Electronic Grade Sulfuric Acid Market Report Scope & Overview:

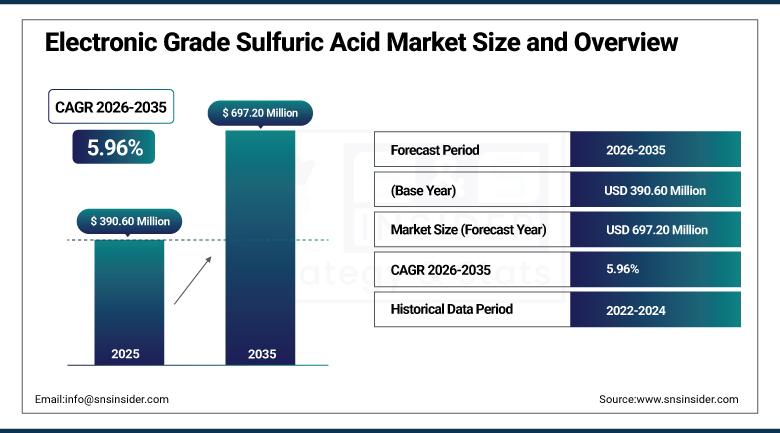

The Electronic Grade Sulfuric Acid Market was valued at USD 390.60 Million in 2025 and is expected to reach USD 697.20 Million by 2035, growing at a CAGR of 5.96% from 2026–2035.

The Electronic Grade Sulfuric Acid Market is experiencing steady growth owing to the rise in demand from the manufacture of semiconductors, particularly in advanced node semiconductors that require high purity acids for wafer cleaning and etching applications. The growth in the manufacture of electronics such as consumer electronic products, automotive electronic devices, and IoT devices is contributing to the rise in demand. The increase in the use of advanced and small semiconductors has increased the demand for high purity acids. Growth in the production of printed circuit boards (PCBs), together with advances in chemical processing accuracy, is enhancing the growth of the market.

In 2024, Stella Chemifa Corporation expanded its electronic grade sulfuric acid production capacity at its Osaka facility with a new ultra-purification line achieving sub-ppt metallic impurity levels meeting SEMI Grade E5 specifications for leading-edge below-3nm node semiconductor fabrication. According to the U.S. Department of Commerce (CHIPS for America Program), over USD 200 billion in private semiconductor investments have been announced in the U.S.

Electronic Grade Sulfuric Acid Market Size and Forecast:

-

Market Size in 2026E: USD 413.90 Million

-

Market Size by 2035: USD 697.20 Million

-

CAGR: 5.96% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On Electronic Grade Sulfuric Acid Market - Request Free Sample Report

Electronic Grade Sulfuric Acid Market Trends:

-

Rising demand from semiconductor manufacturing and microelectronics industry driving adoption of ultra-high purity electronic grade sulfuric acid for wafer cleaning and etching processes

-

Growing expansion of advanced chip fabrication facilities and increasing investments in semiconductor production boosting consumption of high-purity chemicals

-

Increasing miniaturization of electronic components requiring ultra-clean processing chemicals to ensure defect-free chip surfaces and higher yields

-

Expanding use in display panel manufacturing, including LCD and OLED production, supporting precision cleaning and surface preparation applications

-

Continuous improvements in purification and filtration technologies enabling production of higher purity grades to meet stringent semiconductor industry standards

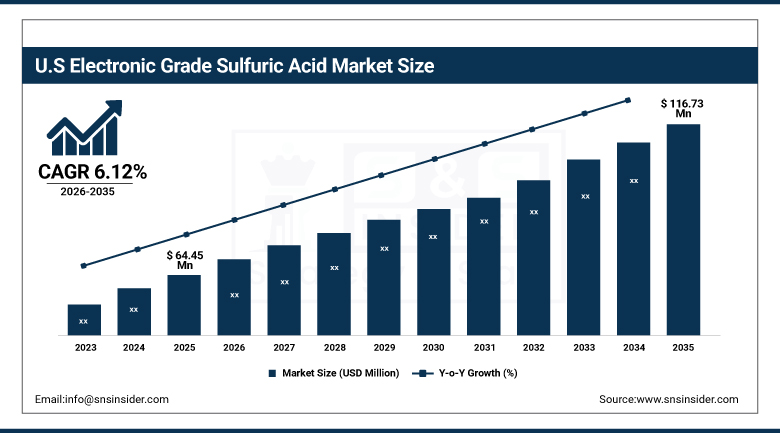

U.S. Electronic Grade Sulfuric Acid Market Outlook:

The U.S. Electronic Grade Sulfuric Acid Market was valued at USD 64.45 Million in 2025 and is expected to reach USD 116.73 Million by 2035, growing at a CAGR of 6.12% from 2026–2035.

The U.S. Electronic Grade Sulfuric Acid Market is the fastest-growing major national market, driven by the CHIPS Act’s USD 52 billion semiconductor manufacturing investment creating domestic fab capacity whose electronic grade chemical procurement is unprecedented in scale. The TSMC Phoenix Arizona Fab 21, Intel Ohio One facility, Samsung Austin’s advanced node expansion, and Micron Memory Idaho facility collectively create structured long-term electronic grade sulfuric acid procurement from qualified domestic and international suppliers. CMC Materials (now Entegris), Honeywell, and KMG Chemicals collectively serve the domestic procurement demand.

In 2025, Entegris (formerly CMC Materials) expanded its electronic grade sulfuric acid supply capacity at its Burnet, Texas facility to serve the growing CHIPS Act-funded semiconductor fab buildout in the U.S. Southwest, establishing long-term supply agreements with TSMC Arizona and Intel Ohio for ultra-pure acid delivery whose purity specifications align with leading-edge below-3nm node fabrication requirements.

Electronic Grade Sulfuric Acid Market Segment Analysis:

-

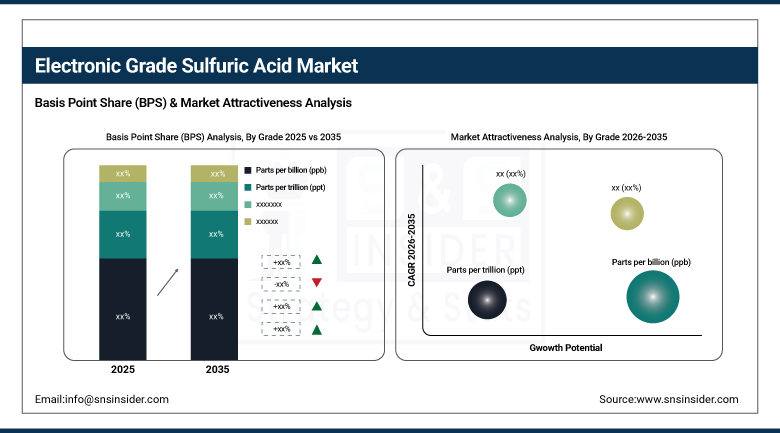

By Grade, parts per billion (ppb) segment dominated the Electronic Grade Sulfuric Acid Market in 2025 with 56% share; parts per trillion (ppt) segment is the fastest growing segment.

-

By Application, semiconductors segment dominated the market in 2025 with 72% share; PCB panels segment is the fastest growing segment.

By Grade, parts per billion (ppb) segment dominates the electronic grade sulfuric acid market, while parts per trillion (ppt) segment is the fastest-growing segment

The parts per billion (ppb) segment dominated the Electronic Grade Sulfuric Acid Market in 2025 because of the high application of this product in semiconductor manufacture where very high purity is required. PPB strikes the right balance between cost efficiency and strict purity requirements in semiconductor production. Existing manufacturing capacity, reliable supply chain management, and wide application in mature fabrication plants have further enabled the segment's dominant position within global electronics and semiconductors applications.

The parts per trillion (ppt) segment is the fastest growing due to increasing demand for ultra-high purity chemicals with minimum contamination in advanced semiconductor nodes. Adoption of semiconductor manufacturing processes for AI chips, high-end computing solutions, and the next generation of memory technologies is boosting ppt market segment growth. The decreasing size of components, along with stringent contamination criteria in fabrication process, are also boosting the ppt segment growth rate in the Electronic Grade Sulfuric Acid market.

By Application, semiconductors segment dominates the electronic grade sulfuric acid market, while PCB panels segment is the fastest-growing segment

The semiconductors segment dominated the Electronic Grade Sulfuric Acid Market in 2025 due to its crucial application in the cleaning, etching, and surface preparation process. Demand for the segment is supported by high volume chip production in consumer electronics, computing, and communication applications. The segment thrives due to massive manufacturing capabilities, extensive investments in advanced nodes, and innovations in integrated circuits. Importance of this segment is evident due to its crucial role in improving yields and minimizing contamination.

The PCB panels segment is the fastest growing due to the rising demand for electronics, automotive electronics, and communications. High adoption rate of high-density interconnect boards and small-sized circuits will continue driving the growth of this segment in coming years. Development of infrastructure associated with 5G network, electric vehicle, and Internet of Things will be major contributors towards the growth of this segment. This segment will be driven by the growing need for high purity chemicals to perform cleaning and etching processes.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

Taiwan |

32.4% |

|

Middle East & Africa |

Israel |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Electronic Grade Sulfuric Acid Market Insights

North America held a significant market share and is the fastest-growing segment during the forecast period. The growth is attributed to the robust semiconductor manufacturing, electronics, and high-technology sectors in the region. The U.S., in particular, has some of the largest semiconductor manufacturers globally, including Intel, Micron Technology, and Applied Materials, which all use high-purity chemicals, including electronic grade sulfuric acid, in their fabrication. Moreover, the investments in developing next-gen technologies like 5G, AI, and IoT are also fueling the demand for more advanced semiconductor components, and hence increasing the consumption of ultra-pure chemicals in North America.

Intel Corporation is investing approximately USD 100+ billion to expand semiconductor fabrication capacity across the U.S. Taiwan Semiconductor Manufacturing Company (TSMC) is also expanding its operations through multi-billion-dollar fabrication plants in Arizona, which is further strengthening demand for ultra-high purity chemical supply chains, including electronic grade sulfuric acid.

Canada contributes approximately 12.6% of North American revenues through its semiconductor and advanced electronics manufacturing, the quantum computing research community’s specialty chemical procurement, and the photovoltaic manufacturing sector’s acid processing demand.

Europe Electronic Grade Sulfuric Acid Market Insights

Europe is a growing electronic grade sulfuric acid market where the EU Chips Act’s European fab investment, ASML’s EUV lithography customer ecosystem creating semiconductor concentration, and the automotive semiconductor supply chain’s domestic capacity investment create structured demand. Germany accounts for approximately 22.3% of European revenues through Infineon’s domestic fab, the automotive semiconductor sector’s quality chemical procurement, and Merck KGaA’s specialty chemical manufacturing.

According to the European Commission (EU Chips Act), Europe aims to achieve 20% of global semiconductor production by 2030, supported by approximately €43 billion in combined public and private investment. Germany and France are also advancing semiconductor initiatives, including large-scale fabs by Intel and STMicroelectronics, which are driving multi-billion-euro investments in advanced manufacturing ecosystems and strengthening demand for ultra-high purity electronic chemicals such as electronic grade sulfuric acid.

Ireland, the Netherlands, and Italy are significant secondary markets where Intel’s Leixlip facility, ASML’s Eindhoven ecosystem, and STMicroelectronics’ Agrate facility create structured electronic grade chemical procurement.

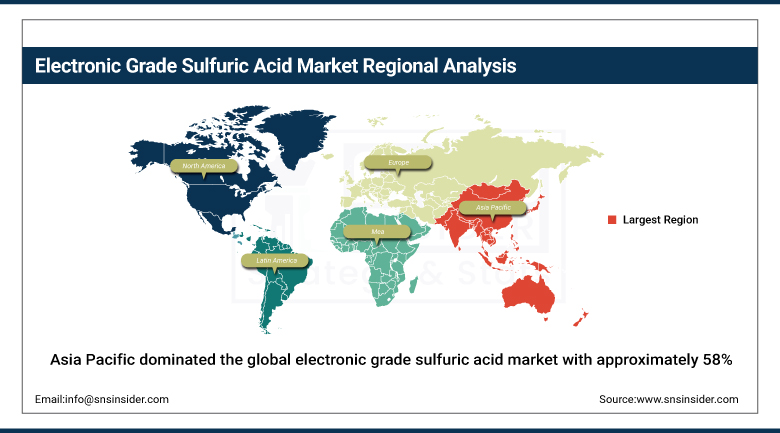

Asia Pacific Electronic Grade Sulfuric Acid Market Insights

Asia Pacific dominated the global electronic grade sulfuric acid market with approximately 58% of revenues in 2025, driven by the world’s largest concentration of semiconductor fabrication capacity in Taiwan, South Korea, Japan, and China. Taiwan accounts for approximately 32.4% of Asia Pacific revenues through TSMC’s extraordinary advanced node fabrication scale, Taiwan Semiconductor Manufacturing’s leading-edge 3nm and 2nm production, and the domestic PCB fabrication industry’s consistent procurement.

According to the Taiwan National Science and Technology Council, Taiwan accounts for ~60% of global foundry output. Taiwan Semiconductor Manufacturing Company (TSMC) produces over 12 million 12-inch wafer equivalents annually, with each wafer undergoing hundreds of wet cleaning processes that require ultra-high purity acids.

In South Korea, Samsung and SK Hynix together contribute more than 30% of global memory chip production. Meanwhile, China’s Ministry of Industry and Information Technology reports strong growth in consumer electronics manufacturing and a semiconductor self-sufficiency target exceeding 70%, further reinforcing demand for advanced electronic-grade chemical supply chains.

South Korea’s Samsung Semiconductor and SK Hynix’s combined DRAM and NAND flash production, Japan’s specialty semiconductor device manufacturing, and China’s expanding domestic fab capacity collectively sustain Asia Pacific’s market dominance across diverse semiconductor and PCB application procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Electronic Grade Sulfuric Acid Market Insights

Israel leads MEA revenues at approximately 38.4% through Intel Haifa’s advanced semiconductor design facility, Tower Semiconductor’s analog fabrication, and the growing domestic research community’s structured electronic grade chemical procurement creating above-average MEA commercial concentration.

Brazil leads Latin American revenues at approximately 44.2% through its PCB fabrication industry’s acid wet processing, the growing domestic electronics manufacturing sector, and the photovoltaic manufacturing sector’s chemical demand. Saudi Arabia’s semiconductor design centre investment and UAE’s technology sector collectively sustain MEA market development through 2035.

Market Dynamics:

Growth Drivers: Global semiconductor fab expansion and CHIPS Act-driven domestic capacity creating structured procurement

The unprecedented spending by the global semiconductor industry, which has annual fab spending on an aggregate basis from TSMC, Samsung, and Intel surpassing USD 200 billion over the period 2023-2026, has led to the greatest demand growth opportunity in terms of commercial certainty in electronic grade chemicals ever seen in the industry. Each 300mm fab built translates into specific procurement of electronic grade sulfuric acid that begins during facility qualification and hits its peak production volume at 12-18 months after wafer out start-up. The CHIPS Act’s build of capacity in the U.S. leads to procurement geographies that were formerly dependent on Asian suppliers.

Purity escalation needs in advanced node transition creates value enhancement to allow revenue growth rates that exceed volume growth rates. Each advanced node transition from 5nm to 3nm to 2nm means a need for procurement specification transition to ppt levels from ppb, resulting in a price premium per liter above standard electronic grade.

Restraints: High production cost for ppt-grade purification and supply chain qualification complexity

The multi-stage distillation, absorption, and metal contamination elimination process used in the manufacture of ultra-high purity grade sulfuric acid makes the business economics for this product more costly than commodities due to the cost of the production structure involved, thereby making the economic feasibility of producing ppt grades possible only through specialized chemical manufacturers with large investments in purification equipment.

The need for SEMI specifications qualification of each new supplier manufacturing ppt grades to each semiconductor manufacturer delays their involvement in premium chemical markets by up to 12-24 months before being able to supply their products.

Opportunities: CHIPS Act domestic supply creation and recycling/regeneration services

CHIPS Act-funded domestic U.S. semiconductor fab capacity creates the most commercially certain near-term electronic grade sulfuric acid market expansion opportunity whose domestic supply preference for qualified U.S.-based chemical suppliers creates commercial motivation for domestic production investment above that which import reliance would justify.

Spent acid recycling and purification services represent an emerging circular economy opportunity whose sustainability credential creates cost reduction and regulatory compliance value for semiconductor fabs seeking to reduce virgin acid consumption through validated regeneration chemistry that meets re-use specification requirements.

Recent Developments:

-

2025: Entegris expanded its electronic grade sulfuric acid supply capacity at its Burnet, Texas facility in 2025, establishing long-term supply agreements with CHIPS Act-funded U.S. semiconductor fabs including TSMC Arizona for ultra-pure acid meeting below-3nm node specifications.

-

2024: Stella Chemifa expanded its electronic grade sulfuric acid production at its Osaka facility in 2024 with a new ultra-purification line achieving sub-ppt metallic impurity levels for leading-edge below-3nm semiconductor fabrication.

-

2024: KMG Chemicals (Entegris) expanded its electronic grade wet chemicals portfolio in 2024 with new ppb-grade sulfuric acid formulations for 5G PCB fabrication and advanced packaging applications, targeting the growing high-density interconnect PCB market.

-

2024: Honeywell Advanced Materials launched enhanced electronic grade sulfuric acid supply services in 2024 with new purity certification documentation protocols supporting CHIPS Act-funded customer qualification requirements at U.S. domestic semiconductor fabs.

-

2023: Mitsubishi Chemical Holdings expanded its electronic grade sulfuric acid production capacity in Japan in 2023, targeting growing Asian semiconductor fab procurement as Samsung, SK Hynix, and domestic Japanese fabs expanded leading-edge production capacity.

Electronic Grade Sulfuric Acid Market Key Players:

-

BASF SE

-

Dow Chemical Company

-

DuPont de Nemours, Inc.

-

Honeywell International Inc.

-

Nouryon

-

INEOS Group Holdings S.A.

-

KMG Chemicals (now part of Asahi/AZ-like chemical assets in some regions)

-

Chemtrade Logistics Inc.

-

Kanto Chemical Co., Inc.

-

Linde plc

-

PVS Chemicals Inc.

-

Merck KGaA

-

Mitsubishi Chemical Corporation

-

Asia Union Electronic Chemical Corp.

-

Chung Hwa Chemical Industrial Works, Ltd.

-

Moses Lake Industries Inc.

-

LANXESS AG

-

Fujifilm Holdings Corporation

-

Solvay S.A.

-

Tata Chemicals Limited

Electronic Grade Sulfuric Acid Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 390.60 Million |

| Market Size by 2035 | USD 697.20 Million |

| CAGR | CAGR of 5.96% from 2026–2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Grade (Parts per trillion (ppt), Parts per billion (ppb)) • By Application (Semiconductors, PCB Panels, Pharmaceuticals) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | BASF SE, Dow Chemical Company, DuPont de Nemours, Inc., Honeywell International Inc., Nouryon, INEOS Group Holdings S.A., KMG Chemicals (now part of Asahi/AZ-like chemical assets in some regions), Chemtrade Logistics Inc., Kanto Chemical Co., Inc., Linde plc, PVS Chemicals Inc., Merck KGaA, Mitsubishi Chemical Corporation, Asia Union Electronic Chemical Corp., Chung Hwa Chemical Industrial Works, Ltd., Moses Lake Industries Inc., LANXESS AG, Fujifilm Holdings Corporation, Solvay S.A., Tata Chemicals Limited |

Frequently Asked Questions

The Electronic Grade Sulfuric Acid Market is expected to grow at a CAGR of 5.96% from 2026 to 2035.

The Electronic Grade Sulfuric Acid Market was valued at USD 390.60 Million in 2025.

Global semiconductor fab capacity expansion driving structured electronic grade sulfuric acid procurement and CHIPS Act-funded U.S. domestic fab investments accelerating ultra-high-purity process chemical demand.

Parts per Billion (ppb) dominated the Electronic Grade Sulfuric Acid Market in 2025, while the Parts per Trillion (ppt) segment is the fastest growing.

Asia Pacific dominated the Electronic Grade Sulfuric Acid Market with approximately 58% of revenues in 2025, while North America is the fastest-growing region.

Get in Touch