Ammunition Market Report Scope & Overview:

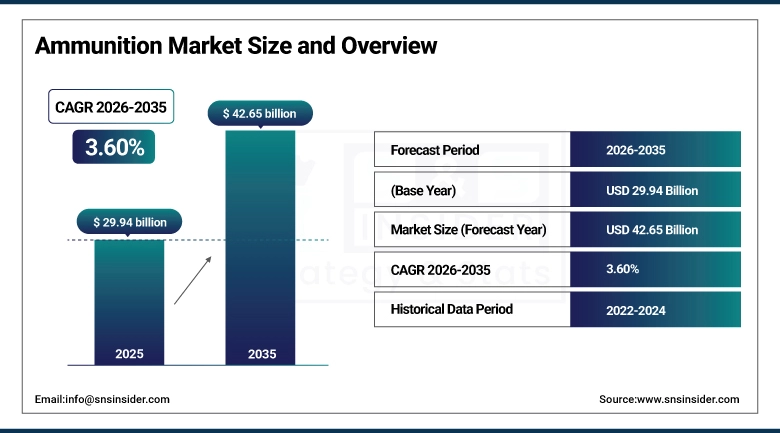

The Ammunition Market size was valued at USD 29.94 Billion in 2025 and is projected to reach USD 42.65 Billion by 2035, growing at a CAGR of 3.60% during 2026–2035.

The Ammunition industry is the production and supply of bullets, shells, and other ammunition for use by the military, law enforcement agencies, and civilians. The ammunition industry is motivated by various factors like an increase in military spending, an increase in geopolitical risks, and an increase in the requirement for individual protection and recreational shooting. Technology advancements like precision ammunition technology, smart ammunition technology, and high-performance ammunition technology are affecting the ammunition industry. Military modernization and training are consistently boosting the ammunition industry.

Ammunition Market Size and Forecast:

-

Market Size in 2025: USD 29.94 Billion

-

Market Size by 2035: USD 42.65 Billion

-

CAGR: 3.60% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Ammunition Market - Request Free Sample Report

Ammunition Market Key Trends:

-

Increasing adoption of precision-guided and smart ammunition to enhance accuracy and minimize collateral damage in modern warfare

-

Rising demand for small-caliber ammunition driven by civilian firearm ownership, law enforcement usage, and shooting sports activities

-

Growing investments in domestic ammunition manufacturing to strengthen defense self-reliance and reduce import dependency

-

Advancements in lightweight, high-performance materials improving ammunition efficiency, range, and operational effectiveness

-

Expansion of less-lethal ammunition usage for crowd control and law enforcement applications amid increasing focus on non-fatal solutions

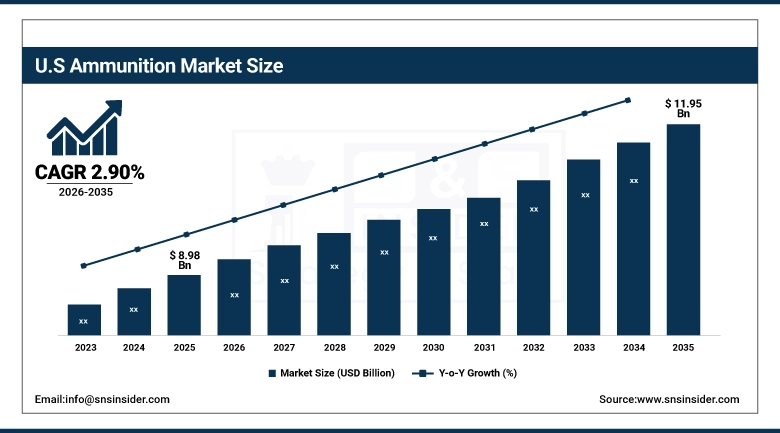

The U.S. Ammunition Market has been valued at USD 8.98 Billion in 2025 and is expected to reach USD 11.95 Billion in 2035, growing at a CAGR of 2.90% from 2026 to 2035, Growth of the U.S. Ammunition Market is driven by high defense spending, continuous military modernization, strong demand from law enforcement agencies, and increasing civilian firearm usage for self-defense and shooting sports.

Ammunition Market Key Drivers:

-

Rising Global Defense Spending and Military Modernization

The increase in defense spending across the world and the modernization of armed forces in the world have provided a significant opportunity for the ammunition market. Across the world, various countries are spending heavily in acquiring technologically advanced defense equipment, ammunition, and military drills for their armed forces. The increase in geopolitical tensions, border disputes, and wars across the world have provided a significant opportunity for small-calibre, medium-calibre, and large-calibre ammunition.

Ammunition Market Key Restraints:

-

Stringent Regulations and Arms Control Policies

Stringent regulations and international policies controlling the use of arms have a significant impact on the ammunition market. Licensing and usage restrictions are imposed on the production and use of ammunition. These regulations affect the production and use of ammunition, especially in the hands of civilians. Ethical issues and disarmament treaties are responsible for controlling the production and use of ammunition. These regulations and treaties affect the production and use of ammunition.

In 2025, over 40% of countries strengthened firearm and ammunition regulations, directly impacting sales, trade flows, and overall market accessibility.

Ammunition Market Key Opportunities:

-

Advancements in Smart and Precision-Guided Ammunition

Smart and precision-guided ammunition technologies are offering significant opportunities for growth in the market. The increasing need for precise weaponry with minimum collateral damage is resulting in the development of guided ammunition technologies enabled with GPS, laser, and AI-based technologies. Defense forces are focusing on the development of next-generation ammunition technologies for better efficiency and success ratios. These technologies are also used for long-range capabilities and precision strikes. Increased R&D investments and partnerships with technology companies are resulting in the development of these technologies.

Ammunition Market Segments:

-

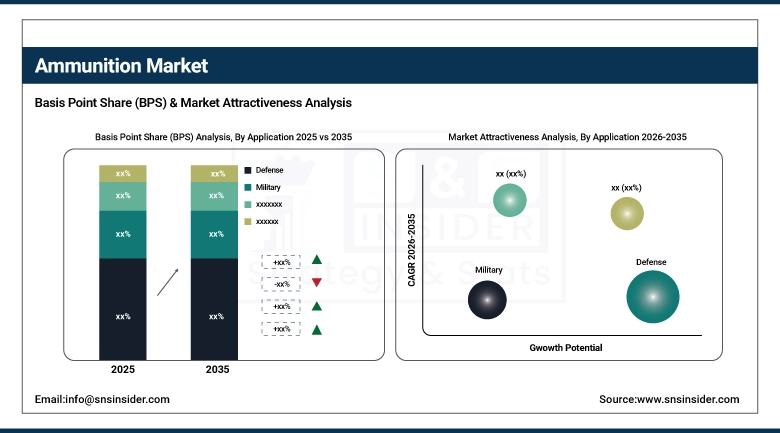

By Application: In 2025, Defense & Military dominated with 65% share; Civil & Commercial (especially Self-defense and Sporting) fastest growing segment during 2026–2035

-

By Caliber: In 2025, Small Caliber dominated with 70% share; Medium Caliber fastest growing segment during 2026–2035

-

By Product: In 2025, Bullets dominated with 60% share; Artillery Shells fastest growing segment during 2026–2035

-

By Component: In 2025, Projectiles & Warheads dominated with 35% share; Fuzes & Primers fastest growing segment during 2026–2035

-

By Guidance Mechanism: In 2025, Non-guided dominated with 80% share; Guided fastest growing segment during 2026–2035

-

By Lethality: In 2025, Lethal ammunition dominated with 85% share; Less-lethal fastest growing segment during 2026–2035

Ammunition Market Segment Analysis:

By Application: Defense & Military Dominates, Civil & Commercial Fastest-Growing

Defense & Military dominates the application segment due to continuous procurement by armed forces, rising defense budgets, and ongoing modernization programs worldwide. Large-scale usage in training, combat operations, and stockpiling further strengthens its leading position.

Civil & Commercial is the fastest-growing segment, driven by rising civilian firearm ownership, increasing interest in shooting sports, and expanding personal safety and self-defense ammunition requirements, especially in developing countries.

By Caliber: Small Caliber Dominates, Medium Caliber Fastest-Growing

Small caliber has the largest market share in the caliber market due to its usage in various applications, including military and law enforcement agencies, and civilian use such as handguns and rifles.

Medium caliber has the largest growth rate compared to all the caliber types. This is because of the increasing demand for their use in various defense applications.

By Product: Bullets Dominates, Artillery Shells Fastest-Growing

Bullets lead in the product segment due to their extensive usage in military, law enforcement, and civilian sectors. This segment has a high consumption rate, repeat business, and a wide range of usage.

Artillery shells are the fastest-growing segment in the industry due to growing military investments in heavy armament, long-range combat equipment, and ongoing geopolitical conflicts.

By Component: Projectiles & Warheads Dominates, Fuzes & Primers Fastest-Growing

Projectiles & warheads occupy the largest share in this component segment, as they form the primary functional component of ammunition, which is necessary for impact in various ammunition types.

Fuzes & primers occupy the highest growth rate in this ammunition component segment owing to innovations in igniter technology and precision and smart detonators.

By Guidance Mechanism: Non-Guided Dominates, Guided Fastest-Growing

Non-guided ammunition dominates the segment due to its cost-effectiveness, high production volume, and widespread use in conventional combat and training exercises.

Guided ammunition is the fastest-growing segment, driven by the need for precision strikes, reduced collateral damage, and increasing adoption of advanced targeting technologies.

By Lethality: Lethal Ammunition Dominates, Less-Lethal Fastest-Growing

Lethal ammunition is the dominant force in the segment due to the fact that it is mostly used by the military for combat purposes. Therefore, it makes up the majority of the ammunition demanded globally.

Less lethal ammunition is the fastest-growing segment of the ammunition industry due to the increase in the demand for the same by law enforcement agencies.

Ammunition Market Regional Analysis:

North America Ammunition Market Insights:

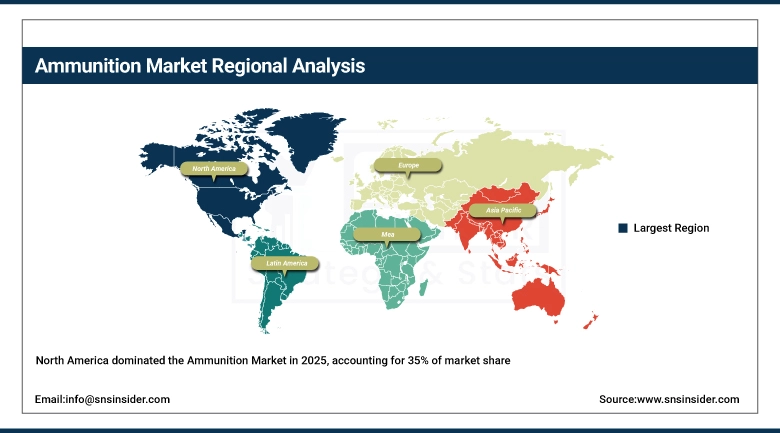

North America region holds the highest market share for the ammunition market and is expected to grow at a high rate, reaching approximately 35% by 2025. This is due to high defense spending in the US, which supports the modernization of the armed forces, as well as high demand for ammunition from law enforcement agencies. In addition, the high number of civilians owning guns and the popularity of the shooting sports industry are key drivers for the ammunition market. Technological advancements in precision and smart ammunition are also expected to drive the market forward. Geopolitics are also playing a crucial role in the growth of the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Ammunition Market Insights:

Europe ammunition market is influenced by increasing defense spending and ongoing military modernization programs in major countries such as Germany, France, and the UK. Geopolitical tensions, especially in Eastern Europe, are also boosting ammunition demand. The region has strong defense ties through NATO and regional defense initiatives, which positively influence ammunition demand. Moreover, major defense players and advancements in precision and guided ammunition also contribute to the growth of the ammunition market in Europe.

Asia-Pacific Ammunition Market Insights:

Asia-Pacific ammunition market holds the highest growth rate, driven by increasing defense spending and military modernization programs in countries such as China, India, and South Korea. In addition, increasing geopolitical risks and security concerns along borders are propelling the demand for technologically advanced ammunition systems. There has been a rise in indigenous capabilities in the Asia-Pacific region, along with government initiatives to enhance defense self-sufficiency. Moreover, increasing law enforcement requirements and internal security concerns are adding to the demand, thus making the Asia-Pacific region a significant growth hub for the global ammunition market.

Latin America Ammunition Market Insights:

Latin America ammunition market is driven by rising internal security concerns, increasing crime rates, and growing demand from law enforcement agencies. Governments are investing in modernizing police and defense forces. Civilian demand for self-defense is also increasing. Expanding security infrastructure and regional instability continue to support steady growth across the market.

Middle East & Africa (MEA) Ammunition Market Insights:

Middle East & Africa (MEA) ammunition market is primarily driven by regional conflicts, high defense spending, and continuous procurement of military equipment and supplies. The countries in the MEA region, particularly in the Middle East, are investing heavily in highly advanced military equipment and ammunition supplies. Additionally, in Africa, internal security issues and peace-keeping operations also contribute significantly to ammunition market growth in this region. Moreover, military modernization and border security concerns in this region also contribute significantly to ammunition market growth.

Ammunition Market Competitive Landscape:

Northrop Grumman Corporation, headquartered in Falls Church, Virginia, USA, is a leading global aerospace and defense technology company and a key player in the ammunition market, specializing in advanced munitions, precision-guided systems, and large-caliber ammunition for military applications. The company focuses on innovation, next-generation weapon systems, and integrated defense solutions, emphasizing technological superiority, reliability, and long-term government contracts.

-

In February 2025: Northrop Grumman secured a major contract to supply advanced precision-guided munitions to the U.S. Department of Defense, strengthening its position in next-generation ammunition systems.

General Dynamics Corporation, headquartered in Reston, Virginia, USA, is a major global defense company and a prominent player in the ammunition market through its Ordnance and Tactical Systems segment, offering a wide range of small, medium, and large-caliber ammunition. The company emphasizes high-performance munitions, advanced manufacturing capabilities, and long-term defense partnerships, supporting military and law enforcement operations worldwide.

-

In January 2025: General Dynamics expanded its ammunition production capacity in the U.S. to meet increasing demand from defense agencies and international allies, enhancing supply chain resilience.

Ammunition Market Key Players:

-

Northrop Grumman Corporation

-

General Dynamics Corporation

-

BAE Systems plc

-

Rheinmetall AG

-

Thales Group

-

Nammo AS

-

Olin Corporation (Winchester Ammunition)

-

Vista Outdoor Inc.

-

FN Herstal

-

CBC Global Ammunition (Companhia Brasileira de Cartuchos)

-

RUAG Group

-

Elbit Systems Ltd.

-

Saab AB

-

Denel SOC Ltd.

-

Poongsan Corporation

-

MESKO S.A.

-

Israel Weapon Industries (IWI)

-

ST Engineering

-

Hirtenberger Defence Systems

-

Nexter Group (KNDS)

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 29.94 Billion |

| Market Size by 2035 | USD 42.65 Billion |

| CAGR | CAGR of 3.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application: (Defense, Military, Homeland Security, Civil & Commercial, Sporting, Hunting, Self-defense) • By Caliber: (Small Caliber, Medium Caliber, Large Caliber) • By Product: (Bullets, Aerial Bombs, Artillery Shells, Mortars) • By Lethality: (Lethal, Less-lethal) • By Component: (Fuzes & Primers, Propellants, Bases, Projectiles and Warheads, Others) • By Guidance Mechanism: (Guided, Non-Guided) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Northrop Grumman Corporation, General Dynamics Corporation, BAE Systems plc, Rheinmetall AG, Thales Group, Nammo AS, Olin Corporation (Winchester Ammunition), Vista Outdoor Inc., FN Herstal, CBC Global Ammunition (Companhia Brasileira de Cartuchos), RUAG Group, Elbit Systems Ltd., Saab AB, Denel SOC Ltd., Poongsan Corporation, MESKO S.A., Israel Weapon Industries (IWI), ST Engineering, Hirtenberger Defence Systems, Nexter Group (KNDS) |

Frequently Asked Questions

The Ammunition Market is expected to grow at a CAGR of 3.60% during 2026–2035.

The market was valued at USD 29.94 Billion in 2025 and is projected to reach USD 42.65 Billion by 2035.

The key drivers of the Ammunition Market include rising defense spending, military modernization, geopolitical tensions, growing law enforcement needs, civilian firearm demand, and advancements in smart, precision ammunition.

The Defense & Military segment dominated during the projected period.

North America dominated the Ammunition Market in 2025.

Get in Touch