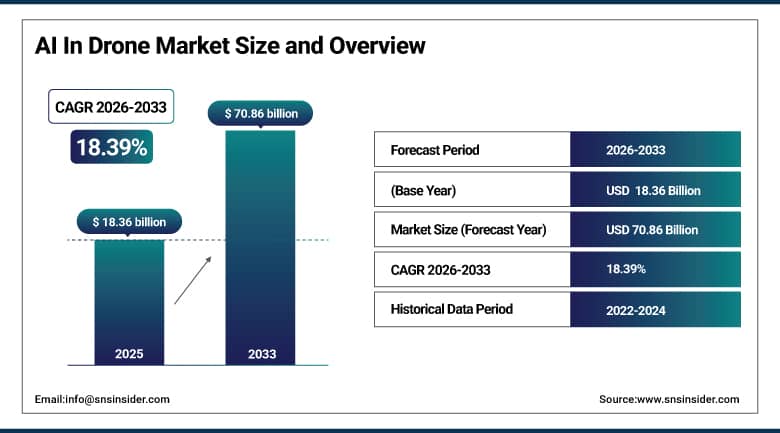

AI In Drone Market Report Scope & Overview:

The AI In Drone Market is valued at USD 18.36 Billion in 2025E and is expected to reach USD 70.86 Billion by 2033, growing at a CAGR of 18.39% during 2026-2033.

AI In Drone Market is driven by improvements in autonomous navigation, computer vision, and machine learning, which let drones do complicated jobs without help from people. Demand is rising due to key uses in agriculture, surveillance, delivery, and industrial inspection, and improvements in regulations and reducing hardware costs. AI integration improves real-time data analysis, avoiding obstacles, and operational efficiency, making drones necessary in business, government, and military settings globally.

81% of commercial drone operators implemented AI-driven autonomy for tasks, such as crop monitoring and infrastructure inspection, increasing operational efficiency by 45% and reducing manual intervention by 60% in 2025.

AI In Drone Market Size and Forecast:

-

Market Size in 2025E: USD 18.36 Billion

-

Market Size by 2033: USD 70.86 Billion

-

CAGR: 18.39% from 2026 to 2033

-

Base Year: 2025E

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get More Information On AI In Drone Market - Request Free Sample Report

AI In Drone Market Trends:

-

Increasing adoption of autonomous drone swarms for large-scale agriculture, disaster management, and security surveillance leveraging collaborative AI and real-time data fusion.

-

Rising integration of AI-powered computer vision for precision tasks such as crop health analysis, structural defect detection, and automated inventory management.

-

Growing deployment of beyond-visual-line-of-sight (BVLOS) drones enabled by AI for navigation and regulatory compliance in delivery and industrial applications.

-

Expansion of edge AI processors in drones for real-time onboard data processing, reducing latency and bandwidth dependency during missions.

-

Increasing use of predictive maintenance and AI analytics to optimize drone fleet operations, battery life, and mission planning across sectors.

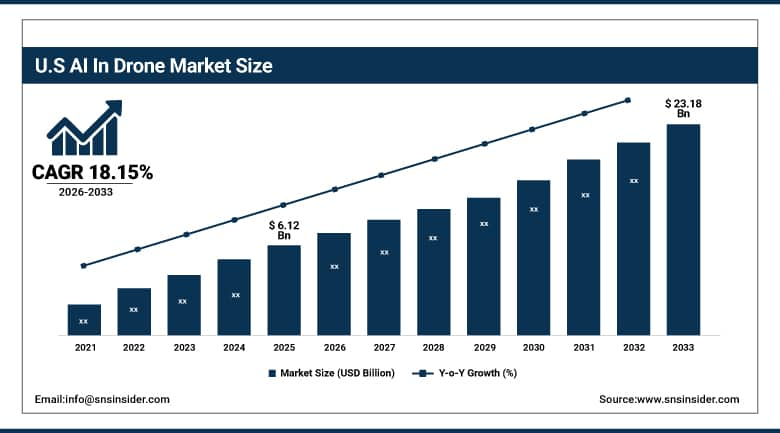

The U.S. AI In Drone Market is valued at USD 6.12 Billion in 2025E and is expected to reach USD 23.18 Billion by 2033, growing at a CAGR of 18.15% during 2026-2033.

U.S. AI In Drone Market is expanding owing to the strict defense investments, FAA regulatory advancements for BVLOS operations, and large adoption in agriculture, logistics, and public safety globally. Leading tech firms and drone manufacturers are integrating AI for fully autonomous systems, driving innovation and market expansion across commercial and government sectors.

AI In Drone Market Growth Drivers:

-

Advancements in AI Algorithms for Autonomous Navigation and Real-Time Decision-Making are Accelerating Drone Adoption across Different Applications Globally

Drones can now fly on their own in changing surroundings thanks to advances in machine learning, sensor fusion, and path-planning algorithms. AI lets drones do complicated jobs, such as spraying crops, delivering packages, and checking infrastructure with very little help from people. These features cut down on operational costs, make things more accurate, and make it possible to deploy them on a larger scale. The need for data-driven insights and efficiency in many fields is driving investments in AI drone technology. This is making autonomy a key driver of growth in the market.

77% of agricultural enterprises adopted AI drones for precision farming in 2025, improving crop yield by 30% and reducing chemical usage by 25% through targeted AI-based spraying and monitoring.

AI In Drone Market Restraints:

-

High Initial Costs of AI-Integrated Drone Systems and Limited ROI Clarity for Small Enterprises Hinder Widespread Adoption across Price-Sensitive Markets

Drones with AI need more modern sensors, processors, and software, which makes them much more expensive than regular drones. Small and medium-sized businesses, especially in developing areas, have trouble with their budgets and aren't sure if they'll receive their money back, which slows down adoption. The necessity for specialized training and integration with existing IT systems also raises the total cost of ownership, making it hard for non-industrial customers to justify spending money, which slows market penetration.

65% of SMEs deferred AI drone investments in 2025 due to high upfront costs exceeding USD 15,000 per unit and unclear long-term operational benefits in competitive markets.

AI In Drone Market Opportunities:

-

Expansion of AI Drone Applications in Precision Agriculture, Smart Cities, and Renewable Energy Inspection Offers Substantial Growth Potential in Emerging Economies

Emerging markets in Asia, Africa, and Latin America are increasingly adopting AI drones for agricultural optimization, urban planning, and infrastructure monitoring. Governments are promoting smart farming and digital infrastructure projects, creating demand for cost-effective drone solutions. AI capabilities such as multispectral imaging and predictive analytics enable smallholder farmers and city planners to improve productivity and resource management, opening new revenue streams for drone manufacturers and service providers.

In 2025, AI drone adoption in emerging economies grew by 55%, driven by government subsidies for precision agriculture and smart city projects, creating a USD 4.2 billion opportunity.

AI In Drone Market Segment Highlights:

-

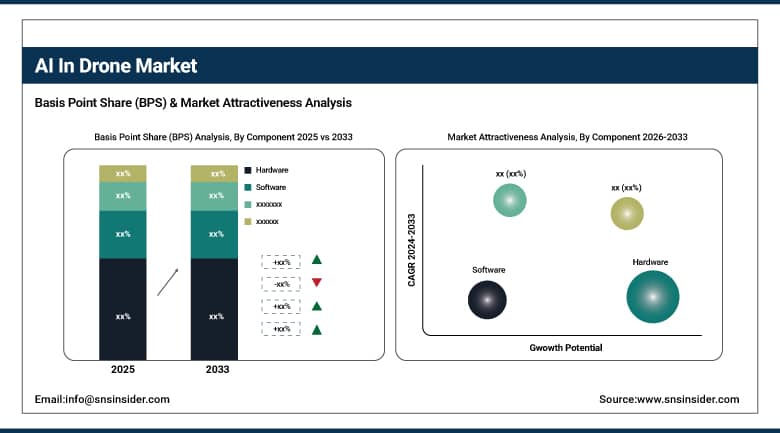

By Component: Hardware led with 48.5% share, while Software is the fastest-growing segment with CAGR of 22.1%.

-

By Application: Security & Surveillance led with 26.3% share, while Agriculture is the fastest-growing segment with CAGR of 24.8%.

-

By Type: Cloud Based led with 53.7% share, while Station Based is the fastest-growing segment with CAGR of 19.5%.

-

By End-Use: Commercial led with 41.2% share, while Government is the fastest-growing segment with CAGR of 20.3%.

AI In Drone Market Segment Analysis

By Component: Hardware Segment Led the Market, while Software is the Fastest-growing Segment Globally

Hardware dominates AI in drone market due to the essential need for advanced processors, sensors, cameras, and communication modules that enable autonomous functionality. The increasing complexity of applications in mapping, inspection, and delivery drives continuous innovation and investment in drone hardware, making it the largest revenue-generating component in the market.

Software is the fastest-growing segment as AI algorithms, machine learning models, and fleet management platforms become critical for drone autonomy and data analytics. The shift toward subscription-based software services, frequent updates for regulatory compliance, and the need for customizable applications across industries accelerate software adoption and revenue growth.

By Application: Security & Surveillance Segment Led, while Agriculture is the Fastest-growing Segment in the Market Globally

Security & Surveillance leads due to rising demand for perimeter monitoring, crowd management, and threat detection in both public and private sectors. Increased defense spending and homeland security initiatives worldwide further solidify this segment's dominant market position.

Agriculture is the fastest-growing application as farmers adopt AI drones for precision farming, crop health monitoring, and automated spraying. Government subsidies, growing global food demand, and technological affordability drive rapid adoption across North America, Europe, and Asia-Pacific, making agriculture a high-growth segment.

By Type: Cloud Based Dominated the Market, while Station Based is the Fastest-growing Segment Globally

Cloud Based systems lead due to advantages in data storage, processing scalability, and collaborative analytics. This is particularly valuable for applications, such as large-scale mapping, disaster response, and infrastructure inspection where data volume is high and insights need to be centralized and accessible from multiple locations.

Station Based (Edge/On-premise) is the fastest-growing type as industries with data sensitivity or remote operations require real-time processing without cloud dependency. Growth is driven by military applications, offshore inspections, and remote industrial sites where data security and immediate decision-making are critical.

By End-Use: Commercial Segment Led the Market, while Government is the Fastest-growing Segment in the Market Globally

Commercial end-use leads the market due to widespread adoption in agriculture, construction, logistics, and media. Businesses leverage AI drones to reduce operational costs, improve safety, and gather actionable insights. The scalability of drone solutions, combined with proven ROI in sectors, such as mining, insurance, and real estate, ensures continued commercial dominance.

Government is the fastest-growing end-use segment driven by increasing investments in smart city projects, border surveillance, disaster management, and public safety. Federal and municipal agencies deploy AI drones for tasks, such as traffic monitoring, search and rescue, and environmental monitoring.

AI In Drone Market Regional Analysis:

North America AI In Drone Market Insights:

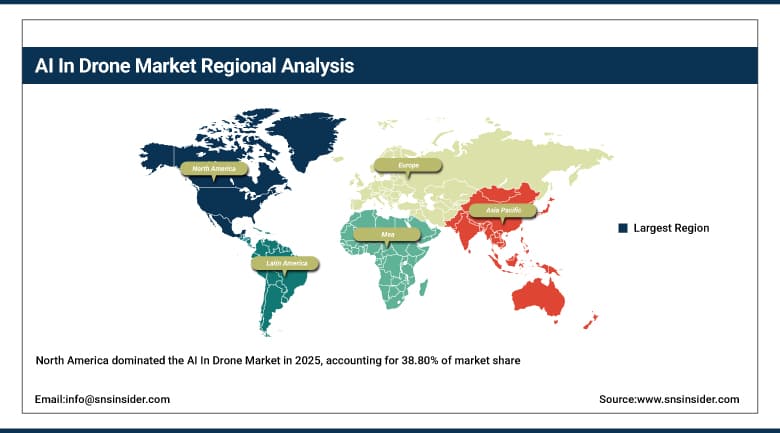

With a 38.80% market share in 2025, North America led the AI drone industry due to robust defense contracts, centers of technological research, and progressive FAA regulations. High adoption in the oil and gas, logistics, and agriculture industries, along with investments from top IT firms, strengthens the region's market dominance and promotes ongoing research and development of autonomous drone systems.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific AI In Drone Market Insights:

Asia Pacific is expected to grow at the fastest CAGR of about 21.50% over 2026–2033, driven by massive agricultural modernization, government smart city initiatives, and expanding industrial automation in China, India, and Japan. AI drone usage in precision farming, infrastructure, and e-commerce delivery is accelerated in the region by growing local manufacturing, falling sensor costs, and supporting UAV regulations.

Europe AI In Drone Market Insights:

Due to strict safety laws, robust industrial automation trends, and EU-funded drone technology innovation projects, Europe held a sizable share of the AI in Drone Market in 2025. Europe's competitive position is strengthened by the region's emphasis on environmental monitoring, renewable energy, and public safety applications, as well as joint ventures between aerospace companies and AI startups.

Middle East & Africa and Latin America AI In Drone Market Insights:

Together, the Middle East & Africa and Latin America demonstrated consistent growth in the AI drone market in 2025 due to government spending in border security and disaster relief, the expansion of agriculture, and the need for oil and gas inspections. Market expansion in these developing areas is supported by growing alliances with international drone suppliers and slow regulatory changes.

AI In Drone Market Competitive Landscape:

DJI

Founded in 2006, DJI is a Chinese technology giant and the global leader in civilian drones and aerial imaging systems. The company dominates the commercial and consumer drone markets with advanced AI features like ActiveTrack, obstacle sensing, and automated flight modes. DJI continuously integrates machine learning for photography, surveying, and industrial inspections, serving sectors from agriculture to filmmaking worldwide.

-

January 2025, DJI launched its next-generation Agras T50 AI agricultural drone with enhanced swarm intelligence and precision spraying algorithms, boosting farm automation capabilities.

Skydio

Established in 2014, Skydio is a U.S.-based autonomous drone pioneer known for its AI-driven obstacle avoidance and computer vision technology. The company focuses on enterprise and government markets, offering drones that navigate complex environments without GPS. Skydio's AI platform enables applications in infrastructure inspection, public safety, and defense, emphasizing autonomy and reliability.

-

March 2025, Skydio released its X10D model for defense and enterprise, featuring advanced AI for reconnaissance and real-time 3D mapping in GPS-denied environments.

Parrot SA

Founded in 1994, Parrot SA is a French drone and wireless products manufacturer with a strong focus on professional and commercial AI drone solutions. The company offers AI-enhanced drones for agriculture, mapping, and surveillance, leveraging computer vision and data analytics. Parrot also provides software tools for fleet management and geospatial analysis, serving sectors like construction, forestry, and security.

-

November 2024, Parrot launched its ANAFI AI drone with 4G connectivity and AI-powered analytics for real-time site monitoring and automated reporting in construction and energy sectors.

AI In Drone Market Key Players:

-

DJI

-

Parrot SA

-

Intel Corporation (Ascending Technologies)

-

Autel Robotics

-

EHang Holdings Limited

-

Kespry Inc.

-

PrecisionHawk Inc.

-

AeroVironment, Inc.

-

Flyability SA

-

Shark Robotics

-

Iris Automation Inc.

-

Skyfront Inc.

-

AgEagle Aerial Systems Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025E | USD 18.36 Billion |

| Market Size by 2033 | USD 70.86 Billion |

| CAGR | CAGR of 18.39 % From 2026 to 2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Application (Retail, Construction, Agriculture, Search and Rescue, Security & Surveillance, Others) • By Type (Station Based, Cloud Based) • By End-Use (Government, Commercial, Military) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | DJI, Skydio, Parrot SA, Intel Corporation (Ascending Technologies), Autel Robotics, EHang Holdings Limited, Kespry Inc., PrecisionHawk Inc., AeroVironment, Inc., Flyability SA, Percepto Ltd., Shark Robotics, Iris Automation Inc., Skyfront Inc., AgEagle Aerial Systems Inc. |

Frequently Asked Questions

Ans- North America region dominated the AI In Drone Market with 36% of revenue share in 2024.

Ans- The Security & Surveillance segment dominated the AI in drone market in 2024 and accounted for a significant revenue share.

Ans- Growing Need for Autonomous Operations Leads to Increased Adoption of AI-Powered Drones in Surveillance, Agriculture, and Logistics

Ans- The AI in drone market size was valued at USD 13.1 billion in 2024 and is expected to reach USD 50.5 billion by 2032

Ans- The expected CAGR of the AI In Drone Market over 2025-2032 is 18.39%.

Get in Touch