Adaptive AI Market Report Scope & Overview:

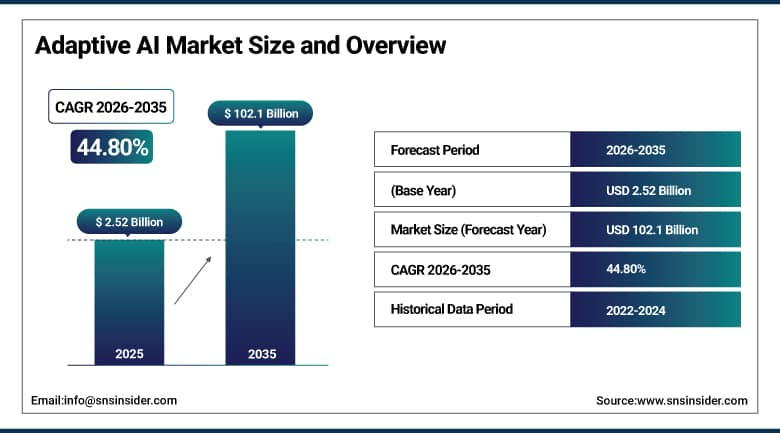

The Adaptive AI Market was valued at USD 2.52 Billion in 2025 and is expected to reach USD 102.1 Billion by 2035, growing at a CAGR of 44.80% from 2026–2035.

The global adaptive AI market is advancing as artificial intelligence systems engineered to continuously learn, retrain, and reconfigure their decision models in response to evolving data distributions, changing environmental conditions, and accumulating operational feedback are displacing static AI models whose performance degrades when deployment conditions diverge from training data characteristics. Adaptive AI’s defining commercial value proposition is its ability to maintain and improve decision accuracy over time without requiring manual model retraining interventions, creating autonomous intelligence systems whose operational value compounds with experience accumulation in ways that fixed-parameter models fundamentally cannot replicate. The convergence of online learning algorithms enabling continuous model updating from production data streams, reinforcement learning from human feedback creating self-improving conversational systems, and transfer learning enabling rapid model adaptation to new domains creates an adaptive AI capability spectrum.

In January 2024, NVIDIA launched the GeForce RTX 40 SUPER Series graphics processors incorporating enhanced on-device AI acceleration capability that enables adaptive machine learning inference at the edge without round-trip cloud latency. Supporting the deployment of continuously learning AI systems in automotive, industrial, and consumer electronics contexts where real-time adaptation requires on-device model update processing rather than centralised cloud-based retraining. The launch accelerated the commercial timeline for adaptive AI deployment in latency-sensitive applications whose practical effectiveness requires local inference and model update capability.

Market Size and Forecast:

-

Market Size in 2026E: USD 3.65 Billion

-

Market Size by 2035: USD 102.1 Billion

-

CAGR: 44.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Adaptive AI Market - Request Free Sample Report

Adaptive AI Market Trends:

-

Large language model fine-tuning and retrieval-augmented generation are creating enterprise adaptive AI systems that continuously update knowledge from proprietary data without full model retraining.

-

Federated learning is enabling adaptive AI model training across distributed data sources without centralising sensitive patient, financial, or personal data to a single training environment.

-

AutoML and neural architecture search platforms are automating adaptive model selection, enabling organisations without AI specialist teams to deploy continuously improving AI systems.

-

Reinforcement learning from human feedback is creating increasingly capable conversational AI systems whose response quality improves continuously from user satisfaction signals.

-

Explainable adaptive AI frameworks are addressing regulatory concerns in financial services and healthcare where decision model transparency is legally required for automated determinations.

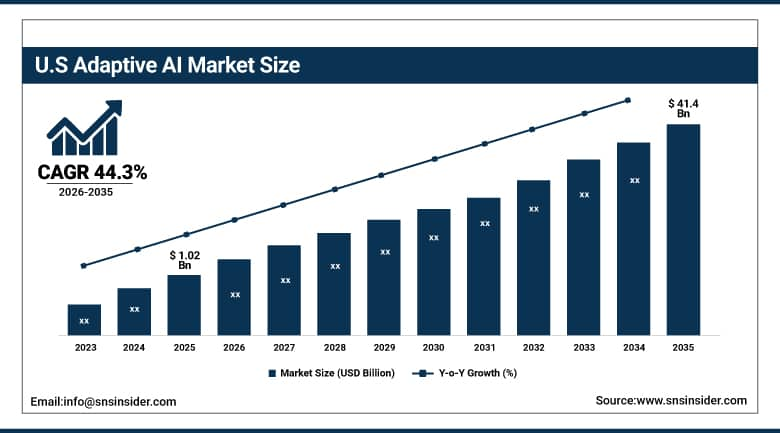

U.S. Adaptive AI Market Outlook:

The U.S. Adaptive AI Market was valued at approximately USD 1.02 Billion in 2025 and is expected to reach approximately USD 41.4 Billion by 2035, growing at a CAGR of approximately 44.3%.

The United States leads North American adaptive AI revenues through the world’s most commercially mature enterprise AI deployment culture, the highest venture capital investment in AI startup companies, and the concentration of foundational AI platform developers including NVIDIA, Microsoft, Google, and IBM whose adaptive AI platform investment defines global capability benchmarks. The SEC’s AI governance guidance and NIST AI Risk Management Framework’s explainability requirements in regulated industries create compliance-driven adaptive AI investment whose documentation and auditability requirements favour platforms with built-in model lineage tracking.

In 2024, Salesforce expanded its Einstein AI platform with adaptive learning capabilities that continuously refine CRM recommendation models from customer interaction data specific to each enterprise deployment, enabling sales, service, and marketing teams to receive personalised predictive guidance that improves with each new customer interaction recorded. The adaptive personalisation demonstrated Salesforce’s strategy of differentiating its CRM platform through AI that becomes more valuable with usage accumulation, creating product stickiness whose incremental adaptation creates switching cost that generic CRM with static AI recommendations cannot match.

Adaptive AI Market Segment Analysis:

-

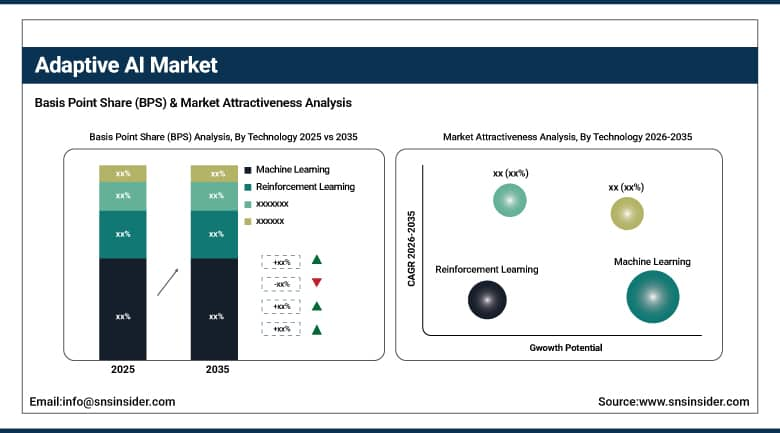

By Technology, machine learning segment dominated the adaptive AI market with the largest share in 2025, while the reinforcement learning segment is the fastest growing technology driven by autonomous decision optimisation and conversational AI quality improvement applications.

-

By Component, platform segment dominated the adaptive AI market with approximately 68% market share in 2025. Meanwhile, the services segment is projected to register the fastest CAGR of around 24.8% during 2026–2035.

-

By Application, the BFSI segment dominated the Adaptive AI Market with the largest share in 2025 through its credit risk, fraud detection, and algorithmic trading adaptive model applications, while the Healthcare segment is the fastest growing application.

-

By Deployment Mode, the Cloud-Based segment dominated the Adaptive AI Market with the largest share in 2025 and is also the fastest growing, driven by scalable training infrastructure and continuous model update deployment that cloud platforms efficiently provide.

By Technology, machine learning dominates, reinforcement learning grows fastest

Machine learning retained the dominant technology position with the largest share of the adaptive AI market in 2025. ML’s commercial primacy reflects the foundational status of supervised, unsupervised, and semi-supervised learning algorithms as the technical core of the adaptive AI applications generating the highest commercial value across recommendation systems, fraud detection, predictive maintenance, and demand forecasting whose continuous model updating from production data creates the adaptive capability that distinguishes deployed ML systems from static analytical models. Online learning algorithms including stochastic gradient descent with streaming data inputs, Bayesian updating of probabilistic models with each new observation, and ensemble methods that dynamically weight constituent models based on recent prediction accuracy.

Reinforcement learning is growing fastest because the deployment of RL-based autonomous optimisation in industrial process control, supply chain management, algorithmic trading, and large language model quality improvement through reinforcement learning from human feedback. This creates a rapidly expanding commercial application set whose learning-by-doing capability creates AI systems whose performance improves through interaction in ways that supervised learning from labelled datasets cannot replicate. Each new RLHF-trained large language model generation whose conversational quality improvement demonstrates reinforcement learning’s commercial value creates platform adoption that sustains investment in RL infrastructure development across AI platform providers.

By Application, BFSI dominates, healthcare grows fastest

BFSI retained the dominant application position with the largest share of the adaptive AI market in 2025. The financial services sector’s structural dependence on continuously adaptive AI reflects the dynamic adversarial environment of financial fraud whose criminal methodology evolution requires fraud detection models that adapt faster than fraudster learning cycles, the credit risk model calibration requirement as economic conditions evolve between model training and deployment, and algorithmic trading’s market microstructure adaptation requirement whose execution quality depends on models that respond to evolving liquidity, volatility, and price impact conditions. JPMorganChase’s COiN contract intelligence adaptive AI, Visa’s real-time fraud detection system processing 65,000 transactions per second with continuous model updating, and BlackRock’s Aladdin portfolio management adaptive AI collectively demonstrate the financial sector’s deepest commercial commitment to adaptive intelligence.

Healthcare is growing fastest because the expanding deployment of adaptive AI in clinical decision support, medical imaging analysis quality improvement, drug interaction monitoring, and personalized treatment response prediction creates a growing commercial application set. Whose continuous learning from electronic health record outcome data improves diagnostic and therapeutic recommendation accuracy in ways that static clinical decision support systems fundamentally cannot achieve. Each hospital that deploys adaptive sepsis detection whose alert threshold self-calibrates to institutional patient population characteristics and each oncology AI system whose response prediction refines continuously from treatment outcome observation creates healthcare adaptive AI adoption that generates above-market segment growth.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

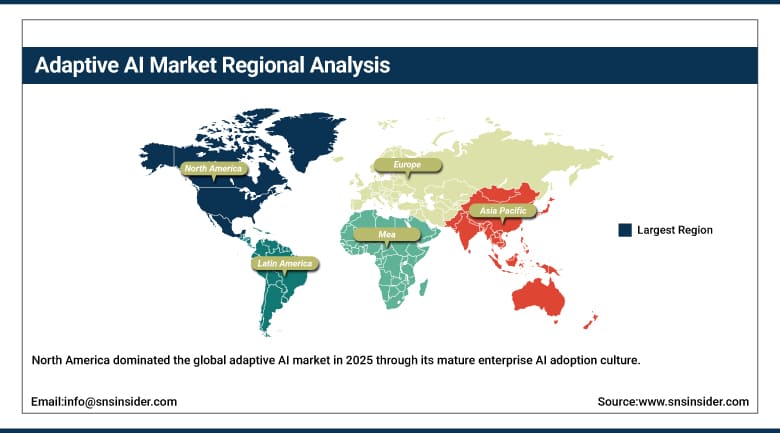

North America Adaptive AI Market Insights

North America dominated the global adaptive AI market in 2025 through its mature enterprise AI adoption culture. The concentration of NVIDIA, Microsoft, Google, IBM, Salesforce, and Cisco whose adaptive AI platform investment defines global technology standards, and the highest venture capital funding for AI startup companies whose adaptive intelligence capabilities are progressively commercializing. The United States accounts for approximately 82.5% of North American revenues through the financial services, healthcare, and technology sectors’ large-scale adaptive AI deployments whose continuous learning infrastructure creates sustained platform and services procurement.

Canada contributes supplementary North American revenues through the Vector Institute, Mila, and AMII’s world-class adaptive AI research whose commercial spin-off activity creates domestic AI company development, the financial services sector’s growing fraud detection and risk management adaptive AI adoption, and government investment in responsible AI frameworks that create institutional adoption motivation across federal and provincial agencies.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Adaptive AI Market Insights

Europe is a significant adaptive AI market where the EU AI Act’s regulatory framework for high-risk AI systems is simultaneously creating compliance investment demand for explainable and auditable adaptive AI platforms and creating market structure that favours technically robust adaptive AI deployments over simpler static alternatives in regulated applications. Germany accounts for approximately 22.4% of European revenues through its large manufacturing sector’s predictive maintenance and process optimization adaptive AI investment, the automotive industry’s autonomous vehicle and ADAS adaptive AI development, and SAP’s enterprise AI platform commercial presence.

The United Kingdom’s financial services sector’s adaptive fraud detection and algorithmic trading AI investment, France’s growing enterprise AI adoption and the INRIA research institute’s adaptive learning contribution, and the Netherlands’ and Sweden’s technology sector’s progressive adaptive AI deployment collectively sustain European market development. European GDPR’s automated decision-making transparency requirements are driving investment in explainable adaptive AI whose regulatory compliance creates technical differentiation for platforms with built-in model explanation capability.

Asia Pacific Adaptive AI Market Insights

Asia Pacific is the fastest-growing regional adaptive AI market, driven by China’s world-leading AI investment and deployment across financial services, industrial manufacturing, and autonomous systems, India’s rapidly expanding enterprise AI adoption driven by the IT services sector’s client programme implementation, and the progressive adaptive AI adoption across South Korea, Japan, and Southeast Asian markets whose digital transformation investment is creating enterprise AI deployment at above-global-average growth rates. China accounts for approximately 44.8% of Asia Pacific revenues through Baidu’s ERNIE adaptive AI, Alibaba’s Tongyi adaptive recommendation systems, and Tencent’s user engagement adaptive intelligence.

India is the most commercially dynamic emerging adaptive AI market, where the IT services sector’s implementation of adaptive AI solutions for global enterprise clients, the fintech sector’s credit scoring and fraud detection adaptive model adoption, and the healthcare sector’s clinical decision support investment collectively create above-regional-average growth momentum. South Korea’s Samsung and LG Electronics’ consumer AI adaptation investment and Japan’s manufacturing sector’s process control adaptive intelligence contribute premium regional demand.

MEA & Latin America Adaptive AI Market Insights

The UAE leads MEA revenues through its AI-forward government digital transformation strategy, the ADNOC oil and gas sector’s adaptive process optimization investment, and the financial services sector’s fraud detection and personalized banking adaptive AI deployment. Saudi Arabia’s Vision 2030 AI strategy and the NEOM smart city adaptive infrastructure investment create growing institutional adaptive AI procurement.

Brazil leads Latin American revenues at approximately 43.8% through its large financial services sector’s credit risk and fraud detection adaptive AI investment, the retail sector’s personalization platform adoption, and the growing enterprise technology sector’s AI implementation services whose adaptive model management requirements sustain professional services demand. Mexico and Colombia contribute growing secondary demand through financial services digitalization and enterprise digital transformation investment.

Market Dynamics:

Growth Drivers: Generative AI’s commercial demonstration of continuously improving AI value and enterprise recognition that static models degrade in dynamic real-world deployment environments

The adaptive AI market’s extraordinary growth rate is driven by generative AI’s commercial demonstration at unprecedented scale of what continuously learning AI can deliver, where large language models’ RLHF-enabled quality improvement creates visible and commercially valued performance gains from each new training iteration that sustain enterprise investment in adaptive AI infrastructure whose compounding improvement creates durable competitive advantage. Each organization whose adaptive AI system demonstrably outperforms its static AI predecessor in production creates an internal reference case whose ROI documentation motivates expansion investment and whose competitive visibility motivates peer organization adoption. The enterprise recognition that static AI models trained on historical data progressively lose prediction accuracy as markets, consumer behavior, and operating conditions evolve creates a structural motivation for adaptive AI investment.

Restraints: Model drift monitoring complexity and regulatory uncertainty around continuously adapting automated decision systems limiting enterprise adoption in risk-averse sectors

Adaptive AI’s continuous learning creates model governance challenges that static AI deployment does not face, where each model update from new data potentially changes decision behavior in ways that require validation before production deployment to ensure continued regulatory compliance, ethical alignment, and business rule adherence. The complexity of monitoring model drift, detecting data poisoning attacks that deliberately inject adversarial training data to corrupt adaptive model behavior, and maintaining documentation of each model update’s provenance for regulatory audit creates governance infrastructure investment that adds operational cost above the AI platform investment itself. Regulatory uncertainty about the permissibility of continuously adapting automated decision systems under fair lending, equal opportunity, and insurance discrimination laws creates legal risk that organizations in regulated industries must manage through legal counsel investment and potentially model update frequency restriction.

Opportunities: Edge adaptive AI for IoT device continuous learning and personalized healthcare AI whose patient-specific model adaptation creates measurably superior clinical outcomes

Edge-deployed adaptive AI whose on-device continuous learning enables IoT sensors, industrial equipment, and autonomous vehicles to improve decision models from operational experience without cloud connectivity creates a commercially significant application category whose latency, bandwidth, and privacy advantages over cloud-dependent adaptive AI sustain growing edge hardware investment from NVIDIA, Qualcomm, and Intel whose AI accelerator chips are progressively incorporating on-device learning capability. Each autonomous vehicle that learns from its specific operating environment, each industrial sensor that calibrates its fault detection threshold from equipment-specific vibration signature data, and each smart building system that optimizes its HVAC control to the specific building’s occupancy patterns creates edge adaptive AI value that cloud-only alternatives cannot deliver at equivalent latency.

Recent Developments:

-

2024: Salesforce expanded its Einstein AI platform with adaptive learning capabilities that continuously refine CRM recommendation models from enterprise-specific customer interaction data, enabling personalized predictive guidance that improves with each new customer interaction and creates compounding product stickiness.

-

2024: NVIDIA launched the GeForce RTX 40 SUPER Series GPUs incorporating enhanced on-device AI acceleration for edge adaptive inference, enabling continuously learning AI systems in automotive, industrial, and consumer electronics without cloud round-trip latency dependency.

-

2024: IBM expanded its Watson AI adaptive model management capabilities with enhanced model drift detection, automated retraining trigger management, and lineage documentation for regulated industry deployment, enabling financial services and healthcare organizations to manage continuously learning AI systems within compliance governance frameworks.

Adaptive AI Market Key Players are:

-

NVIDIA Corporation

-

Microsoft Corporation

-

Google LLC (DeepMind)

-

IBM Corporation (Watson AI)

-

Amazon Web Services Inc. (SageMaker)

-

Salesforce Inc. (Einstein AI)

-

Cisco Systems Inc.

-

Meta Platforms Inc. (Meta AI)

-

Hewlett Packard Enterprise Co. (HPE Ezmeral AI)

-

C3.ai Inc.

-

DataRobot Inc.

-

H2O.ai Inc.

-

Darktrace PLC

-

Aisera Inc.

-

Informatica LLC

-

Clarifai Inc.

-

Kogentix Inc.

-

SparkCognition Inc.

-

Infor Inc.

-

Peak AI Ltd.

Adaptive AI Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.52 Billion |

| Market Size by 2035 | USD 102.1 Billion |

| CAGR | CAGR of 44.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Platform, Services) • By Technology (Machine Learning, Natural Language Processing, Computer Vision, Reinforcement Learning, Others) • By Deployment Mode (Cloud-Based, On-Premise) • By Application (Healthcare, BFSI, Manufacturing, Retail & E-Commerce, IT & Telecom, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | NVIDIA Corporation, Microsoft Corporation, Google LLC (DeepMind), IBM Corporation (Watson AI), Amazon Web Services Inc. (SageMaker), Salesforce Inc. (Einstein AI), Cisco Systems Inc., Meta Platforms Inc. (Meta AI), Hewlett Packard Enterprise Co. (HPE Ezmeral AI), C3.ai Inc., DataRobot Inc., H2O.ai Inc., Darktrace PLC, Aisera Inc., Informatica LLC, Clarifai Inc., Kogentix Inc., SparkCognition Inc., Infor Inc., and Peak AI Ltd. |

Frequently Asked Questions

The Adaptive AI Market is expected to grow at a CAGR of 44.80% from 2026 to 2035.

The Adaptive AI Market was valued at USD 2.52 Billion in 2025.

Generative AI demonstrating compounding value from continuous learning, enterprise recognition that static models degrade in dynamic deployment environments, RLHF enabling self-improving conversational AI are the primary growth factors.

The machine learning segment dominated the adaptive AI market with the largest share in 2025.

North America dominated the Adaptive AI Market in 2025.

Get in Touch