Adhesion Barrier Market Report Scope & Overview:

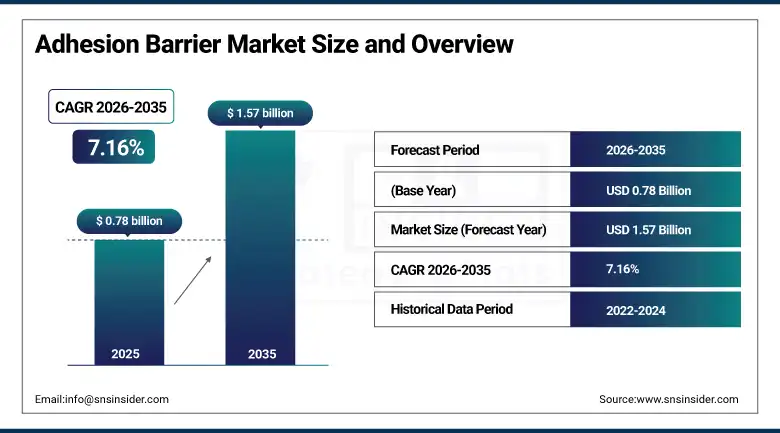

The Adhesion Barrier Market was valued at USD 0.78 Billion in 2025 and is expected to reach USD 1.57 Billion by 2035, growing at a CAGR of 7.16% from 2026–2035.

Adhesion barrier products address this clinical challenge by physically separating surgically traumatised tissue surfaces during the critical early wound healing phase when fibrinous adhesion formation occurs, providing a temporary mechanical barrier that prevents contact between surfaces until natural re-epithelialisation restores the serosal lining that physiologically prevents adhesion formation in healthy tissue. The clinical value of adhesion prevention has been demonstrated through randomised controlled trials showing significant reductions in adhesion formation scores, adhesion extent, and adhesion density at re-operation in patients receiving adhesion barrier treatment compared with untreated controls, with downstream reductions in the bowel obstruction, infertility, and chronic pain complications that adhesions cause providing the patient outcome justification that drives clinical adoption and healthcare system investment in prophylactic adhesion prevention.

The American College of Surgeons' estimation that adhesion-related hospital readmissions cost the U.S. healthcare system over USD 2 Billion annually in direct treatment costs, excluding the productivity loss and quality of life burden borne by affected patients, establishes a compelling health economic framework for adhesion barrier prophylaxis investment that payers and hospital procurement committees are increasingly incorporating into product value assessment.

Market Size and Forecast

-

Market Size in 2026E: USD 0.84 Billion

-

Market Size by 2035: USD 1.57 Billion

-

CAGR: 7.16% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Adhesion Barrier Market - Request Free Sample Report

Adhesion Barrier Market Trends

-

Growing development of next-generation bioresorbable adhesion barrier formulations with optimised resorption timelines matched to the specific adhesion formation windows of different surgical procedure types, addressing the limitation of existing products whose uniform resorption profiles may not align with the variable healing kinetics of different tissue types and surgical contexts.

-

Rising adoption of sprayable adhesion barrier formulations that can be applied laparoscopically to anatomically complex or difficult-to-access surgical sites where film and mesh-based products are impractical to position accurately, expanding the addressable surgical procedure range for adhesion prevention from open surgery contexts toward the rapidly growing minimally invasive surgical volume.

-

Increasing clinical evidence generation for adhesion barriers in cardiac surgery applications, where re-operative cardiac procedures including valve replacement, coronary artery bypass revision, and heart failure device implantation are complicated by dense pericardial adhesions from previous sternotomy that significantly increase the risk and duration of re-operative procedures, creating compelling clinical demand for prophylactic adhesion prevention at primary cardiac surgery.

-

Growing interest from gynaecological surgery in adhesion barriers addressing post-myomectomy and post-endometriosis surgery adhesion formation that contributes to female infertility, as the reproductive medicine community's focus on fertility preservation outcomes following uterine surgery is creating a premium-price demand segment for proven adhesion prevention in patients where fertility outcomes are the primary surgical success criterion.

-

Expanding regulatory approvals for adhesion barrier products in emerging market healthcare systems including China, India, Brazil, and South Korea, where growing surgical volumes and improving hospital procurement capabilities are creating commercial market conditions in geographies that were previously limited by regulatory pathway completion and reimbursement framework development.

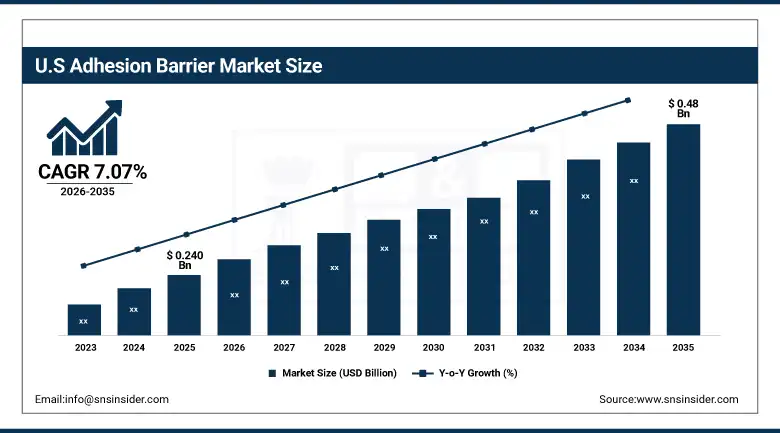

U.S. Adhesion Barrier Market Outlook

The U.S. Adhesion Barrier Market was valued at approximately USD 0.240 Billion in 2025 and is expected to reach approximately USD 0.48 Billion by 2035, growing at a CAGR of 7.07%, supported by sophisticated healthcare infrastructure, well-established reimbursement frameworks covering adhesion barrier use in approved surgical indications, the pervasive integration of minimally invasive surgical techniques that create new product development requirements and market opportunities, and strong clinical awareness of adhesion-related complications among U.S. surgeons across relevant specialties.

The United States is the world's largest and most commercially developed adhesion barrier market, where the FDA's regulatory approval framework for medical devices has validated the safety and effectiveness of leading adhesion barrier products including Gynesonics' Seprafilm hyaluronate-carboxymethylcellulose bioresorbable membrane and Lifecore Biomedical's Gynecare Interceed oxidised regenerated cellulose product for specific gynaecological and abdominal surgical indications, providing the regulatory foundation that supports commercial product adoption and healthcare system procurement. The U.S. healthcare system's progressive adoption of episode-based payment models and hospital readmission penalty programmes under the Affordable Care Act's Hospital Readmissions Reduction Programme creates financial incentives for hospitals to invest in prophylactic adhesion prevention that reduces the readmission rates for bowel obstruction and re-operation that impose both direct treatment costs and CMS reimbursement penalties. Leading U.S. adhesion barrier market participants including Ethicon (Johnson & Johnson), BD, and Baxter International maintain strong market positions through product portfolio breadth, established hospital relationships, and sustained clinical education investment that maintains surgeon awareness of adhesion barrier options across general surgery, gynaecology, and cardiac surgery specialties.

The FDA's support for clinical research in adhesion prevention through its Breakthrough Device Designation programme for novel adhesion barrier technologies addressing unmet clinical needs in procedures where existing products have not demonstrated adequate efficacy is accelerating the clinical development pipeline for next-generation adhesion prevention technologies that could significantly expand the addressable market beyond current product categories.

Adhesion Barrier Market Segment Analysis

-

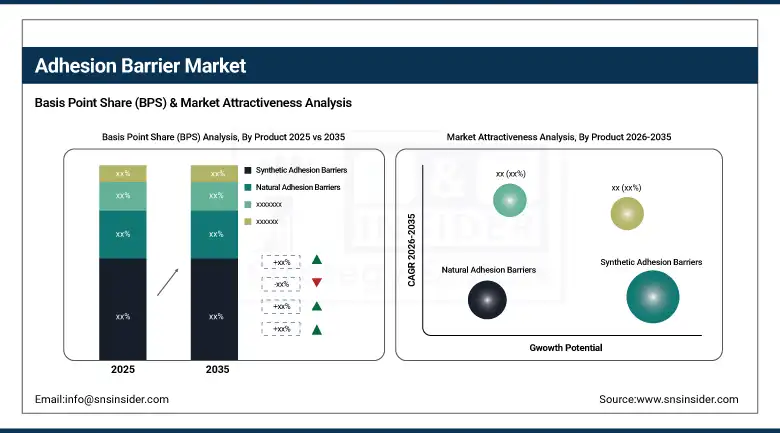

By Product, Synthetic adhesion barriers dominated with approximately 78.22% of revenues in 2025 through superior biocompatibility, predictable resorption characteristics, and consistent manufacturing quality; Natural adhesion barriers are the fastest-growing segment at a CAGR of 7.57% as demand grows for biocompatible, fully biodegradable materials derived from biological sources that align with the medical community's increasing preference for materials with established physiological compatibility profiles.

-

By Application, Cardiovascular surgeries held approximately 40.86% of revenues in 2025 as high-risk procedures with significant re-operative adhesion complication rates create compelling clinical demand; Gynaecological surgeries are the fastest-growing application at a CAGR of 7.79% driven by increasing minimally invasive gynaecological procedure volumes and the reproductive medicine community's prioritisation of adhesion prevention in fertility-preserving surgical approaches.

-

By Formulation, Film/Mesh formulations led with approximately 50.84% of revenues in 2025 through ease of application in open surgical contexts, established clinical efficacy evidence, and compatibility with a wide range of surgical procedures; Gel formulations are the fastest-growing at a CAGR of 8.22% as their applicability to minimally invasive and laparoscopic procedures through narrow cannula delivery enables adhesion prevention in procedure categories where film products are impractical to deploy.

-

By End-User, Hospitals dominated with approximately 72.86% in 2025 as the primary site for the complex surgical procedures where adhesion barrier use is clinically indicated; Ambulatory Surgery Centers are the fastest-growing end-user segment at a CAGR of 7.58% as the migration of gynaecological and abdominal procedures to outpatient settings expands the commercial setting where adhesion barrier products are purchased and used.

By Product, Synthetic dominates, Natural is expected to grow fastest

Synthetic adhesion barriers retained the dominant product position with approximately 78.22% of Adhesion Barrier Market revenues in 2025, reflecting the established clinical evidence base and commercial market development that synthetic barrier materials including hyaluronate-carboxymethylcellulose, polyethylene glycol hydrogels, expanded polytetrafluoroethylene membranes, and oxidised regenerated cellulose have accumulated across decades of clinical investigation and commercial deployment. The biocompatibility advantages of advanced synthetic polymer chemistry, where material properties including resorption timeline, mechanical flexibility, tissue adhesion characteristics, and inflammatory response profile can be precisely engineered to match specific surgical application requirements, have enabled the development of adhesion barrier products with predictable and reproducible clinical performance that is essential for surgical product regulatory approval and clinical adoption. Polyethylene glycol-based hydrogel barrier systems that cross-link in situ upon application to surgical surfaces, conforming to complex anatomical geometries and providing a continuous liquid-to-gel adhesion barrier without the positioning and fixation challenges of pre-formed films, represent the synthetic category's current technological frontier.

Natural adhesion barriers derived from biological sources including hyaluronic acid, collagen, cellulose, and fibrin are the fastest-growing product segment at a CAGR of 7.57% through 2035, as the increasing clinical and regulatory emphasis on biocompatibility, biodegradability, and the avoidance of synthetic polymer residues in implanted medical products is creating market preference for materials whose physiological integration pathways are well characterised through the extensive clinical experience with hyaluronic acid and collagen-based medical products in orthopaedics, wound care, and drug delivery. The fertility medicine community's particular preference for hyaluronic acid-based adhesion prevention products in gynaecological surgery, where concerns about residual synthetic material effects on pelvic tissue and reproductive outcomes favour naturally derived formulations with demonstrated safety in female reproductive tract applications, is creating a specialty demand segment that supports premium pricing for clinically validated natural adhesion barrier products.

By Application, Cardiovascular dominates, Gynaecological is expected to grow fastest

Cardiovascular surgeries retained the largest application position with approximately 40.86% of Adhesion Barrier Market revenues in 2025, reflecting the particular clinical severity of pericardial adhesion formation following cardiac surgery procedures that make re-operative cardiac procedures substantially more dangerous and technically demanding than primary operations on adhesion-free tissue. The adhesion of the heart and great vessels to the sternum and pericardium following median sternotomy creates a dissection challenge at re-operation where blunt or sharp dissection to separate densely adherent structures carries risk of haemorrhage, cardiac laceration, and air embolism that significantly increases the morbidity of repeat cardiac procedures and motivates surgeon adoption of prophylactic adhesion barriers at primary cardiac surgery as a risk mitigation measure for the re-operative scenario that may occur years later.

Gynaecological surgeries are the fastest-growing application at a CAGR of 7.79% through 2035, driven by the combination of rapidly growing minimally invasive gynaecological procedure volumes including laparoscopic myomectomy, hysteroscopic uterine septum resection, and laparoscopic endometriosis excision where adhesion formation following surgery can directly impair the fertility outcomes that are the primary clinical objective of fertility-preserving procedures, and growing reproductive medicine and gynaecological surgery specialist awareness of adhesion barriers as evidence-based fertility-preserving tools for women undergoing uterine or pelvic surgical interventions. The clinical imprimatur provided by professional society guidelines from the American Society for Reproductive Medicine and the European Society of Human Reproduction and Embryology recommending adhesion prevention consideration in specific gynaecological surgical contexts is translating research evidence into clinical practice adoption at increasing rates across the gynaecological surgery specialty.

Regional Insights:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.5% |

|

Europe |

Germany |

26.4% |

|

Asia Pacific |

China |

40.7% |

|

Middle East & Africa |

Saudi Arabia |

29.8% |

|

Latin America |

Brazil |

44.1% |

North America Adhesion Barrier Market Insights

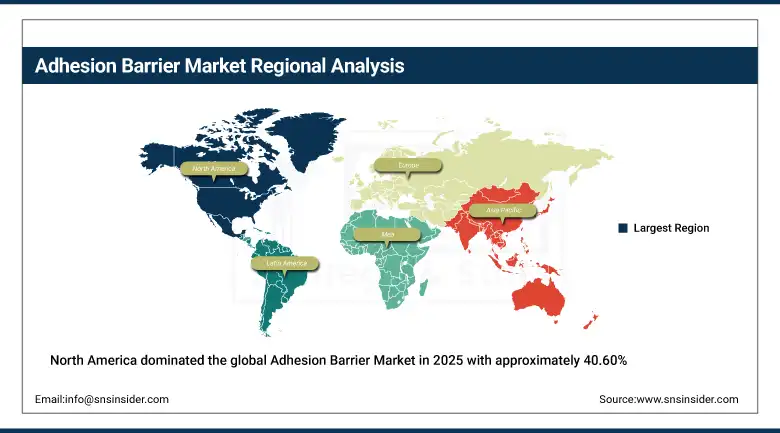

North America dominated the global Adhesion Barrier Market in 2025 with approximately 40.60% of revenues, with the United States accounting for approximately 83.5% of North American revenues as the world's largest single market for adhesion barrier products. The region's market leadership reflects its combination of the highest volume surgical procedure rates among major economies, the most mature commercial development of adhesion barrier products with multiple FDA-approved options across several surgical indications, established hospital procurement of adhesion prevention products as standard surgical supply for relevant procedure categories, and the healthcare system's financial incentives for complication prevention that support adhesion barrier investment. The presence of leading product manufacturers including Ethicon, BD, Baxter, and Integra LifeSciences headquartered or principally operating in North America sustains clinical education investment and commercial infrastructure that maintain surgeon awareness and product availability across the full range of relevant surgical specialties.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Adhesion Barrier Market Insights

Europe is a technically sophisticated adhesion barrier market characterised by national health technology assessment processes that evaluate adhesion barrier products for reimbursement eligibility based on clinical evidence of efficacy and cost-effectiveness relative to the complications they prevent. Germany accounts for approximately 26.4% of European revenues as the region's largest national market, driven by a high-volume surgical system with strong specialist surgical training culture and adoption of evidence-based medical device use, supported by GKV statutory health insurance coverage for medically indicated adhesion barrier use in approved surgical contexts. The United Kingdom, France, Italy, and the Netherlands represent significant additional European markets where national formulary inclusion processes and health technology assessment endorsements shape hospital procurement decisions for adhesion barrier products differently from the U.S. market's more direct commercial adoption pathway.

Asia Pacific Adhesion Barrier Market Insights

Asia Pacific is the fastest-growing regional adhesion barrier market with a CAGR of 7.91% through 2035, driven by rapidly expanding surgical volumes across the region's major healthcare systems as population ageing, rising chronic disease prevalence, and improving healthcare access collectively increase the rate of abdominal, cardiac, and gynaecological procedures that generate adhesion prevention requirements. China accounts for approximately 40.7% of Asia Pacific revenues, reflecting the country's extraordinary surgical volume growth as its hospital system has expanded dramatically to serve an ageing population with rising rates of cardiovascular disease, cancer requiring surgical treatment, and gynaecological conditions addressed through surgical intervention. The progressive commercialisation of adhesion barrier products through China's NMPA regulatory approval process and the development of domestic manufacturing capability by Chinese medical device companies are expanding market access at price points competitive with imported products.

MEA & Latin America Adhesion Barrier Market Insights

The Middle East and Africa and Latin America represent developing adhesion barrier markets where increasing surgical capability, growing surgeon awareness of adhesion complications and prevention options, and improving healthcare procurement processes are creating market development conditions that support progressive commercial expansion from a current low penetration base. Saudi Arabia leads MEA adhesion barrier adoption at approximately 29.8% of regional revenues through its high-volume public and private hospital sector, strong purchasing power supported by oil revenue healthcare investment, and active clinical education programmes by international medical device companies seeking to establish early clinical relationships with the specialist surgical community. Brazil accounts for approximately 44.1% of Latin American revenues, driven by the country's large hospital sector encompassing both a substantial public SUS system and a significant private healthcare market with procurement practices for innovative surgical products that are more comparable to developed market clinical adoption patterns than other Latin American healthcare systems.

Market Dynamics

Growth Drivers: Rising global surgical procedure volumes generating adhesion prevention requirements combined with expanding clinical evidence base establishing adhesion barriers as standard of care in high-risk surgical contexts

The primary structural growth driver for the Adhesion Barrier Market is the sustained global increase in the surgical procedure volumes that generate adhesion formation risk, driven by the simultaneous pressures of population ageing expanding the patient pool with age-related cardiovascular, musculoskeletal, and gastrointestinal conditions requiring surgical treatment, cancer incidence rising with demographic ageing and environmental exposure creating surgical oncology caseloads, and the progressive improvement in healthcare access across developing economies enabling surgical care for patient populations previously lacking access to elective and semi-urgent procedures. The growing proportion of minimally invasive procedures in total surgical volume, while introducing procedural technical differences that challenge conventional adhesion barrier application methods, simultaneously increases the clinical relevance of adhesion prevention as patients undergoing laparoscopic abdominal and pelvic surgery typically experience faster recovery but retain the full adhesion formation risk of open procedures at the sites of tissue manipulation and energy-based dissection.

Restraints: Reimbursement limitations constraining adhesion barrier use to specific high-risk surgical indications in cost-constrained healthcare systems, clinical evidence gaps for newer formulations limiting formulary access, and limited surgeon awareness in developing markets

A significant restraint on the Adhesion Barrier Market is the reimbursement environment in national health systems across Europe, Asia Pacific, and Latin America where health technology assessment bodies apply strict cost-effectiveness criteria to adhesion barrier products that in many cases result in restricted formulary coverage limited to the highest-risk surgical contexts, excluding the broader preventive use in moderate-risk procedures where clinical benefit exists but the cost-per-quality-adjusted-life-year calculation does not meet the reimbursement threshold at current product prices. The clinical evidence base for adhesion barriers, while substantial in certain specific indications particularly around abdominal and gynaecological surgery, contains gaps in long-term follow-up data, head-to-head comparisons between products, and evidence for newer formulation types that create challenges for formulary applications requiring Level 1 evidence across the full range of claimed clinical benefits.

Opportunities: Novel material science formulations enabling laparoscopic application expanding the minimally invasive surgery adhesion prevention market, value-based healthcare frameworks creating reimbursement pathways for cost-effective adhesion prevention, and AI-powered patient risk stratification enabling targeted prevention deployment

The development of adhesion barrier formulations specifically engineered for laparoscopic and robotic surgical application through standard endoscopic ports, including self-deploying films that can be introduced through narrow cannulae and expand to cover target tissue areas under laparoscopic visualisation, injectable hydrogels that conform to complex anatomical geometries without requiring direct manipulation, and sprayable aerosol formulations that provide uniform coverage of large surgical fields through a laparoscopic spray catheter, represents the most commercially significant product innovation opportunity in the adhesion barrier market as it unlocks the large and rapidly growing minimally invasive abdominal surgery volume that existing products cannot efficiently address. AI-powered surgical risk stratification tools that identify patients at highest adhesion formation and complication risk based on procedure type, prior surgical history, anatomical characteristics, and comorbidity profile could enable targeted adhesion barrier deployment in highest-risk cases with the strongest cost-effectiveness evidence, supporting both broader clinical adoption and more defensible reimbursement applications.

Recent Developments:

-

June 2024: Baxter International's PEG-based hydrogel adhesion barrier demonstrated in clinical evaluation that it significantly reduced re-operation rates in cardiovascular surgery cases compared with untreated controls, providing high-quality clinical evidence for a surgical context where the adhesion barrier market has historically lacked robust randomised controlled trial data.

-

2025: Ethicon (Johnson & Johnson) continued clinical development of its next-generation sprayable adhesion barrier formulation designed for laparoscopic gynaecological surgery applications, addressing the applicability gap that has limited adhesion prevention uptake in the rapidly growing minimally invasive gynaecological procedure category.

-

2025: Anika Therapeutics expanded its hyaluronate-based bioresorbable product portfolio with a new formulation optimised for orthopaedic surgical applications, entering a procedure category where tendon and joint surgery adhesion complications create clinical demand not fully addressed by existing products designed primarily for abdominal and pelvic surgical contexts.

-

2025: Integra LifeSciences invested in expanded manufacturing capacity for its adhesion barrier product lines, reflecting anticipated growth in clinical adoption across abdominal and cardiovascular surgical indications driven by increasing surgeon education and awareness programmes conducted through surgical society partnerships.

-

2024: CryoLife advanced clinical investigation of its next-generation cardiac adhesion prevention system designed to address pericardial adhesion formation following cardiac surgery, targeting the specific re-operative cardiac procedure risk context where the clinical and economic case for prophylactic adhesion prevention is particularly compelling.

Adhesion Barrier Market Key Players

-

Becton, Dickinson and Company

-

Ethicon (Johnson & Johnson)

-

Baxter International Inc.

-

FzioMed Inc.

-

Molnlycke Health Care

-

Confluent Surgical

-

CryoLife, Inc.

-

Integra LifeSciences

-

Terumo Corporation

-

Cohera Medical, Inc.

-

Medtronic plc

-

Adhezion Biomedical

-

BioHorizons, Inc.

-

Anika Therapeutics, Inc.

-

Cousins Medical

-

GlucoSite Medical

-

Axia Medical

-

Hemoshear Technologies

-

Polyganics BV

-

SurgiQuest

Adhesion Barrier Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.78 Billion |

| Market Size by 2035 | USD 1.57 Billion |

| CAGR | CAGR of 7.16% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Synthetic Adhesion Barriers, Natural Adhesion Barriers) • By Application (Cardiovascular Surgeries, Abdominal & General Surgeries, Gynecological Surgeries, Orthopedic Surgeries, Neurological Surgeries, Others) • By Formulation (Film/Mesh, Gel, Liquid, Others) • By End-User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Becton, Dickinson and Company, Ethicon (Johnson & Johnson), Baxter International Inc., FzioMed Inc., Molnlycke Health Care, Confluent Surgical, CryoLife, Inc., Integra LifeSciences, Terumo Corporation, Cohera Medical, Inc., Medtronic plc, Adhezion Biomedical, BioHorizons, Inc., Anika Therapeutics, Inc., Cousins Medical, GlucoSite Medical, Axia Medical, Hemoshear Technologies, Polyganics BV, SurgiQuest |

Frequently Asked Questions

North America dominated with approximately 40.60% of revenues in 2025.

Ans: Synthetic adhesion barriers dominated with approximately 78.22% of revenues in 2025.

Ans: Rising global surgical procedure volumes generating adhesion formation requirements combined with expanding clinical evidence establishing adhesion barriers as a cost-effective prevention tool for bowel obstruction, infertility, and re-operative complication risks associated with post-surgical adhesion formation.

Ans: The Adhesion Barrier Market was valued at USD 0.785 billion in 2025.

Ans: The Adhesion Barrier Market is expected to grow at a CAGR of 7.16% from 2026 to 2035.

Get in Touch