Additive Manufacturing in Aerospace Market Size & Trends:

The Additive Manufacturing in Aerospace Market size was valued at USD 8.75 Billion in 2025 and is projected to reach USD 44.96 Billion by 2035, growing at a CAGR of 17.79% during 2026–2035.

The Additive Manufacturing in Aerospace market is witnessing steady growth due to the rising demand for lightweight, high-strength aircraft components and increasing aircraft production rates. Aerospace OEMs and MRO providers are increasingly adopting additive manufacturing to reduce material waste, shorten lead times, and enable complex geometries that are difficult to achieve using conventional methods. Technologies such as powder bed fusion and directed energy deposition are gaining traction for engine components, structural parts, and tooling. Furthermore, growing investments in space exploration, defense modernization programs, and digital manufacturing initiatives are accelerating the integration of additive manufacturing across the aerospace value chain.

Market Size and Forecast:

-

Market Size in 2025: USD 8.75 Billion

-

Market Size by 2033: USD 44.96 Billion

-

CAGR: 17.79% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Additive Manufacturing in Aerospace Market - Request Free Sample Report

Trends in the Additive Manufacturing in Aerospace Market:

-

Rising demand for lightweight and fuel-efficient aircraft components is accelerating adoption of metal additive manufacturing.

-

Increasing aircraft production and fleet expansion are driving use of 3D printing for structural and engine parts.

-

Growing focus on reducing material waste and production costs is supporting additive manufacturing adoption.

-

Expanding use of additive manufacturing in maintenance, repair, and overhaul (MRO) is improving supply-chain flexibility.

-

Advancements in aerospace-grade alloys and polymers are enhancing part durability and performance.

-

Progress in certification standards is enabling wider deployment in safety-critical aerospace applications.

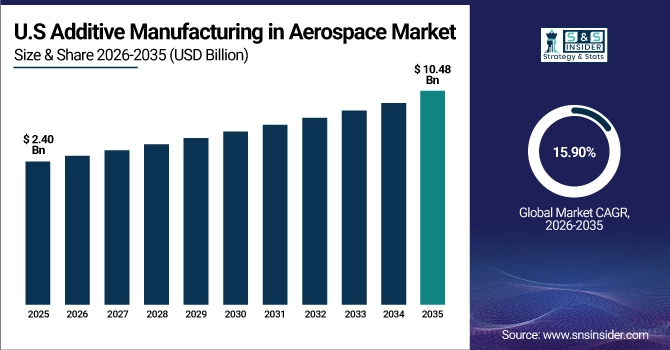

U.S. Additive Manufacturing in Aerospace Market Size Outlook:

The U.S. Additive Manufacturing in Aerospace Market was valued at USD 2.40 Billion in 2025 and is projected to reach USD 10.48 Billion by 2033, growing at a CAGR of 15.90%, driven by strong defense spending, increasing commercial aircraft deliveries, and rising adoption of advanced manufacturing technologies. Growing investments in space programs and rapid adoption by leading aerospace OEMs and MRO providers further support market expansion.

Market Drivers: Growing Demand for Lightweight and Fuel-Efficient Aircraft Components

The increasing demand for lightweight and fuel-efficient aircraft components is a key driver of the Additive Manufacturing in Aerospace Market. As airlines and defense operators face rising fuel costs and stricter emission regulations, aerospace manufacturers are under pressure to reduce aircraft weight while maintaining high performance and safety standards. Additive manufacturing enables complex geometries, part consolidation, and topology-optimized designs that are not feasible with traditional manufacturing methods. These capabilities directly lead to reduced material usage and lighter components, which in turn improve fuel efficiency and lower operational costs. Additionally, additive manufacturing shortens production lead times and minimizes tooling requirements, allowing faster design iterations and cost savings. As aircraft production rates increase and fleet modernization programs expand, aerospace OEMs are increasingly integrating additive manufacturing into serial production, reinforcing its role as a core manufacturing technology.

In April 2024, a major commercial aircraft manufacturer expanded the use of additively manufactured titanium structural brackets, achieving nearly 45% weight reduction compared to conventionally produced parts, resulting in measurable fuel savings across its narrow-body aircraft fleet.

Market Restraints: Stringent Certification Processes and High Qualification Costs for Aerospace-Grade Additive Components

Stringent certification requirements and high qualification costs significantly restrain the growth of the Additive Manufacturing in Aerospace Market. Aerospace components must meet extremely strict safety, reliability, and performance standards, making regulatory approval processes lengthy and complex. Additively manufactured parts require extensive testing, validation, and repeatability studies to ensure consistent quality, which increases development timelines and costs. This creates a cause-and-effect challenge, as prolonged certification delays discourage widespread adoption, particularly among smaller suppliers with limited resources. Furthermore, variability in materials, machines, and printing parameters complicates standardization efforts. As a result, many aerospace manufacturers restrict additive manufacturing to non-critical or secondary components, slowing its broader integration into primary aircraft structures and limiting near-term market scalability.

In August 2023, multiple aerospace suppliers postponed the deployment of additively manufactured engine components due to extended certification timelines, delaying program commercialization by over one year.

Market Opportunities: Rising Space Exploration and Defense Modernization Programs Create New Growth Avenues for Additive Manufacturing

The expansion of space exploration initiatives and defense modernization programs presents a significant opportunity for the Additive Manufacturing in Aerospace Market. Government agencies and private space companies increasingly require lightweight, highly customized, and low-volume components, driving demand for flexible manufacturing solutions. Additive manufacturing enables rapid prototyping, part consolidation, and on-demand production, which directly reduces lead times and supply-chain dependency. This cause-and-effect relationship is strengthening as space missions become more frequent and defense systems more technologically complex. Additionally, additive manufacturing supports advanced materials and intricate designs required for propulsion systems, satellites, and hypersonic platforms. As investment in space and defense programs rises, additive manufacturing is transitioning from experimental use to mission-critical production, unlocking substantial long-term market growth.

In October 2024, a U.S. defense contractor adopted additive manufacturing for rocket propulsion components in a next-generation space program, reducing production lead times by nearly 40% and improving design flexibility.

Additive Manufacturing in Aerospace Market Segmentation Analysis:

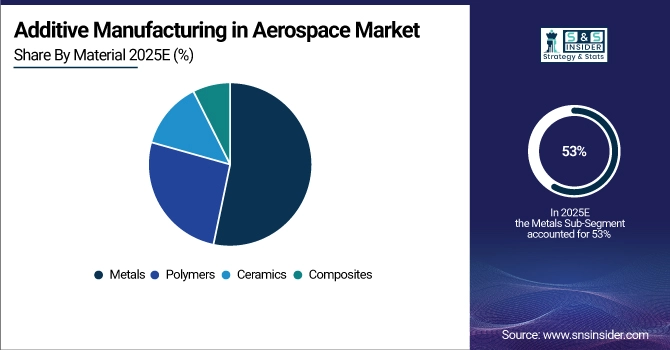

By Material: Metals Dominate Revenue While Composites Experience Rapid Expansion

The Metals segment accounted for 53% of revenue in 2025, driven by strong demand for titanium, aluminum, and nickel-based alloys in aerospace applications. Because metal components offer high strength-to-weight ratios and thermal resistance, they are widely used in engines, airframes, and load-bearing structures. This causes aerospace OEMs to prioritize metal additive manufacturing for flight-critical parts. Advancements in metal powder quality and process control directly enhance durability and certification readiness, reinforcing metals’ dominance in the Additive Manufacturing in Aerospace Market.

The Composites segment is expected to grow at a CAGR of 23.06% during 2026–2035, driven by increasing demand for lightweight, corrosion-resistant components. Because composite materials significantly reduce aircraft weight while maintaining structural performance, they support fuel efficiency and emission reduction goals. Product development in continuous fiber reinforcement and high-temperature composite printing is expanding aerospace applications. This accelerates adoption in interior panels, UAV structures, and secondary components, strengthening composites’ role in long-term market expansion.

By Technology: Powder Bed Fusion Leads Market Share While Binder Jetting Registers Fastest Growth

Powder Bed Fusion (PBF) dominates the Additive Manufacturing in Aerospace Market with a 42% revenue share in 2025 due to its ability to produce high-strength, lightweight, and geometrically complex metal components. Because aerospace OEMs require precision-critical parts such as turbine blades, brackets, and structural components, PBF enables tight tolerances and superior mechanical performance. This causes higher adoption in serial production and engine applications. Continuous product development in laser-based PBF systems and aerospace-grade alloys further strengthens its role, directly supporting aircraft weight reduction and fuel-efficiency goals.

Binder Jetting is projected to grow at the highest CAGR of 22.52% from 2026 to 2035 as aerospace manufacturers seek faster, scalable, and cost-efficient production methods. Because binder jetting allows high-volume printing without thermal distortion, it reduces production time and enables mass manufacturing of non-critical and near-net-shape components. This drives adoption for tooling and interior parts. Ongoing product development in sintering processes and metal powder compatibility is accelerating its integration, expanding its contribution to overall aerospace additive manufacturing growth.

By Application: Production Parts Dominate While MRO Accelerates Rapidly

The Production Parts segment held a 51% revenue share in 2025, as additive manufacturing transitions from prototyping to full-scale production. Because aerospace manufacturers increasingly rely on part consolidation and complex geometries, additive manufacturing enables fewer assemblies and improved reliability. This drives cost efficiency and faster aircraft production cycles. Continuous product development in certified materials and repeatable printing processes directly supports serial production, making production parts the largest revenue contributor to the market.

The Maintenance, Repair & Overhaul (MRO) segment is projected to grow at a CAGR of 20.80% from 2026 to 2035, driven by aging aircraft fleets and spare-part shortages. Because additive manufacturing enables on-demand production of replacement components, it reduces downtime and inventory costs. Product advancements in digital part libraries and rapid qualification processes are accelerating adoption, positioning MRO as a high-growth contributor within the Additive Manufacturing in Aerospace Market.

By Aircraft Type: Commercial Aircraft Lead Revenue While UAVs Record Fastest Growth

Commercial Aircraft accounted for nearly 50% of revenue in 2025E, driven by rising passenger traffic and aircraft deliveries. Because commercial OEMs prioritize fuel efficiency and cost reduction, additive manufacturing enables lightweight components and faster production cycles. This cause-and-effect relationship increases adoption for interior, structural, and engine parts. Continuous product development in large-format printers and certified alloys strengthens additive manufacturing’s integration across commercial aircraft programs.

The Unmanned Aerial Vehicles (UAVs) segment is expected to grow at a CAGR of 20.35% during the forecast period, driven by defense modernization and commercial drone adoption. Because UAVs require lightweight, highly customized designs, additive manufacturing enables rapid prototyping and low-volume production. Ongoing product development in composite materials and compact metal printing systems accelerates UAV manufacturing efficiency, making this segment a key future growth driver in the aerospace additive manufacturing market.

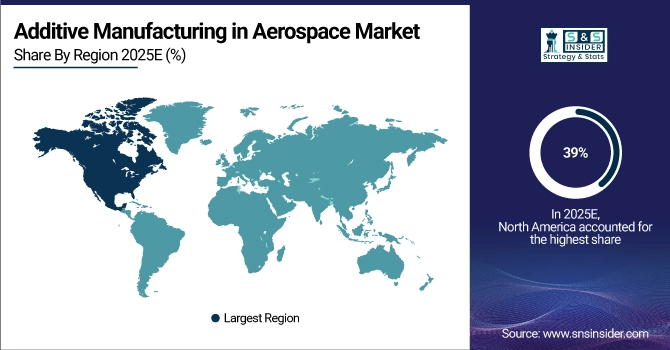

Additive Manufacturing in Aerospace Market Regional Insights:

North America Dominates Additive Manufacturing in Aerospace Market in 2025

In 2025, North America commands an estimated 39% share of the Additive Manufacturing in Aerospace Market, driven by its strong aerospace manufacturing base, high defense spending, and early adoption of advanced manufacturing technologies. The region benefits from the presence of major aerospace OEMs, defense contractors, and space agencies that increasingly rely on additive manufacturing for lightweight components, engine parts, and MRO applications. Rising commercial aircraft production, combined with digital manufacturing initiatives, further accelerates adoption, making North America the leading region in aerospace additive manufacturing.

The United States dominates the North American market due to its leadership in commercial aviation, defense programs, and space exploration. U.S.-based aerospace companies extensively use additive manufacturing to reduce production lead times, optimize part designs, and improve fuel efficiency. Strong R&D investments, supportive regulatory frameworks, and collaboration between OEMs and additive manufacturing providers reinforce the country’s dominant position in the regional market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific is the Fastest-Growing Region in Additive Manufacturing in Aerospace Market

Asia-Pacific is projected to grow at an estimated CAGR of 20.83% during 2026–2035, fueled by expanding aircraft manufacturing capabilities and rising defense modernization programs. Increasing demand for cost-efficient production methods and localized supply chains is accelerating the adoption of additive manufacturing across the region’s aerospace sector.

China dominates the Asia-Pacific market due to significant investments in domestic aircraft production, military aviation, and space programs. The country increasingly leverages additive manufacturing to shorten development cycles, reduce import dependency, and enable complex component fabrication. Government-backed initiatives promoting advanced manufacturing technologies further support rapid market expansion across aerospace applications.

Europe Additive Manufacturing in Aerospace Market Insights, 2025

Europe held a substantial share of the Additive Manufacturing in Aerospace Market in 2025, supported by advanced aerospace engineering capabilities and a strong focus on sustainability. European manufacturers adopt additive manufacturing to reduce aircraft weight, comply with strict emission regulations, and improve material efficiency. Continuous innovation in metal and composite printing technologies enables broader adoption across commercial and defense aircraft programs.

Germany leads the European market due to its strong aerospace industrial base, advanced engineering expertise, and leadership in metal additive manufacturing systems.

Middle East & Africa and Latin America Additive Manufacturing in Aerospace Market Insights, 2025

In 2025, the Middle East & Africa region showed steady adoption of additive manufacturing in aerospace, driven by expanding defense budgets and the development of aircraft MRO hubs. Countries in the Middle East increasingly use additive manufacturing to produce spare parts and reduce aircraft downtime.

Latin America also experienced gradual growth, led by Brazil and Mexico, as airlines modernize fleets and invest in localized maintenance capabilities. Both regions represent emerging markets, with additive manufacturing supporting cost efficiency and supply-chain resilience in aerospace operations.

Competitive Landscape for the Additive Manufacturing in Aerospace Market

3D Systems Corporation

3D Systems Corporation is a U.S.-based pioneer in additive manufacturing technologies, offering advanced metal and polymer 3D printing solutions tailored for aerospace applications. The company provides end-to-end solutions, including printers, materials, software, and on-demand manufacturing services. Its technologies support the production of lightweight structural components, tooling, and certified flight-ready parts. 3D Systems plays a critical role in the aerospace additive manufacturing market by enabling complex geometries, reducing material waste, and accelerating production timelines. Through close collaboration with aerospace OEMs and defense contractors, the company helps transform traditional manufacturing processes into agile, digitally driven production models that enhance performance and cost efficiency.

-

-

In February 2024, 3D Systems expanded its aerospace-qualified metal additive manufacturing portfolio, introducing enhanced titanium and aluminum alloy solutions designed for serial production of flight-critical components.

-

Stratasys Ltd.

Stratasys Ltd. is a global leader in polymer-based additive manufacturing, providing advanced 3D printing platforms widely adopted across aerospace design, tooling, and interior component production. The company specializes in high-performance thermoplastics such as ULTEM and Antero, which meet stringent aerospace standards for strength, heat resistance, and flame retardancy. Stratasys plays a vital role in the aerospace additive manufacturing market by enabling rapid prototyping, lightweight interior parts, and cost-effective tooling solutions. Its focus on production-grade polymer printing supports reduced lead times and greater design flexibility for aerospace manufacturers transitioning toward digital manufacturing.

-

-

In May 2024, Stratasys introduced an upgraded aerospace-focused polymer printing platform, enhancing build speed and material performance for aircraft interior and tooling applications.

-

EOS GmbH

EOS GmbH is a Germany-based leader in industrial metal additive manufacturing, specializing in laser powder bed fusion technologies for aerospace-grade components. The company delivers advanced 3D printing systems, materials, and software optimized for high-precision, high-strength applications such as engine parts, structural brackets, and lightweight assemblies. EOS plays a central role in the aerospace additive manufacturing market by supporting serial production and certification-ready processes. Its continuous innovation in machine performance, material development, and process stability enables aerospace manufacturers to scale additive manufacturing from prototyping to full production.

-

-

In October 2024, EOS launched an advanced metal additive manufacturing system designed to improve productivity and part consistency for aerospace and defense serial production programs.

-

GE Additive (General Electric)

GE Additive, a subsidiary of General Electric, is a key innovator in metal additive manufacturing for aerospace and aviation applications. Leveraging GE’s deep aerospace expertise, the company provides electron beam melting (EBM) and laser powder bed fusion technologies used extensively in aircraft engine and structural components. GE Additive’s role in the aerospace additive manufacturing market is highly strategic, as it enables part consolidation, weight reduction, and performance optimization in next-generation aircraft engines. Through integration with GE Aerospace’s production ecosystem, GE Additive accelerates industrial-scale adoption of additive manufacturing across commercial, defense, and space platforms.

-

-

In March 2025, GE Additive advanced the deployment of its metal additive systems for next-generation aircraft engine components, supporting higher production volumes and improved fuel-efficiency performance.

-

Additive Manufacturing in Aerospace Companies are:

-

3D Systems Corporation

-

Stratasys Ltd.

-

GE Additive (General Electric)

-

SLM Solutions Group AG

-

ExOne Company

-

Renishaw plc

-

Materialise NV

-

Voxeljet AG

-

Arcam AB

-

Concept Laser GmbH

-

EnvisionTEC GmbH

-

Markforged Inc.

-

HP Inc.

-

Desktop Metal, Inc.

-

Carbon, Inc.

-

Farsoon Technologies

-

Airbus SE

-

Boeing Company

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 8.75 Billion |

| Market Size by 2035 | US$ 44.96 Billion |

| CAGR | CAGR of 17.79 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Powder Bed Fusion, Directed Energy Deposition, Material Extrusion, Binder Jetting, Others) • By Material (Metals, Polymers, Ceramics, Composites) • By Application (Prototyping, Production Parts, Tooling, Maintenance, Repair & Overhaul (MRO)) • By Aircraft Type (Commercial Aircraft, Military Aircraft, Spacecraft, Unmanned Aerial Vehicles (UAVs)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3D Systems Corporation, Stratasys Ltd., EOS GmbH, GE Additive (General Electric), SLM Solutions Group AG, ExOne Company, Renishaw plc, Materialise NV, Optomec Inc., Voxeljet AG, Arcam AB, Concept Laser GmbH, EnvisionTEC GmbH, Markforged Inc., HP Inc., Desktop Metal, Inc., Carbon, Inc., Farsoon Technologies, Airbus SE, Boeing Company |

Frequently Asked Questions

North America leads the market, while Asia-Pacific is the fastest-growing region.

Metals such as titanium and aluminum are most widely used, followed by polymers and composites.

Powder Bed Fusion leads due to high precision and suitability for aerospace-grade metal parts.

Demand for lightweight components, fuel efficiency, faster production, and growing defense and space programs.

It is the use of 3D printing to produce aircraft and spacecraft parts with complex designs and reduced weight.

Get in Touch