Land Based Smart Weapons Market Report Scope & Overview:

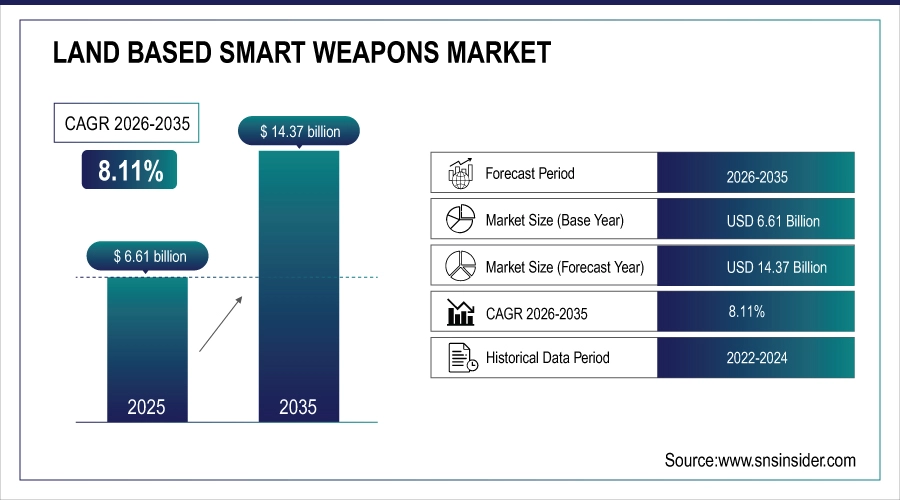

The Land Based Smart Weapons Market is valued at USD 6.61 billion in 2025 and is expected to reach USD 14.37 billion by 2035, growing at a CAGR of 8.11 % from 2026-2035.

The Land Based Smart Weapons Market is growing due to increasing defense modernization programs and rising demand for precision-guided munitions. Armed forces are focusing on enhancing accuracy, reducing collateral damage, and improving battlefield effectiveness through advanced guidance, navigation, and targeting technologies. Integration of AI, sensors, and network-centric warfare systems is further improving operational capabilities. Additionally, growing geopolitical tensions, asymmetric warfare threats, and increased defense budgets across major countries are driving procurement of advanced land-based smart weapons, supporting sustained market growth over the forecast period.

87% of major defense forces globally accelerated procurement of land-based smart weapons driven by modernization mandates, AI-enabled targeting, and network-centric warfare integration to enhance precision, minimize collateral damage, and counter evolving asymmetric threats.

Land Based Smart Weapons Market Size and Forecast

-

Market Size in 2025: USD 6.61 Billion

-

Market Size by 2035: USD 14.37 Billion

-

CAGR: 8.11 % from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Land Based Smart Weapons Market - Request Free Sample Report

Land Based Smart Weapons Market Trends

-

Rising defense modernization programs driving adoption of advanced precision-guided and network-enabled land-based weapon systems

-

Increasing integration of artificial intelligence and autonomous targeting technologies to enhance battlefield accuracy and responsiveness

-

Growing demand for long-range and high-precision munitions to strengthen deterrence and operational effectiveness

-

Expansion of military digitization initiatives supporting sensor fusion and real-time battlefield data integration

-

Rising focus on modular and upgradeable weapon platforms to extend service life and reduce lifecycle costs

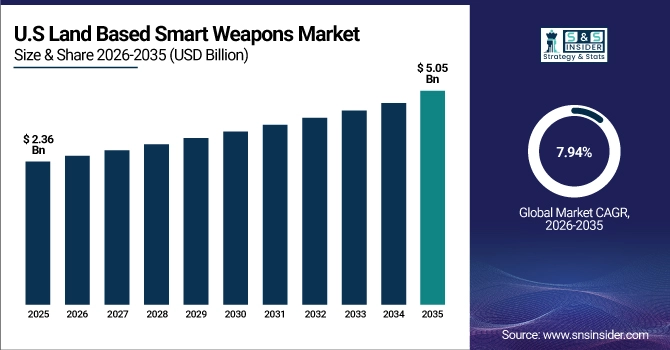

U.S. Land Based Smart Weapons Market is valued at USD 2.36 billion in 2025 and is expected to reach USD 5.05 billion by 2035, growing at a CAGR of 7.94 % from 2026-2035.

The U.S. Land Based Smart Weapons Market is growing due to ongoing military modernization and strong investment in precision-guided munitions. The focus on improving battlefield accuracy, reducing collateral damage, and integrating advanced guidance, sensors, and networked combat systems is driving adoption. Rising defense budgets and evolving threat environments further support steady market expansion.

Land Based Smart Weapons Market Growth Drivers:

-

Growing adoption of digital transformation in laboratories and increasing demand for efficient data management are driving ELN implementation across academic, pharmaceutical, and industrial research environments

Laboratories across pharmaceutical, biotechnology, academic, and industrial sectors are increasingly adopting digital tools to enhance productivity and streamline data management. Electronic Lab Notebooks (ELNs) provide structured, searchable, and centralized storage of experimental data, replacing traditional paper notebooks. The need to improve collaboration, reduce manual errors, and accelerate research timelines is driving adoption. Additionally, ELNs facilitate integration with laboratory information management systems (LIMS), laboratory instruments, and cloud platforms, enabling seamless workflows. The global push for operational efficiency, digital transformation, and real-time data access is significantly fueling ELN market growth.

86% of academic, pharmaceutical, and industrial research labs implemented Electronic Lab Notebooks (ELNs) accelerated by digital transformation initiatives and the urgent need for efficient, structured, and scalable scientific data management.

-

Rising focus on regulatory compliance, data integrity, and research reproducibility is accelerating demand for secure and audit-ready electronic lab notebook solutions globally

Strict regulations in pharmaceutical, clinical, and chemical research require accurate documentation, traceability, and audit trails. ELNs ensure data integrity and compliance with regulatory frameworks such as FDA 21 CFR Part 11, GLP, and GMP standards. Researchers benefit from standardized protocols, automated record-keeping, and reproducibility of experimental results. These capabilities reduce the risk of non-compliance penalties and enhance trust in research outcomes. The growing emphasis on reproducible science and transparent data management is driving laboratories to adopt secure, audit-ready ELNs, further expanding the global market across both academic and commercial research environments.

84% of research institutions globally prioritized secure, audit-ready Electronic Lab Notebook (ELN) solutions driven by stringent regulatory requirements, data integrity mandates, and the critical need for reproducible, traceable scientific research.

Land Based Smart Weapons Market Restraints:

-

High implementation costs, integration challenges with legacy laboratory systems, and user resistance to digital workflows limit ELN adoption, particularly among small research organizations

Implementing ELNs requires significant investment in software licenses, IT infrastructure, training, and support services. Small laboratories and academic institutions with limited budgets often find adoption cost-prohibitive. Additionally, integrating ELNs with existing LIMS, instruments, and data systems can be technically complex, requiring specialized expertise. Resistance from researchers accustomed to traditional paper-based workflows further slows adoption. Concerns about learning curves, usability, and workflow disruption contribute to reluctance in deployment. These financial, technical, and cultural barriers hinder market penetration, particularly among small or resource-constrained organizations, limiting the overall growth potential of the ELN market.

77% of small research organizations limited ELN adoption due to high implementation costs, difficulties integrating with legacy lab systems, and resistance to digital workflow changes hindering broader modernization of scientific data management.

-

Data security concerns, privacy risks, and fear of intellectual property loss restrain ELN deployment in highly sensitive research and proprietary development environments

Research data stored in ELNs, especially in pharmaceutical and biotech sectors, is highly confidential. Concerns over cyberattacks, unauthorized access, or accidental data leaks make organizations cautious about digital adoption. Intellectual property protection is critical, and companies fear that cloud-based ELNs may compromise sensitive formulations or proprietary protocols. These security and privacy concerns, coupled with regulatory scrutiny, create hesitancy in implementation. Without robust encryption, secure access controls, and compliance with data protection regulations, organizations may delay or avoid ELN adoption, restricting widespread market growth despite strong functional benefits.

79% of research organizations in highly sensitive sectors such as pharmaceuticals and defense delayed ELN adoption due to data security concerns, privacy risks, and fears of intellectual property exposure, despite the platforms’ operational benefits.

Land Based Smart Weapons Market Opportunities:

-

Advancements in cloud computing, AI, and laboratory automation create opportunities to enhance ELN functionality, collaboration, and real-time data analytics capabilities

Emerging technologies such as cloud platforms, artificial intelligence, machine learning, and IoT-enabled lab instruments are revolutionizing ELNs. Cloud-based ELNs provide remote accessibility, scalability, and lower infrastructure costs, while AI-driven analytics help researchers derive insights faster. Integration with automated laboratory equipment reduces manual data entry and errors. Real-time collaboration tools within ELNs enhance teamwork across geographically dispersed research teams. These innovations allow vendors to offer feature-rich solutions that improve efficiency, accuracy, and decision-making in laboratories, creating significant growth potential for the ELN market across industries and academic institutions.

85% of Electronic Lab Notebook (ELN) platforms integrated cloud computing, AI, and lab automation enabling real-time data analytics, seamless collaboration, and intelligent experiment management across global R&D teams.

-

Increasing R&D investments in pharmaceuticals, biotechnology, and life sciences offer strong growth opportunities for ELN vendors across emerging and developed markets

Rising global investments in R&D, particularly in drug discovery, diagnostics, and personalized medicine, are driving demand for advanced laboratory tools. ELNs help researchers manage complex experimental data, ensure regulatory compliance, and accelerate innovation. Developed markets, including North America and Europe, are witnessing extensive ELN adoption due to advanced infrastructure, while emerging markets show growing interest as pharmaceutical and biotech sectors expand. Increased funding for clinical trials, scientific research, and laboratory modernization creates a strong opportunity for ELN providers to capture new clients, expand geographic reach, and strengthen market presence globally.

83% of ELN vendors expanded their market presence fueled by rising R&D investments in pharmaceuticals, biotech, and life sciences enabling digital transformation of lab workflows across both emerging and developed economies.

Land Based Smart Weapons Market Segment Highlights

-

By Weapon Type: Precision‑Guided Missiles led with 32% share, while Smart Artillery & Howitzers is the fastest-growing segment.

-

By Platform: Armored Vehicles led with 34% share, while Infantry Carriers is the fastest-growing segment.

-

By Guidance Technology: GPS / Satellite-Guided led with 30% share, while Combination / Hybrid Guidance is the fastest-growing segment.

-

By Application: Offensive Operations led with 36% share, while Border Security is the fastest-growing segment.

-

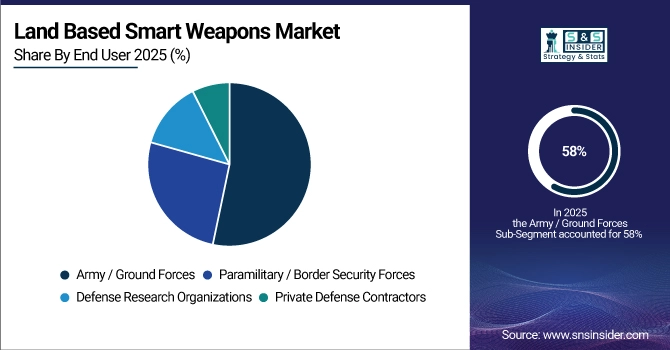

By End User: Army / Ground Forces led with 58% share, while Paramilitary / Border Security Forces is the fastest-growing segment.

Land Based Smart Weapons Market Segment Analysis

By End User: Army / Ground Forces led, while Paramilitary / Border Security Forces is the fastest-growing segment.

Army and ground forces dominate as the primary end users of land-based smart weapons. They operate across conventional, urban, and asymmetric warfare scenarios, leveraging precision-guided missiles, guided rockets, and smart artillery. Their significant procurement budgets, structured modernization programs, and tactical doctrines drive large-scale adoption. Integration with armored vehicles, tanks, and command networks ensures optimal operational efficiency. Army end users prioritize weapon effectiveness, survivability, and networked operations, reinforcing their dominance as the key revenue-generating segment in the smart weapons market.

Paramilitary and border security forces are the fastest-growing end-user segment due to the increasing need for territorial defense, surveillance, and rapid-response capabilities. Smart weapons enhance their ability to manage cross-border threats, prevent infiltration, and respond to asymmetric attacks. Adoption is accelerated by procurement programs, integration of automated systems, and the need for precision in high-risk zones. Expansion of technology-enabled border monitoring, small-scale mobile units, and cost-effective deployment options contribute to strong growth, positioning paramilitary and border security forces as a high-growth end-user segment in the market.

By Weapon Type: Precision‑Guided Missiles led, while Smart Artillery & Howitzers is the fastest-growing segment

Precision-Guided Missiles dominate the land-based smart weapons market due to their unmatched accuracy, long-range capability, and operational flexibility. They enable forces to conduct high-precision strikes while minimizing collateral damage, making them critical for modern offensive operations. Widely deployed on armored vehicles, tanks, and artillery platforms, these missiles integrate with advanced guidance systems like GPS and laser targeting. Continuous modernization programs and procurement by armies globally reinforce their dominance. Their ability to engage high-value targets with reduced risk to personnel and enhanced battlefield effectiveness positions precision-guided missiles as the largest revenue-generating weapon type.

Smart Artillery and Howitzers are the fastest-growing weapon type, driven by modernization of indirect fire systems and network-centric battlefield integration. These systems combine precision guidance, automated targeting, and real-time battlefield analytics to enhance operational accuracy. Rising demand is fueled by armies seeking cost-effective alternatives to missile strikes for area suppression and long-range engagement. Integration with advanced command-and-control systems, automated fire control, and GPS guidance enables rapid deployment and high operational efficiency. Increasing procurement in emerging markets and modernization of legacy artillery contribute to strong growth momentum for this segment.

By Platform: Armored Vehicles led, while Infantry Carriers is the fastest-growing segment.

Armored vehicles dominate as the primary deployment platform for land-based smart weapons due to mobility, protection, and integration capabilities. They carry a wide range of munitions, including precision-guided missiles and guided rockets, while providing crew safety and battlefield maneuverability. Armored platforms allow real-time coordination with command systems and rapid engagement of targets. High adoption by armies worldwide, combined with modernization programs and integration of advanced sensors and communication networks, reinforces their dominance. Armored vehicles serve as a key enabler for deploying smart weapons efficiently across varied combat environments.

Infantry carriers are the fastest-growing platform segment as armies increasingly integrate smart weapons for dismounted and mechanized infantry operations. These carriers provide mobility, protection, and firepower to small units while supporting anti-tank guided missiles and automated weapon systems. The growth is driven by rising urban warfare needs, asymmetric threats, and modernization programs emphasizing troop survivability and rapid deployment. Technological enhancements in automation, sensor fusion, and platform-network integration accelerate adoption. Infantry carriers enable smaller units to deliver precision fire effectively, making them a high-growth segment in the smart weapons market.

By Guidance Technology: GPS / Satellite-Guided led, while Combination / Hybrid Guidance is the fastest-growing segment.

GPS/Satellite-guided systems dominate due to their high accuracy, long-range capability, and all-weather operational advantage. These systems allow precision targeting in diverse terrains and combat conditions, reducing collateral damage and increasing mission success. Widely integrated with missiles, artillery, and rockets, they enable network-centric operations and seamless coordination with command-and-control platforms. Their reliability, global coverage, and compatibility with modern smart weapons reinforce dominance. Procurement programs globally prioritize GPS-guided solutions to enhance operational readiness, battlefield efficiency, and tactical advantage, making it the largest guidance technology segment in the market.

Combination or hybrid guidance systems are the fastest-growing segment due to their ability to overcome countermeasure and jamming threats while improving target acquisition accuracy. These systems integrate multiple sensor types, including GPS, laser, infrared, and electro-optical guidance, ensuring adaptability in complex combat scenarios. Growth is fueled by increasing adoption in precision-guided missiles, smart artillery, and advanced rockets, as militaries demand resilient targeting solutions. Rising investment in next-generation battlefield technologies, combined with the need for versatility in urban and asymmetric warfare, positions hybrid guidance as a high-growth segment in smart weapons systems.

By Application: Offensive Operations led, while Border Security is the fastest-growing segment.

Offensive operations dominate as the primary application for land-based smart weapons, driving adoption of precision-guided missiles, rockets, and artillery. Modern militaries prioritize rapid, accurate strike capabilities to engage strategic targets while minimizing collateral damage. Smart weapons integrated with advanced guidance, targeting, and fire-control systems enhance battlefield effectiveness, operational efficiency, and mission success. High-volume procurement by armies worldwide for combat readiness and modernization programs reinforces dominance. Offensive operations leverage smart weapons to maintain tactical superiority, ensure precision engagement, and strengthen operational outcomes, making it the largest market application segment.

Border security is the fastest-growing application segment due to rising geopolitical tensions and the need for surveillance and rapid response. Smart weapons deployed in border zones provide deterrence, precision targeting, and real-time operational capability. Growth is driven by demand for automated monitoring, counter-infiltration measures, and low-collateral engagement options. Integration with sensors, automated turrets, and networked systems enhances effectiveness in both defensive and offensive border security missions. Emerging markets, modernization programs, and technological advancements collectively accelerate the adoption of smart weapons in border security operations, driving robust segment growth.

Land Based Smart Weapons Market Regional Analysis

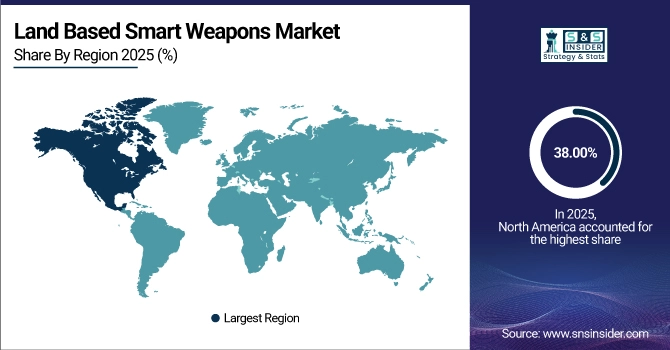

North America Land Based Smart Weapons Market Insights:

North America dominated the Land Based Smart Weapons Market with a 38.00% share in 2025 due to its advanced defense infrastructure, high military spending, and strong presence of leading defense manufacturers. Continuous modernization of armed forces, integration of advanced targeting systems, and extensive R&D investments further reinforced the region’s leadership in smart weapon technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Land Based Smart Weapons Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 9.71% from 2026–2035, driven by increasing defense budgets, modernization of military arsenals, and rising regional security concerns. Rapid adoption of advanced smart weapons, growing domestic defense manufacturing capabilities, and strategic government initiatives to strengthen national security accelerate market growth across the region.

Europe Land Based Smart Weapons Market Insights

Europe held a significant share in the Land Based Smart Weapons Market in 2025, supported by its advanced defense infrastructure, well-established military technology manufacturers, and continuous modernization of armed forces. Strong government investments in defense R&D, strategic collaborations, and adoption of advanced targeting and autonomous systems further reinforced Europe’s market presence.

Middle East & Africa and Latin America Land Based Smart Weapons Market Insights

The Middle East & Africa and Latin America together demonstrated steady growth in the Land Based Smart Weapons Market in 2025, driven by increasing defense budgets, rising geopolitical tensions, and growing demand for modernized military equipment. Expansion of domestic defense manufacturing, strategic defense partnerships, and adoption of advanced smart weapon systems contributed to the regions’ gradually strengthening market position.

Land Based Smart Weapons Market Competitive Landscape:

Lockheed Martin Corporation

Lockheed Martin Corporation is a leading global aerospace and defense company with a strong presence in the land-based smart weapons market. It develops advanced precision-guided missiles, rockets, and integrated ground-launched weapon systems used by armed forces worldwide. Its portfolio emphasizes high accuracy, advanced guidance, and network-centric capabilities. Through continuous investment in research and development, Lockheed Martin enhances sensor fusion, targeting precision, and battlefield effectiveness while supporting modern military modernization programs.

-

May 2024, Lockheed Martin successfully completed flight tests of the Precision Strike Missile (PrSM) Increment 2, featuring a multi-mode seeker (RF + imaging infrared) for moving target engagement on land.

Raytheon Technologies Corporation

Raytheon Technologies Corporation plays a key role in the land-based smart weapons market through its development of guided missiles, precision munitions, and advanced fire-control systems. The company integrates sophisticated guidance, radar, and sensor technologies to improve targeting accuracy and operational reliability. Raytheon’s smart weapon solutions are widely used by global defense forces, supporting enhanced strike precision, reduced collateral damage, and improved mission effectiveness across diverse land combat scenarios.

-

November 2024, RTX (via its Raytheon business) announced the U.S. Army adoption of the Ground-Launched BRIMSTONE, a variant of the UK-developed precision missile, now integrated onto Stryker and JLTV platforms.

BAE Systems plc

BAE Systems plc is a major defense and security company offering a broad range of land-based smart weapons, including precision-guided munitions, artillery systems, and advanced fire-control solutions. The company focuses on improving battlefield accuracy, survivability, and mobility through digital integration and modular designs. BAE Systems supports ground forces worldwide by delivering smart weapon technologies that enable precise engagement, improved situational awareness, and enhanced operational flexibility in modern combat environments.

-

February 2025, BAE Systems launched iMPS, a next-generation munition programming and fire control system that enables real-time fuzing and targeting updates for 155mm smart artillery shells, including Bofors STRIX and Excalibur-compatible rounds.

Land Based Smart Weapons Market Key Players

Some of the Land Based Smart Weapons Market Companies are:

-

Raytheon Technologies Corporation

-

Northrop Grumman Corporation

-

General Dynamics Corporation

-

Thales Group

-

MBDA Missile Systems

-

Rheinmetall AG

-

Saab AB

-

Rafael Advanced Defense Systems Ltd.

-

L3Harris Technologies, Inc.

-

Kongsberg Gruppen ASA

-

Elbit Systems Ltd.

-

Israel Aerospace Industries Ltd.

-

Textron Inc.

-

The Boeing Company (Defense, Space & Security)

-

Hanwha Aerospace Co. Ltd.

-

Diehl Defence GmbH & Co. KG

-

Poongsan Corporation

-

Safran SA

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 6.61 Billion |

| Market Size by 2035 | USD 14.37 Billion |

| CAGR | CAGR of 8.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Weapon Type: Precision-Guided Missiles, Guided Rockets, Smart Artillery & Howitzers, Smart Small Arms, Anti-Tank Guided Missiles (ATGMs) • By Platform: Armored Vehicles, Tanks & Self-Propelled Guns, Infantry Carriers, Fixed Installations / Defense Systems • By Guidance Technology: Laser-Guided, Infrared / Thermal-Guided, GPS / Satellite-Guided, Electro-Optical-Guided, Combination / Hybrid Guidance • By Application: Offensive Operations, Defensive Operations, Counter-Terrorism, Border Security, Urban Warfare • By End User: Army / Ground Forces, Paramilitary / Border Security Forces, Defense Research Organizations, Private Defense Contractors |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation, Raytheon Technologies Corporation, BAE Systems plc, Northrop Grumman Corporation, General Dynamics Corporation, Thales Group, MBDA Missile Systems, Rheinmetall AG, Saab AB, Rafael Advanced Defense Systems Ltd., L3Harris Technologies, Inc., Kongsberg Gruppen ASA, Elbit Systems Ltd., Israel Aerospace Industries Ltd., Textron Inc., The Boeing Company (Defense, Space & Security), Hanwha Aerospace Co. Ltd., Diehl Defence GmbH & Co. KG, Poongsan Corporation |

Frequently Asked Questions

North America dominated the Land Based Smart Weapons Market in 2025.

Offensive Operations dominated the Land Based Smart Weapons Market.

Increasing defense modernization programs and rising demand for precision-guided, AI-enabled weapon systems are driving market growth.

The Land Based Smart Weapons Market was valued at USD 6.61 billion in 2025.

The Land Based Smart Weapons Market is expected to grow at a CAGR of 8.11% from 2026 to 2035.

Get in Touch