Aerospace Engineering Services Outsourcing Market Size Analysis:

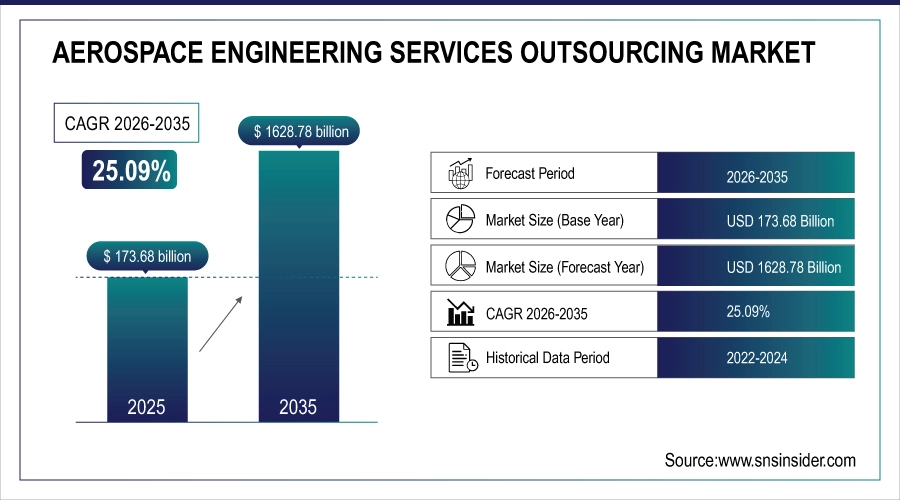

The Aerospace Engineering Services Outsourcing Market size was valued at USD 173.68 Billion in 2025 and is expected to reach USD 1628.78 Billion by 2035, growing at a CAGR of 25.09% over the forecast period of 2026-2035.

The Aerospace Engineering Services Outsourcing Market is expanding as aerospace manufacturers increasingly rely on external engineering expertise to manage complex design, validation, manufacturing, and maintenance processes. Outsourcing enables faster development cycles, access to specialized skills, reduced operational costs, and improved scalability, particularly as software-driven and digitally validated aircraft platforms become more prevalent.

Market Size and Forecast:

-

Market Size in 2025: USD 173.68 Billion

-

Market Size by 2035: USD 1628.78 Billion

-

CAGR: 25.09% From 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data Coverage: 2022–2024

To Get more information on Aerospace Engineering Services Outsourcing Market - Request Free Sample Report

Aerospace Engineering Services Outsourcing Market Trends Highlights:

-

Rising outsourcing of design, simulation, and digital validation services to manage increasing aircraft complexity and reduce development timelines

-

Growing demand for embedded software and avionics engineering as software content accounts for over 40% of modern aircraft system value

-

Expansion of offshore engineering delivery models to optimize costs while maintaining compliance with stringent aerospace regulations

-

Increased adoption of digital twins, model-based systems engineering (MBSE), and virtual testing to reduce physical prototyping costs

-

Strong demand from defense, space, and unmanned aerial systems (UAS) programs supporting long-term engineering service contracts

-

Challenges related to data security, intellectual property protection, regulatory compliance, and integration across distributed engineering teams

U.S. Aerospace Engineering Services Outsourcing Market Driven by Aircraft Programs and Digital Transformation

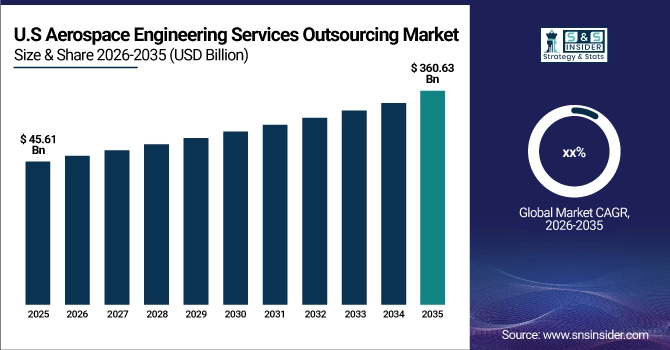

The U.S. Aerospace Engineering Services Outsourcing Market size was valued at USD 45.61 billion in 2025 and is expected to reach USD 360.63 billion by 2035. Growth is supported by strong commercial aircraft backlogs, rising defense modernization programs, and increasing reliance on outsourced digital engineering and simulation services. Over 60% of U.S.-based aerospace OEMs outsource at least part of their engineering workflows, while investments in digital twins, autonomous systems, and advanced avionics continue to accelerate demand for specialized engineering partners.

Aerospace Engineering Services Outsourcing Market Drivers:

-

Rising aircraft complexity and digital engineering adoption drive increased reliance on outsourced aerospace engineering services globally.

Increasing aircraft system complexity combined with the rapid adoption of digital engineering tools is a major driver of the Aerospace Engineering Services Outsourcing Market. Modern aircraft platforms integrate advanced avionics, embedded software, lightweight materials, and digital twins, significantly increasing engineering workload and specialization requirements. As a result, aerospace OEMs and Tier-1 suppliers increasingly outsource design, simulation, and validation activities to access specialized expertise and accelerate development timelines. Outsourcing also helps manage cost pressures and engineering talent shortages while ensuring compliance with strict regulatory standards. The growing aircraft production backlog and expansion of defense and space programs further intensify the need for scalable engineering resources, reinforcing outsourcing as a strategic solution rather than a short-term cost-saving approach.

Aerospace Engineering Services Outsourcing Market Restraints:

-

Stringent regulatory compliance, data security concerns, and intellectual property risks limit the extent of aerospace engineering outsourcing adoption.

Aerospace engineering services outsourcing faces restraints due to strict regulatory frameworks, export control laws, and heightened concerns around data security and intellectual property protection. Aerospace programs operate under rigorous certification and compliance requirements, particularly in defense, space, and dual-use applications. Outsourcing engineering activities across global delivery centers increases the risk of data breaches, compliance inconsistencies, and unauthorized access to sensitive design information. These risks create hesitation among OEMs to outsource mission-critical engineering functions, resulting in longer vendor qualification cycles and restricted outsourcing scopes.

Aerospace Engineering Services Outsourcing Market Opportunities:

-

Expansion of software-defined aircraft, autonomous systems, and digital aviation platforms creates new growth opportunities for outsourcing providers.

The increasing shift toward software-defined aircraft and autonomous aviation systems presents a strong opportunity for the Aerospace Engineering Services Outsourcing Market. As software content becomes a dominant component of aircraft system value, demand rises for specialized embedded software, systems engineering, cybersecurity, and digital validation services. Aerospace companies increasingly outsource these functions to accelerate innovation cycles, address software talent shortages, and manage growing system complexity. The development of unmanned aerial vehicles, advanced air mobility platforms, and autonomous flight technologies further amplifies demand for external engineering expertise. Outsourcing enables faster prototyping, testing, and certification of software-intensive aerospace systems, opening new long-term revenue streams for service providers.

According to research, software now accounts for over 40% of the total value of next-generation aircraft systems, significantly increasing demand for outsourced embedded software and digital engineering services.

Aerospace Engineering Services Outsourcing Market Segmentation Analysis:

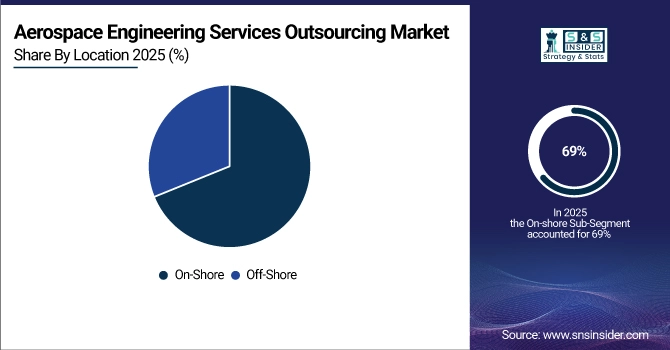

By Location, On-shore Services Dominate While Off-shore Outsourcing Expands Rapidly

The On-shore segment dominated the market with a 69% revenue share in 2025, supported by stringent regulatory requirements, defense contracts, and intellectual property sensitivity. Aerospace OEMs prefer on-shore outsourcing for critical design, certification, and systems integration tasks to ensure compliance and security. Product development programs involving defense modernization, space exploration, and next-generation aircraft platforms reinforced on-shore service dominance within the Aerospace Engineering Services Outsourcing Market.

The Off-shore segment is anticipated to grow at the fastest CAGR of 26.43% during 2026–2035 due to cost optimization and talent availability. Rising engineering labor costs in developed regions have caused OEMs to expand offshore delivery centers for software development, simulation, and documentation. Product development cycles increasingly leverage offshore teams for scalable execution, accelerating off-shore outsourcing adoption and strengthening its growth trajectory in the Aerospace Engineering Services Outsourcing Market.

By Service, Mechanical Engineering Leads Market While Embedded Software Engineering Registers Fastest Growth

The Mechanical Engineering segment dominated the Aerospace Engineering Services Outsourcing Market with a 39% revenue share in 2025, driven by high demand for structural design, aerodynamics, thermal analysis, and materials engineering. Increasing aircraft production rates and the need for lightweight, fuel-efficient airframes have caused OEMs to outsource mechanical design and stress analysis to specialized service providers. Product development initiatives focusing on composite structures, additive manufacturing, and next-generation propulsion systems further strengthened outsourcing demand, reinforcing Mechanical Engineering’s dominant role in supporting cost-efficient and scalable aerospace programs.

The Embedded Software Engineering segment is expected to grow at the highest CAGR of 28.92% during 2026–2035 due to the rapid shift toward software-defined aircraft. Increasing integration of avionics, flight control systems, and autonomous functionalities has caused software content to exceed 40% of total aircraft system value. This complexity drives OEMs to outsource embedded software development, verification, and cybersecurity. Product development in autonomous flight systems, unmanned aerial vehicles, and digital cockpits significantly accelerates outsourcing demand within the Aerospace Engineering Services Outsourcing Market.

By Function, Design Segment Dominates Revenue While Simulation & Digital Validation Grows Rapidly

The Design segment held the largest revenue share of 42% in 2025, as aircraft manufacturers increasingly outsourced conceptual, detailed, and systems-level design activities. Rising demand for new aircraft platforms, cabin modernization, and lightweight component design has driven outsourcing to accelerate development cycles. Product development initiatives involving composite structures, modular aircraft architectures, and next-generation propulsion systems intensified the need for external design expertise, making design outsourcing a foundational contributor to revenue growth in the Aerospace Engineering Services Outsourcing Market.

The Simulation & Digital Validation segment is projected to grow at the highest CAGR of 30.02% from 2026 to 2035, driven by the need to reduce physical testing costs and certification timelines. Increased adoption of digital twins, model-based systems engineering, and virtual certification has caused OEMs to outsource simulation-intensive workloads. Product development focused on virtual flight testing, predictive maintenance modeling, and regulatory compliance validation continues to accelerate demand, positioning digital validation as a high-growth driver within the Aerospace Engineering Services Outsourcing Market.

By Component, Hardware Leads Market While Software Registers Fastest Growth

The Hardware segment accounted for the largest revenue share of 57% in 2025E, driven by extensive outsourcing of structural components, avionics hardware integration, and mechanical assemblies. Increasing aircraft production volumes and demand for lightweight, high-performance components caused OEMs to rely on external engineering support for hardware development and validation. Product development in advanced materials and propulsion systems reinforced hardware outsourcing demand within the Aerospace Engineering Services Outsourcing Market.

The Software segment is expected to grow at the highest CAGR of 26.01% over the forecast period, driven by increasing software content in modern aircraft. The shift toward software-defined avionics, digital cockpits, and autonomous flight systems has caused OEMs to outsource software development and validation. Product development in AI-enabled systems and cybersecurity accelerates software outsourcing demand, making it a critical growth engine for the Aerospace Engineering Services Outsourcing Market.

Aerospace Engineering Services Outsourcing Market Regional Insights:

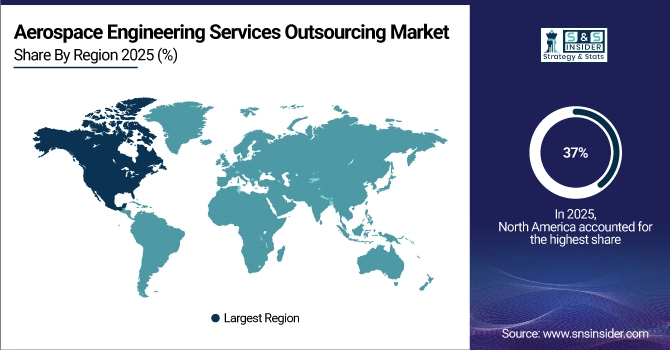

North America Dominates Aerospace Engineering Services Outsourcing Market in 2025

In 2025, North America commands an estimated 37% share of the Aerospace Engineering Services Outsourcing Market, driven by high commercial aircraft backlogs, defense modernization programs, and advanced aerospace R&D infrastructure. OEMs and Tier-1 suppliers increasingly outsource design, simulation, and embedded software development to accelerate innovation, reduce costs, and meet stringent regulatory standards. Strong investment in autonomous systems, space programs, and next-generation propulsion technologies further amplifies demand, making North America the focal point for aerospace engineering outsourcing.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States is the dominating country in North America, hosting major OEMs, defense contractors, and space agencies. Its leadership stems from advanced R&D capabilities, extensive regulatory frameworks, and high-value aircraft production, which drive significant outsourcing of design, digital validation, and embedded software development.

Asia-Pacific is the Fastest-Growing Region in Aerospace Engineering Services Outsourcing Market During 2026–2035

Asia-Pacific is projected to grow at an estimated CAGR of 28.29% during 2026–2035, fueled by cost-effective engineering talent, increasing aircraft manufacturing, and expanding offshore delivery centers. The region’s growth is driven by rising demand from North America and Europe to outsource embedded software, simulation, and documentation services, supporting scalable development cycles and faster time-to-market for advanced aircraft platforms.

India dominates the Asia-Pacific market due to its large pool of aerospace engineers, cost advantages, and presence of global engineering service providers. Government support for aerospace manufacturing and defense modernization programs accelerates outsourcing adoption, particularly in software engineering, digital validation, and systems integration.

Europe Aerospace Engineering Services Outsourcing Market Insights, 2025

Europe held a significant portion of the Aerospace Engineering Services Outsourcing Market in 2025, supported by advanced aerospace R&D programs and sustainability-focused aircraft development. Stringent emission regulations and digital aircraft programs drive OEMs to outsource design, simulation, and lightweight material engineering.

Germany dominates Europe’s market due to its strong engineering expertise, automotive-to-aerospace technology transfer, and presence of leading aerospace suppliers. The country’s emphasis on innovation, fuel efficiency, and regulatory compliance reinforces its leadership in aerospace engineering outsourcing within Europe.

Middle East & Africa and Latin America Aerospace Engineering Services Outsourcing Market Insights, 2025

In 2025, Middle East & Africa showed moderate growth driven by MRO hub expansion, defense procurement, and national aerospace ambitions. The UAE and Saudi Arabia lead the region by outsourcing engineering services to support fleet expansion and local aerospace initiatives.

Latin America experienced steady growth, led by Brazil and Mexico, supported by regional aircraft manufacturing, cost-effective engineering talent, and nearshore outsourcing demand from North America. Both regions are emerging markets focusing on sustainable aerospace growth and operational efficiency.

Competitive Landscape for the Aerospace Engineering Services Outsourcing Market:

Altair Engineering Inc.

Altair Engineering Inc. is a U.S.-based leader in simulation-driven design, product development, and engineering software solutions for aerospace, automotive, and industrial sectors. The company provides specialized services in structural analysis, multi-physics simulation, and digital twin development, enabling aerospace OEMs and suppliers to optimize performance, reduce weight, and accelerate time-to-market. Its role in the Aerospace Engineering Services Outsourcing Market is critical, as it combines software platforms with engineering consulting to deliver scalable, high-precision solutions across mechanical, electrical, and embedded systems. Altair’s offerings support both design and validation phases of aircraft development.

-

In March 2025, Altair Engineering expanded its aerospace service offerings with advanced cloud-based simulation tools, allowing OEMs to run high-fidelity structural and thermal simulations across distributed teams, reducing physical prototyping costs and shortening development cycles.

Alten Group

Alten Group is a France-based global engineering and R&D services provider specializing in aerospace, defense, automotive, and digital systems. It delivers design, embedded software, and systems engineering solutions, helping aerospace clients optimize product development, manage complex programs, and meet regulatory compliance. Alten’s role in the Aerospace Engineering Services Outsourcing Market is significant, providing multidisciplinary expertise that accelerates aircraft development and integrates digital engineering, simulation, and embedded software services to OEMs and Tier-1 suppliers worldwide. Its engineering teams support projects across mechanical, electrical, and software domains.

-

In January 2025, Alten Group launched a dedicated aerospace digital validation center in Germany, enabling virtual testing of flight-critical components and embedded systems, reducing certification timelines and strengthening outsourcing adoption.

Capgemini Engineering

Capgemini Engineering, formerly Altran, is a global leader in engineering and R&D services, providing design, simulation, embedded software, and digital transformation solutions to aerospace and defense clients. The company specializes in integrating advanced software platforms, IoT-enabled systems, and autonomous technologies into aircraft platforms. Capgemini’s role in the Aerospace Engineering Services Outsourcing Market is pivotal, supporting OEMs in reducing product development cycles, accelerating innovation, and delivering compliant, high-performance solutions for both commercial and defense programs. Its services cover mechanical, electrical, and software engineering at scale.

-

In February 2025, Capgemini Engineering introduced a collaborative digital twin platform for aerospace OEMs, enabling real-time simulation and predictive maintenance workflows, enhancing outsourcing efficiency and system reliability.

Bertrandt AG

Bertrandt AG is a Germany-based aerospace and automotive engineering services provider, offering design, simulation, systems integration, and embedded software development. The company supports complex aircraft projects, providing outsourced expertise in mechanical structures, avionics systems, and digital validation. Bertrandt’s role in the Aerospace Engineering Services Outsourcing Market is key, as it helps OEMs manage engineering capacity, reduce time-to-market, and optimize aircraft performance while maintaining regulatory compliance. Its services encompass product design, virtual testing, and embedded software development for commercial, defense, and space programs.

-

In April 2025, Bertrandt AG launched an advanced simulation and structural optimization service for next-generation aircraft fuselage designs, enabling clients to minimize weight and production costs while improving certification readiness.

Aerospace Engineering Services Outsourcing Companies are:

-

Alten Group

-

Capgemini Engineering (formerly Altran)

-

Bertrandt AG

-

EWI (EWI Technology)

-

ITK Engineering GmbH

-

L&T Technology Services Limited

-

LISI Group

-

Teledyne Technologies Incorporated

-

BAE Systems Plc.

-

L3Harris Technologies, Inc.

-

Elbit Systems Ltd.

-

RTX Corporation (parent of Collins Aerospace & Pratt & Whitney)

-

HCL Technologies (HCLTech)

-

Cyient Ltd.

-

Infosys Limited

-

Wipro Limited

-

QuEST Global

-

Tech Mahindra

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 173.68 Billion |

| Market Size by 2035 | US$ 1628.78 Billion |

| CAGR | CAGR of 25.09 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service (Mechanical Engineering, Electric/Electronic Engineering, Embedded Software Engineering, Others) • By Function (Design, Simulation & Digital Validation, Production Process, Maintenance Process) • By Location (On-shore, Off-shore • By Component (Hardware, Software) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Altair Engineering Inc., Alten Group, Capgemini Engineering (formerly Altran), Bertrandt AG, EWI (EWI Technology), Honeywell International Inc., ITK Engineering GmbH, L&T Technology Services Limited, LISI Group, Teledyne Technologies Incorporated, BAE Systems Plc., L3Harris Technologies, Inc., Elbit Systems Ltd., RTX Corporation (parent of Collins Aerospace & Pratt & Whitney), HCL Technologies (HCLTech), Cyient Ltd., Infosys Limited, Wipro Limited, QuEST Global, Tech Mahindra. |

Get in Touch