Aliphatic Hydrocarbon Market Report Scope & Overview:

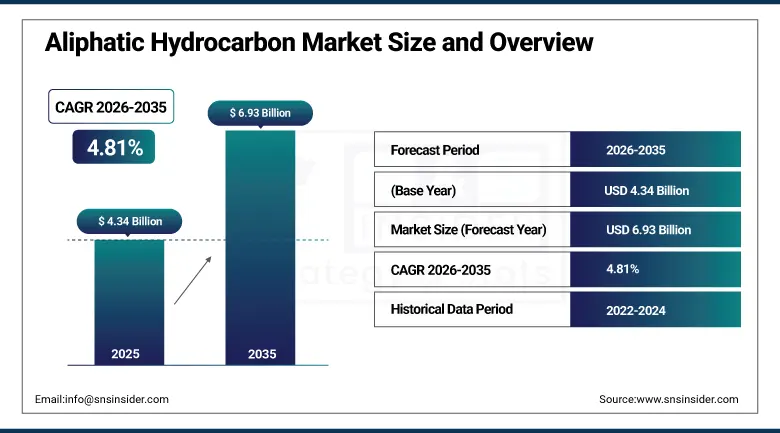

The Aliphatic Hydrocarbon Market was valued at USD 4.34 Billion in 2025 and is expected to reach USD 6.93 Billion by 2035, growing at a CAGR of 4.81% from 2026 to 2035.

Aliphatic hydrocarbon market growth is fuelled by the perfect fit that exists between the growing stringency of VOC emission standards globally and the properties of aliphatic hydrocarbon solvents that have less aromatic compounds and higher flash points than those of the older generation aromatic solvents, making them a better choice to meet the requirements of such regulations due to their lesser acutely toxic nature. Documentation by the European Solvent Industries Group of the growing trend of VOC solvent substitution in EU member countries coupled with VOC emission rules in the United States EPA and increasing VOC emission standards in China for industrial paints and adhesives provides constant regulatory pressure on aliphatic hydrocarbon substitution.

In August 2023, LyondellBasell launched new grades of its CirculenRecover range in North America, broadening the range of aliphatic hydrocarbon offerings in its portfolio that utilize recycled/recovered content sourced through advanced chemical recycling processes. The inclusion of the recycled/recovered feedstock in the range of products within the CirculenRecover range without any sacrifice in terms of purity, performance, and regulation compliance as expected by industrial coatings and adhesives producers from their aliphatic solvents suppliers shows the increasing economic feasibility of circular economy-based raw materials sourcing for the aliphatic hydrocarbon production process.

Market Size and Forecast

-

Market Size in 2026E: USD 4.55 Billion

-

Market Size by 2035: USD 6.93 Billion

-

CAGR: 4.81% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Aliphatic Hydrocarbon Market - Request Free Sample Report

Aliphatic Hydrocarbon Market Trends

-

Low-VOC and dearomatized aliphatic hydrocarbon solvents are gaining popularity as industries shift toward environmentally compliant and low-emission formulations.

-

Bio-based aliphatic hydrocarbons are emerging as sustainable alternatives, driven by renewable feedstocks and growing demand for greener chemical solutions.

-

High-purity aliphatic hydrocarbon grades are witnessing increased adoption in pharmaceutical, personal care, and food-contact applications due to stringent quality standards.

-

Chemical recycling and circular economy initiatives are creating sustainable hydrocarbon feedstock sources and supporting environmentally responsible production.

-

New applications in lithium-ion batteries and fuel cell technologies are expanding demand for high-purity aliphatic hydrocarbons beyond traditional industrial uses.

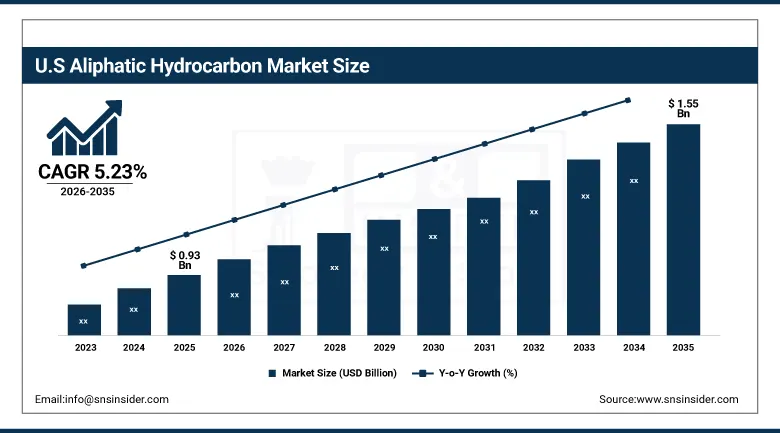

The U.S. Aliphatic Hydrocarbon Market Outlook

The U.S. Aliphatic Hydrocarbon Market was valued at approximately USD 0.93 Billion in 2025 and is expected to reach approximately USD 1.55 Billion by 2035, growing at a CAGR of approximately 5.23%.

The United States aliphatic hydrocarbon market benefits from the world's most advanced petroleum refining infrastructure, whose deep conversion refinery capacity and de-aromatization technology sophistication enable cost-competitive production of the high-purity aliphatic solvent grades that premium coating, adhesive, and personal care formulation applications demand. The U.S. EPA's VOC emission regulations for architectural and industrial maintenance coatings, whose progressively tightening limits have driven formulation transitions away from aromatic and high-VOC solvents toward aliphatic alternatives, represent the most commercially significant single regulatory driver of domestic aliphatic hydrocarbon demand growth over the past two decades. The U.S. construction industry's large scale, whose combined residential and non-residential activity creates the world's largest domestic market for architectural and protective coatings, sustains the most commercially important single end-use application for aliphatic hydrocarbon solvents in the domestic market.

In June 2023, Henkel erected a new adhesive technologies manufacturing facility at Yantai Chemical Industry Park in China at an investment of approximately EUR 135 million, expanding production and supply capability for adhesives in the Asia Pacific market. Henkel's adhesive formulations across construction, industrial, and consumer applications utilise aliphatic hydrocarbon solvents as carriers and diluents whose consumption scales with adhesive production volume, creating indirect demand for aliphatic hydrocarbons from adhesive manufacturer capacity expansion investments that signal growing regional aliphatic solvent demand aligned with adhesive market growth in rapidly industrialising economies.

Aliphatic Hydrocarbon Market Segment Analysis

-

By Type, saturated aliphatic hydrocarbons dominated the market with approximately 64% share in 2025, while cyclic aliphatic hydrocarbons serve growing specialty chemical synthesis applications.

-

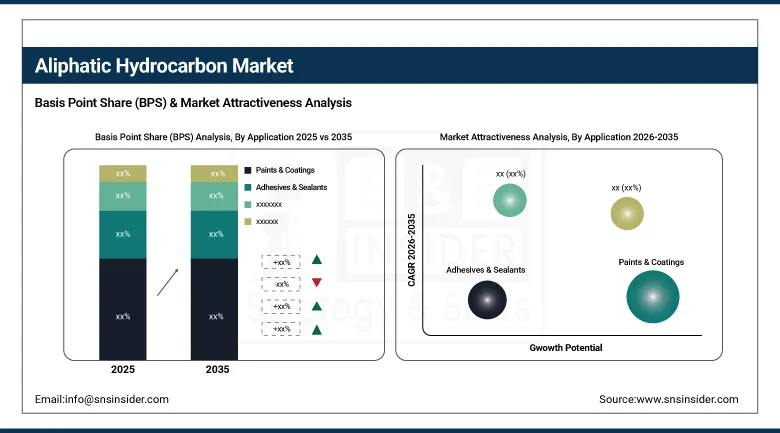

By Application, paints & coatings dominated the Aliphatic Hydrocarbon market with approximately 34.22% share in 2025, while the adhesives & sealants segment is the fastest growing application during 2026 to 2035.

-

By End Use, the industrial segment dominated the Aliphatic Hydrocarbon market in 2025, while the construction end use is the fastest growing during 2026 to 2035.

By Type, saturated hydrocarbons dominate, unsaturated aliphatic hydrocarbon is expected to grow fastest

Saturated aliphatic hydrocarbons generated approximately 64% of market revenue in 2025, reflecting their commercial dominance across the broadest range of solvent, diluent, and process aid applications whose performance requirements favour the chemical stability, low reactivity, and predictable evaporation profile of alkane-based solvent systems. Saturated aliphatic hydrocarbons' regulatory advantage over aromatic alternatives, including lower carcinogenicity classification, lower photochemical ozone creation potential, and greater compatibility with tight VOC compliance requirements, has progressively strengthened their market position as environmental and occupational health regulations in major markets have raised barriers to aromatic solvent use in consumer-facing and workplace applications. Mineral spirits, naphtha fractions, and high-purity dearomatized solvent grades collectively constitute the commercial heart of the saturated aliphatic hydrocarbon market whose diverse product grades address application requirements spanning from commodity cleaning solvent to ultra-high-purity pharmaceutical excipient.

Unsaturated aliphatic hydrocarbons, encompassing alkene and alkyne derivatives, serve chemical intermediate applications in organic synthesis, polymer production, and specialty chemical manufacturing whose technical performance requirements for reactive double bond functionality cannot be served by saturated alternatives. Cyclic aliphatic hydrocarbons including cyclohexane and its derivatives serve important industrial solvent and chemical synthesis applications, particularly in nylon precursor production and pharmaceutical intermediate synthesis, where their non-aromatic cyclic structure provides specific solvency and reactivity characteristics distinct from both linear saturated and aromatic alternatives.

By Application, paints & coatings dominate, adhesives & sealants grow fastest

Paints and coatings generated approximately 34.22% of aliphatic hydrocarbon market revenue in 2025, reflecting the dominant position of coating formulation as the single largest volume end-use category for aliphatic solvent consumption globally. Aliphatic hydrocarbon solvents serve as essential diluents and carriers in alkyd, epoxy, polyurethane, and acrylic coating systems whose application viscosity, drying time, levelling behaviour, and film formation characteristics are significantly influenced by solvent selection whose VOC content, evaporation rate, and solvency power must be balanced within tightening regulatory and performance constraints. The construction industry's architectural coating demand, the automotive industry's refinishing and OEM coating demand, and the industrial infrastructure's protective coating demand collectively create the diversified end-use base that sustains paints and coatings as the most commercially significant aliphatic hydrocarbon application category through the forecast period.

Adhesives and sealants are growing fastest as construction activity expansion across rapidly developing Asian and Middle Eastern economies creates growing demand for solvent-borne construction adhesives and sealants whose aliphatic hydrocarbon carrier systems are preferred over aromatic alternatives for indoor use applications. The automotive industry's expanding adhesive bonding application in lightweight body construction, where structural adhesives increasingly supplement or replace spot welding across aluminium and composite multi-material body assemblies, creates growing technical demand for aliphatic solvent-based adhesive systems whose low aromatic content satisfies automotive OEM indoor air quality standards for new vehicle interiors.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

42.84% |

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Middle East & Africa |

Saudi Arabia |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Aliphatic Hydrocarbon Market Insights

North America held a significant share of global aliphatic hydrocarbon revenues in 2025, supported by advanced refining capacity, stable crude oil supply, and stringent regulations that favour low-VOC and eco-friendly solvents. The United States accounts for approximately 82.47% of regional revenue through its large paints and coatings market, substantial adhesives and sealants industry, and petroleum refining infrastructure whose de-aromatization technology capability enables cost-competitive production of high-purity aliphatic solvent grades. The U.S. market's regulatory environment favouring low-aromatic, low-VOC solvents creates a structural commercial advantage for aliphatic hydrocarbon suppliers whose product portfolios address compliance requirements that aromatic alternatives cannot satisfy.

Europe Aliphatic Hydrocarbon Market Insights

Europe held a significant share of global aliphatic hydrocarbon revenues in 2025. Germany, France, the United Kingdom, the Netherlands, and Belgium are the leading national markets whose large chemical manufacturing, paints and coatings, and adhesives industries create substantial aliphatic hydrocarbon consumption. Germany accounts for approximately 28.47% of European revenues through its large automotive and industrial coatings sectors, major chemical manufacturing industry whose aliphatic hydrocarbon consumption spans diverse formulation applications, and the commercial presence of European petroleum refining and specialty chemical companies including Shell, TotalEnergies, and Neste whose aliphatic solvent product lines serve the European industrial market. The EU's Paints and Varnishes Directive and REACH regulations create the most demanding compliance environment globally for industrial solvent use, sustaining structural demand for low-aromatic aliphatic alternatives.

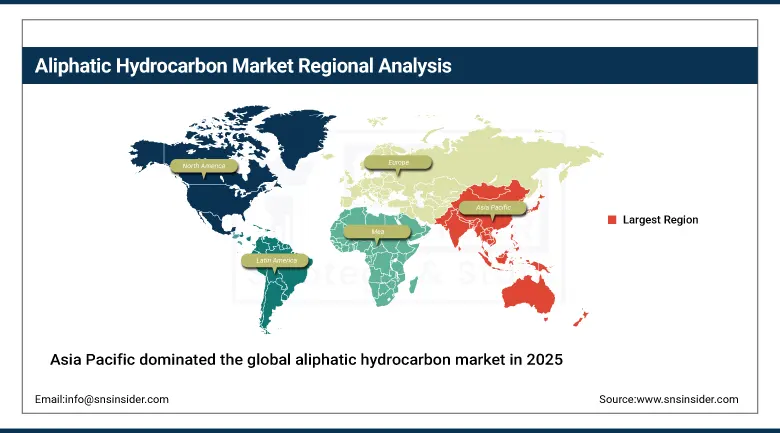

Asia Pacific Aliphatic Hydrocarbon Market Insights

Asia Pacific dominated the global aliphatic hydrocarbon market with the largest regional revenue share in 2025, driven by rapid industrialisation, construction activity expansion, growing automotive manufacturing, and chemical industry development across China, India, South Korea, Taiwan, and Southeast Asian economies. China accounts for approximately 42.84% of Asia Pacific revenues through its world-leading construction and manufacturing sectors whose coating and adhesive consumption creates the largest single national demand pool for aliphatic hydrocarbon solvents, combined with its domestic petrochemical industry's growing aliphatic solvent production capacity. India is growing rapidly as construction activity, automotive production, and chemical manufacturing expansion create accelerating aliphatic hydrocarbon demand whose growth rate substantially exceeds the global market average.

Get Customized Report as per Your Business Requirement - Enquiry Now

MEA & Latin America Aliphatic Hydrocarbon Market Insights

Middle East and Latin America are growing Aliphatic Hydrocarbon markets where expanding construction, automotive, and industrial sectors are creating increasing solvent demand. Saudi Arabia leads MEA revenues at approximately 22.84% of the regional total through its large petrochemical production base, whose integration with upstream crude oil production creates cost-competitive aliphatic hydrocarbon feedstock availability, and its rapidly expanding construction sector under Vision 2030 whose coating and adhesive consumption is growing proportionally with infrastructure investment scale. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large construction market, significant domestic automotive manufacturing and refinishing sector, and chemical industry whose aliphatic solvent consumption across adhesives, coatings, and industrial process applications creates consistent domestic demand.

Market Dynamics

Growth Driver: Tightening global VOC emission regulations driving substitution of aromatic solvents with aliphatic alternatives and expanding construction and industrial activity

The aliphatic hydrocarbon market's growth is powered by the regulatory substitution tailwind that is progressively redirecting solvent demand from aromatic to aliphatic chemistry across all major industrial end-use categories. VOC emission regulations in the EU, United States, and increasingly in China and other major Asian economies have created compliance obligations that aromatic solvent systems cannot satisfy at previously acceptable VOC content levels, while aliphatic solvent reformulations can meet within technically equivalent formulation performance parameters. Each national regulatory tightening that reduces permissible aromatic solvent VOC content in coating, adhesive, or cleaning product formulations creates proportional volume substitution toward aliphatic alternatives whose market volume grows structurally with each successive regulatory revision.

Restraint: Crude oil price volatility affecting aliphatic hydrocarbon feedstock economics and competition from waterborne formulation technologies

Aliphatic hydrocarbons are petroleum-derived chemical products whose production economics are directly linked to crude oil pricing and refinery feedstock availability, creating input cost volatility that can significantly alter product economics within months of crude oil market movements and compress supplier margins during periods of feedstock cost escalation relative to finished product pricing. Waterborne coating and adhesive technologies, whose progressive performance improvement and broadening application range have enabled substitution of solvent-borne formulations in a growing share of painting and bonding applications, represent a long-term structural headwind for solvent demand in applications where waterborne performance equivalence has been demonstrated and regulatory support for water-based systems reinforces technology adoption incentives.

Opportunity: Bio-based aliphatic hydrocarbon development and high-purity specialty grade expansion for pharmaceutical and personal care applications represent premium market frontiers rewarding sustainability and quality differentiation.

The development of bio-based aliphatic hydrocarbons from renewable feedstocks including agricultural residues, vegetable oils, and sugarcane derivatives creates a premium product category whose sustainability documentation satisfies corporate procurement commitments to bio-content supply chains that are becoming standard requirements among major coating, adhesive, and consumer goods manufacturers. Each commercial-scale bio-based aliphatic hydrocarbon production programme, including Neste's renewable hydrocarbons and LyondellBasell's CirculenRecover recycled content products, validates the technical and commercial viability of non-fossil aliphatic hydrocarbon supply whose adoption scales with corporate sustainability commitments. High-purity pharmaceutical and personal care grade aliphatic hydrocarbons whose traceable purity documentation, pharmacopoeial compliance, and consistent specification across production batches command significant price premiums above industrial commodity grades, creating a speciality market segment whose growth tracks pharmaceutical and personal care industry investment.

Recent Developments:

-

2023: LyondellBasell introduced new CirculenRecover product grades incorporating recycled content from advanced chemical recycling processes in North America, expanding the availability of aliphatic hydrocarbon products with sustainability documentation for corporate supply chains adopting circular economy procurement commitments.

-

2023: Henkel expanded its adhesive technologies manufacturing capacity with a new facility at Yantai Chemical Industry Park in China at EUR 135 million investment, increasing production of adhesive formulations that consume aliphatic hydrocarbon solvents as carriers, reflecting the growing Asia Pacific demand for high-performance adhesives.

-

2023: Shell Chemicals announced investment in its proprietary GTL technology to expand production of gas-to-liquid derived aliphatic hydrocarbon solvents whose zero aromatic content, consistent specification, and clean origin from natural gas feedstock without crude oil processing intermediaries provide premium quality positioning in specialty solvent applications.

Aliphatic Hydrocarbon Market Key Players are:

-

ExxonMobil Corporation

-

Royal Dutch Shell PLC

-

LyondellBasell Industries Holdings BV

-

SABIC (Saudi Aramco)

-

Neste Corporation

-

TotalEnergies SE

-

SK Global Chemical Co. Ltd.

-

Idemitsu Kosan Co. Ltd.

-

Calumet Specialty Products Partners LP

-

Haltermann Carless GmbH

-

Sasol Limited

-

Reliance Industries Limited

-

HF Sinclair Corporation

-

Chevron Phillips Chemical Company LLC

-

Braskem SA

-

ENEOS Corporation

-

Formosa Plastics Corporation

-

Ineos Group Holdings SA

-

Cepsa SA

-

Repsol SA

Aliphatic Hydrocarbon Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.34 Billion |

| Market Size by 2035 | USD 6.93 Billion |

| CAGR | CAGR of 4.81% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Saturated Aliphatic Hydrocarbons, Unsaturated Aliphatic Hydrocarbons, Cyclic Aliphatic Hydrocarbons) • By Application (Paints & Coatings, Adhesives & Sealants, Polymer & Rubber Processing, Cleaning Agents, Printing Inks, Fuel Blending & Additives, Personal Care & Pharmaceuticals, Others) • By End Use (Industrial, Automotive, Construction, Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ExxonMobil Corporation, Royal Dutch Shell PLC, LyondellBasell Industries Holdings BV, SABIC (Saudi Aramco), Neste Corporation, TotalEnergies SE, SK Global Chemical Co. Ltd., Idemitsu Kosan Co. Ltd., Calumet Specialty Products Partners LP, Haltermann Carless GmbH, Sasol Limited, Reliance Industries Limited, HF Sinclair Corporation, Chevron Phillips Chemical Company LLC, Braskem SA, ENEOS Corporation, Formosa Plastics Corporation, Ineos Group Holdings SA, Cepsa SA, and Repsol SA |

Frequently Asked Questions

Tightening global VOC emission regulations driving substitution of aromatic solvents with aliphatic alternatives in coating and adhesive formulations, expanding construction and automotive manufacturing activity in Asia Pacific and the Middle East creating volume demand growth.

The paints & coatings segment dominated the aliphatic hydrocarbon market in 2025 with approximately 34.22% share, as aliphatic hydrocarbon solvents serve as essential diluents and carriers across architectural, automotive, and industrial coating formulations.

Asia Pacific dominated the Aliphatic Hydrocarbon Market in 2025 with the largest regional revenue share.

The Aliphatic Hydrocarbon Market is expected to grow at a CAGR of 4.81% from 2026 to 2035.

The Aliphatic Hydrocarbon Market was valued at USD 4.34 Billion in 2025.

Get in Touch