Aircraft Engine Test Cell Market Report Scope & Overview:

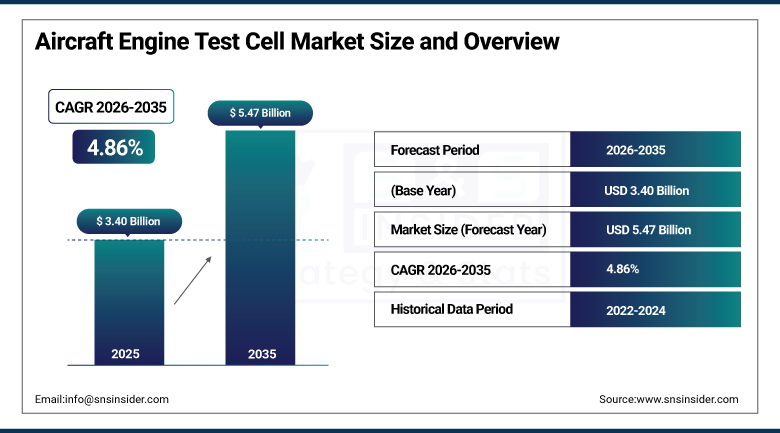

The Aircraft Engine Test Cell Market was valued at USD 3.40 Billion in 2025 and is expected to reach USD 5.47 Billion by 2035, growing at a CAGR of 4.86% from 2026 to 2035.

The Aircraft Engine Test Cell Market continues to expand as these mission-critical facilities evolve well beyond static acceptance testing into an integrated ecosystem for propulsion certification, health monitoring, predictive maintenance, noise control, emissions verification, and lifecycle optimization. Modern aircraft engines operate at higher temperatures, pressures, and bypass ratios than previous generations, requiring test infrastructure capable of reproducing increasingly demanding operating conditions while protecting personnel, equipment, and surrounding communities. Tighter environmental regulations, rising engine complexity, and increasing use of digital instrumentation continue reshaping demand for advanced test cell capability across commercial aviation, defense aviation, business aviation, rotorcraft, and maintenance, repair, and overhaul environments worldwide.

Lockheed Martin completed its first LM 400 satellite platform bus in January 2023 using the company's digital production line, though the aerospace giant's broader propulsion and flight test infrastructure investment continues extending into adjacent engine validation capability supporting military, civil, and commercial aviation programs across its production network.

Market Size and Forecast

- Market Size in 2026E: USD 3.57 Billion

- Market Size by 2035: USD 5.47 Billion

- CAGR: 4.86% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information On Aircraft Engine Test Cell Market - Request Free Sample Report

Aircraft Engine Test Cell Market Trends

- Digital instrumentation and automated data acquisition systems are becoming standard requirements for modern test cell facilities.

- Rising engine bypass ratios and operating temperatures are pushing test infrastructure toward higher-capacity thrust handling capability.

- Tighter environmental and noise regulations near populated areas continue driving investment in acoustic suppression technology.

- Predictive maintenance and health monitoring capability are increasingly integrated directly into test cell control systems.

- Growing military modernization programs continue expanding demand for specialized defense aviation engine test infrastructure.

The United States Aircraft Engine Test Cell Market Outlook

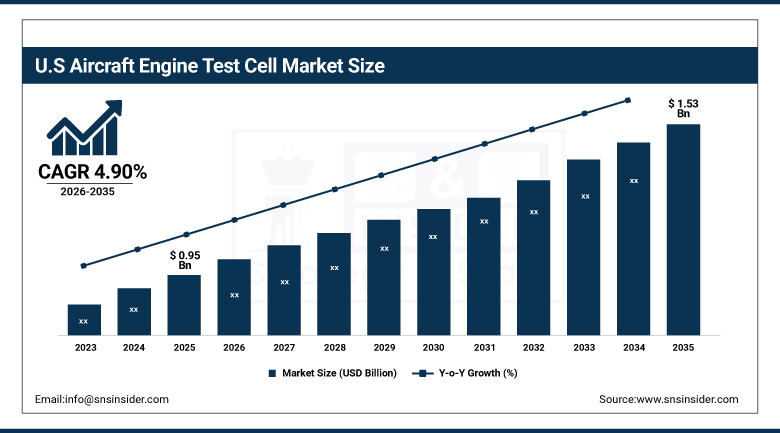

The United States Aircraft Engine Test Cell Market was valued at USD 0.95 Billion in 2025 and is expected to reach USD 1.53 Billion by 2035, growing at a CAGR of 4.90% from 2026 to 2035.

The US retained its leadership position in North America in terms of aircraft engine test cells, owing to the presence of prominent engine manufacturers, a vast defense industry, and numerous facilities for maintenance, repairs, and overhauls in the country. Investment in new testing technologies alongside growing production of civil and military aircraft ensured that the country remained one of the most commercially important national markets for such technology during the year.

In February 2023, the National Aeronautics and Space Administration renewed its partnership with Esri in order to increase access to geospatial data relevant for research and exploration objectives, which was indicative of the continued integration between aerospace testing infrastructure and data analysis technologies in the country.

Aircraft Engine Test Cell Market Segmentation Analysis

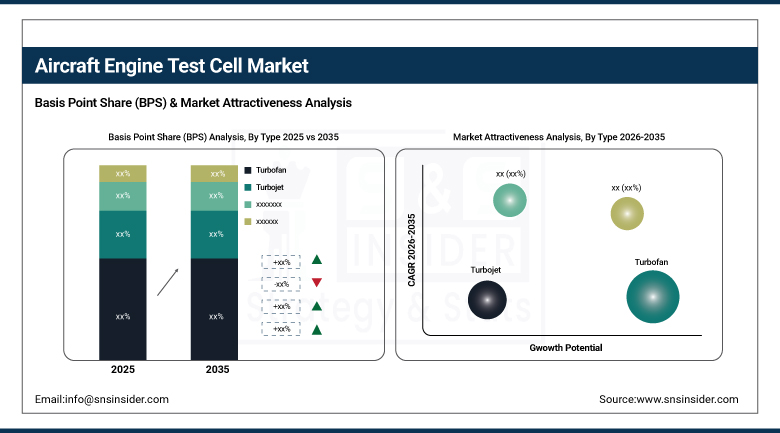

- By Type, the Turbofan segment held approximately 42.30% share in 2025, while the Turboshaft segment is the fastest growing.

- By Application, the Commercial Aviation segment held the largest share in 2025, while the Military Aviation segment is the fastest growing.

- By Component, the Test Stands segment held the largest share in 2025, while the Data Acquisition Systems segment is the fastest growing.

- By End-User, the OEMs segment held the largest share in 2025, while the MROs segment is the fastest growing.

By Type, Turbofan led the market, Turboshaft grew fastest

The Turbofan segment dominated the type category in 2025, holding approximately 42.30% of total revenue, driven by the overwhelming prevalence of high-bypass turbofan powerplants across the global commercial aviation fleet and a growing installed base of military turbofan engines on platforms ranging from fifth-generation fighters to large tactical transports. Turbofan test cells remain the most capital-intensive category, with full-capability large turbofan test cell installations capable of accommodating wide-body engine thrust levels, keeping this segment firmly at the top of the broader type segmentation.

Turbojet will witness the fastest CAGR throughout the forecasted period on account of the increasing production of rotorcraft along with modernization programs of military helicopters which would require specialized testing facilities specific to turboshaft engines. Increasing demand for advanced vertical lift aircraft is driving the growth rate of this particular type category above other types.

By Application, Commercial Aviation led the market, Military Aviation grew fastest

The Commercial Aviation segment held the largest application share in 2025, driven by increasing demand for commercial aircraft and related maintenance, repair, and overhaul services as airlines expand fleets to meet growing passenger demand. That expanding fleet base continues generating sustained testing volume, keeping commercial aviation firmly at the center of overall aircraft engine test cell demand across nearly every major aerospace manufacturing region.

The Military Aviation segment is projected to grow at the fastest CAGR during the forecast period, driven by expanding defense budgets and military modernization programs requiring specialized, often classified, engine testing infrastructure. Rising geopolitical tension continues reinforcing government investment in domestic military aviation testing capability, pushing this application category's growth rate ahead of the broader application segmentation.

By Component, Test Stands led the market, Data Acquisition Systems grew fastest

The Test Stands segment held the largest component share in 2025, anchored by the foundational structural infrastructure, inlet and exhaust airflow management, and fuel and lubrication systems that form the physical backbone of any engine test facility. That necessary foundational infrastructure layer keeps test stands firmly at the top of the broader component segmentation across nearly every test cell installation worldwide.

The Data Acquisition Systems segment is projected to grow at the fastest CAGR during the forecast period, as increasing use of digital instrumentation continues transforming test cells from static acceptance testing facilities into integrated ecosystems for propulsion certification and predictive maintenance. Rising demand for real-time performance data spanning thrust, fuel consumption, temperature, and vibration continues pushing this component category's growth rate ahead of the broader component segmentation.

By End-User, OEMs led the market, MROs grew fastest

The OEMs segment held the largest end-user share in 2025, reflecting original equipment manufacturers' need for comprehensive engine validation and certification testing before new engine models enter commercial or military service. That certification and validation requirement keeps OEMs firmly at the center of overall aircraft engine test cell demand across the broader end-user segmentation.

The MROs segment is projected to grow at the fastest CAGR during the forecast period, driven by increasing demand for commercial aircraft and related maintenance services as airlines expand their fleets to meet growing passenger demand. Rising post-maintenance performance evaluation requirements continue pushing this end-user segment's growth rate ahead of the broader end-user segmentation as global engine deliveries and overhaul cycles increase.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.20% |

|

Europe |

France |

27.60% |

|

Asia Pacific |

China |

35.90% |

|

Middle East & Africa |

UAE |

26.70% |

|

Latin America |

Brazil |

37.40% |

North America Aircraft Engine Test Cell Market Insights

North America held the largest share of the global Aircraft Engine Test Cell Market in 2025, supported by the presence of major engine manufacturers including General Electric and Pratt and Whitney, a massive defense sector, and extensive maintenance, repair, and overhaul operations across the region. That combination of manufacturing depth and defense sector scale continued keeping North America firmly ahead of every other region in this market throughout the year.

The United States accounted for roughly 83.20% of regional revenue, reflecting its concentration of major engine OEMs and defense aviation programs. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding aerospace and MRO sector, keeping North America among the most commercially significant regional markets for aircraft engine test cells throughout the year.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Aircraft Engine Test Cell Market Insights

Europe constituted a sizeable portion of the global Aircraft Engine Test Cell Market in 2025, owing to its emphasis on research towards sustainability in aviation, which was being sponsored by government and EU policies, along with the presence of leading original equipment manufacturers in engines and aircrafts. The region witnessed around 27.60% contribution of France in the revenue generation, which is due to the presence of its leading players in the market like Safran and its Airbus assembly lines.

In addition to that, the UK and Germany also contributed significantly to the demand for the market in the region owing to their established manufacturing facilities for engines and leading companies like Rolls-Royce and MTU Aero Engines.

Asia Pacific Aircraft Engine Test Cell Market Insights

Asia Pacific was the fastest-growing region in the global Aircraft Engine Test Cell Market, driven by explosive growth in air travel and aircraft deliveries across the region's rapidly expanding aviation markets. Continued investment in domestic engine testing infrastructure, including new narrowbody-focused test cell facilities, continued reinforcing regional demand throughout the year.

China accounted for roughly 35.90% of regional revenue, supported by expanding domestic MRO capacity and growing narrowbody engine testing infrastructure investment. Japan and South Korea contributed significant additional regional demand through their own advanced aerospace manufacturing and MRO industries, reinforcing Asia Pacific's position as the clear growth leader in this market through the forecast period.

MEA & Latin America Aircraft Engine Test Cell Market Insights

The Middle East and Africa region recorded steady growth in aircraft engine test cell adoption in 2025, driven by expanding regional airline fleets and growing MRO hub investment across the Gulf states in particular. The UAE accounted for roughly 26.70% of regional revenue, supported by national aviation hub strategy investment and rising demand for regional engine testing and overhaul capability.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.40% of regional revenue, where growing regional airline fleet expansion continued to support category growth. Mexico and Argentina followed a similar trajectory as regional aerospace manufacturing and MRO capacity expanded further through the remainder of the forecast period.

Growth Drivers: Rising aircraft deliveries and stricter environmental compliance

Increasing demand for commercial aircraft and related maintenance, repair, and overhaul services continues to be the central force behind aircraft engine test cell market growth, as airlines expand fleets to meet growing passenger demand. That expanding fleet base requires corresponding growth in engine testing and maintenance capacity, reinforcing structural demand across nearly every major aerospace manufacturing and MRO region worldwide.

Tighter environmental regulations, rising engine complexity, and increasing use of digital instrumentation continue reshaping demand for advanced test cell capability. Modern aircraft engines operating at higher temperatures, pressures, and bypass ratios require test infrastructure capable of reproducing increasingly demanding operating conditions, reinforcing sustained capital investment across commercial, defense, and business aviation test cell categories.

Restraints: High retrofitting costs and stringent siting regulations

High costs associated with retrofitting aging test cell infrastructure continue restricting modernization pace among operators managing older facility networks. That retrofit cost burden can meaningfully affect capital planning for MRO providers and smaller engine manufacturers working with constrained infrastructure budgets.

Stringent environmental and noise regulations in populated areas continue complicating new test cell siting decisions, as acoustic suppression and emissions control requirements add both cost and design complexity to new facility construction. That regulatory complexity continues concentrating new large-scale test cell investment among well-capitalized operators capable of navigating extended permitting and compliance timelines.

Opportunities: Digital twin integration and hypersonic engine test capability

The increasing use of digital twin solutions opens up a considerable amount of potential for test cell operators who have the capability to combine virtual modeling with physical testing systems. This can help reduce development time and increase predictive maintenance capabilities, resulting in an increasing share of demand from engine manufacturers looking to accelerate their certification processes.

In addition, the increased need for testing capabilities for hypersonic and adaptive cycle engines is another important potential for growth, as the development of advanced propulsion technologies continues to accelerate. Test cell operators with the capacity to venture into such high-end, high-revenue categories can generate considerable income through 2035.

Recent Developments:

- 2025: Mitsubishi Heavy Industries continued supplying engine test cells for post-maintenance performance evaluation of aircraft jet engines, with facilities capable of accommodating large jet engines generating up to 140,000 pounds of thrust force.

- 2025: MTU Maintenance advanced operational readiness of its Zhuhai Jinwan Branch test cell in China, a 60,000-pound thrust facility specifically engineered to accommodate narrowbody engines including the PW1100G-JM and V2500 models.

- 2025: General Electric Aviation continued expanding its global engine test and service network, reinforcing its position as the competitive landscape leader with the broadest service footprint supporting commercial and military engine programs.

Aircraft Engine Test Cell Market key players are:

- General Electric Company

- Rolls-Royce Holdings plc

- Pratt & Whitney

- Safran S.A.

- MTU Aero Engines AG

- Honeywell International Inc.

- CFM International

- Mitsubishi Heavy Industries, Ltd.

- ATEC

- Universal Hydraulik GmbH

- Aerodyne Industries LLC

- ETS Aviation Ltd.

- Sonic Development LLC

- Duncan Aviation, Inc.

- AAR Corp.

- ST Engineering Aerospace

- Lufthansa Technik AG

- CATIC

- Woodward, Inc.

- Meggitt PLC

Aircraft Engine Test Cell Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.40 Billion |

| Market Size by 2035 | USD 5.47 Billion |

| CAGR | CAGR of 4.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Turbofan, Turbojet, Turboprop, Turboshaft) • By Application (Commercial Aviation, Military Aviation, General Aviation) • By Component (Test Stands, Data Acquisition Systems, Control Systems, Instrumentation) • By End-User (OEMs, MROs, Airlines) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | General Electric Company, Rolls-Royce Holdings plc, Pratt & Whitney, Safran S.A., MTU Aero Engines AG, Honeywell International Inc., CFM International, Mitsubishi Heavy Industries, Ltd., ATEC, Universal Hydraulik GmbH, Aerodyne Industries LLC, ETS Aviation Ltd., Sonic Development LLC, Duncan Aviation, Inc., AAR Corp., ST Engineering Aerospace, Lufthansa Technik AG, CATIC, Woodward, Inc., Meggitt PLC |

Frequently Asked Questions

Rising commercial and military aircraft deliveries combined with stricter environmental compliance requirements is the major growth factor.

The Aircraft Engine Test Cell Market is expected to grow at a CAGR of 4.86% from 2026 to 2035.

The Aircraft Engine Test Cell Market was valued at USD 3.40 Billion in 2025.

North America held the largest share of the Aircraft Engine Test Cell Market in 2025, while Asia Pacific was the fastest-growing region.

The Turbofan segment held approximately 42.30% share in 2025.

Get in Touch