Active Wound Care Market Report Scope & Overview:

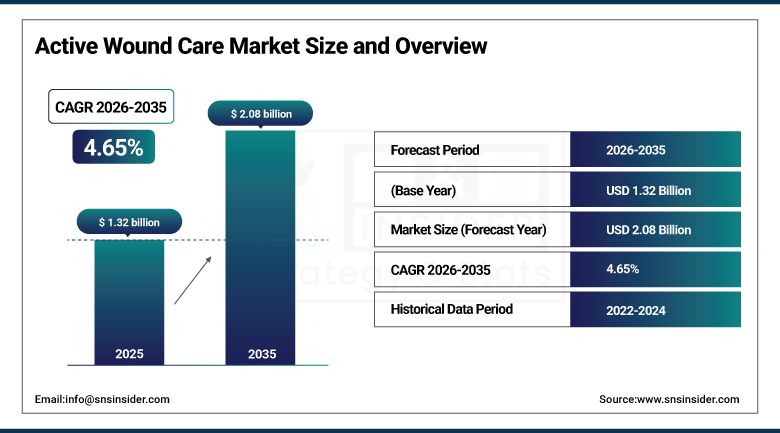

The Active Wound Care Market was valued at USD 1.32 Billion in 2025 and is expected to reach USD 2.08 Billion by 2035, growing at a CAGR of 4.65% from 2026–2035.

Active wound care sits at the more sophisticated end of the wound management spectrum, encompassing biomaterials, skin substitutes, and growth factor therapies designed to genuinely accelerate healing rather than simply protecting a wound while the body does its own work. The market's growth is closely tied to the rising incidence of chronic wounds, diabetic foot ulcers, pressure ulcers, and venous leg ulcers chief among them, conditions that have become considerably more common as global rates of diabetes and vascular disease continue climbing. An aging population compounds this trend meaningfully, since older patients heal more slowly and develop chronic wounds at a substantially higher rate than younger adults. Continued innovation in biomaterials and skin substitute technology, paired with expanding home healthcare infrastructure, is helping close some of the treatment gap, particularly across developing economies where advanced wound care access has historically lagged.

Research using the UK's General Practice Research Database has found that venous leg ulcer prevalence runs three to four times higher, and pressure ulcer prevalence five to seven times higher, in people over 80 compared with those aged 65 to 70. Chronic wound care is estimated to cost roughly USD 10 billion annually, with the overwhelming majority of that cost concentrated among patients aged 65 and above, a demographic reality that continues to shape both clinical demand and healthcare system spending priorities.

Market Size and Forecast

-

Market Size in 2026E: USD 1.38 Billion

-

Market Size by 2035: USD 2.08 Billion

-

CAGR: 4.65% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Active Wound Care Market - Request Free Sample Report

Active Wound Care Market Trends

-

Skin substitute technology continues advancing rapidly, with tissue engineering and stem cell-based approaches improving integration and reducing healing times for severe, full-thickness wounds.

-

Home healthcare-based wound management is expanding steadily, supported by telemedicine integration and remote monitoring tools that reduce the need for repeat clinical visits.

-

Regenerative therapies are gaining physician preference over traditional dressing-based approaches, particularly for complex chronic wounds that haven't responded to conventional treatment protocols.

-

Manufacturers are increasingly pursuing regional joint ventures and clinical research partnerships to accelerate product development and expand market presence outside their home territories.

-

Industry conference activity and clinical study publication continue to play an outsized role in driving physician adoption of newer biomaterial and growth factor product lines.

U.S. Active Wound Care Market Outlook

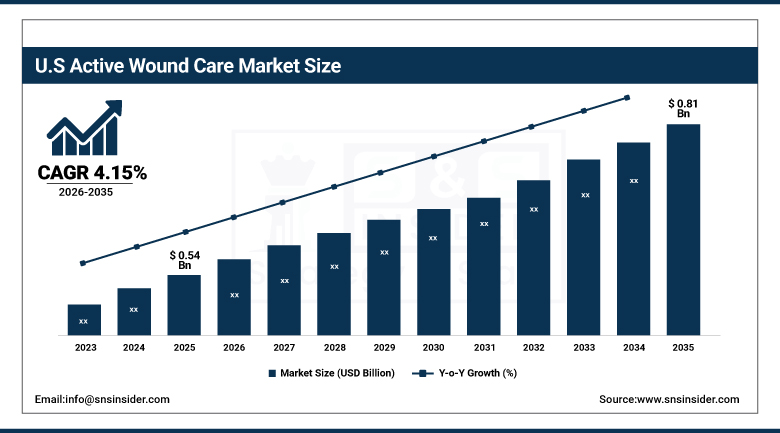

The U.S. Active Wound Care Market was valued at approximately USD 0.54 Billion in 2025 and is expected to reach approximately USD 0.81 Billion by 2035, growing at a CAGR of approximately 4.15%.

The U.S. dominates the North American active wound care market on the strength of well-developed healthcare infrastructure, a high prevalence of chronic wounds tied to the country's substantial diabetic population, and a strong concentration of leading industry players headquartered domestically. Ongoing investment in research and development, combined with generally favorable reimbursement policy for advanced wound care products, continues to support sustained market growth, while rising adoption of technologically advanced wound care products keeps driving better patient outcomes and, correspondingly, greater clinical demand.

In March 2025, ConvaTec Group PLC, a leading provider of chronic condition management technologies and medical products, attended the European Wound Management Association's 2025 conference in Barcelona, where it showcased recent innovations in advanced wound care solutions. Industry conference participation of this kind continues to serve as a meaningful channel through which U.S.-headquartered and multinational wound care companies alike introduce new clinical data and product innovations to the broader physician community.

Active Wound Care Market Segmentation Analysis

-

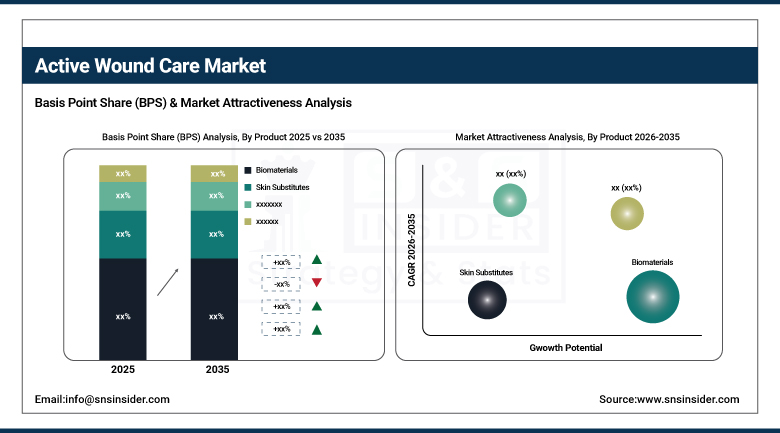

By Product, the Biomaterials segment dominated the Active Wound Care Market with a 48.03% revenue share in 2025, while the Skin Substitutes segment is expected to register the fastest growth.

-

By Application, the Chronic Wounds segment dominated the Active Wound Care Market with a 61.38% revenue share in 2025, while the Acute Wounds segment is expected to show the fastest growth.

-

By End-use, the Hospitals segment dominated the Active Wound Care Market with approximately 48.15% share in 2025, while the Home Healthcare segment is expected to register the fastest growth.

By Product, biomaterials dominate, skin substitutes grow fastest

Biomaterials held 48.03% of the market in 2025, the largest product share, owing to their significant contribution toward faster and improved wound healing outcomes. Materials including collagen, hydrocolloids, and alginates create an ideal healing environment by keeping the wound moist, preventing infection, and promoting faster tissue regeneration, and their extensive use across both chronic and acute wound care applications, particularly for pressure ulcers and diabetic foot ulcers, has helped cement this segment's market leadership.

Skin substitutes are expected to register the fastest growth over the forecast period, driven by rising demand for sophisticated, biologically active products capable of treating chronic wounds more effectively than traditional dressings. Grafts and cellular therapies take a more integrated approach, specifically targeting severe wounds including full-thickness burns and non-healing ulcers, and growing physician awareness of the clinical benefits these products offer, better integration and reduced healing times chief among them, continues to drive segment growth alongside ongoing advances in tissue engineering and stem cell technology.

By Application, chronic wounds dominate, acute wounds grow fastest

Chronic wounds are expected to make up 61.38% of the demand due to applications in 2025 because of the increasing incidence of diabetes, obesity, and vascular disorders leading to non-healing wounds that need special treatment. It is believed that chronic wounds affect about 2% of the American population, including 8.2 million Medicare recipients, and the costs incurred by the health sector for treatment of such patients amount to USD 28 billion per year, which is why the application type stays the leader among others.

Acute wounds are projected to exhibit the fastest growth over the forecast period due to the growing incidence of traumatic injuries, surgical wounds, and burns – the types of wounds that need immediate and special attention. Growing number of surgeries, traumatic incidents, and accidents keep boosting the need for innovative wound care products for acute situations, and technological developments facilitating fast healing and recovery periods contribute to accelerating the growth in this category.

By End-use, hospitals dominate, home healthcare grows fastest

Hospitals accounted for approximately 48.15% of the market in 2025, reflecting their central role in treating a broad range of chronic and acute wounds. Advanced facilities, sophisticated medical equipment, and trained medical staff capable of managing complex wounds, including diabetic foot ulcers, pressure ulcers, and extensive burns, make hospitals the preferred setting for treating high-risk wound cases, and higher reimbursement levels combined with greater institutional capital continue to support hospital investment in newer wound care technology.

Home healthcare is expected to register the fastest growth over the forecast period, as patients increasingly opt for more comfortable, cost-effective care delivered from home rather than requiring repeat hospital or clinic visits. Rising chronic disease prevalence, combined with advances in telemedicine, remote monitoring, and home-based wound care systems, continues to drive this shift, offering continuous care in a familiar environment while lowering hospital readmission rates and reducing overall costs for both patients and healthcare systems.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

81.0% |

|

Europe |

Germany |

24.0% |

|

Asia Pacific |

China |

36.0% |

|

Latin America |

Brazil |

35.0% |

|

Middle East & Africa |

Saudi Arabia |

25.0% |

North America Active Wound Care Market Insights

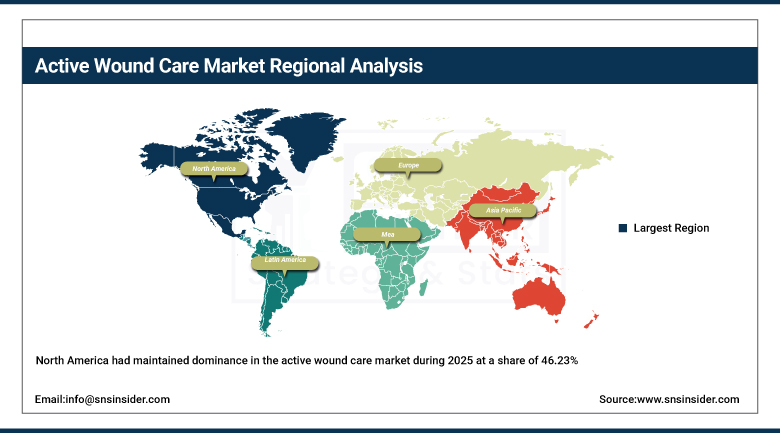

North America had maintained dominance in the active wound care market during 2025 at a share of 46.23% due to advanced healthcare facilities, high expenditures on healthcare, and a large number of key companies in active wound care and chronic wound treatments located in this region. The high prevalence rate of chronic ailments such as diabetes and obesity, which lead to the development of diabetic foot ulcers and pressure ulcers, will help maintain healthy regional demand.

Positive reimbursement policies, regulatory framework, and availability of advanced technology in wound care are some of the factors that have contributed to the dominance of North America in the market. North America is largely driven by the US, which contributes to most of the regional revenue.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Active Wound Care Market Insights

Asia Pacific is the fastest-growing region in the active wound care market, with a projected CAGR of 5.28% through the forecast period, propelled by an aging population, rising chronic disease prevalence, and growing awareness of advanced wound care solutions. Accelerating urbanization, improving healthcare access, and rising investment in medical facilities across China, India, and Japan continue to drive regional market demand.

Government efforts to optimize wound management practices, combined with substantial untapped market potential across the region, are prompting global active wound care companies to increase their regional presence. As healthcare infrastructure across the region's largest economies continues to mature, Asia Pacific looks positioned to sustain its lead as the market's fastest-growing region well into the next decade.

Europe Active Wound Care Market Insights

Europe has a huge market presence in terms of active wound care worldwide, backed by a combination of a highly developed healthcare system, increased demand for advanced wound care products, and an established presence of biomaterials, skin substitutes, and growth factor therapy. Europe’s highly developed healthcare system continues to help in adopting new wound care treatments much faster than any other parts of the world where healthcare systems are not very developed.

United Kingdom is at the top in terms of market dominance in Europe, with a well-developed healthcare system, a high usage of wound care technology, and substantial R&D capabilities in the country. The NHS is one of the most influential bodies in helping with adoption of new technologies in the field of wound care by providing the best-in-class wound care solutions to all chronic wound sufferers.

MEA & Latin America Active Wound Care Market Insights

Latin America is experiencing moderate growth in active wound care, driven by rising prevalence of chronic diseases including diabetes and obesity, an aging population, and growing awareness of advanced wound care options. Economic disparity, uneven healthcare infrastructure, and inconsistent reimbursement policy across the region continue to limit the market's ability to reach its full potential, even as underlying demand keeps expanding.

The Middle East and Africa region is seeing similarly moderate expansion, driven by high rates of chronic conditions, aging populations, and increased healthcare expenditure across key markets including Saudi Arabia and South Africa. The region continues to face real challenges, including limited access to cutting-edge wound care technology, economic constraints, and inconsistent levels of clinical awareness, all of which continue to shape the pace of market development.

Growth Drivers: Rising chronic disease prevalence and an aging population sustain demand

The growing prevalence of chronic diseases, including diabetes, obesity, and vascular disorders, represents one of the primary growth drivers for the active wound care market. These conditions, diabetes in particular, tend to cause non-healing wounds such as diabetic foot ulcers that demand advanced wound care products rather than standard dressings, and as the global prevalence of these underlying conditions continues rising, demand for sophisticated wound care products capable of treating them rises correspondingly.

The increasing global geriatric population represents an equally significant driver, since older adults face greater susceptibility to chronic wounds, pressure ulcers, and other skin problems due to reduced skin elasticity and circulation. This demographic shift continues to drive demand for appropriate wound care treatment, particularly advanced products including biomaterials and skin substitutes, and non-healing wounds, sometimes described in clinical literature as a silent epidemic, represent a genuinely significant multi-billion-dollar burden across hospitalizations, long-term antibiotic exposure, and ongoing local wound therapy that continues to reinforce demand across the broader market.

Restraints: Lengthy regulatory approval processes constrain new product introduction

A major constraint on active wound care market growth is the time-consuming and complex regulatory approval process required for new products. Wound care products face strict regulatory guidelines and approval procedures across multiple regions globally, particularly in the U.S. and Europe, requiring rigorous clinical trials, testing, and documentation to satisfy requirements set by regulatory bodies including the FDA and EMA.

These extended approval timelines have the practical effect of delaying market entry for innovative products, increasing development costs, and reducing overall investment appetite for research and development into new wound care technologies. For smaller manufacturers in particular, the combination of lengthy timelines and substantial compliance costs can make it genuinely difficult to bring promising new biomaterial or growth factor products to market at a competitive pace relative to established, larger competitors.

Opportunities: Expanding home healthcare and emerging market access create meaningful upside

The increasing growth of home healthcare will be a significant market opportunity for active wound care manufacturers as patients look for comfortable and cheaper means of accessing treatment away from hospitals. The developments in telemedicine and remote monitoring technology have made this move more practical, and manufacturers that are able to come up with solutions aimed at home wound care management will get the chance to take advantage of the growing trend.

Increasing investment in healthcare infrastructure in developing nations will be the second major market opportunity as the increased availability of wound care products in the underdeveloped regions will make it possible to reach more patients than before. With the government of Asia Pacific, Latin America, and Middle East prioritizing better wound management in their health policy agenda, manufacturers can capitalize on such developments.

Recent Developments:

-

2024: Kerecis continued expanding distribution of its fish-skin-derived wound care products across multiple international markets throughout 2024, building on strong clinical outcomes data for chronic and burn wound applications.

-

2025: In March 2025, Mölnlycke Health Care AB issued a new clinical study demonstrating the advantages of enhanced dressing regimens, extended its Saudi Arabian joint venture operations, and signed a research agreement with Transdiagen to continue advancing wound care technology.

-

2025: In March 2025, ConvaTec Group PLC attended the European Wound Management Association's 2025 conference in Barcelona, held March 26 to 28, where it showcased recent innovations in advanced wound care solutions.

Active Wound Care Market Key Players

-

3M (Acelity)

-

ConvaTec Group PLC

-

Organogenesis Inc.

-

MiMedx Group, Inc.

-

Integra LifeSciences Holdings Corporation

-

Derma Sciences, Inc.

-

Hollister Incorporated

-

Kerecis

-

Coloplast A/S

-

Baxter International Inc.

-

Medline Industries, LP

-

Cardinal Health, Inc.

-

Acell, Inc.

-

Vericel Corporation

-

Osiris Therapeutics, Inc.

-

PolyNovo Limited

-

Urgo Medical

-

B. Braun SE

Active Wound Care Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.32 Billion |

| Market Size by 2035 | USD 2.08 Billion |

| CAGR | CAGR of 4.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product (Biomaterials, Skin Substitutes, Growth Factors) • by Application (Chronic Wounds, Acute Wounds) • by End-use (Hospitals, Clinics, Home Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Smith & Nephew plc, 3M (Acelity), Mölnlycke Health Care AB, ConvaTec Group PLC, Organogenesis Inc., MiMedx Group, Inc., Integra LifeSciences Holdings Corporation, Derma Sciences, Inc., Hollister Incorporated, Kerecis, Coloplast A/S, Baxter International Inc., Medline Industries, LP, Cardinal Health, Inc., Acell, Inc., Vericel Corporation, Osiris Therapeutics, Inc., PolyNovo Limited, Urgo Medical, B. Braun SE |

Frequently Asked Questions

North America dominated the Active Wound Care Market in 2025 with a 46.23% market share, while Asia Pacific is the fastest-growing region.

The rising prevalence of chronic diseases, particularly diabetes, combined with an aging global population that faces significantly higher rates of chronic wounds.

Biomaterials dominated with a 48.03% revenue share in 2025, while Skin Substitutes is expected to register the fastest growth.

The Active Wound Care Market is expected to grow at a CAGR of 4.65% from 2026 to 2035.

The Active Wound Care Market was valued at USD 1.32 Billion in 2025.

Get in Touch