeast Asia, fueled by titles like PUBG Mobile, which has exceeded USD 10 billion in lifetime revenue. Action games also dominate eSports, representing 45% of total prize pools and driving a 28% year-over-year surge in Twitch engagement.

Action Games Market Size and Forecast

-

Market Size in 2024: USD 17.63 Billion

-

Market Size by 2032: USD 30.33 Billion

-

CAGR: 7.03% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

To Get more information On Action Games Market - Request Free Sample Report

Action Games Market Trends

-

The global Action Games Market is expanding steadily, supported by the broader gaming industry’s growth, which surpassed USD 180 billion, with action titles accounting for over 30% of total game revenues worldwide.

-

Rising popularity of multiplayer and battle royale action games is driving engagement, with online multiplayer penetration exceeding 65% among action game players globally.

-

Growth of mobile action games is accelerating, contributing to nearly 50% of action game downloads, fueled by smartphone penetration exceeding 75% in key markets.

-

Increasing adoption of in-game purchases and microtransactions is boosting monetization, with more than 60% of action game revenue generated through digital add-ons and live services.

-

Expansion of cloud gaming and cross-platform play is enhancing accessibility, with cross-platform titles witnessing 20–25% higher player retention rates compared to single-platform games.

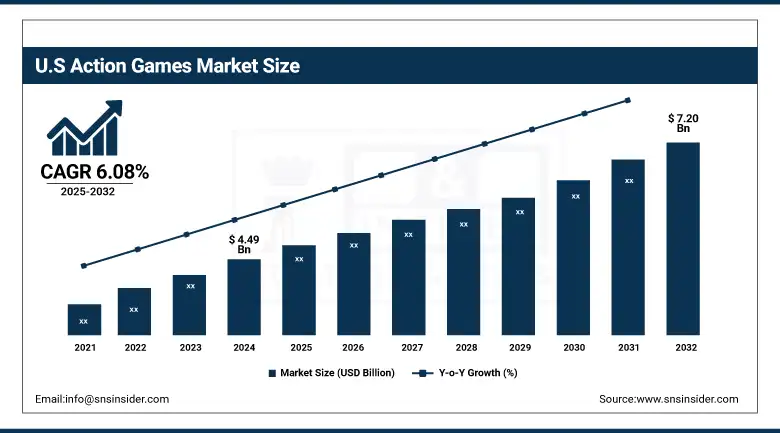

The U.S Action Games Market size reached USD 4.49 billion in 2024 and is expected to reach USD 7.20 billion in 2032 at a CAGR of 6.08% from 2025 to 2032.

In the U.S., the action games market is at the forefront worldwide, supported by a well-established gaming ecosystem, strong consumer spending, and famous developers like Activision Blizzard, Electronic Arts, and Epic Games. Beloved franchises such as Call of Duty, Fortnite, and Star Wars Jedi have gained massive popularity across consoles and PCs. With excellent internet infrastructure, cutting-edge gaming hardware, and a large, tech-savvy player community, the U.S. also enjoys a strong cultural acceptance of gaming, alongside the rise of platforms like Twitch. American studios are continuously pushing the envelope with cross-platform capabilities, engaging storylines, and monetization methods like DLCs and subscriptions, solidifying the U.S.'s dominance in this genre.

Action Games Market Drivers:

-

Rising Multiplayer and Cross-Platform Play Fuel Global Gamer Engagement

The rise of multiplayer and cross-platform gaming has really ramped up player engagement, as folks are increasingly drawn to real-time, competitive experiences that span different devices. Games like Fortnite and Call of Duty: Warzone are perfect examples of this trend, pushing developers to create more immersive and unified gaming ecosystems.

As of 2025, over 60% of top-grossing action games support cross-play, while 67% of gamers actively engage in multiplayer formats. Multiplayer titles contribute 40% of total revenue, with players spending around 7 hours weekly online. Notably, women now make up 45% of the global gaming audience.

Action Games Market Restraints:

-

Rising Development Costs and Resource Intensity Hinder Independent Studio Participation and Market Entry.

To create high-quality action games, developers need advanced graphics, smart AI, and complex gameplay, which naturally raises production costs. With consumer expectations on the rise, smaller studios with limited resources often struggle to keep pace, which can hinder innovation. The growing need for skilled talent and thorough testing adds to the operational challenges, resulting in a consolidation within the action games industry where only well-funded publishers can afford AAA development, restricting diverse content and market access for up-and-coming developers.

Action Games Market Opportunities:

-

Expansion of Cloud Gaming Services and 5G Networks Unlocks New Avenues for Real-Time Gaming Experiences.

The rise of cloud gaming platforms and speedy 5G networks is revolutionizing how players access action games, allowing them to enjoy high-performance titles on smartphones and budget devices. This transition not only expands the user base in mobile-first regions but also paves the way for new monetization models like subscriptions and in-game purchases.

|

Key Insight & Source |

Strategic Implication |

|---|---|

|

"Try Before You Buy" Boost 72% of cloud gamers are more likely to buy a full game after trying it via streaming. – Accenture, 2024 |

Cloud gaming acts as a powerful monetization engine, driving sales through instant-access demos. |

|

5G Gamers Spend More Gamers on 5G networks spend 42% more on in-game purchases than those on 4 G. – Ericsson, 2024 |

Faster 5G connections directly correlate with higher monetization potential, especially in action games. |

|

Latency Matters. A latency improvement from 50ms to under 10ms increases player retention by 34% in real-time action games. – OpenSignal, 2024 |

5G is crucial for enabling smoother, stickier experiences in multiplayer titles, significantly boosting player retention. |

|

Cloud Gaming Reduces Churn Players using cloud-based gaming platforms have a 23% lower churn rate than those downloading games traditionally. – Deloitte, 2024 |

The convenience of instant access and device-agnostic play in cloud gaming actively keeps players engaged longer. |

Action Games Market Challenges:

-

Increasing Regulatory Scrutiny and Content Restrictions Across Regions Challenge Global Distribution Strategies.

Action games with violent or mature content often face regulatory scrutiny and age-based restrictions across regions. Growing concerns over youth exposure and digital addiction are prompting bans and modifications, as seen with PUBG and Call of Duty. These regulations disrupt global launches, complicate localization, and restrict content, impacting market access and timelines.

As of 2025, over 45 countries enforce restrictions or bans on violent or mature-themed video games, reflecting growing global regulatory scrutiny. In 2024, 52% of top-selling action games were rated “M,” while 68% of U.S. parents support stricter age-verification, signaling rising pressure for responsible content governance.

Action Games Market Segment Analysis

By Target Audience

In 2024, the age group segment led with a 47.32% revenue share, primarily driven by players aged 18–34 who favor immersive, fast-paced action content. This demographic is highly engaged with AAA titles and multiplayer formats like Call of Duty and God of War. Increasing digital penetration and cultural acceptance of gaming among adults further fuel demand for cinematic storytelling and realistic visuals.

The gender segment is the fastest-growing in the action games market, expanding at a CAGR of 7.93%, driven by rising female participation. Developers are introducing inclusive characters and diverse narratives, while platforms like PlayStation and Xbox enhance accessibility. This shift reflects evolving perceptions, promoting gender-neutral gaming through inclusive design and engagement strategies.

By Gameplay Style

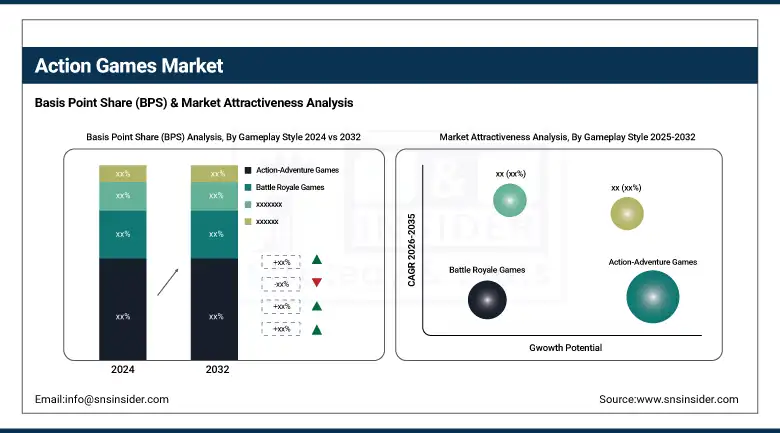

Action-Adventure Games led with a 38.42% revenue share in 2024, driven by hybrid gameplay blending exploration, combat, and storytelling. Popular titles like Marvel’s Spider-Man 2 highlight its appeal. Enhanced AI and animations, along with rising console and PC adoption, attract both casual and hardcore gamers seeking immersive experiences.

Battle Royale Games are growing rapidly with a CAGR of 8.34%, driven by competitive survival gameplay and global hits like Fortnite and Apex Legends. Real-time PvP combat, frequent content updates, and eSports integration keep players engaged. Investments in seasonal passes and mobile optimization broaden the genre’s appeal across all platforms.

By Genre-Based

First-person Shooter (FPS) games captured the largest market share at 34.59% in 2024, led by popular titles such as Call of Duty, Halo Infinite, and Valorant. Their immersive viewpoints, realistic combat, and dynamic multiplayer features fuel engagement. Continuous innovation in weapon mechanics, expansive maps, and cross-platform play strengthens their role in eSports and solidifies FPS dominance in the action gaming segment.

Hack and Slash Games are expanding at a CAGR of 8.04%, fueled by rising demand for combo-based, high-speed combat. Titles like Devil May Cry 5 and Elden Ring blend RPG depth with dynamic action. Their appeal lies in stylish gameplay, mechanical depth, and immersive world-building, attracting global audiences across platforms.

By Device Type

Console Games held a dominant 39.48% market share in 2024, driven by the popularity of high-performance platforms like PlayStation and Xbox. These consoles offer exclusive AAA titles, powerful hardware, and immersive real-time gameplay. Recent releases such as Spider-Man 2 and Starfield have boosted engagement. Innovations like adaptive triggers and haptic feedback further enhance player experience, sustaining strong user loyalty and platform demand.

Mobile games are growing at a CAGR of 7.59%, fueled by rising smartphone usage and demand in mobile-first regions like Southeast Asia and India. Popular titles such as PUBG Mobile and Free Fire highlight this trend. Enhanced 5G, cloud streaming, and accessible, free-to-play models are driving widespread adoption and engagement.

By Monetization Model

Premium Games dominated with a 41.39% share in 2024, driven by demand for full-priced AAA titles like God of War Ragnarök. Players prefer ad-free, complete experiences with rich stories. Core gamers and console users fuel growth, while studios boost revenue through premium models combined with optional DLCs.

Subscription-based games are expanding rapidly at a 9.24% CAGR, driven by platforms like Xbox Game Pass and PlayStation Plus Extra. These services offer affordable access to large game libraries, cloud gaming, and day-one releases, creating recurring revenue and high consumer value.

Action Games Market Regional Analysis

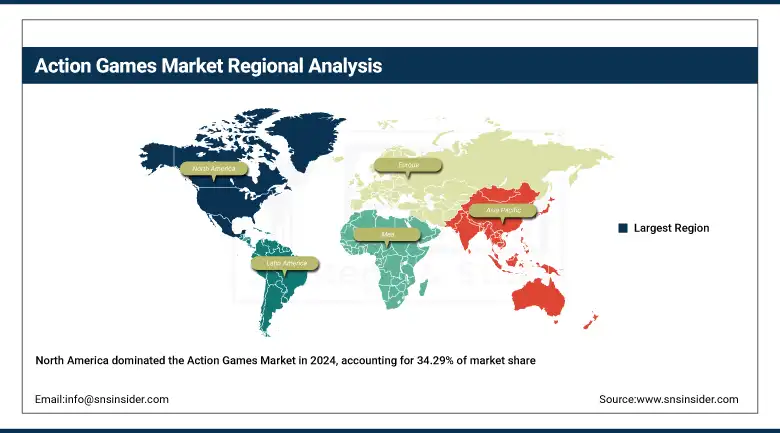

In 2024, North America led the action games market with a 34.29% share, driven by its advanced gaming ecosystem and widespread console usage. Home to major developers like Activision Blizzard, Electronic Arts, and Epic Games, the region excels in high-budget game production, innovation, and eSports infrastructure. Strong digital spending, broadband access, and the popularity of multiplayer and premium console games further solidify North America’s dominance in the global action games industry.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States leads the region due to its vast player base, early tech adoption, and homegrown publishing giants who continually launch top-performing action titles.

Key U.S. Action Gaming Insights Shaping Market Momentum

Twitch Users Fuel Action Game Momentum

-

44 million U.S. Twitch users aged 18–34 drive action game popularity, livestream engagement, and in-game monetization through titles like Warzone and Valorant.

Gamers Embrace 4 K-Capable Hardware

-

Around 70% of U.S. gamers now use 4 K-ready devices, increasing demand for immersive, cinematic AAA action games with high-performance gameplay.

Game Subscriptions Shape Action Title Success

-

Approximately 35% of U.S. console players subscribe to platforms like Game Pass, positioning these services as major channels for monetizing and distributing action games.

Europe holds a major share of the action games market, driven by strong PC and console use, quality regulations, and developers in Germany, the UK, and France. Gamers prefer action-adventure and story-rich shooters. The action games market growth in cross-platform games, digital marketplaces, eSports, and streaming boosts engagement, with Germany leading due to hardware adoption and a robust developer community.

In 2024, Asia Pacific led as the fastest-growing action games market with a 29.29% share, driven by rising mobile penetration and large youth populations in China, India, and Japan. Popular mobile and eSports FPS games, localized content, and 5G adoption boost growth. China dominates due to its vast gamer base, mobile gaming culture, and strong government support.

The Middle East & Africa and Latin America action games markets are growing rapidly, driven by rising smartphone use, digital infrastructure, and youth demand. UAE and Brazil lead their regions, with mobile gaming and eSports expanding, despite challenges like limited console adoption and economic constraints in some areas.

Major Market Competitors

The major key players of the action games market are Electronic Arts, Ubisoft, Capcom, Square Enix, Bandai Namco Entertainment, Epic Games, CD Projekt, FromSoftware, Remedy Entertainment, and SEGA and others.

Key Developments

-

In April 2025, Epic Games acquired Loci, an AI-powered 3D asset tagging platform, to enhance content creation workflows and improve intellectual property detection. This move supports Epic’s strategic push toward automating game development and protecting creative assets.

-

In January 2025, Bandai Namco Entertainment partnered with Rebel Wolves to publish the Blood of Dawnwalker, an upcoming action-RPG scheduled for a 2026 release, marking a strategic move to expand its dark fantasy gaming portfolio.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 17.63 Billion |

| Market Size by 2032 | USD 52.90 Billion |

| CAGR | CAGR of 7.03% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Target Audience – (Age Groups, Gender, Gaming Experience Level) By Gameplay Style – (Single-player Games, Multiplayer Games, Battle Royale Games, Action-Adventure Games) •By Genre-Based – (First-person Shooter (FPS), Third-person Shooter, Platformer Games, Hack and Slash Games) •By Device Type – (Console Games, PC Games, Mobile Games) •By Monetization Model – (Premium Games, Free-to-Play Games, Subscription-Based Games, Downloadable Content (DLC) Offerings) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Keysight Technologies, Viavi Solutions Inc., Spirent Communications, EXFO Electronic Arts, Ubisoft, Capcom, Square Enix, Bandai Namco Entertainment, Epic Games, CD Projekt, FromSoftware, Remedy Entertainment, SEGA. |

Frequently Asked Questions

North America dominated the Action Games Market in 2024 with a 34.29% market share.

By gameplay style, Action-Adventure Games dominated the Action Games Market, accounting for a 38.42% revenue share in 2024.

The major growth drivers include rising multiplayer and cross-platform gaming demand, advanced graphics, immersive storytelling, and the expansion of cloud gaming and 5G networks.

The Action Games Market reached a valuation of USD 17.63 billion in the year 2024.

The market is projected to grow at a CAGR of 7.03% from 2025 to 2032.

Get in Touch