Agricultural Adjuvants Market Report Scope & Overview:

Get More Information on Agricultural Adjuvants Market - Request Sample Report

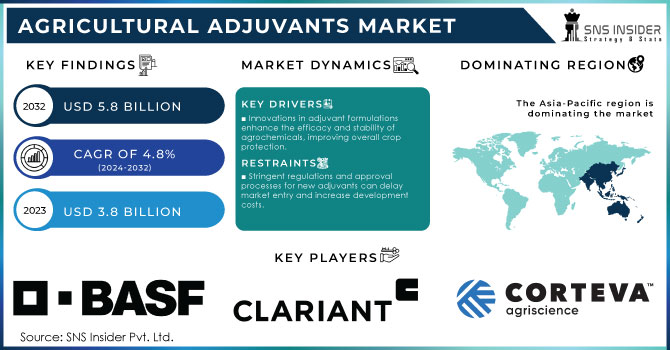

The Agricultural Adjuvants Market Size was valued at USD 3.8 billion in 2023, and is expected to reach USD 5.8 Billion by 2032, and grow at a CAGR of 4.8% over the forecast period 2024-2032.

The need to enhance the efficiency of agrochemicals herbicides, insecticides, and fungicides also makes the agricultural adjuvants market a critical component of modern farming. Adjuvants are substances that alter the behavior of pesticides, enhancing the performance of pesticides by increasing their effectiveness, stability, and application efficiency. It is a very dynamic market driven by such factors as technological advancements, changes in legislation, and changing consumer preference to more sustainable agriculture.

Recently, there have been impressive breakthroughs in the development and use of adjuvants for agricultural purposes. For instance, one significant innovation took place early this year in March 2022 when Clariant officially launched a new adjuvant called ADJUWEX. The new adjuvant is an additive intended to boost the effectiveness of glufosinate herbicides, meant to control weeds on various crops. This formulation is targeted towards improvement in herbicide performance since it maximizes the intake of active ingredients, hence better crop protection overall. It is one of the latest developments in a trend toward more efficient and focused agricultural solutions. Similarly, in April 2024, CHS Inc. presented pragmatic advice on adjuvant selection, reminding the public to choose the right adjuvants to maximize pesticide performance. The keys pointed out as far as selecting appropriate adjuvants in place are better crop yield and reduced chemical usage, the advisory reminded the public that this is where the focus is going more and more on optimizing adjuvant use to cultivate more sustainable agricultural practices. Furthermore, May 2024 was witness to a landmark moment in the marrying of adjuvants with yeast-based vaccines. This may well revolutionize the nature of vaccines available in agriculture, going forward. From that, it is clear that the role of adjuvants in applications beyond their use in pesticides can only grow. Another great development was the announcement in October 2023 of a partnership between Inimmune and Boston Children's Hospital toward developing novel adjuvants. Novel adjuvants could make vaccines more effective. This development is human health-oriented, but the findings made may impact the agricultural sector in the future as it will depend on how to enhance the formulation of the vaccine and pesticide formulations.

Additionally, January 2023 has to do with the proper application of adjuvants, which enables the herbicide to do an effective job. Such information enhances the proper execution of weed control and would thereby enhance crop management and productivity. The agricultural adjuvants market is evolving, and constant innovation and adaptation are taking place. The new developments point toward the improvement in the performance and versatility of adjuvants toward the universal aim of agricultural efficiency and sustainability.

Agricultural Adjuvants Market Dynamics:

Drivers:

-

Innovations in adjuvant formulations enhance the efficacy and stability of agrochemicals, improving overall crop protection.

Formulations of adjuvants have greatly enhanced the efficiency and stability of agrochemicals for broader crop protection. For instance, new surfactants and emulsifiers help in making more effective delivery systems for pesticides and herbicides. New adjuvants, for example, provide a better wetting and spreading of herbicide solutions to herbicides, resulting in uniform deposition on plant surfaces. This upsurges uptake into leaves and enhances the efficiency of herbicides in controlling weeds. Beyond this, advances in adjuvant technology have led to the development of stable adjuvants that are insensitive to extreme conditions of the environment like elevated temperatures and pH fluctuations. These conditions ensure efficacy during their application period using a reduced number of treatments and chemicals. Advanced adjuvants based on nanotechnology are a good example, which can help increase the precision of pesticide application to control specific pest species so that off-target effects will be reduced. These new technologies enhance not only pest and disease management but also contribute to more sustainable farming practices since their incorporation brings minimal environmental impacts from the application of agrochemicals. In general, such technological advancements in adjuvant formulations are important so that crop protection methods can be optimized to be much more effective and reliable in modern agriculture.

-

Growing demand for sustainable farming practices boosts the adoption of adjuvants that increase the efficiency and environmental benefits of pesticides.

Increased demand for sustainable farming, with sustainable pesticide application using the help of improved adjuvants, increases efficiency and environmental advantage in the use of pesticides. As farmers and agricultural interests become more environmental conscious, seeking to minimize adverse impacts while realizing maximum output, pesticide adjuvants present a need for improvement in pesticide performance and diminish adverse impacts. For instance, the utilization of adjuvants that enhance pesticide adhesion and penetration enables the application of pesticides at low rates while reducing chemical load in the environment. Biodegradable and environment-friendly adjuvants have been developed in place of traditional formulations that can linger in the environment and cause harm to non-target organisms. Among the notable advancements is the application of adjuvants that act synergistically with an integrated pest management approach. These enhance pesticide selectivity-pesticides that kill pests and spare all beneficial insects and pollinators. Other adjuvants improve nutrient and agrochemical absorption, reduce runoff and leaching, and thus contribute to healthier soils and waters. However the embracing of such advanced adjuvants shows a large movement to agricultural methods that balance productivity and environmental stewardship, thereby overcoming both economic and ecological concerns in modern agriculture.

Restraint:

-

Stringent regulations and approval processes for new adjuvants can delay market entry and increase development costs.

Strict regulations and complicated processes of approval for new adjuvants may increase their entry time to the market and also influence cost development. In general, regulatory authorities always impose strict requirements regarding the safety of new adjuvants for users and the environment so more tests and documentation are required for new adjuvants. For instance, several clinical trials should be conducted before a newly discovered adjuvant could be sold on the market to determine its safety, environmental acceptability, and even risk to the health of human and animal subjects. These requirements translate into long approval times and investments from the companies. For example, a development company for a new adjuvant could end up spending much time and cost on several rounds of testing and data submissions. This regulatory burden might be specific enough to choke the smaller firms or market entrants, potentially restraining innovation and slowing the adoption of advanced adjuvant technologies.

Opportunity:

-

Expanding agricultural sectors in developing regions present opportunities for growth in adjuvant adoption to improve crop yields and pest control.

The growth of agriculture sectors in developing regions is one of the biggest opportunities for adjuvants, given that these areas look for ways to improve their crop yields and find better systems for pest control. Improved cropping systems have a growing requirement for more effective technologies that can boost productivity, and this demand should create an opportunity for advanced adjuvants. For instance, with countries under rapid agricultural growth whether in Sub-Saharan Africa or Southeast Asiapo, farmers embrace modern techniques to increase food production and take better care of pests. The transformation would be all that much easier if adjuvants were able to enhance the performance of pesticides and fertilizers, thus more effective crop protection and nutrient use. This trend therefore portrays a highly lucrative market for the firms that have successfully developed innovative adjuvant products specifically designed for these unique needs and challenges in these developing regions. This, on the other hand, goes to improve agricultural productivity and food security.

Challenge:

-

The need for highly specialized and compatible adjuvant formulations can complicate product development and market differentiation.

Highly specialized and compatible adjuvant formulations in the agricultural adjuvants market are a major challenge because they complicate product development as well as market differentiation. Because these effective adjuvants interact with various pesticides while responding to crop-specific requirements, adjuvants involve intricate formulation science and rigorous testing. For instance, developing an adjuvant for a particular herbicide formulation should be compatible so as not to harm the herbicide performance or crop safety. Such complexity calls for extensive research and development to create tailor-fit solutions-which would be both time and resource-consuming. The marketplace also gets filled up with divergent adjuvant products, making it even harder to identify what is unique from the crowd. But as this happens, there is an even greater need for innovation and optimal marketing strategies to differentiate and remain competitive. This reflects the importance of specialized knowledge and strategic planning to successfully penetrate and expand in the competitive marketplace of adjuvant formulation with a competitive edge.

Agricultural Adjuvants Market Segment Overview

By Source

The petroleum-based segment dominated the agricultural adjuvants market in 2023, accounting for an estimated 65% share. This is because petroleum-based adjuvants have been widely used today due to their cost-effectiveness and proven reliability for performance in agrochemical applications. Petroleum-based adjuvants remain a favorite due to their variety and effectiveness in impeding and promoting a wide range of pesticides and herbicides. For instance, these adjuvants are used and formulated to increase the spreadability and absorption of chemicals on the leaves and surfaces of the plant in enhancement of pest control and crop protection. Though interest in bio-based alternatives is getting larger, infrastructure and proven benefits built up using petroleum-based adjuvants will secure their leading position in the market.

By Product

In 2023, activator adjuvants dominated the market by holding approximately a share of about 55%. The segment of activator adjuvants is at the top because activator adjuvants, primarily surfactants and oil-based adjuvants, have an indispensable function in improving the performance of agrochemicals. Surfactants, for instance, enhance the wetting, spreading, and penetration of pesticides and herbicides to create a more thorough coverage and better absorption by plant surfaces. Oil-based adjuvants also help agrochemicals to improve their wetting ability and ability to penetrate deeper into the plant tissue. Through maximization of the utility of chemical application effectiveness, activator adjuvants have enjoyed a strong preference, thus entrenching them as market leaders.

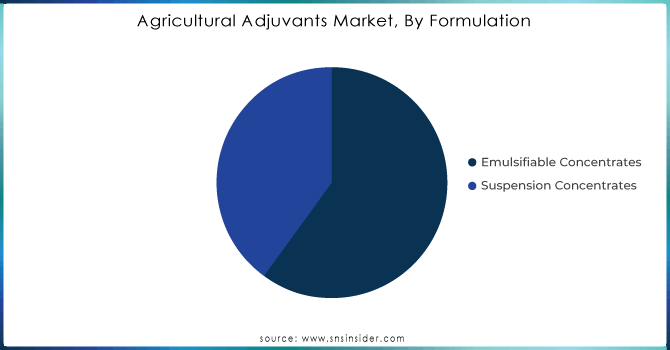

By Formulation

The emulsifiable concentrates segment dominated the agricultural adjuvants market in 2023, accounting for approximately 60%. This can be primarily attributed to the versatile application and effectiveness of emulsifiable concentrates in agrochemical formulations of various sizes. These products consist of active ingredients dissolved in oil, with water being mixed to create an emulsion and exhibit superior performance in spreading and penetration on plant surfaces. For example, emulsifiable concentrates are extensively used in herbicides and insecticides, which enhance coverage and effectiveness; they are more effective when it comes to controlling pests and crop protection. Due to them being easy to use and compatible with a wide range of agrochemicals, their leading market position has been contributed.

Get Customised Report as per Your Business Requirement - Enquiry Now

By Crop Type

In 2023, the fruits & vegetables segment dominated and accounted for a market share of about 50% in the agricultural adjuvants market. Its leadership status owes to the high requirement of fruit and vegetable crops for intensive pest management and protection, needing special adjuvants to ensure proper application and favorable quality of the yield. For example, on the ingredient part, adjuvants enhance the attachment and penetration of fungicides and insecticides on delicate surfaces of fruits and vegetables, thereby improving disease control and pest resistance. Consequently, factors like crop value and perishable nature stimulate considerable demand for advanced adjuvant solutions that can provide precise protection thus maintaining the dominant market for this ingredient segment.

By Application

The herbicides segment dominated and accounted for a market share of around 45% in the agricultural adjuvants market in 2023. This is due to the wide usage of herbicides in weed management, where active adjuvants take an important role in enhancing herbicide effectiveness against unwanted vegetation. Herbicide adjuvants improve adhesion and spreadability and enhance the absorption of herbicides on the leaf surfaces of plants. Examples include surfactants and oil-based adjuvants. They are usually applied with herbicides. These adjuvants enable the action of the herbicides by reducing the surface tension and increasing penetration into the weed tissues. The largest driving force for this market is the colossal demand by most crops like cereals and vegetables for effective weed control solutions.

Agricultural Adjuvants Market Regional Analysis

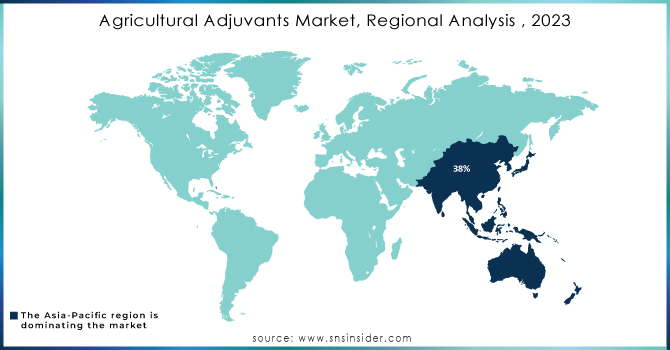

The Asia-Pacific region dominated the Agricultural Adjuvants Market with a revenue share of approximately 38% in 2023. The agricultural landscape in the region accommodates a wide variety of crops and farming practices. A considerable part of the world's population resides in this region, so the demand for food and agricultural products is always high. Hence, Asian-Pacific farmers and agricultural professionals are constantly seeking innovative ways to increase the yields of their crops to address this escalating demand. In addition, the Asian Development Bank has invested heavily in the program to help alleviate a worsening food crisis in Asia. The Asian Development Bank recently launched its ambitious allocation plan of at least $14 billion between 2022 and 2025 because of the intensifying food crisis in the Asia-Pacific region. This support program not only deals with short-term problems but also strives to build long-term food security by strengthening food systems against the impacts of climate change and biodiversity loss. It represents a major expansion of ADB's current efforts to address the imperative of food security in the region. Astonishingly, there are now about 1.1 billion people in Asia and the Pacific without access to adequate diets, as the twin burdens of poverty and sky-high food prices have reached unprecedented heights in 2022.

Key Players

-

BASF SE (Dash HC, Agnique, Break-Thru)

-

Brandt Consolidated, Inc. (Brandt 5 Star, Brandt Smart System, Brandt TriTek)

-

Clariant AG (Synergen OS, Genagen, Hostapon)

-

Corteva Agriscience (VaporGrip, Surpass NXT, Keystone NXT)

-

Croda International PLC (Atplus, Renex, Hypermer)

-

Dow Chemical Company (Verdict, Intrepid Edge, Surpass)

-

Evonik Industries AG (BREAK-THRU S240, BREAK-THRU DF, BREAK-THRU SD 260)

-

GarrCo Products, Inc. (Snap, Surfate, Tenacity)

-

Helena Chemical Company (Induce, Grounded, Delta Gold)

-

Huntsman International LLC (Agrimax, Teric, Ethylan)

-

KALO, Inc. (RainDrop, Aqua-Zorb, Hydro-Wet)

-

Miller Chemical & Fertilizer (Induce, Tank and Tracker, Millerplex)

-

Nufarm Ltd. (Nuance, LI 700, WeedMaster)

-

Precision Laboratories (Border Xtra, Protyx, Jet Shield)

-

Solvay SA (Rhodafac, Geronol, Actizone)

-

Stepan Company (STEPGROW, STEPOSOL, MAKON)

-

Tanatex Chemicals B.V. (Baytan, Verbenone, Dropp)

-

UPL Limited (DewAqua, Lifeline, Interline)

-

Wilbur-Ellis Holdings, Inc. (Brimstone, Kudos, Destiny)

-

Winfield United (MasterLock, Interlock, Strike Force)

Recent Developments

-

July 2024: SPI Pharma and Inimmune Corp. collaborated to research and market novel adjuvant systems for vaccines, by utilizing the key advantages to boost vaccine performance further.

-

March 2024: Croda International collaborated with AAHI to provide some of the most impactful vaccine adjuvant technologies and to assist in the development of next-generation vaccines around the globe for vaccination.

-

February 2024: Ginkgo Bioworks and SaponiQx were awarded a contract to design next-generation vaccine adjuvants using generative molecular design to enhance vaccine performance.

-

January 2023: Lavoro Acquires Cromo Química in a Bid to Extend Its Offerings and Boost Its Sales Positioning within Latin American Agriculture while Strengthening Crop Protection Products.

-

Agricultural Adjuvants Market Report Scope:

Report Attributes Details Market Size in 2023 US$ 3.8 Billion Market Size by 2032 US$ 5.8 Billion CAGR CAGR of 4.8% From 2024 to 2032 Base Year 2023 Forecast Period 2024-2032 Historical Data 2020-2022 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments •By Source (Bio-based, Petroleum-based)

•By Product (Utility Adjuvants [Compatibility Agents, Buffering Agents, Water Conditioning Agents, Drift Control Agents, Antifoaming Agents, Others], Activator Adjuvants [Oil-based Adjuvants, Surfactants])

•By Formulation (Emulsifiable Concentrates, Suspension Concentrates)

•By Crop Type (Fruits & Vegetables, Cereals & Grains, Oilseeds & Pulses, Others)

•By Application (Insecticides, Herbicides, Fungicides, Others)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) Company Profiles BASF SE, Clariant AG, Croda International PLC,

Dow Chemical Company, Evonik Industries AG, Huntsman International LLC, Miller Chemical & Fertilizer, Nufarm Ltd., Solvay SA, Stepan Company and other key playersKey Drivers • Innovations in adjuvant formulations enhance the efficacy and stability of agrochemicals, improving overall crop protection

• Growing demand for sustainable farming practices boosts the adoption of adjuvants that increase the efficiency and environmental benefits of pesticidesRESTRAINTS • Stringent regulations and approval processes for new adjuvants can delay market entry and increase development costs

Frequently Asked Questions

Ans: The herbicide segment holds the highest revenue share of about 49.2% for the Agricultural Adjuvants Market in 2023.

Ans: The activator adjuvants segment dominated the Agricultural Adjuvants Market with a revenue share of about 71.3% in 2023.

Ans: Stringent regulations and approval processes for new adjuvants can delay market entry and increase development costs hinder the growth of the Agricultural Adjuvants Market.

Ans: The Agricultural Adjuvants Market is growing at a CAGR of 4.8% during the forecast period of 2024-2032.

Ans: The market size of Agricultural Adjuvants was valued at USD 3.79 billion in 2023.

Get in Touch