ADVANCED GLASS MARKET REPORT SCOPE & OVERVIEW:

Get more information on Advanced Glass Market - Request Sample Report

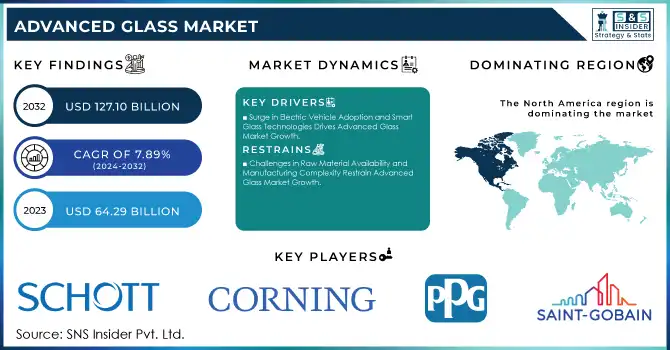

The Advanced Glass Market was valued at USD 64.29 Billion in 2023 and is expected to reach USD 127.10 Billion by 2032, growing at a CAGR of 7.89% over the forecast period 2024-2032.

The Advanced Glass Market has high potential with the growing application of Advanced glass in construction, automotive, electronics, as well as aerospace. With the high demand for energy-efficient and high-performance materials, advanced glass technologies are becoming crucial in providing such needs. Tempered and laminated glass is commonly used in buildings and automobiles because it is less likely to break and is more resilient. Driven by a trend towards sustainable building practices in the construction property, advanced glass solutions such as energy-efficient windows and solar control glass are increasingly becoming popular. Advanced glass plays an important role in automobiles as it reduces the overall weight, improves safety, and enhances the aesthetic of the vehicle which is expected to fuel the demand for advanced glass in automotive which in turn is driving the growth of the market. Energy-efficient glass used in construction is leading to 25-30% energy savings in commercial buildings. Advanced glass in the automotive sector, for instance, lighter laminated glass reduces the weight of the vehicle to 10-20% Functions by increasing the fuel efficiency of vehicles and mileage by 3-5%. Moreover, OLED display technology is also predicted to have a 15% annual adoption of advanced glass from 2024 through 2032 as demand for higher resolution and durability in consumer electronics rises.

Moreover, the increasing technological advancements in the electronics and aerospace sectors are also driving the growth of the advanced glass market. Ceramic and specialized coatings drive the high-performance glass required for electronics, touchscreens, displays, and solar panels. It transforms the glass materials used in aerospace since lightweight and hard-wearing glass is needed for commercial aerospace to enhance the performance of aircraft and the safety of passengers. Other factors for the market growth are a rising focus on renewable energy solutions and an increasing trend for smart buildings. Aerospace components have been the familiar application of advanced glass since 2023, accounting for 9% of the annual demand. Today around 15–20% of new commercial aircraft utilize energy-efficient and thermally resistant composite glass as windows and components of airframe systems and structures. Currently, 75% of smartphones in the world are using some form of glass technology (mostly for displays and protective glass) in 2023

MARKET DYNAMICS:

KEY DRIVERS

-

Surge in Electric Vehicle Adoption and Smart Glass Technologies Drives Advanced Glass Market Growth

Growing demand for electric vehicles (EVs) and the increasing adoption of smart glass technologies are two of the most significant key drivers fuelling the growth of the Advanced Glass Market. EVs are becoming increasingly popular as the world automotive sector transitions to sustainability, making them both environmentally friendly and government-supported. This transformation is dependent on the use of advanced glass that is lighter and helps to create energy-efficient EVs that would further enhance their performance and efficiency. Advanced glass solutions, including laminated and tempered glass to minimize vehicle weight and improve energy efficiency, which is an important factor in increasing battery life and performance of the vehicle are some of them. In addition, automotive applications using heavy glass for larger windows and roofs in electric vehicles (EVs) are promoting aesthetic characteristics, enhancing cabin space, and offering better driving experiences, which, in turn, fuels market growth in the automotive sector. Almost 14 million electric cars were sold worldwide in 2023, accounting for 20% of all new car sales. Electric and hybrid vehicles represented 18.7% of total new light-duty vehicle sales in the U.S. in Q2 2024, up from 17.8% in Q1. China became a third electric in the latest figures for new car registrations in 2023, with Europe clocking more than one in five as electric and the U.S. reaching one in ten.

-

Rising Demand for Smart Glass Technologies Boosts Energy Efficiency and Green Building Adoption Worldwide

The adoption of smart glass technologies is another major factor that is driving demand, as they are finding applications in both residential and commercial buildings. Smart glass that changes transparency or color upon environmental stimuli (temperature, light, etc.) offers great energy-saving effects and improved comfort, thus, it has been attracting a lot of attention lately. The technology controls the volume of light moving in and out of a building, reducing heating and cooling costs, which makes it an appealing choice for environmentally aware consumers and businesses. Smart glass, for example, is being applied to windows, facades, and skylights to encourage the construction of more aesthetically pleasing green buildings. With the increasing need for energy-efficient buildings and smart infrastructures, smart glass technologies are projected to demonstrate strong adoption, further fuelling the advanced glass market growth. These smart glass technologies can save as much as 25% on heating and cooling costs for commercial buildings. More than 60% of new commercial buildings are implementing energy-efficient technologies such as smart glass that help meet stricter environmental standards. Smart glass can now be found in 30,000-plus buildings around the world, including, for example, the Apple Campus in Cupertino.

RESTRAIN

-

Challenges in Raw Material Availability and Manufacturing Complexity Restrain Advanced Glass Market Growth

Raw Materials Availability acts as a Restraint to Advanced Glass Market Specialized materials needed for some high-end glasses (ceramic and high-performance glass, for example) are less readily available, expanding the supply chain and slowing the production process. This can limit the growth of the market as a whole, for example, where demand exceeds the supply of these materials. Another major restraint is the complicated process of manufacturing and the requirement for specialist skills. Many advanced glass products such as glass coatings or complex lamination innate beyond the capacity of many types of machinery, and require sophisticated craft. This raises the technical threshold for newcomers and presents hurdles for makers scaling up production. Moreover, product quality and consistency are typically difficult to control across larger volumes, which can affect the performance of high-tech glass field solutions in their end-use applications.

KEY MARKET SEGMENTS:

BY PRODUCT TYPE

The market share for tempered glass held an impressive 42.2% in 2023 on account of its extensive range of applications in industries including construction, automotive, and safety. The reason behind its popularity is due to its flexible nature, strength & durability which makes it suitable for windows, facades & vehicle windshields. And, tempered glass is also known for shattering into small, harmless, or less damageable parts, so it is widely used in automotive and architecture for safety reasons. Such unique properties of tempered glass, make it a safe and strong glass, which consequently creates significant room for the market, to reach a wide range of applications in 2023.

Ceramic glass will witness a robust growth rate, registering the fastest CAGR during the year 2024-2032, as it has unique physical characteristics that make it most suitable for high-demand applications. The high thermal resistance of ceramic glass makes it a key requirement across industries where heat management is vital, especially in electronics, automotive (electric vehicles primarily), and aerospace. As these sectors continue to boom, its application in high-temperature environments is growing even faster from electric car batteries to cooktops and aerospace parts. The emergence of end-use sectors like electronics, automotive, and others where the use of advanced technologies and energy-efficient solutions are increasingly adopted is followed by trends for high-performance materials pushing the ceramic glass market growth rapidly.

BY APPLICATION

Safety & Security led the market share of advanced glass with 39.8% in 2023, owing to the vital contribution of advanced glass in protection and durability in numerous sectors, including automotive, construction, and defense. The applications for this type of glass include high-pressure tempered glass and laminated glass, which is meant to be impact-resistant and bulletproof or shatterproof for some specific areas that need to comply with safety. Safety glass prevents passengers from harming themselves in case of automobile accidents in automotive applications, in the form of windows and facades, safety glass prevents glass from breaking and provides structural integrity in the construction field. Due to increasing safety concerns in public and private spaces and the requirement of safety glass in buildings and vehicles under various regulations, this segmentation continues to hold the highest market share.

Solar Control is expected to be the fastest-growing application between 2024 and 2032, due to the growing demand for sustainable and energy-efficient solutions. Solar control glass refracts both light and heat energy and makes a big difference in enhancing the energy efficiency of buildings and vehicles. It limits the entry of solar heat and light into the building or vehicle, effectively cutting down the need for air conditioning or heating. Due to an increase in global interest in sustainability across the board, including the rise of green buildings, solar control glass is now an essential material for smart buildings as well as eco-friendly cars. It is crucial to improve occupant comfort and utilization of energy, thus, becoming a major solution to meet energy-efficiency standards and environmental regulations. Following this pattern, smart & energy-efficient technologies boost its growth therefore, solar control glass is surging and will achieve the quickest growth in the years ahead.

BY END USE

The automobiles segment accounted for the largest market share of 41.1% in 2023 owing to the growing requirement for advanced glass solutions in vehicles for safety, comfort, and aesthetics. Advanced glass types such as laminated and tempered glass, have a key role in increasing vehicle safety they prevent shattering and provide better structural support. An expansion in the adoption of features such as bigger windows, larger panoramic roofs, and lightweight materials in many of the modern vehicles only spurs the need for advanced glass. Furthermore, given the transition of the automotive industry to electric vehicles (EVs), the rising requirement for weight-saving energy-efficient glass that enhances batteries and other equipment and vehicle performance is further increasing the glass market share. This trend is anticipated to persist, which will make sure that the automotive sector continues to be a major contributor to the advanced glass market.

Construction is to witness the fastest CAGR from 2024-2032, as there is a growing focus on using energy-efficient and environmentally friendly building materials. Energy-efficient windows, facades, and solar control glass are increasingly regarded as integral components of modern buildings when looking to reduce energy usage and improve commercial building performance. The construction sector is adapting advanced glass technologies to fulfill global regulatory requirements and commit to sustainability, with an increased focus on green building standards and smart cities. Solar control and smart glass technologies are increasingly being used in buildings to improve comfort for occupants, reduce HVAC costs, and enhance the aesthetic appeal of a structure.

REGIONAL ANALYSIS:

North America was the largest market, accounting for a 34.7% trademark in 2023, thanks to its high demand in the automotive and construction sectors. A practical example of this is Tesla, a US-based electric car maker. Tesla employs various glass technologies ranging from laminated windshields to panoramic roofs, all of which aid in better safety and insulation, and double up as part of the vehicle's aesthetic appeal. Advanced glass also finds applications in the North American construction sector, such as at smart buildings like the Apple Park headquarters in Cupertino, California. The edifice uses energy-efficient glass which maintains the inside temperature and lightweight glass which saves energy a structure that embodies innovations in environmentally friendly, sustainable architecture for the region.

Asia Pacific is expected to grow with the highest CAGR from 2024–2032 due to the rapid developments in the automotive, construction, and electronics industries. One such example is Chinese EV maker BYD, which equips its EVs with smart glass as part of advanced driver assistance systems (ADAS) to enhance safety, aesthetics, and energy efficiency. Along with this trend, smart glass technologies are also on the rise in the region, with smart cities such as Songdo, South Korea implementing advanced glass technologies for buildings and infrastructure to make buildings and cities more sustainable. In addition, the growth of electronics industries in Asian countries such as Japan, where corporates such as Sony and Sharp are manufacturing advanced glass for consumer electronics and displays, is responsible for increasing the advanced glass market in Asia Pacific. Asia Pacific is the fastest-growing region for advanced glass applications, driven by the fast adoption of these technologies in multiple sectors.

Get Customized Report as per your Business Requirement - Request For Customized Report

KEY PLAYERS:

Some of the major players in the Advanced Glass Market are:

-

Saint-Gobain (Glass wool, Laminated glass)

-

PPG Industries (Architectural glass, Automotive glass)

-

Corning Incorporated (Gorilla Glass, Optical fiber)

-

AGC Inc. (Solar glass, Display glass)

-

Schott AG (Pharmaceutical glass, Display glass)

-

NSG Group (Automotive glass, Architectural glass)

-

Guardian Industries (Float glass, Automotive glass)

-

Asahi Glass Co., Ltd. (AGC) (Solar glass, Display glass)

-

Vitro SAB (Glass containers, Flat glass)

-

Owens-Illinois Inc. (Glass containers, Pharmaceutical packaging)

-

Ardagh Group (Glass packaging, Metal packaging)

-

Verallia (Glass packaging, Food and beverage containers)

-

Vetropack Group (Glass containers, Pharmaceutical packaging)

-

Bormioli Rocco (Glass containers, Tableware)

-

Stoelzle Glass Group (Glass packaging, Pharmaceutical packaging)

-

AGI Glasspack Ltd (Glass containers, Pharmaceutical packaging)

-

Vidrala (Glass containers, Food and beverage packaging)

-

O-I Glass, Inc. (Glass containers, Food and beverage packaging)

-

HNG Float Glass Limited (Float glass, Solar glass)

-

Saint-Gobain SEFPRO (Refractory products, Glass contact materials)

Some of the Raw Material Suppliers for Advanced Glass companies:

-

Corning Incorporated

-

Schott AG

-

Ohara Inc.

-

Heraeus Holding GmbH

-

Pilkington

-

Tosoh Quartz Corporation

-

Saint-Gobain SEFPRO

-

AICELLO Chemical Europe GmbH

-

Glass Service

-

American Glass Research

RECENT TRENDS:

-

In September 2024, Corning unveiled its EXTREME ULE® Glass, designed to enhance microchip production by improving the precision of EUV lithography.

-

In October 2024, AGC Glass Europe partnered with ROSI to advance recycling in the glass industry, aiming to reuse end-of-life photovoltaic glass for flat glass production.

-

In February 2024, Verallia inaugurated the world’s largest all-electric furnace at its plant in Cognac, France, reducing CO₂ emissions by 60%. The furnace will produce eco-friendly glass packaging, supporting sustainability in the Cognac industry.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 64.29 Billion |

| Market Size by 2032 | USD 127.10 Billion |

| CAGR | CAGR of 7.89% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Tempered Glass, Laminated Glass, Ceramic Glass, Others) • By Application (Solar Control, Optics & Lighting, Safety & Security, High Performance, Others) • By End Use (Construction, Infrastructure, Automobiles, Electronics, Aerospace & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Dow Inc., LyondellBasell Industries Holdings B.V., Royal Dutch Shell PLC, BASF SE, SKC Company, AGC Inc., Repsol S.A., Sumitomo Chemical Co., Ltd., Tokuyama Corporation, Indorama Ventures Public Company, INEOS Oxide, Jishen Chemical Industry Co. Ltd., Manali Petrochemicals, Tianjin Dagu Chemical Co., Ltd., PJSC Nizhnekamskneftekhim, PCC Rokita, Wudi XINYUE Chemical Co., Ltd., Oltchim S.A., Wanhua Chemical Group Co. Ltd., S–OIL Corporation |

| Key Drivers | • Surge in Electric Vehicle Adoption and Smart Glass Technologies Drives Advanced Glass Market Growth • Rising Demand for Smart Glass Technologies Boosts Energy Efficiency and Green Building Adoption Worldwide |

| Restraints | • Challenges in Raw Material Availability and Manufacturing Complexity Restrain Advanced Glass Market Growth |

Frequently Asked Questions

Ans. The projected market size for the advanced glass market is USD 114.8 billion by 2032.

Ans: Advanced Glass Market size was USD 64.29 Billion in 2023 and is expected to Reach USD 127.10 Billion by 2032.

Ans: The major growth factor of the Advanced Glass Market is the increasing demand for energy-efficient and sustainable solutions across industries like construction, automotive, and electronics.

Ans: The Automobiles segment dominated the Advanced Glass Market in 2023.

Ans: North America dominated the Advanced Glass Market in 2023.

Ans: The Advanced Glass Market is expected to grow at a CAGR of 7.89% during 2024-2032.

Get in Touch