Aerospace Parts Manufacturing Market Size & Trends:

The Aerospace Parts Manufacturing Market size was valued at USD 1002.46 Billion in 2025 and is projected to reach USD 1568.37 Billion by 2035, growing at a CAGR of 4.58% during 2026–2035.

The aerospace parts manufacturing market is experiencing steady growth due to rising aircraft production, fleet modernization programs, and increasing defense and space investments. Aerospace manufacturers are focusing on producing high-precision components such as airframes, engine parts, avionics housings, and structural assemblies to meet strict performance and safety standards. Growing demand for lightweight and fuel-efficient aircraft is driving the adoption of advanced materials, including composites and high-performance alloys.

Market Size and Forecast:

-

Market Size in 2025: USD 1002.46 Billion

-

Market Size by 2035: USD 1568.37Billion

-

CAGR: 4.58% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Aerospace Parts Manufacturing Market - Request Free Sample Report

Trends in the Aerospace Parts Manufacturing Market:

-

Increasing aircraft deliveries are driving higher demand for structural and engine components.

-

Rising focus on fuel efficiency is accelerating adoption of lightweight composites and advanced alloys.

-

Expansion of defense and space programs is boosting demand for high-precision, mission-critical parts.

-

Growing use of automation, robotics, and digital twins is improving manufacturing accuracy and throughput.

-

Increasing adoption of additive manufacturing enables complex part geometries and faster prototyping.

-

Stricter regulatory and quality standards are shaping advanced inspection and certification processes.

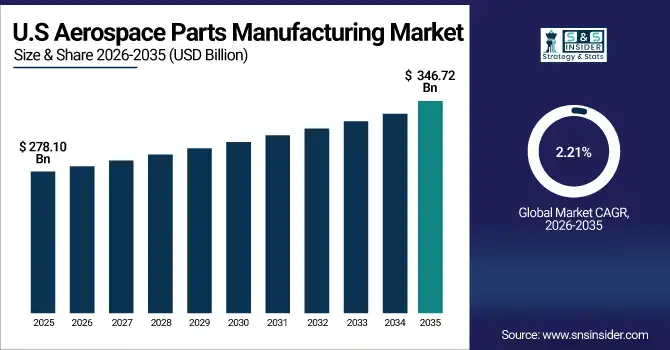

U.S. Aerospace Parts Manufacturing Market Size Outlook:

The U.S. Aerospace Parts Manufacturing Market was valued at USD 278.10 Billion in 2025 and is projected to reach USD 346.72 Billion by 2035, growing at a CAGR of 2.21%, driven by rising aircraft production, strong defense spending, and expanding space programs. Increasing investments in automation, advanced materials, and precision manufacturing further support market growth, enabling U.S. manufacturers to meet stringent quality requirements and maintain global competitiveness across commercial and defense aerospace supply chains.

Market Drivers: Rising Aircraft Production and Fleet Modernization Across Commercial and Defense Aviation

Increasing aircraft production and fleet modernization across commercial and defense aviation is a significant driver of the aerospace parts manufacturing market. As airlines expand fleets to accommodate rising passenger traffic and replace aging aircraft, demand increases for airframe structures, engine components, landing systems, and avionics housings. Similarly, defense agencies are upgrading aircraft platforms to improve fuel efficiency, performance, and mission readiness, further boosting component demand. These factors drive higher production volumes and encourage manufacturers to invest in advanced machining, automation, and quality-control systems. Additionally, growing backlogs at aircraft OEMs translate into long-term supply contracts for component manufacturers. Continuous design improvements and use of lightweight materials further accelerate demand, strengthening the overall aerospace parts manufacturing industry.

In March 2024, a major commercial aircraft manufacturer announced higher monthly production targets for narrow-body aircraft, prompting tier-1 and tier-2 suppliers to expand capacity for structural components and engine parts.

Market Restraints: High Manufacturing Costs and Strict Regulatory and Certification Requirements

High manufacturing costs and strict regulatory and certification requirements act as major restraints on the aerospace parts manufacturing industry. Aerospace components must comply with rigorous safety, performance, and traceability standards, requiring extensive testing, documentation, and certification. This increases production time and capital investment in advanced machinery, inspection equipment, and skilled labor. Rising raw material prices for titanium alloys, composites, and superalloys further elevate costs. Additionally, frequent audits and requalification processes can delay production schedules and disrupt supply chains. These factors increase operational complexity and limit scalability, particularly for small and mid-sized manufacturers. As a result, profit margins are pressured, and market entry barriers remain high, restraining overall market expansion despite strong demand.

Market Opportunities: Adoption of Advanced Manufacturing Technologies Accelerates Productivity and Design Innovation

The growing adoption of advanced manufacturing technologies presents a strong opportunity for the aerospace parts manufacturing market. Manufacturers are increasingly implementing automation, additive manufacturing, digital twins, and advanced machining to improve precision and reduce lead times. These technologies enable the production of complex geometries, lightweight components, and customized parts while minimizing material waste. As aircraft designs evolve, advanced manufacturing supports faster prototyping and improved cost efficiency. This cause-and-effect relationship shows that technology adoption enhances productivity, which then increases competitiveness and scalability.

In June 2024, several aerospace suppliers expanded metal additive manufacturing capabilities to support next-generation aircraft and space programs, creating new revenue opportunities across commercial and defense segments.

Aerospace Parts Manufacturing Market Segmentation Analysis:

By Type, Airframe Structures Segment Dominates Aerospace Parts Manufacturing Market with 43% Share in 2025, Interior Components Segment to Record Fastest Growth with 8.24% CAGR

The Airframe Structures segment held a dominant share of approximately 43% in 2025. Increasing global aircraft deliveries and fleet modernization programs are driving demand for fuselage, wing, and structural components. High-strength, lightweight airframe assemblies improve fuel efficiency and safety, prompting manufacturers to adopt advanced machining and precision fabrication techniques. Rising defense aircraft upgrades and new aircraft programs further accelerate production, boosting the aerospace parts manufacturing industry and encouraging innovation in modular and durable structures.

The Interior Components segment is expected to experience the fastest growth in the aerospace parts manufacturing market over 2026–2035 with a CAGR of 8.24%. Rising passenger expectations for comfort, luxury, and cabin amenities are driving demand for advanced seating, panels, and in-flight entertainment components. Manufacturers are focusing on lightweight, ergonomic, and modular designs to meet these evolving requirements. Expansion in premium cabins and retrofit programs for commercial aircraft further fuels the growth of interior components, supporting overall market expansion.

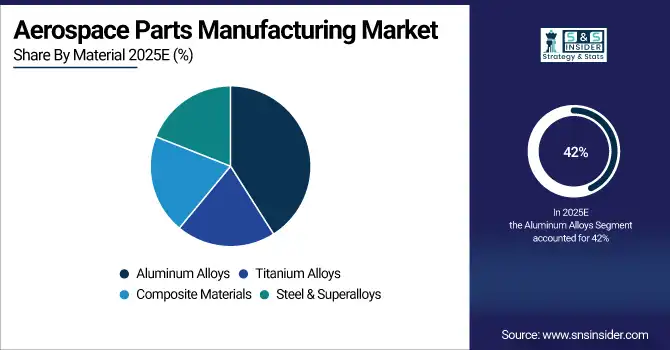

By Material, Aluminum Alloys Segment Dominates Aerospace Parts Manufacturing Market with 42% Share in 2025, Composite Materials Segment to Record Fastest Growth with 6.58% CAGR

The Aluminum Alloys segment held the largest revenue share of 42% in 2025. Its high strength-to-weight ratio and corrosion resistance make it ideal for airframe structures, wing assemblies, and engine mounts. Adoption of aluminum alloys improves fuel efficiency and reduces operating costs, prompting manufacturers to scale production and integrate advanced machining processes. The rising volume of commercial and defense aircraft production further strengthens the market, driving the aerospace parts manufacturing sector’s growth globally.

The Composite Materials segment is expected to record the fastest growth in the aerospace parts manufacturing market over 2026–2035 with a CAGR of 6.58%. Use of carbon fiber and hybrid composites reduces aircraft weight while enhancing strength and thermal resistance. Increasing integration of composites in fuselage, wings, and engine components improves performance and fuel efficiency. Advancements in composite manufacturing techniques and rising adoption across commercial and defense aircraft accelerate market expansion, establishing composites as a key growth driver in aerospace parts manufacturing.

By Aircraft Type, Commercial Aircraft Segment Dominates Aerospace Parts Manufacturing Market with 46% Share in 2025, UAVs / Drones Segment to Record Fastest Growth with 7.23% CAGR

The Commercial Aircraft segment held a dominant share of approximately 46% in 2025. Increasing passenger traffic and airline fleet expansion are driving demand for structural, propulsion, and avionics components. Aircraft OEMs and suppliers focus on lightweight, fuel-efficient materials and precision manufacturing techniques. Growing modernization and retrofit programs further contribute to demand, strengthening the aerospace parts manufacturing and fostering innovation in high-performance aircraft components.

The UAVs / Drones segment is expected to experience the fastest growth in the aerospace parts manufacturing Industry over 2026–2035 with a CAGR of 7.23%. Rising defense, surveillance, logistics, and agriculture applications drive demand for lightweight airframes, advanced propulsion, and integrated avionics. Innovation in miniaturized components and modular designs accelerates production efficiency and performance. Expanding UAV adoption globally supports aerospace parts manufacturing growth, highlighting drones as a rapidly emerging segment.

By Manufacturing Technology, Machining Segment Dominates Aerospace Parts Manufacturing Market with 43% Share in 2025, Additive Manufacturing (3D Printing) Segment to Record Fastest Growth with 5.92% CAGR

The Machining segment held a dominant share of 43% in 2025. Precision CNC machining ensures high-tolerance production for structural, engine, and landing gear components. Growing aircraft production, fleet modernization, and defense upgrades drive demand for machined parts. Advanced tooling and automated machining systems improve efficiency, supporting market expansion in aerospace parts manufacturing.

The Additive Manufacturing (3D Printing) segment is expected to record the fastest growth in the aerospace parts manufacturing Industry over 2026–2035 with a CAGR of 5.92%. Rapid prototyping and production of complex, lightweight components enhance design flexibility, reduce material waste, and shorten production cycles. Increasing adoption in commercial and defense aircraft accelerates innovation and cost efficiency, driving expansion in the aerospace parts manufacturing.

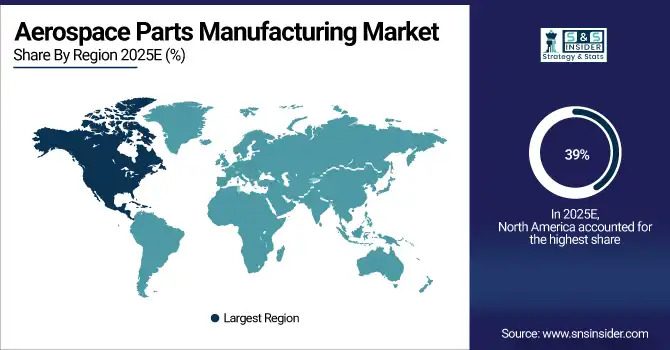

Aerospace Parts Manufacturing Market Regional Insights:

North America Dominates Aerospace Parts Manufacturing Market in 2025

In 2025, North America commands an estimated 39% share of the Aerospace Parts Manufacturing Industry. Strong aerospace and defense infrastructure, coupled with high investments in aircraft modernization and R&D, drives market growth by increasing production efficiency and advanced component adoption.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States is the dominating country in North America, hosting major aircraft manufacturers, component suppliers, and defense contractors. The U.S. leads due to extensive commercial and military aircraft programs, advanced manufacturing capabilities, and a robust supply chain. Continuous R&D investments in lightweight materials, propulsion systems, and avionics, along with government support, further solidify its leadership, driving high demand for precision aerospace parts and fueling regional market growth.

Asia-Pacific is the Fastest-Growing Region in Aerospace Parts Manufacturing Industry from 2026–2035

Asia-Pacific is projected to grow at an estimated CAGR of 7.02% during 2026–2035. Rapid industrialization, increasing commercial aircraft deliveries, and defense modernization are driving growth by boosting demand for high-precision aerospace parts and local production capabilities.

China is the dominating country in the Asia-Pacific aerospace parts manufacturing market. The nation leads due to significant investments in civil aviation expansion, large-scale military aircraft programs, and the establishment of advanced aerospace manufacturing hubs. Collaboration with international OEMs, adoption of advanced materials, and development of indigenous supply chains enhance production efficiency and innovation. Rising domestic airline fleets and defense modernization initiatives further accelerate aerospace parts demand, contributing to the region’s rapid growth.

Europe Aerospace Parts Manufacturing Market Insights, 2025

In 2025, Europe held a significant share of the Aerospace Parts Manufacturing Market, driven by advanced aerospace engineering, strong regulatory standards, and growing demand for commercial and defense aircraft components.

Germany dominates Europe’s aerospace parts market due to its robust commercial aircraft and defense manufacturing ecosystem. High-precision engineering, advanced material expertise, and a strong automotive-aerospace knowledge base drive innovation in lightweight and fuel-efficient components, ensuring Europe’s competitive advantage in aerospace parts manufacturing.

Middle East & Africa and Latin America Aerospace Parts Manufacturing Market Insights, 2025

In 2025, the Middle East & Africa and Latin America regions demonstrated steady growth in aerospace parts manufacturing. Demand is driven by expanding airline fleets, defense modernization, and infrastructure development.

The Middle East focuses on enhancing national airlines and military programs, particularly in the UAE and Saudi Arabia, boosting demand for precision aerospace components. Latin America, led by Brazil and Mexico, invests in local aerospace manufacturing and maintenance, repair, and overhaul (MRO) facilities, stimulating regional market growth. Both regions emphasize technology adoption and local production to meet rising commercial and defense aircraft requirements.

Competitive Landscape:

JAMCO Corporation

JAMCO Corporation is a Japan-based leader in aerospace interiors and component manufacturing, specializing in aircraft seating, cabin systems, and oxygen systems. With decades of experience, the company designs, engineers, and installs advanced interior solutions for commercial and business aircraft. JAMCO operates globally, serving major OEMs and airlines, and plays a pivotal role in the aerospace parts manufacturing by providing reliable, high-quality, and innovative components that enhance passenger comfort, safety, and operational efficiency. The company’s engineering expertise and strong collaborations ensure consistent supply and advanced manufacturing capabilities.

-

-

In March 2025, JAMCO introduced a next-generation lightweight aircraft seating system for wide-body aircraft, reducing weight by 15% while improving ergonomics and passenger comfort, enhancing fuel efficiency for airlines.

-

Intrex Aerospace

Intrex Aerospace is a U.S.-based manufacturer specializing in precision-engineered aerospace components, including structural assemblies, landing gear parts, and flight-critical hardware. The company focuses on high-performance materials and machining technologies to meet the stringent requirements of commercial and military aircraft. Intrex Aerospace is central to the aerospace parts manufacturing industry, providing components that ensure aircraft reliability, durability, and regulatory compliance. Its advanced production capabilities and supply chain integration allow OEMs and MRO operators to access high-quality parts efficiently, supporting rapid aircraft assembly and maintenance operations.

-

-

In July 2025, Intrex Aerospace unveiled a high-strength titanium landing gear component, improving load-bearing capacity by 12% and reducing maintenance downtime for commercial aircraft operators.

-

Rolls-Royce plc

Rolls-Royce plc is a U.K.-based global leader in aircraft engine design and manufacturing, producing engines, propulsion systems, and related aerospace components for commercial and military aviation. With over a century of experience, the company engineers high-performance, fuel-efficient engines and integrates advanced materials to optimize performance, reliability, and emissions standards. Rolls-Royce plays a key role in the aerospace parts manufacturing industry by supplying OEMs and airline operators with cutting-edge propulsion components that enhance aircraft efficiency, reduce operating costs, and comply with global environmental regulations.

-

-

In May 2025, Rolls-Royce launched its Trent XWB-97 engine variant, featuring improved thermal efficiency and reduced fuel consumption by 5%, supporting next-generation wide-body aircraft operations.

-

CAMAR Aircraft Parts Company

CAMAR Aircraft Parts Company is a U.S.-based aerospace parts manufacturer specializing in precision structural components, avionics housings, and mechanical assemblies for commercial and defense aircraft. The company combines advanced machining, additive manufacturing, and quality assurance systems to deliver high-precision parts critical to aircraft performance and safety. CAMAR’s role in the aerospace parts manufacturing industry is significant, providing OEMs and MRO providers with reliable components that meet rigorous industry standards, supporting aircraft production, maintenance, and modernization initiatives worldwide.

-

-

In January 2025, CAMAR introduced a lightweight composite avionics housing for commercial jets, reducing weight by 8% while maintaining structural integrity and improving assembly efficiency.

-

Aerospace Parts Manufacturing Companies are:

-

JAMCO Corporation

-

Rolls Royce plc

-

CAMAR Aircraft Parts Company

-

Woodward, Inc.

-

Engineered Propulsion System

-

Eaton Corporation plc

-

Aequs

-

Aero Engineering & Manufacturing Co.

-

GE Aviation

-

Lycoming Engines

-

Pratt & Whitney

-

Superior Air Parts Inc.

-

MTU Aero Engines AG

-

Honeywell International, Inc.

-

Collins Aerospace

-

Composite Technology Research Malaysia Sdn. Bhd.

-

Mitsubishi Heavy Industries Ltd.

-

Kawasaki Heavy Industries Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1002.46 Billion |

| Market Size by 2035 | USD 1568.37 Billion |

| CAGR | CAGR of 4.58 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Airframe Structures, Engine Components, Avionics & Electrical Systems, Interior Components) • By Material (Aluminum Alloys, Titanium Alloys, Composite Materials, Steel & Superalloys) • By Aircraft Type (Commercial Aircraft, Defense & Military Aircraft, Business Jets & General Aviation, UAVs / Drones) • By Manufacturing Technology (Machining, Casting, Additive Manufacturing (3D Printing), Forging) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | JAMCO Corporation, Intrex Aerospace, Rolls Royce plc, CAMAR Aircraft Parts Company, Safran Group, Woodward, Inc., Engineered Propulsion System, Eaton Corporation plc, Aequs, Aero Engineering & Manufacturing Co., GE Aviation, Lycoming Engines, Pratt & Whitney, Superior Air Parts Inc., MTU Aero Engines AG, Honeywell International, Inc., Collins Aerospace, Composite Technology Research Malaysia Sdn. Bhd., Mitsubishi Heavy Industries Ltd., Kawasaki Heavy Industries Ltd. |

Frequently Asked Questions

Get in Touch