Construction Equipment Market Size & Overview:

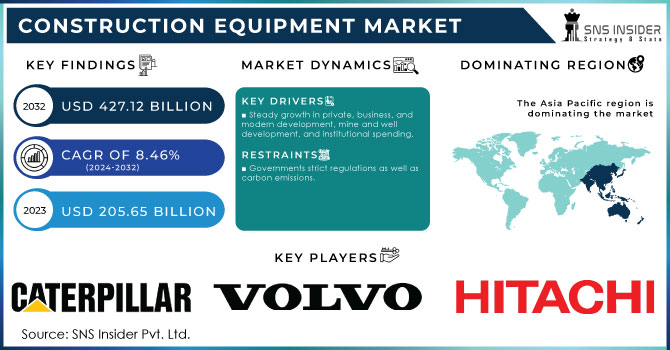

The Construction Equipment Market Size was valued at USD 179.37 billion in 2023 and is expected to reach at USD 345.08 billion by 2032 with a growing CAGR of 7.54% over the forecast period 2024-2032. This report provides a unique perspective on the Construction Equipment Market by analyzing regional output trends and utilization rates, offering insights into operational efficiency. It highlights maintenance and downtime metrics, addressing cost implications and fleet reliability. The study also examines technological adoption rates, such as AI-driven diagnostics and electrification trends, across key regions. Additionally, export/import data uncovers shifting trade dynamics. To enhance the analysis, the report includes automation in construction equipment, rental market penetration, and supply chain disruptions, providing a well-rounded view of the industry's evolving landscape.

To get more information on Construction Equipment Market - Request Free Sample Report

Construction Equipment Market Dynamics

Drivers

-

Rising infrastructure investments in roads, bridges, railways, and smart cities are driving demand for advanced, efficient, and technology-driven construction equipment.

The rising investments in infrastructure development, including roads, bridges, railways, and smart cities, are significantly boosting the demand for construction equipment. Across the world, especially in developing economies, governments are earmarking significant budgets to large infrastructure projects that are being pursued for better connectivity and urbanization. This tendency is fuelling the utilization of sophisticated construction equipment, like excavators, loaders, and cranes, in order to enhance the performance and decrease the duration of the projects. Furthermore, as the push towards developing smart cities continues, demand for technologically driven equipment such as IoT smart equipment and other autonomous machinery is on the rise. The construction equipment industry is experiencing consistent growth in demand across the world, driven by an increase in public-private partnerships and foreign direct investments into infrastructure. Several key trends are shaping the industry, including the adoption of electric/hybrid equipment, sustainability-driven innovations, and innovating construction processes through digitalization. The rise in infrastructure projects across the globe would market growth in forecasted period owing to high power output along with fuel efficient as well as automated construction equipment will drive market.

Restraint

-

High initial investment costs limit the adoption of advanced construction equipment, especially for small and mid-sized firms, due to financial constraints and additional operational expenses.

The high initial investment cost of advanced construction equipment poses a significant barrier to adoption, especially for small and mid-sized construction firms. Excavators, bulldozers, and cranes are all heavy machinery that is expensive and can put a shock to cash flow when purchasing them outright. Moreover, advanced equipment with automation, telematics and green engines compound upfront costs. Many smaller companies have difficulty making such investments because of intermittent project demands and inconsistent construction activity. In addition, financing options are available but often impose high interest rates and as such, ownership becomes more challenging. Thus, a lot of companies decide for rent or lease parts of equipment rather than buying, restricting general market development. On top of this financial burden are the added costs of maintenance, insurance and operator training. Small businesses struggle to compete with better-capitalized players in the industry, but large construction firms can swallow these costs.

Opportunities

-

The integration of IoT and telematics in construction equipment enhances efficiency, reduces downtime, lowers costs, and optimizes fleet management through real-time monitoring and predictive maintenance.

The integration of IoT and telematics in construction equipment is revolutionizing the industry by enhancing efficiency, safety, and cost-effectiveness. Smart or connected machinery, on the other hand, allows real-time monitoring of equipment performance, fuel consumption, and operational data for predictive maintenance and reduced downtime. Telematics solutions enable monitoring of equipment location, usage patterns, and wear-and-tear, optimizing fleet management and enhancing productivity. By avoiding costly surprise failures and reducing maintenance costs (both timeframe and expense), such technologies increase equipment longevity and reduce overall ownership costs. Moreover, automation powered by IoT improves remote diagnostics and operational control, enabling informed decisions and efficient resource utilization. Smart construction equipment is gaining traction and drawing lucrative investments due to the high demand to enhance efficiency and adhere to stringent regulatory standards. Furthermore, data analytics originating from IoT powered systems assist in preemptive planning, decreasing inefficiencies and promoting profitability. With digital transformation ti, the need for IoT-integrated construction equipment is likely to increase and drive innovation in the sector.

Challenges

-

Economic uncertainties, including inflation, geopolitical tensions, and market fluctuations, impact infrastructure investments, equipment demand, and overall industry growth.

Economic uncertainties pose a significant challenge to the construction equipment market, as fluctuations in global and regional economies directly impact infrastructure investments. Inflation is increasing the prices of raw materials, fuel and labor; all contributing to a higher cost for construction projects and reducing budget allocations for buying new equipment. And rising interest rates have made it more expensive to finance construction projects and heavy machinery, also putting demand on a tighter leash. Geopolitical tensions, trade restrictions, and supply chain disruptions introduce earnings volatility into equipment availability and pricing, exerting upward pressure on capital and operating costs for manufacturers and end-users alike. Movements in the market, such as economic downturns or declines in key industries like real estate and mining, can cause capital spending to decrease on large-scale construction projects. Cuts in government funding or delays with infrastructure programs because of economic instability further fuel market uncertainty. Hence, construction equipment manufacturers need to implement flexible strategies, such as cost optimization and diversification, to mitigate such economic challenges efficiently.

Construction Equipment Market Segmentation Analysis

By Product

The Material handling machinery segment dominated with a market share of over 38% in 2023. This segment comprises the cranes and the forklifts used in lifting, transporting, and placing heavy material at the construction sites. With the rise in the infrastructure development, rapid urbanization, and expanding commercial & industrial projects globally, the demand for material handling machinery is increasing. Equipment efficiency is aided by advancements in automation and smart technologies, in turn enabling adoption. Moreover, government investments in largescale construction projects, logistics, and warehousing have propelled the segment's dominance, firmly establishing it as a key driver of growth in the construction equipment market.

By Equipment Type

The Heavy Construction Equipment segment dominated with a market share of over 62% in 2023, due to its crucial role in large-scale infrastructure projects, mining operations, and commercial construction. From excavators to bulldozers and loaders, these machines are heavy-duty workhorses that are essential for applications such as earthmoving, material handling, and demolition. The demand for heavy equipment is further fueled by poll governments, investing in infrastructure development. Moreover, continuous technological developments like automation and telematics have further increased the efficiency and productivity of this segment leading to its continued dominance. The saga of prominent manufacturers makes it easier to proceed it and the increasing demand for durable, high-performance machinery fuels continuous growth. With construction activities worldwide, the heavy construction equipment segment is projected to continue its dominant position in the market.

By Propulsion Type

The ICE (Internal Combustion Engine) segment dominated with a market share of over 52% in 2023, due to its high-power output, durability, and ability to operate in demanding conditions. Diesel equipment is still the industry standard, offering higher efficiency, longer runtimes and the ability to perform heavy-duty applications in remote and off-grid locations. Its charging infrastructure is also widely implemented. ICE-powered machinery remains the preferred choice due to its reliability and cost-effectiveness even as environmental concerns rise. However, as stricter emissions regulations come into effect and alternative technologies advance, slowly-filling electric and hybrid construction equipment are projected to be on the rise over the following years.

By Power

The <100 HP segment dominated with a market share of over 34% in 2023, due to its extensive use in compact and highly versatile machinery such as mini excavators, skid-steer loaders, and backhoe loaders. These machines are found among urban construction, landscaping and small-scale infrastructure projects where their superior maneuverability is the requirement due to space constraints. Their lower fuel consumption and operational efficiency make them an ideal choice for contractors and businesses to cost-effective. Moreover, rising investments in smart cities and residential developments boost the demand for compact construction equipment. Moreover, the increasing trend towards electrification in this segment also makes it more attractive, as electric and hybrid models have lower emissions and lower operating costs, which appeals to global sustainability goals and stricter emissions regulations.

By Engine Capacity

The 250-500 HP segment holds a significant share due to its versatility and widespread application across key construction activities. This segment comprises formidable construction equipment, including excavators, bulldozers, loaders, and graders, which are crucial for large-scale infrastructure development, road construction, and material handling. The market for these machines is fueled by rising urbanization, government expenditure in infrastructure, and developing commercial and residential construction. And with new technologies such as better fuel economy, automation, and telematics integration only adding to the desirability of this segment. To improve the balance of power and efficiency at a solid 250-500 HP, this tier of machines continues to be the go-to for contractors needing dependable, well-engineered equipment for rugged construction operations.

Construction Equipment Market Regional Outlook

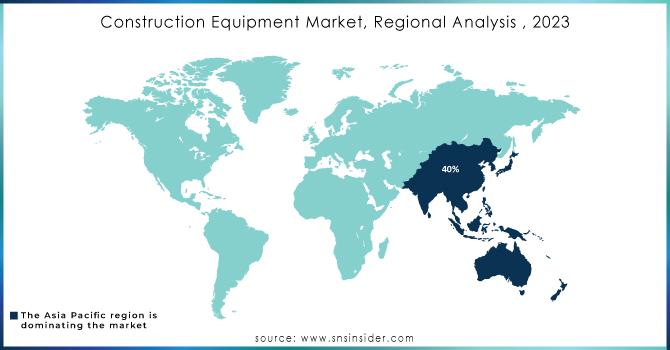

Asia-Pacific region dominated with a market share of over 44% in 2023, due to rapid urbanization, large-scale infrastructure projects, and increasing investments in the construction sector. Even countries like China, India, and Japan lead this segment as they fuel the growing demand for advanced machinery. The development of China's Belt and Road Initiative (BRI) and India's Smart Cities Mission has also played a crucial role in driving construction activities, thus further accelerating the growth of the market. Moreover, the domination of the region is due to initiatives taken by the government, the increasing foreign direct investments (FDI), and the developments in the real estate sector. Adoption of automation, intelligent construction technologies, and environmentally friendly equipment is growing, as well. As populations grow, urban housing needs expand and mega infrastructure projects are under construction, Asia-Pacific is once again the global leader in construction equipment.

North America is the fastest-growing region in the construction equipment market, driven by rising demand for advanced machinery and smart construction technologies. Adoption of automation, telematics, and electric powered equipment is growing across the region to promote efficiency and sustainability. Government initiatives, like the U.S. Infrastructure Investment and Jobs Act, are also spurring large-scale construction projects, from highways and bridges to smart cities. Moreover, emphasis on lowering carbon emissions is boosting the need for energy-efficient and eco-friendly devices. Moreover, the continuous technological progress and increasing presence of prominent industry participants further propel the growth of the market. North America is already in a position to see such booming expansion due to increased investments in residential, commercial, and industrial infrastructure across the region.

Need any customization research on Construction Equipment Market - Enquiry Now

Construction Equipment Market Companies are:

-

Hitachi Ltd.(Excavators, Loaders, Cranes)

-

AB Volvo (Wheel Loaders, Articulated Haulers, Excavators)

-

Caterpillar Inc. (Dozers, Excavators, Loaders, Motor Graders)

-

CNH Industrial N.V. (Backhoe Loaders, Skid Steer Loaders, Excavators)

-

Deere And Company (Excavators, Loaders, Scrapers, Backhoes)

-

Hyundai Doosan Infracore Co. Ltd. (Excavators, Wheel Loaders, Dump Trucks)

-

J C Bamford Excavators. Ltd (JCB) (Backhoe Loaders, Telehandlers, Excavators)

-

Komatsu Ltd. (Bulldozers, Dump Trucks, Hydraulic Excavators)

-

Liebherr-International Ag, (Tower Cranes, Loaders, Mining Trucks)

-

XCMG Group (Excavators, Road Rollers, Cranes)

-

Sany Group (Concrete Machinery, Piling Machinery, Cranes)

-

Terex Corporation (Aerial Work Platforms, Cranes, Material Handlers)

-

Zoomlion Heavy Industry Science & Technology Co. Ltd. (Excavators, Concrete Machinery, Cranes)

-

Manitou Group (Telehandlers, Forklifts, Aerial Work Platforms)

-

Kubota Corporation (Mini Excavators, Tractors, Compact Loaders)

-

Wirtgen Group (A John Deere Company) (Road Pavers, Cold Milling Machines, Compactors)

-

Tadano Ltd. (Mobile Cranes, Aerial Work Platforms)

-

Atlas Copco (Drilling Equipment, Compressors, Power Tools)

-

Schwing Stetter (Concrete Mixers, Batching Plants, Concrete Pumps)

-

Mahindra Construction Equipment (Backhoe Loaders, Earthmovers, Road Equipment)

Suppliers for (Excavators, bulldozers, loaders, and mining equipment) on Construction Equipment Market

-

Caterpillar (USA)

-

Komatsu (Japan)

-

John Deere (USA)

-

XCMG (China)

-

Sany (China)

-

Liebherr (Germany)

-

Volvo Construction Equipment (Sweden)

-

Hitachi Construction Machinery (Japan)

-

JCB (United Kingdom)

-

Doosan Bobcat (South Korea)

Recent Development

In May 2024: Volvo CE introduced the EC230, its largest electric excavator, at the Japan CSPI-Expo. This marked the first commercial launch of the EC230 Electric in Asia, with subsequent introductions planned for North America and select European markets.

In February 2024: Deere & Company (US) unveiled the 9RX tractor models, featuring an 830 HP option. The lineup includes three high-horsepower four-track models: 9RX 710, 9RX 770, and 9RX 830.

In November 2023: Komatsu Ltd., through its subsidiary Komatsu America Corp., announced the acquisition of American Battery Solutions, Inc., a U.S.-based battery manufacturer. This acquisition enables Komatsu Ltd. to develop and manufacture its own battery-powered mining and construction equipment by integrating advanced battery technology with its existing expertise.

In May 2023: Caterpillar Inc. introduced the upgraded Cat D10 Dozer, engineered for demanding construction environments and challenging job sites. The new model features load-sensing hydraulics and a stator clutch torque converter to enhance power transmission efficiency.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 179.37 Billion |

| Market Size by 2032 | USD 345.08 Billion |

| CAGR | CAGR of 7.54% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Products (Earth Moving Machinery (Excavators, Loaders, Dump Trucks, Moto Graders, Dozers), Material Handling Machinery (Crawler Cranes, Trailer Mounted Cranes, Truck Mounted Cranes, Forklift), Concrete and Road Construction Machinery (Concrete Mixer & Pavers, Construction Pumps, Others) •By Equipment Type (Heavy Construction Equipment, Compact Construction Equipment) •By Propulsion Type (ICE, Electric, CNG/LNG) •By Power (<100 HP, 101-200 HP, 201-400 HP, >401 HP) •By Engine Capacity (Up to 250 HP, 250-500 HP, More than 500 HP) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Hitachi Ltd., AB Volvo, Caterpillar Inc., CNH Industrial N.V., Deere & Company, Hyundai Doosan Infracore Co. Ltd., J C Bamford Excavators Ltd. (JCB), Komatsu Ltd., Liebherr-International AG, XCMG Group, Sany Group, Terex Corporation, Zoomlion Heavy Industry Science & Technology Co. Ltd., Manitou Group, Kubota Corporation, Wirtgen Group (A John Deere Company), Tadano Ltd., Atlas Copco, Schwing Stetter, Mahindra Construction Equipment. |

Frequently Asked Questions

Ans: Asia-Pacific dominated the Construction Equipment Market in 2023

Ans: The “Material handling machinery” segment dominated the Construction Equipment Market.

Ans: Rising infrastructure investments in roads, bridges, railways, and smart cities are driving demand for advanced, efficient, and technology-driven construction equipment.

Ans: The Construction Equipment Market was USD 179.37 billion in 2023 and is expected to reach USD 345.08 billion by 2032.

Ans: The Construction Equipment Market is expected to grow at a CAGR of 7.54% during 2024-2032.

Get in Touch