Alkyd Resin Market Report Scope & Overview:

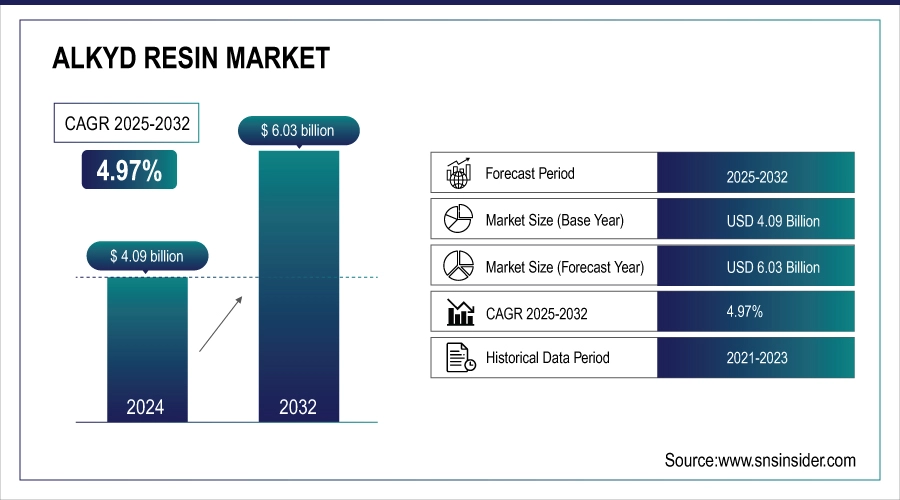

The Alkyd Resin Market Size was valued at USD 4.09 Billion in 2024 and is expected to reach USD 6.03 Billion by 2032, growing at a CAGR of 4.97% over the forecast period of 2025-2032.

Alkyd Resin market analysis reveals increasing demand from packaging and specialty sectors. This is achieved by the need for coatings that are both durable and protective, while also being attractive in the case of packaging for cartons, paperboard, and industrial containers. Specialty industries, namely marine, aerospace, and pipelines, prefer this type of resins because of the good adhesion and resistance of alkyd resins to corrosion and weatherability. Meanwhile, industrialization and the emergence of certain sectors are helping to support demand throughout high-value sectors. Increased desire for the highest possible levels of functionality and capacity for withstanding tough environments while maintaining quality has coincided in recent years with an increase in these certain industries as well which drive the alkyd resin market growth.

To Get more information On Alkyd Resin Market - Request Free Sample Report

At the same time, advances in modified and hybrid alkyd resins enable the sectors to achieve strong results without sacrificing sustainability and this has given rise to an increase in demand for Alkyd Resin in a variety of distinctive applications industries over the period.

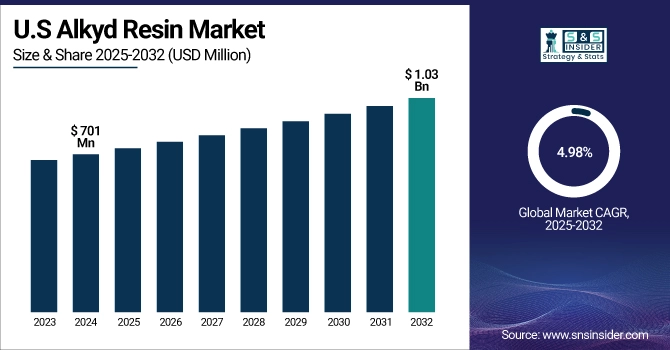

The U.S. Alkyd Resin market size was USD 701 million in 2024 and is expected to reach USD 1.03 billion by 2032 and grow at a CAGR of 4.98% over the forecast period of 2025-2032. It is due to strong demand for premium, durable, and low-maintenance kitchen and bathroom fixtures. Rising home renovation projects, new residential and commercial construction, and the hospitality sector’s expansion are key growth drivers. Consumers increasingly prefer corrosion-resistant and eco-friendly finishes, which PVD coatings provide.

Market Dynamics

Key Drivers:

-

Growth in Construction and Infrastructure Activities Drives the Market Growth

As urbanization and industrialization across the globe increases, the construction activities have also increased, resulting in the growing need of long-lasting decorative coatings on construction surfaces. Carbonate alkyds are a common type of alkyd resins that are used in the paints of residential, institutional and industrial buildings and that have outstanding adhesiveness and weather resistance. In the US, government investment in infrastructure, such as the USD 1.2 trillion Infrastructure Investment and Jobs Act (2021), has led to a demand for industrial coatings, in turn stimulating alkyd resin consumption. Expanding Production Capacities by Application Manufacturers are expanding capacities to cater to application demand;

for example, in 2022, BASF expanded its coating raw material production in North America in construction application

Restrain:

Competition from Alternative Resins, Which May Hamper the Market Growth

Alternative resins competition is key restraint regarding the alkyd resin market. Though alkyd resins are appreciated for their toughness, gloss, and ease of application, other resins including acrylics, epoxies and polyurethanes, are finding favor in numerous industrial and specialty markets. These have typically better chemical resistance, higher speed of drying, and better mechanical properties and, thus, are better suited for performance applications such as automotive, aerospace, and industrial machinery coatings. As a result of this, producers of alkyd resins are forced to develop modified, hybrid and waterborne alkyds to improve performance and to maintain market share.

Opportunities:

-

Innovation and Product Development Create an Opportunity for the Market

Growing popularity of innovation and product development is a positive growth influencer of alkyd resin market. There is a growing demand for high-performance, environmentally friendly, multi-functional coatings, a demand that has driven traditional alkyd formulations to be superseded by hybrid, UV-curable, and bio-based resins. These advancements deliver properties such as faster dry, improved chemical resistance, better adhesion, lower VOC, meeting sustainability and regulatory needs. They are a result of R&D investments that manufacture is able to devote to these next-generation products, which are unlocking new applications in industrial, automotive, aerospace and decorative coatings which drive the alkyd resin market trends.

Segment Analysis:

By Type

The market is dominated by short oil alkyds of approximately 48% as they are inexpensive and fast drying and can be used in decorative and industrial coatings. Modified Alkyds (Urethane-modified, Acrylic-modified, Silicone-modified) is the fastest growing sub-segment owing to the rising need of high-performance coatings in automotive, marine and other specialty applications. Growth is driven by demand for improved chemical resistance, durability and product development, with short oil alkyds still being favoured for traditional coating applications.

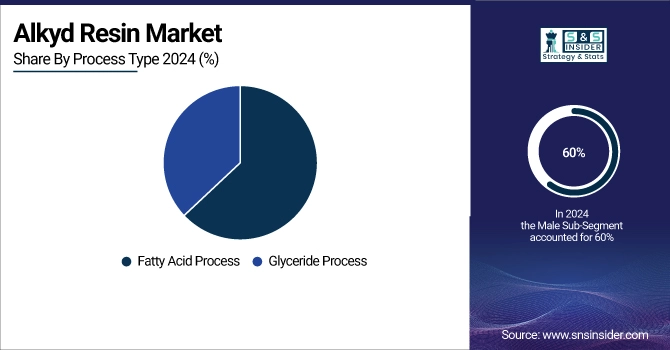

By Process Type

The Fatty Acid Process is the dominant method, accounting for about 60% of production and is the oldest and the less expensive way to obtain resins of consistent quality. Glyceride Process is the largest sub-segment and is the fastest-growing sub-segment due to the production of superior performance alkyd resins for specialty and industrial coatings. The growing demand for high quality coatings in automotive, aerospace and industrial applications is driving the growth of glyceride process, while fatty acid process will continue to lead in general industrial and decorative applications.

By Formulation Type

High Solids Alkyds continue to dominate at approximately 50% market share, because of their low-VOC capabilities and compliance with environmental requirements. The Waterborne Alkyds segment is registering its fastest growth as a result of more stringent environmental regulations and growing use of environment-friendly coatings. The same VOC-driven trends that are favouring waterborne alkyds for commercial finishes are pushing use in residential and industrial decorative coatings markets, while high-solids alkyds continue to claim a strong hold on these sectors.

By Application

Paints & Coatings dominate the range accounting for nearly 55% share, well-all – round household name in residential, commercial, and industrial infrastructure. Fastest growth is expected for Adhesives & Sealants, spurred by demand for robust adherence and durability in industrial and packaging applications. Adhesives & sealants will be driven by rising packaging, construction, and industrial markets, and paints & coatings are the backbone for historical demand from infrastructure and decorative work.

Regional Analysis:

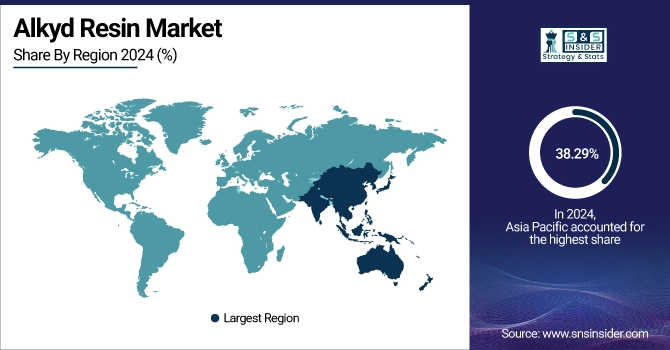

Asia Pacific held the largest Alkyd Resin Market Share in 2024, around 38.29% 2024. It is due to rapid urbanization, rising disposable incomes, and expanding residential and commercial construction projects. Consumers in countries like China, India, and Southeast Asian nations are increasingly seeking premium, durable, and aesthetically appealing kitchen and bathroom fixtures. The growth of modern infrastructure, luxury housing developments, and hospitality projects has further fuelled demand for high-quality finishes. Additionally, increasing awareness of sustainability and long-lasting products has led to higher adoption of PVD-coated faucets, which offer superior corrosion resistance and durability.

Get Customized Report as per Your Business Requirement - Enquiry Now

Investments by key players in manufacturing facilities and product launches, such as Moen’s Lumi coat finishes in 2023, demonstrate industry confidence in the region’s market potential. Overall, a combination of economic growth, urban development, and consumer preference for premium products is driving the Asia Pacific market forward.

The North America region is the fastest-growing market. It is owing to rising demand for durable, low-maintenance and great-looking kitchen and bathroom fixtures. Increasing home improvements, the growth of commercial infrastructure projects and a robust hospitality industry are fuelling demand for high-end finishes. Both consumers and businesses are turning more towards sustainable and anti-corrosive options, such as PVD coatings. Performance and durability have never been better, with product innovations and technology, like Moen Lumicoat PVD finishes (launched in 2024), offering increased performance and durability, and ultimately more usage. Moreover, increasing disposable incomes and knowledge of durable, superior finishes foster market growth.

Europe is witnessing promising growth in the alkyd resin market, it is due to increasing demand for premium, durable, and aesthetically appealing kitchen and bathroom fixtures. Strict environmental regulations and sustainability standards encourage the use of low-VOC and long-lasting finishes, which PVD coatings provide. Consumers and businesses in countries such as Germany, France, and the U.K. prefer high-quality, corrosion-resistant, and easy-to-maintain products. Expansion in residential, commercial, and hospitality infrastructure further drives market adoption.

Key Players:

Major Alkyd Resin companies are BASF, AkzoNobel, Allnex, PPG Industries, Hexion Inc., Dow Inc., Eastman Chemical Company, Lubrizol Corporation, Resinadco, Shandong Taihe Resin Co., Ltd., Hempel, Lanxess, Nuplex Industries, Arkema, Cray Valley, Evonik Industries, Jayant Resin, Kaneka Corporation, Synthomer, Sayerlack.

Recent Development:

-

In 2023, Moen launched Lumicoat finishes in polished nickel, champagne bronze, and matte black with Diamond Seal valve technology, enhancing durability and resistance to water spots and stains. This innovation targets consumer demand for low-maintenance, long-lasting faucet finishes.

-

In 2022, Delta expanded its Lumicoat finishes to include additional styles and configurations designed to resist mineral buildup and hard water stains, providing consumers with more durable and easy-to-maintain faucet options.

| Report Attributes | Details |

| Market Size in 2024 | USD 4.09 Billion |

| Market Size by 2032 | USD 6.03 Billion |

| CAGR | CAGR of4.97% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type – Short Oil Alkyds, Medium Oil Alkyds, Long Oil Alkyds, Modified Alkyds (Urethane-modified, Acrylic-modified, Silicone-modified); • By Process Type – Fatty Acid Process, Glyceride Process; • By Formulation Type – High-Solids Alkyds, Waterborne Alkyds, Others (Solvent-borne Alkyds, UV-cured Alkyds, Hybrid Alkyds); • By Application – Paints & Coatings, Industrial Coatings, Automotive Coatings, Decorative Coatings, Adhesives & Sealants, Printing Inks, Varnishes & Enamels, Others (Marine, Aerospace, Packaging, Pipeline Coatings, Specialty Industrial Coatings) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | BASF, AkzoNobel, Allnex, PPG Industries, Hexion Inc., Dow Inc., Eastman Chemical Company, Lubrizol Corporation, Resinadco, Shandong Taihe Resin Co., Ltd., Hempel, Lanxess, Nuplex Industries, Arkema, Cray Valley, Evonik Industries, Jayant Resin, Kaneka Corporation, Synthomer, Sayerlack |

Frequently Asked Questions

Key trends include waterborne and bio-based polymer adoption, hybrid coatings, and automation to improve efficiency and environmental compliance.

The market is shifting toward lightweight, recyclable, and high-barrier coatings to meet sustainability goals and extend product shelf life.

Polyethylene (PE), polypropylene (PP), polyvinylidene chloride (PVDC), and ethylene-vinyl acetate (EVA) are the most widely used materials

Growth is driven by rising demand for sustainable, high-barrier packaging, increased e-commerce shipments, and advancements in polymer technologies.

The Extrusion Coating Market involves applying a molten polymer layer onto substrates like paper, foil, or film to enhance barrier, durability, and printability for industrial applications.

Get in Touch