Air Deflector Market Report Scope & Overview:

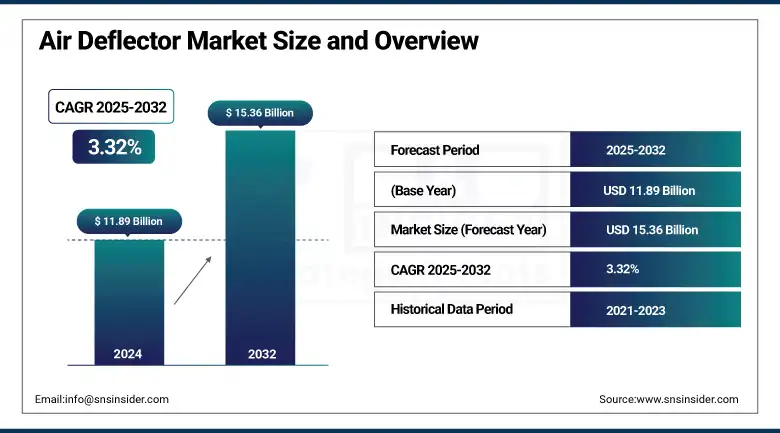

The air deflector market size was valued at USD 11.89 billion in 2024 and is expected to reach USD 15.36 billion by 2032, growing at a CAGR of 3.32% over the forecast period of 2025-2032.

The air deflector market trends are associated with aerodynamic optimization, the use of lightweight materials, and improved fuel efficiency of vehicles. In the developing region, this market is driven by increasing demand from both OEM and aftermarket segments. The integration of smart deflectors compatible with sensors and sustainable composites is leveraging technological innovation.

The analysis of the air deflector market is segmented in terms of the deployment in commercial vehicles, owing to the growing need for enhanced fuel efficiency as per government mandates, whereas in passenger vehicles, the revenue-generating opportunities are driven by consumer preferences toward design customization and aesthetic appeal. Since, largest air deflector market share is held by the ones based in Asia-Pacific, the manufacturers are planning to expand their operations on a regional basis. At the same time, globally, product trends are being reformulated as regions address sustainability and aesthetic improvements.

To Get more information On Air Deflector Market - Request Free Sample Report

“For instance, in May 2024, Piedmont Plastics innovates plastic manufacturing technology, increasing precision and efficiency of material supports innovation in the air deflector, supporting performance, durability, and sustainability for automotive components.”

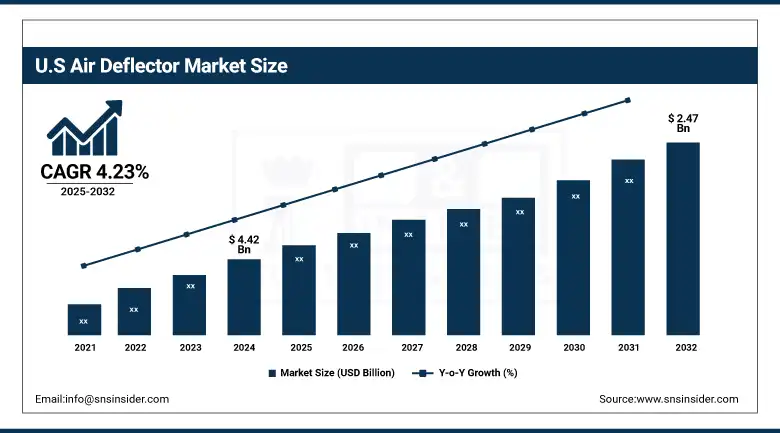

The U.S. air deflector market size was valued at USD 4.42 billion in 2024 and is expected to reach USD 2.47 billion by 2032, growing at a CAGR of 4.23% over the forecast period of 2025-2032.

The U.S. air deflector market is growing steadily due to increasing classy car configurations and wind flow functional domain requests. Demand for air deflector market analysis is increasing day by day across SUVs and trucks, owing to a substantial aftermarket trend. The Air Deflector market growth is attributed to improved design, fuel economy, and consumer preference for cosmetic upgrades.

Air Deflector Market Dynamics:

Drivers:

-

Rising Focus on Aerodynamic Efficiency and Fuel Economy Drives Installation of Air Deflectors in Modern Vehicle Designs

With increasing global emission regulations, automakers are adopting air deflectors to improve the aerodynamic efficiency of vehicles, which will reduce drag and increase fuel economy. This makes for enhanced air flow, which allows for a more comfortable ride and less fuel use, especially with SUVs and trucks. At the same time, increasing demand for energy-efficient solutions in the automotive sector has made air deflectors a design element found in most of the newly designed cars. This transition not only helps sustainability objectives but also improves car design and efficiency. Consequently, manufacturers are reaping the benefits from these factors, which is another reason or aspect enhancing the air deflector market growth among developed and developing automotive markets.

-

Growing Demand for Eco-Friendly Products in Various Industries Boosts the Air Deflector Market Growth

As climate change awareness increases, manufacturers are using recyclable and lightweight materials, such as ABS and acrylic for air deflector. These green materials are lightweight, which contributes to better mileage and fewer emissions. Similarly, the need for eco-friendly product solutions demanded by both regulatory pressure and green consumerism is encouraging automakers and aftermarket providers to innovate. Based on such sustainable initiatives, stakeholders are focusing on R&D about the manufacturing of high-performance recyclable deflectors fulfilling functionality and environmental standards, thereby promoting sustainable demand across the passenger cars and commercial vehicle segments, impacting the overall air deflector market trends in the long term.

Restraints:

-

Limited Awareness in Emerging Economies Slows Adoption of Advanced Air Deflector Solutions in Entry-Level Vehicle Segments

The awareness toward the benefits of air deflectors, such as aerodynamic and fuel savings, is less in developing regions, which will negatively impact the market in entry-level vehicle segments. It creates a barrier to mass adoption and slows down time to market. Locally, most buyers prefer the must-haves for their vehicles and overlook aerodynamic tweaks on the whole, often viewing deflectors as optional rather than functional. In addition, there were hardly any marketing campaigns and poor training of the dealer network, leading to an overall low level of product visibility. As cited in the last air deflector market analysis, the gap still limits the scope of expansion in rural and semi-urban markets, with cost-sensitive consumers steering purchasing decisions.

Air Deflector Market Segmentation Outlook:

By Type

The air deflector market by type was led by the window deflector segment with a revenue share of approximately 46.59% in 2024, as its demand is high in both OEM and aftermarket, particularly in passenger cars. They allow for ventilation, but cut down on the rain and wind noise while driving. These provide low-cost, easy installation, and functional utility, which is well accepted by the consumer. Also, stable demand irrespective of geographical conditions has enabled them to hold on to the dominance in the market, reaffirming fundamental air deflector market insights and buffer consumer preference.

The bug deflector segment is projected to witness a significant CAGR of monotonous 3.67%, owing to the growing demand for bug deflector within the bug deflector for off-road and commercial vehicles. Bug deflectors are becoming an increasingly popular aftermarket accessory as vehicle owners look to add protection to hoods and windshields against the negative effects of insects and road debris. The trend is confirmed by their increasing use in North American and Australian trucks and SUVs. Growing aftermarket customization and emphasis on the Vehicle Air Management Systems, incorporating bug deflectors, are driving their adoption.

By Material

The air deflector market was led by the acrylic segment in terms of revenue contribution in 2024, as it is lightweight, durable, and cost-effective. It has a high level of transparency, sweat-resistance, and is easy to make, another common choice made by manufacturers and consumers alike. The product supports mass customization and ensures OEMs and aftermarket applications. Its ingress will be improved by the constant ability to enhance the stability of the structure, where it performs exceptionally well under different climatic conditions, which is a sharp match with practicality in consumer requirements, and trends for the market.

The ABS segment is projected to flourish during the forecast period over 2025–2032, owing to increased toughness and better impact resistance, thereby driving the growth of the impact modifiers market within this segment. With the evolution of modern vehicles, the manufacturers are more inclined toward materials that are strong as well as lightweight, and ABS comes to this balance. Its application is further driven by the growing requirement for style and integrated dainty deflectors, particularly in the luxury car segment. Moreover, developments, such as those of air deflectors companies to target sustainable and eco-sensitive consumers are in alignment with the sustainability goals, as they support the overall recyclability of ABS.

By Vehicle Type

The Passenger Cars segment held the largest revenue share of over 55% in the air deflector market in 2024, as the sales volume of passenger vehicles in the world is huge in comparison to other categories of vehicles. Air deflectors have been adopted in sedans and SUVs to help with the comforts of aerodynamics and customer personalization. It is seen that the more consumer interest in noise reduction combined with energy efficiency, has also further encouraged us to use it. Furthermore, factory-fitted and aftermarket options have made air deflectors more accessible, reinforcing the dominance of the passenger car segment in the new air deflector market analysis.

The LCV (Light Commercial Vehicle) segment is projected to register the highest CAGR during 2025–2032, owing to the rising logistics and last-mile delivery market. The demand for air deflectors by operators of LCVs is continuously rising, as it helps to lower the operational cost of LCVs and improve fuel efficiency. Growing aftermarket desirability for aerodynamic elements and practical enhancements in vans and pickups is increasing demand. With fleet owners looking for ways to increase performance and mobility, LCV is likely to be a high-potential segment for air vent deflector.

By Mounting Method

Tape-on segment accounted for the highest revenue share in the air deflector market in 2024 due to its easy installation process and compatibility with a large number of vehicles. This means that it needs no drilling, which makes it less likely to harm the vehicle's external finishes, and targets both do-it-yourself consumers and aftermarket retailers. Tape-on deflectors have become a popular feature globally, mainly due to their cost-effectiveness and aesthetic appeal. According to market insights, the utility and aesthetic appeal have made this method of mounting a market leader.

The in-channel segment is projected to experience the fastest CAGR during 2025–2032, as it is easier to fit and combine scale design elements internally than outside to reduce detection and make the fit more secure. In-channel deflectors have been gaining traction as consumer favors shift toward minimalist, flush-mounted accessories. They are also capable of withstanding high-speed wind pressure without moving out of place, which makes them ideal for high-performance vehicles.

Air Deflector Market Regional Analysis:

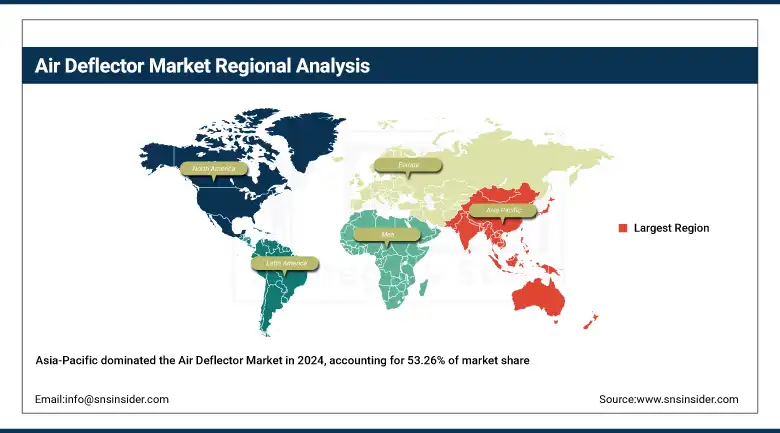

In 2024, Asia-Pacific accounted for the largest share of the market with approximately 53.26% revenue share owing to huge automotive production and sales volume of the region, especially China, Japan, and India. These factors, including rising customization demand, expansion of passenger and commercial vehicles demand, are significantly driving the market growth. Moreover, the high number of both OEMs and aftermarket players, along with the cost-effective manufacturing in the region, continues to bolster the region as a leader in this segment, backed by enabling regulations and evolving consumer preferences.

Get Customized Report as per Your Business Requirement - Enquiry Now

The North America region is estimated to witness a substantial compound annual growth rate (CAGR) of nearly 4.46% over 2025–2032, on the back of vast aftermarket trends coupled with the expansion of pickup and SUVs, and increasing necessity for aerodynamic enhancements. The North American buyers have a very high tendency to modify a vehicle for either performance or visual appeal. Established manufacturers, technological innovation, and expanding demand for fuel efficiency also propel adoption further within the North America region, making it one of the most lucrative prospects in the market.

The European air deflector market is driven by strict emission regulations and growing demand for vehicle efficiency. The latter accounts for the regional leadership of Germany thanks to its strong automotive manufacturing base. More recently, we've seen air deflectors with integrated sensors that optimize the performance of the smart vehicle. Increasing electric vehicle adoption and aerodynamic innovations are evolving the regional market.

Key Players in Air Deflector Market are:

The major players operating in the market are Lund International, Climair UK Ltd, Piedmont Plastics, Magna International Inc., WeatherTech, AVS (Auto Ventshade), Stampede Automotive Accessories, TROX, Heko, and Airodyne Industries, Inc.

Recent Developments:

-

September 2023 - TROX UK launches the RFD-V Swirl Air Diffuser, enhancing airflow control and energy efficiency, advancing HVAC technology that parallels innovation trends influencing the broader market.

-

December 2023 - Comfort First Products launches HVAC vent diverters and deflectors to improve commercial airflow efficiency, enhancing occupant comfort and energy savings—contributing to innovation and growth in the market.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 11.89 Billion |

| Market Size by 2032 | USD 15.36 Billion |

| CAGR | CAGR of 3.32% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Window Deflector, Sunroof Deflector, Bug Deflector) • By Material (Acrylic, ABS, Fiberglass, Others) • By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)) • By Mounting Method (Tape-on, Bolt-on, In-channel) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Lund International, Climair UK Ltd, Piedmont Plastics, Magna International Inc., WeatherTech, AVS (Auto Ventshade), Stampede Automotive Accessories, TROX, Heko, Airodyne Industries, Inc. |

Frequently Asked Questions

Asia-Pacific dominated the air deflector market in 2024.

The Window Deflector segment dominated the air deflector market.

The major growth factor of the air deflector market is the rising demand for improved vehicle aerodynamics to enhance fuel efficiency and reduce emissions.

The air deflector market size was USD 11.89 billion in 2024 and is expected to reach USD 15.36 billion by 2032.

The air deflector market is expected to grow at a CAGR of 3.32% from 2024-2032.

Get in Touch