Diamond Coatings Market Size & Trends

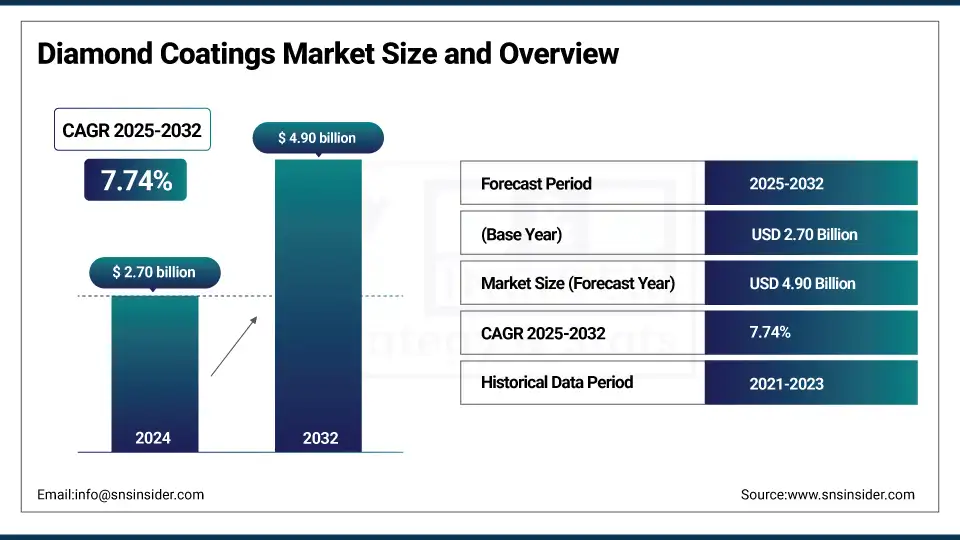

The Diamond Coatings Market size was valued at USD 2.70 billion in 2024 and is expected to reach USD 4.90 billion by 2032, growing at a CAGR of 7.74% over the forecast period of 2025-2032.

Diamond Coatings Market analysis identifies the most significant factors behind market growth, with the increase in adoption of cutting and machining tools being one of the major driving forces behind the market growth. Tools that are coated with diamond show superior hardness, wear resistance, and sharpness retention properties under extreme operating conditions. These characteristics enable them to be ideal for high-speed and high-accuracy machining of hard materials such as composites, ceramics, and non-ferrous metals. In industries such as automobile, aerospace, electronics, and others, which require high efficiency and high durability of the processes to be performed in the manufacturing of machine elements, the use of diamond-coated tools has become widespread. They are preferred in many advanced machining operations due to their enhanced productivity and cost savings, owing to their longer tool life and lower downtime. The increased dependence on high-performance tooling solutions further drives the diamond coatings market growth.

The U.S. Department of Energy report reveals that almost one-third of all industrial drilling footage globally is drilled with polycrystalline diamond compact (PDC) bits. PDC bits offer unsurpassed service life, and DOE estimates that PDC bits can save USD 100,000 per bit through reduced replacement and downtime.

Diamond Coatings Market Size and Forecast

-

Market Size in 2024: USD 2.70 Billion

-

Market Size by 2032: USD 4.90 Billion

-

CAGR: 7.74% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2020–2024

To Get more information On Diamond Coatings Market - Request Free Sample Report

Diamond Coatings Market Trends:

-

Rising demand from cutting tools and machining applications is driving adoption, as diamond-coated tools improve tool life by 3–5 times and enhance cutting speeds by 20–30%.

-

Growing use in electronics and semiconductors is expanding the market, with thermal management applications increasing at a CAGR of over 8% due to diamond’s high thermal conductivity (up to 2000 W/mK).

-

Increasing adoption in medical devices and implants is supporting growth, as biocompatible diamond coatings reduce wear rates by up to 40% in surgical instruments.

-

Expansion in automotive and aerospace sectors is boosting demand, with lightweight and wear-resistant coatings contributing to 15–25% longer component lifespan.

-

Technological advancements in CVD and PVD processes are improving coating uniformity and adhesion strength, reducing defect rates by 20–30% and enhancing large-scale industrial deployment.

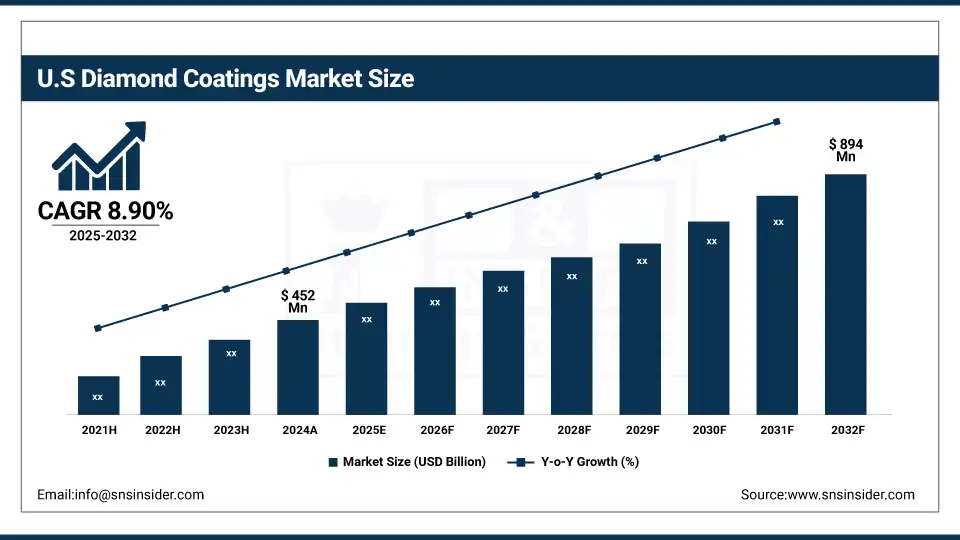

The U.S. Diamond Coatings market size was USD 452 million in 2024 and is expected to reach USD 894 million by 2032 and grow at a CAGR of 8.90% over the forecast period of 2025-2032. The country’s growth is driven by the presence of technologically advanced companies, bulk high-value manufacturing, and need-based applications from the aerospace, medical devices, and defense sectors. American firms are the leaders in the use of diamond coatings, which are rapidly penetrating metal machining, semiconductor tools, orthopaedic implants, and high-speed sensors. In addition, the U.S. government is making investments that foster more innovation and manufacturing capability at home in critical industries, compelling businesses to extend tool life, minimize material waste, and enhance product durability.

Diamond Coatings Market Dynamics

Drivers:

-

Growth in Electronics & Semiconductor Industry Drive the Market Growth

Diamond deposition is commercially popular for electronic component thermal management, optical transparency, and surface protection of devices. Thermal conductivity becomes paramount with the continued commercialization of very small devices that consume large amounts of power, such as in chips and substrates. Wafers, heat spreaders, and lenses coated in diamond make devices last longer and work better. Various applications of high-speed and high-precision electronics are increasingly demanding thin diamond films.

For instance, in 2024, Blue Wave Semiconductors announced a diamond-coated optical and semiconductor substrates fabrication facility to meet increasing demand in microelectronics.

Restraints:

-

Limited Availability of Skilled Workforce May Hamper the Market Growth

The deposition of diamond coatings mostly through CVD or PECVD processes requires special knowledge in the fields of materials science, chemistry, and high-vacuum systems. Particularly in the context of developing economies, there are simply not enough trained professionals in the field to handle the process competently. The lack of this slows production scale-up and affects the uniformity of the coating quality. The high capital investment required to train and recruit contributes to the cost of business operations. The demand is only expected to keep rising, but unless a workforce is developed to meet it, the market may struggle to keep pace.

Opportunities:

-

Adoption of Renewable Energy and Optics Creates an Opportunity in the Market

Diamond coatings are gaining attention as a high-value functional material for renewable energy and optical technologies because of their unique combination of high optical transparency, high hardness, high thermal conductivity, and high chemical stability. These coatings offer minimal light loss and can be used on lens components in solar panels, and in high-performance optical components, such as sensors for satellite imaging, lasers, and aerospace systems. The same technique can be used to make solar cells more efficient by preventing surface wear and protecting them from environmental factors including dust, humidity, and UV radiation, particularly from remote, arid, or extreme environments, by coating the cells with diamond-coated glass, which drives the diamond coatings market trends.

The U.S. Department of Energy funded diamond-coated lenses in 2024 as part of the Next-Generation Sensors and Advanced Optics program for clean energy applications and aerospace imaging systems.

Diamond Coatings Market Segmentation Analysis

By Technology

Chemical Vapor Deposition held the largest Diamond Coatings market share, around 67%, in 2024 due to its capacity to achieve high-purity, uniform, and well-adhered diamond films on various substrates (metals, ceramics, semiconductors). CVD enables control of the coating thickness and quality, which makes it suitable for applications that require a highly engineered performance, such as cutting tools, medical devices, optical components, and semiconductors. This is particularly crucial for industries that require ultimate hardness, thermal stability, and wear resistance. Continuous advances in CVD scalability and reliability ensure CVD will remain the process of choice for diamond coatings as manufacturing sectors continue to seek economic solutions for high-performance, durable coatings.

Physical Vapor Deposition held a significant Diamond Coatings market share. The large share was mainly attributed to the increase in its usage in applications, which need precision coatings that are thin, hard, and can resist high abrasive wear. While CVD remains the volume leader, PVD is gaining traction owing to the ability to deposit DLC coatings at lower temperatures and with higher energy efficiency. This quality renders it appropriate for heat-degradable substrates and complex geometries present in microelectronics, biomedical tools, and automotive components. PVD is also able to provide shorter process times and cleaner operations, which can be a major advantage in industries where sustainability and cost efficiency such key objectives.

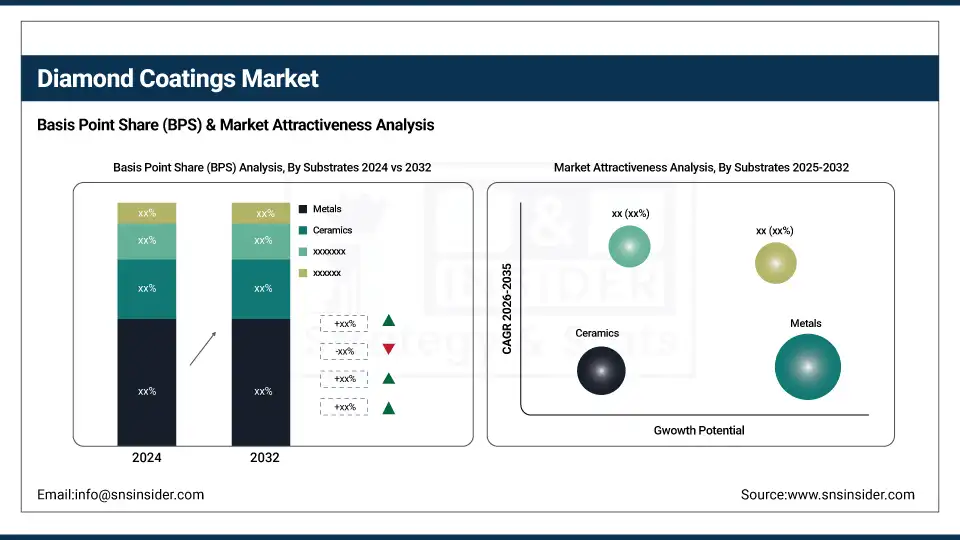

By Substrates

Metals segment held the largest market share, around 42.34%, in 2024 due to the extensive application of diamond coatings on metal substrates, particularly steel, titanium, and Aluminum in advanced industrial sectors, mainly driving this dominance. These coatings improve the hardness, wear resistance, and thermal stability of metal parts and are therefore suitable for use in cutting tools, machining tools, aerospace components, and medical devices. Diamond coatings on metal surfaces substantially increase component life, reduce maintenance requirements, and improve efficiency in extreme service environments.

Composites have a significant market share in the Diamond Coatings market owing to their increasing usage in industries requiring lightweight but high-strength materials. The composite materials are used to enhance the surface hardness, thermal conductivity, and wear and corrosion resistance when coated with diamond films and thus exhibit specific features required in aerospace, defense, electronics, and high-performance sports equipment, among others. These coatings aid in increasing the lifespan of composite components, sometimes in applications, where friction, heat, or harsh environments could degrade the uncoated surfaces instead.

By End-Use

Industrial held the largest market share, around 44%, in 2024. The dominance of this segment is additionally justified by the extensive penetration of tools and components coated with industrial diamond coatings in the metal machining, construction, mining, and heavy equipment manufacturing industries. They are best suited for high wear, high precision environments as diamond coatings augment the life of the tools including drills, cutters, and grinding wheels, among others. With such advancement, the tool coated with diamond to become an inexpensive solution for the industries that are always on the lookout to reduce downtime and increase the tool life and thereby productivity.

Medical has a significant market share in the diamond coatings market owing to increased demand for biocompatible, durable, and corrosion-resistant materials in healthcare applications. Diamond coatings are being used more than ever on surgical instruments, dental tools, orthopedic implants, and diagnostic devices because of their high hardness, low friction, and chemical inertness. The impressive antibacterial properties of silver increase the accuracy and durability of medical tools while preventing the transmission and infection risks during various medical procedures. Diamond coatings are used in orthopedic and implantable devices to enhance wear resistance and reduce the foreign body reaction, which are essential characteristics for long-term implantation inside human body.

Diamond Coatings Market Regional Outlook

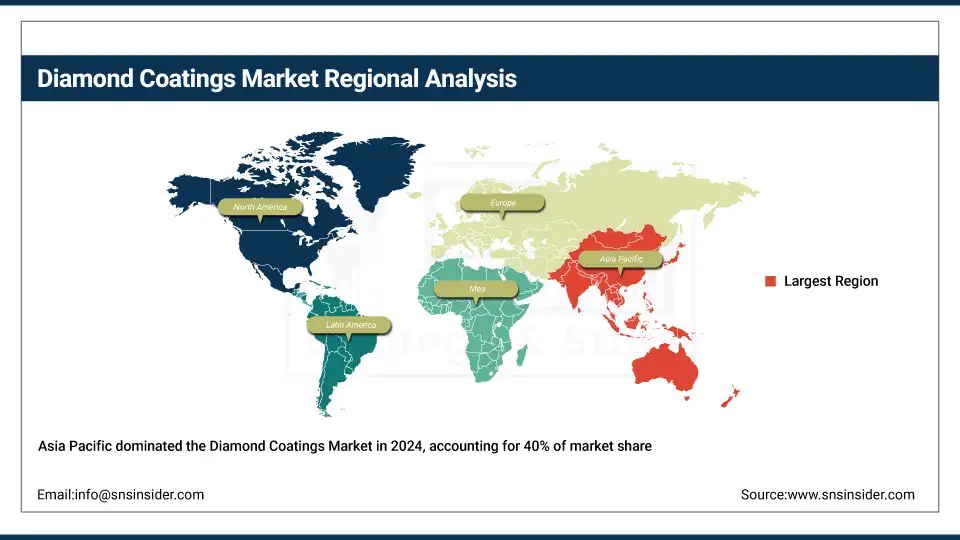

Asia Pacific Diamond Coatings market held the largest market share, around 40%, in 2024. It is owing to the huge ecosystem of manufacturing in countries such as China, Japan, South Korea, and India. The region also has a strong demand for diamond-coated tools and components due to its dominance in consumer electronics, semiconductors, automotive components, and industrial equipment. Moreover, the global rapid industrialization and continuous infrastructure development are demanding high-durability materials, particularly in sectors, such as abrasives and hard metals, where resistance to heat and chemicals is a priority. All these and numerous other applications from large-scale production of smartphones, wearables, EV parts, and LED optics are increasingly benefiting from the attachment of diamond-coated surfaces that enable higher reliability and performance.

Get Customized Report as per Your Business Requirement - Enquiry Now

For instance, in 2024, a Japanese electronics manufacturer adopted nano-diamond coatings on smartphone camera lenses to make them brush-resistant, scratch-resistant, and ensure clarity of light transmittance.

North America Diamond Coatings market held a significant market share and is the fastest-growing segment in the forecast period. The growth is owing to its extensive industrial infrastructure and emphasis on precision-based manufacturing. The diamond coating tool is widely used in several sectors including the aerospace industry, the defense industry, the automotive industry, and heavy engineering due to its operational efficiency, low tool wear, and improved quality of the product. In addition, the presence of a number of advanced research institutions and coating technology providers in the region also boosts the growth of the market as they develop and commercialize advanced coating techniques, such as Chemical Vapor Deposition (CVD).

Europe held a significant market share in the forecast period due to the presence of precision manufacturing, renewable energy, and medical equipment. Given the high sustainable and high-efficiency standard of many European companies, diamond coatings fit this requirement by promoting less maintenance, longer component lifetime, and reliable performance in extreme conditions. Diamond coatings provide greater functionality, and the ability to push into higher performance areas has made them a contributor to advanced optics, aerospace parts, and medical technology in the region. Also, EU rules for environmentally friendly production are leading to a growing preference for diamond coatings as replacements for toxic surface treatment processes such as chrome plating.

Diamond Coatings Market Key Players

The major Diamond Coatings companies are Oerlikon, Morgan Advanced Materials, Diatex, Element Six, NeoCoat, Advanced Diamond Technologies, SP3 Diamond Technologies, Diamond Product Solutions, Blue Wave Semiconductors, and JCS Technologies.

Recent Developments in the Diamond Coatings Market

-

In 2024, Blue Wave Semiconductors announced plans to build a new production facility for diamond-coated optical and semiconductor substrates, addressing growing demand for precision and durable coatings in microelectronics.

-

In 2023, HOYA Vision Care introduced Hi‑Vision Meiryo Diamond, a premium diamond-enhanced optical lens coating with enhanced clarity, scratch resistance, and durability, signaling adoption in consumer optics.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.70 Billion |

| Market Size by 2032 | USD 4.90 Billion |

| CAGR | CAGR of 7.74% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Chemical Vapor Deposition, and Physical Vapor Deposition) • By Substrates (Metals, Ceramics, Composites, and Others) • End-Use (Electrical & Electronics, Medical, Industrial, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Oerlikon, Morgan Advanced Materials, Diatex, Element Six, NeoCoat, Advanced Diamond Technologies, SP3 Diamond Technologies, Diamond Product Solutions, Blue Wave Semiconductors, JCS Technologies |

Frequently Asked Questions

Ans The diamond coating process, especially using CVD technology, is capital-intensive due to the need for specialized equipment, high energy consumption, and complex processing conditions.

Ans Advancements in electronics significantly boost the Diamond Coatings Market by increasing demand for durable, thermally conductive, and electrically insulating materials. Diamond coatings help manage heat in high-performance chips, protect sensitive components from wear, and enhance device longevity. As electronics become smaller and more powerful, the need for high-precision, reliable coatings like diamond continues to grow.

Ans The main applications of diamond coatings in the medical industry include surgical instruments, dental tools, orthopedic implants, and diagnostic devices. These coatings provide superior hardness, wear resistance, biocompatibility, and reduced friction, enhancing the durability and performance of tools while minimizing infection risk and tissue damage during procedures.

Ans Chemical Vapor Deposition (CVD) forms high-purity diamond coatings through chemical reactions in a gas phase, ideal for uniform coatings on complex shapes. Physical Vapor Deposition (PVD) involves physically vaporizing solid materials and depositing them as thin diamond-like films, typically at lower temperatures. CVD is preferred for crystalline diamond layers, while PVD is used for diamond-like carbon (DLC) films.

Ans The most commonly used technologies in the Diamond Coatings Market are Chemical Vapor Deposition (CVD) and Physical Vapor Deposition (PVD). CVD dominates due to its ability to produce high-quality, uniform, and adherent diamond films. PVD is also gaining traction for low-temperature applications and diamond-like carbon (DLC) coatings.

Get in Touch