Additive Manufacturing in Defense Market Report Scope & Overview:

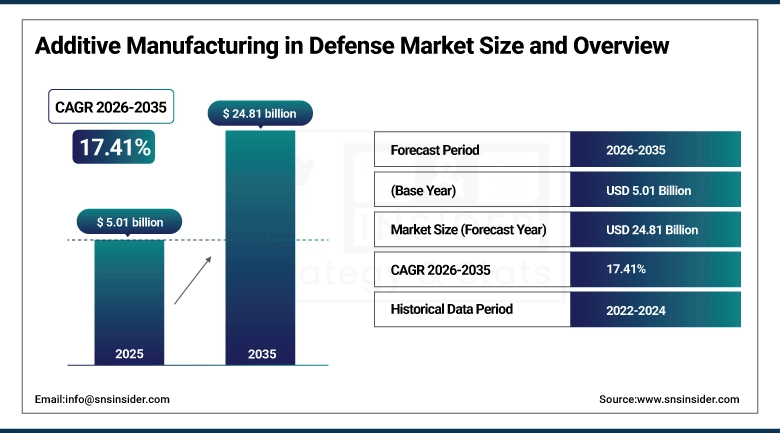

The Additive Manufacturing in Defense Market size was valued at USD 5.01 Billion in 2025 and is projected to reach USD 24.81 Billion by 2035, growing at a CAGR of 17.41% during 2026–2035.

The Additive Manufacturing in Defense Market is witnessing growth due to increased demand for lightweight yet high-strength components, rapid prototyping capabilities, and cost-effective manufacturing processes. Increasing defense modernization programs, the need for complex and customized components, reduced lead times, and advancements in 3D printing technologies are also contributing to market growth.

Additive Manufacturing in Defense Market Size and Forecast:

-

Market Size in 2025: USD 5.01 Billion

-

Market Size by 2035: USD 24.81 Billion

-

CAGR: 17.41% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Additive Manufacturing in Defense Market - Request Free Sample Report

Additive Manufacturing in Defense Market Highlights:

-

Defense logistics is the primary economic driver of AM adoption: on-demand printing of qualified replacement parts at forward locations reduces the inventory carrying cost, lead time, and supply chain vulnerability of long-tail spare parts programs that are major cost centers in every military’s sustainment budget.

-

Powder bed fusion is the dominant technology because its ability to produce dense, high-strength metal parts from titanium and nickel superalloys makes it the primary process for load-bearing aerospace and propulsion components where mechanical performance requirements are strictest.

-

Metals and alloys account for nearly half the market by material value because the most cost-justified defense AM applications are metal replacement parts for aircraft, ground vehicles, and ships where the alternative is expensive tooled machining or long-lead casting procurement.

-

Aircraft and aerospace components are the dominant application category because aerospace certifications have been the focus of the defense AM qualification effort since its inception, and the F-35 program’s adoption of additively manufactured components validated the technology’s readiness for flight-critical applications.

-

Asia Pacific is the fastest-growing regional market, driven by China’s strategic defense AM investment, Japan and South Korea’s F-35-related production and sustainment requirements, and India’s defense indigenization programs.

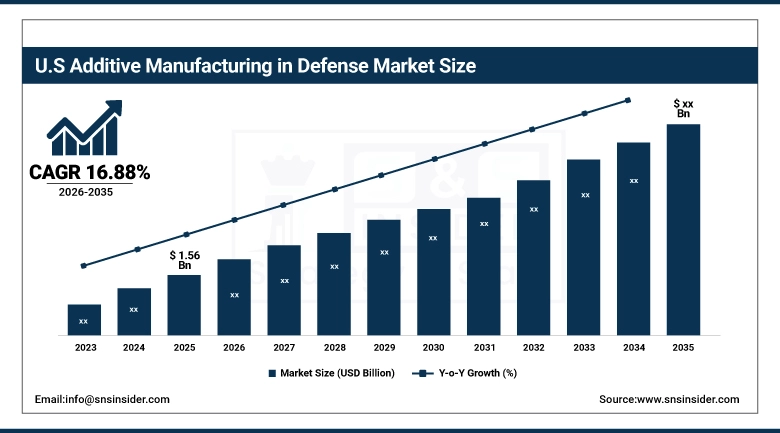

The U.S. Additive Manufacturing in Defense Market was valued at USD 1.56 Billion in 2025, growing at a CAGR of 16.88% through 2035. The United States leads through the scale of DoD-funded development programs, the depth of defense prime contractor AM capability, and active part qualification programs across the Air Force, Navy, and Army certifying additively manufactured components for operational use.

Additive Manufacturing in Defense Market Drivers:

-

Defense 3D Printing Booms Lightweight Components, Rapid Prototyping, and Modernization Drive Market Growth

The major factor contributing to the growth of the market is the increased demand from the defense industry, which is looking for lightweight, high-performance components, as well as prototyping. The growing demand for defense modernization programs across the world will drive the demand for 3D printing, as it allows for complex geometries, reduced material waste, and increased production rates. The increased demand for spare parts, maintenance, repair, and overhaul will also drive the growth of the market. The advancements made in powder bed fusion, directed energy deposition, and composites will improve manufacturing efficiency. The strategic initiatives of defense original equipment manufacturers and governments investing in advanced manufacturing technologies will drive the growth of the market.

In 2025, the U.S. Department of Defense budget request allocated about USD 3.3 billion to additive manufacturing programs up from approximately $1.8 billion the prior year, highlighting increasing public investment in AM technologies for defense applications

Additive Manufacturing in Defense Market Restraints:

-

Defense 3D Printing Faces Challenges: High Costs, Skilled Labor Shortages, and Material Limitations

The Additive Manufacturing in Defense industry is being held back by the high cost of equipment and materials, which is acting as a barrier to the widespread adoption of this technology. The lack of skilled personnel to operate this technology is another factor contributing to the delay in the adoption of this technology. The limitations in the materials being used, such as the strength and durability of the materials, are acting as barriers to the use of this technology in some applications.

Additive Manufacturing in Defense Market Opportunities:

-

Defense 3D Printing Expands Opportunities: On-Demand Parts, Advanced Materials, and Strategic Manufacturing Innovations

The Additive Manufacturing in Defense market provides opportunities in on-demand production of spares, which can help in reducing supply chain dependencies. The use of advanced materials can result in lightweight and high-strength parts, which can be used in aircraft, naval, and land applications. Expanding the use of Additive Manufacturing in MRO applications can also provide opportunities. The partnerships between defense OEMs, governments, and technology companies can drive innovation, which can result in cost-effective and rapid prototyping capabilities for future defense programs.

In August 2025, 3D Systems received a USD 7.65 million U.S. Air Force contract to develop a large‑format metal 3D printing system for high‑speed flight applications, showing direct military investment in AM capabilities

Additive Manufacturing in Defense Market Segment Highlights:

-

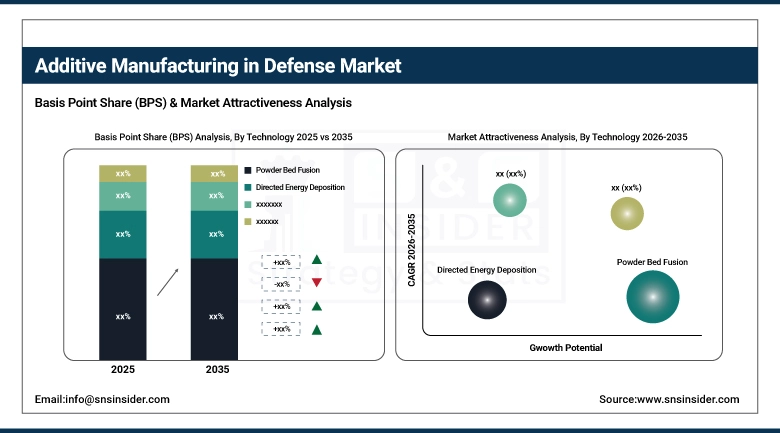

By Technology: Dominant – Powder Bed Fusion (34.72% in 2025, CAGR 16.76%); Fastest-Growing – Binder Jetting (CAGR 18.14%)

-

By Material Type: Dominant – Metals & Alloys (48.36% in 2025, CAGR 17.01%); Fastest-Growing – Composites (CAGR 18.17%)

-

By Component Type: Dominant – Aircraft & Aerospace Components (36.48% in 2025, CAGR 16.84%); Fastest-Growing – Weaponry & Ammunition (CAGR 18.29%)

-

By End-User / Defense Segment: Dominant – Air Force & Aerospace Divisions (37.25% in 2025, CAGR 16.95%); Fastest-Growing – Defense Research & Development Organizations (CAGR 18.07%)

Additive Manufacturing in Defense Market Segment Analysis:

Powder Bed Fusion Leads Technologies; Binder Jetting Drives Fastest Growth

Powder bed fusion leads because its metal printing capability selective laser melting and electron beam melting of titanium, Inconel, and stainless steel delivers the mechanical properties required for load-bearing structural and propulsion components. Binder jetting is growing fastest because advances in sintering process control have improved binder-jetted metal part density to the point where they are competitive for many non-critical structural applications at significantly higher throughput and lower cost per part, making them attractive for the high-volume, lower-criticality parts that constitute the majority of spare parts demand by count.

Metals & Alloys Lead Materials; Composites Drive Fastest Growth

Metals lead because replacing machined or cast metal defense parts is where AM investment cost justification is most straightforward. Composites are growing fastest because continuous fiber composite printing can produce structural parts with strength-to-weight ratios competing with machined aluminum at reduced weight, and the aerospace defense sector’s constant attention to weight reduction is driving qualification programs for printed composite structural components.

Aircraft & Aerospace Leads Component Types; Weaponry & Ammunition Drives Fastest Growth

Aerospace leads through the longest qualification history, highest value per qualified part, and most acute obsolescence problem in the global defense fleet. Weaponry and ammunition is growing fastest because AM’s ability to produce customized tooling, training rounds, inert practice munitions, and test fixtures without conventional lead times is increasingly used in both development and sustainment programs, and its faster CAGR reflects an earlier adoption stage relative to the mature aerospace segment.

Air Force & Aerospace Divisions Lead End-Users; Defense R&D Organizations Drive Fastest Growth

Air Force and aerospace divisions lead as the primary institutional home of both the most technically advanced AM qualification programs and the largest volume of flight hardware requiring AM-compatible parts. Defense R&D organizations are growing fastest because additive manufacturing has become a standard rapid prototyping tool across defense research agencies from DARPA to DSTL, and R&D-phase AM volume is increasing as the technology’s accessibility and material range expand.

Additive Manufacturing in Defense Market Regional Analysis:

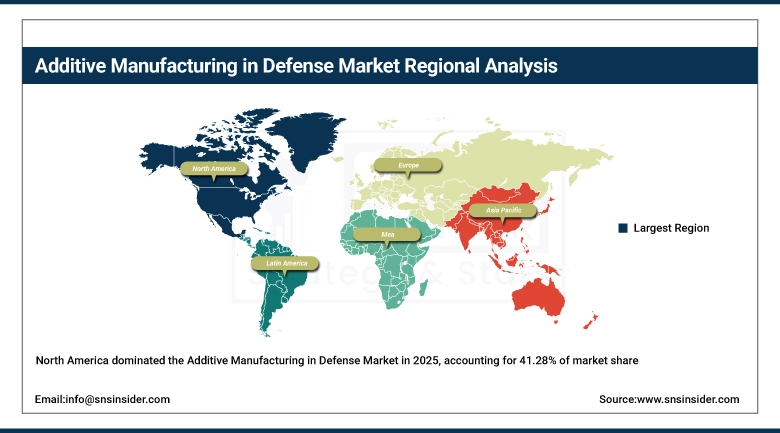

North America Additive Manufacturing in Defense Market Insights

North America dominated in 2025 at USD 2.07 Billion (41.28%), projected to reach USD 9.87 Billion by 2035 at a CAGR of 16.97%. The region’s leadership is built on the depth of U.S. DoD-funded AM development programs, operational AM deployment across Air Force, Navy, and Army sustainment, and the defense prime contractor ecosystem Boeing, Lockheed Martin, GE Aerospace, Raytheon that simultaneously develops and consumes military-grade AM technology across multiple platform programs.

Get Customized Report as per Your Business Requirement - Enquiry Now

United States Additive Manufacturing in Defense Market Insights

The United States leads North American defense AM demand through the DoD Additive Manufacturing Strategy implementation, the Air Force Rapid Sustainment Office qualifying hundreds of parts for operational use, and the world’s largest defense aerospace industrial base integrating AM across aircraft, missile, and ground system production programs.

Europe Additive Manufacturing in Defense Market Insights

Europe held a 24.57% share in 2025 at USD 1.23 Billion, growing to USD 5.92 Billion by 2035 at a CAGR of 17.06%. Post-2022 defense spending increases are accelerating European defense AM investment. France’s DGA, the UK’s Defence Equipment and Support, and Germany’s Bundeswehr all operate active AM qualification programs, with Airbus Defence and Space and Dassault Aviation integrating additive manufacturing into A400M, Eurofighter, and Rafale production and sustainment.

United Kingdom Additive Manufacturing in Defense Market Insights

The United Kingdom leads European defense AM through DE&S Digital Depot programs qualifying printed spare parts for Army and RAF platforms, DSTL-funded naval AM research, and Rolls-Royce integration of additive manufacturing into combat aircraft engine production and overhaul programs.

Asia Pacific Additive Manufacturing in Defense Market Insights

Asia Pacific is expected to grow at the fastest regional CAGR of approximately 18.58%, rising from USD 1.12 Billion in 2025 to USD 6.13 Billion by 2035. China’s large-scale AM investment for aerospace and naval programs is the dominant driver, alongside Japan’s adoption for JMSDF and JASDF sustainment, South Korea’s integration into domestic fighter and naval programs, and India’s DRDO and HAL programs using AM for indigenous defense hardware development.

China Additive Manufacturing in Defense Market Insights

China leads Asia Pacific defense AM through PLA strategic prioritization of additive manufacturing for aerospace and naval production, large titanium AM capacity built specifically for military aerospace applications, and state-funded research developing defense-specific AM materials and processes at a scale comparable to U.S. DoD investment.

Latin America and Middle East & Africa Additive Manufacturing in Defense Market Insights

Latin America held a 6.34% share in 2025 at USD 317 Million, growing at 17.72% CAGR to USD 1.62 Billion by 2035. Brazil leads through Embraer Defense AM adoption and Brazilian Air Force integration of printed components in F-39 Gripen sustainment planning. Middle East & Africa held a 5.42% share at USD 271 Million, growing at 16.84% CAGR to USD 1.28 Billion by 2035. Israel leads MEA through IAI and Rafael AM integration in missile and drone system production. Israel leads MEA defense AM through IAI and Rafael Advanced Defense Systems’ integration of additive manufacturing into missile, UAS, and precision munition production, supported by a domestic aerospace manufacturing ecosystem that has adopted AM for both production efficiency and rapid development cycle reduction.

Additive Manufacturing in Defense Market Competitive Landscape:

Boeing

Boeing is one of the largest consumers and developers of defense additive manufacturing, integrating printed components across its F/A-18 Super Hornet, Apache helicopter, P-8 Poseidon, and B-21 Raider programs. Boeing Defense, Space & Security operates an internal AM center qualifying part for both new production and sustainment programs, with investment spanning powder bed fusion, directed energy deposition, and large-format polymer printing reflecting the range of applications its defense portfolio requires.

In February 2025, Boeing qualified over 600 additively manufactured parts for the CH-47F Chinook under its Block II upgrade program the largest single-platform AM qualification milestone in the company’s history covering structural fittings, ducting, and mounting hardware in aluminum and titanium alloys, with the program expected to reduce Chinook sustainment costs by approximately 15% for the qualified part population.

GE Aerospace

GE Aerospace is the technology leader in defense AM for propulsion applications, having achieved the first FAA-certified additively manufactured jet engine component with the LEAP fuel nozzle in 2015 and subsequently qualifying AM components in military programs including the T901, F414, and related engine programs. Its Avio Aero subsidiary is a primary site for turbine component AM development, and the GE Additive Technology Center in Cincinnati operates as both internal production resource and development partner for military engine qualification programs.

In April 2025, GE Aerospace received a U.S. Air Force contract to develop and qualify additively manufactured turbine blade components for the F110 engine powering the F-16 fleet, addressing a supply chain vulnerability created by declining conventional casting supplier capacity. Initial qualification testing was expected to complete by late 2026.

Additive Manufacturing in Defense Market Key Players:

-

3D Systems

-

Stratasys

-

EOS

-

ExOne

-

GE Additive

-

Materialise

-

SLM Solutions

-

Renishaw

-

Höganäs

-

Arcam

-

Markforged

-

Desktop Metal

-

Optomec

-

Voxeljet

-

HP

-

Trumpf

-

Raytheon Technologies

-

Boeing

-

Airbus

-

Lockheed Martin

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.01 Billion |

| Market Size by 2035 | USD 24.81 Million |

| CAGR | CAGR of 17.41% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Powder Bed Fusion, Directed Energy Deposition, Material Extrusion, Binder Jetting, Vat Photopolymerization, and Sheet Lamination) • By Material Type (Metals & Alloys, Polymers & Plastics, Composites, and Ceramics) • By Component Type (Aircraft & Aerospace Components, Ground Vehicle Systems, Naval Systems, Weaponry & Ammunition, and Maintenance, Repair & Overhaul (MRO)) • By End-User / Defense Segment (Air Force & Aerospace Divisions, Army & Ground Forces, Navy & Marine Corps, Defense Research & Development Organizations, and Defense OEMs) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3D Systems, Stratasys, EOS, ExOne, GE Additive, Materialise, SLM Solutions, Renishaw, Höganäs, Arcam, Markforged, Desktop Metal, Optomec, Voxeljet, HP, Trumpf, Raytheon Technologies, Boeing, Airbus, Lockheed Martin. |

Frequently Asked Questions

North America dominated the Additive Manufacturing in Defense in 2025

Powder Bed Fusion dominated the Additive Manufacturing in Defense in 2025.

Rising defense modernization, demand for lightweight high-performance components, rapid prototyping, and MRO applications drive the market.

The Additive Manufacturing in Defense size was USD 5.01 Billion in 2025 and is expected to reach USD 24.81 Billion by 2035.

The Additive Manufacturing in Defense is expected to grow at a CAGR of 17.41% from 2026–2035.

Get in Touch