Anhydrous Hydrogen Fluoride Market Report Scope & Overview:

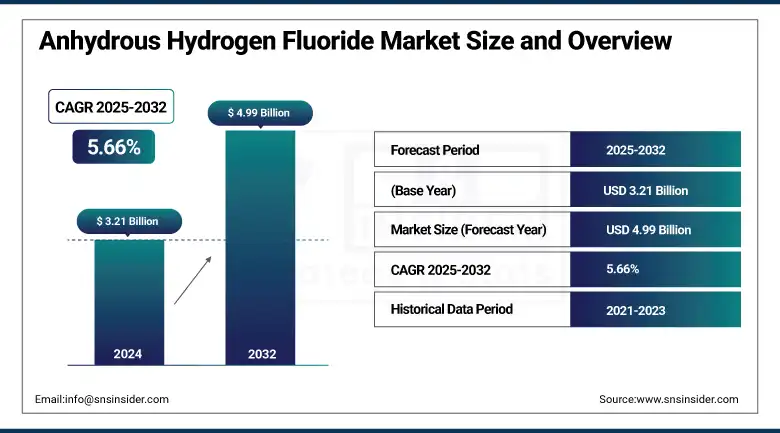

The Anhydrous Hydrogen Fluoride market size was valued at USD 3.21 billion in 2024 and is expected to reach USD 4.99 billion by 2032, growing at a CAGR of 5.66% over the forecast period of 2025-2032.

The anhydrous hydrogen fluoride market growth is fuelled by the high requirement of high-purity anhydrous hydrogen fluoride in semiconductor etching, petroleum alkylation, and stainless-steel pickling. The anhydrous hydrogen fluoride market trends are sustainability efforts and capacity expansions. Solvay completed an upgrade of its Ciudad Juarez facility to increase local supply, and Chemours and Honeywell further expanded a reclaim program in the EU and the U.K., respectively, to support circular economy ambitions.

To Get more information On Anhydrous Hydrogen Fluoride Market - Request Free Sample Report

According to the U.S. Geological Survey, Hydrofluoric acid is still the primary input for the vast majority of fluorine-containing compounds, and is widely used in Texas and Louisiana. Solvay has three large hubs spread globally, dedicated to the growth of anhydrous hydrogen fluoride. The U.S. Geological Survey 2023 data continue to underscore the strategic value of acid-grade fluorspar in the U.S. industrial consumption, supporting anhydrous hydrogen fluoride market studies and supply chain reliability.

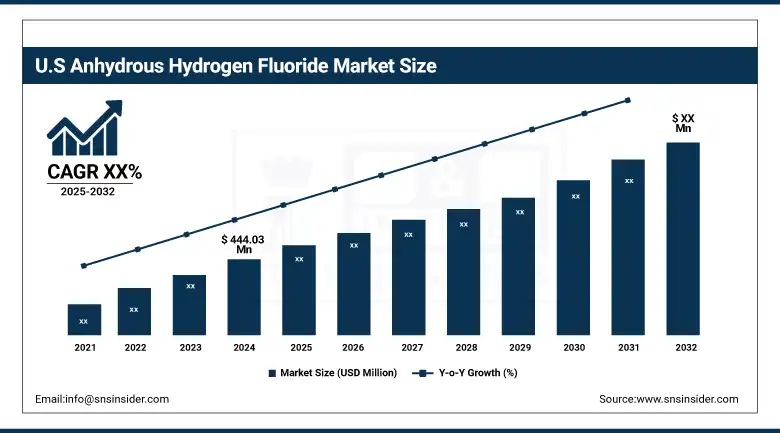

The U.S market leads with a market valuation of USD 444.03 million and market share of around 56% in 2024

Market Dynamics:

Drivers:

-

Petrochemical Refinery Upgrades Amplify Acid-Grade Anhydrous Hydrogen Fluoride Consumption

Worldwide refinery modernizations to meet tighter sulfur regulations for low-sulfur fuels are raising demand for the acid-grade anhydrous hydrogen fluoride needed in alkylation units. Five large U.S. refineries have undertaken alkylation unit upgrades in 2023 and are projected to consume about 8% more hydrofluoric acid than they did in 2022, the U.S. Energy Information Administration said. These installations make it possible to produce higher-octane gasoline, with the added benefit of reducing olefins, and contribute to securing the position of hydrofluoric acid as an essential catalyst. Major petrochemical companies, such as ExxonMobil and Shell have announced multi-year hydrogen fluoride contracts to 2027. This further underlines a robust anhydrous hydrogen fluoride market share and long-term demand. This trend further reinforces the overall anhydrous hydrogen fluoride market size and indicates the need for strong anhydrous hydrogen fluoride market analysis.

-

Expansion of Semiconductor Fabrication Centers Drives High-purity Anhydrous Hydrogen Fluoride Demand

The presence of wafer fabrication plants in North America and Asia is driving substantial consumption of high-purity anhydrous hydrogen fluoride (AHF) in silicon wafer etching and chamber cleaning. To back up this demand, Thiele said the USGS had observed a 12% year-on-year increase in the use of acid-grade fluorspar feedstock in 2023, due to a 20% rise in global semiconductor etching capacity. Top anhydrous hydrogen fluoride firms, such as Solvay and DuPont, have answered with new purification systems providing sub-5 ppm hydrogen fluoride purity to satisfy stringent semiconductor needs. This is a result of very strong growth in the anhydrous hydrogen fluoride market and suggests the necessity of focused and dedicated anhydrous hydrogen fluoride market research to assist investment decisions in the anhydrous hydrogen fluoride sector.

Restraints:

-

Safety concerns and handling complexities hinder the wider adoption of anhydrous hydrofluoric acid

Anhydrous hydrofluoric acid is deadly and burns through everything, necessitating significant safety measures too expensive for some smaller chemical companies to implement. In 2022, the National Institute for Occupational Safety and Health identified more than 120 incidents of hydrofluoric acid exposure in the workplace. OSHA, in turn, responded by enacting more stringent safety requirements, including enhanced personal protective equipment and specialized operator training. These steps are not only arduous, but they are also expensive, about USD 250,000 per facility, creating obstacles to entry for new or cash-strapped companies. This has led to companies within the developing regions not wanting to be early adopters of hydrogen fluoride-based processes despite the potential technical benefits, and thus restricting the taking of anhydrous hydrogen fluoride market share in many regions globally.

Segmentation Analysis:

By Purity

The <99.90% purity segment accounted for the largest share of about 63% in 2024. The strength of this segment is underpinned by broad utilization in industries needing lower purity grade, notably petrochemical alkylation and metal pickling. Acid-grade fluorspar consumption in petroleum processing plants rose by 8% in 2023, in strong feedstock conversion as reported by the USGS. Solvay, Honeywell, and other large suppliers have high production capacity for sub-99. 90% grades, guaranteeing stable supply chains and strengthening segment leadership and reliability.

The 99.90% purity segment is the fastest-growing anhydrous hydrogen fluoride market with a CAGR of 6.19%. The growing requirement for ultra-high-purity acid in semiconductor etching and pharmaceutical synthesis drives the market to invest in advanced fluorination facilities. The Semiconductor Industry Association projected a 15% jump in wafer starts needing ultra-low impurity hydrogen fluoride in 2023, highlighting the continued necessity of precision etching. The growth of companies, including DuPont and Solvay, has been adding on purification trains, underscoring purity as a key anhydrous hydrogen fluoride market trend in purity-driven technological applications.

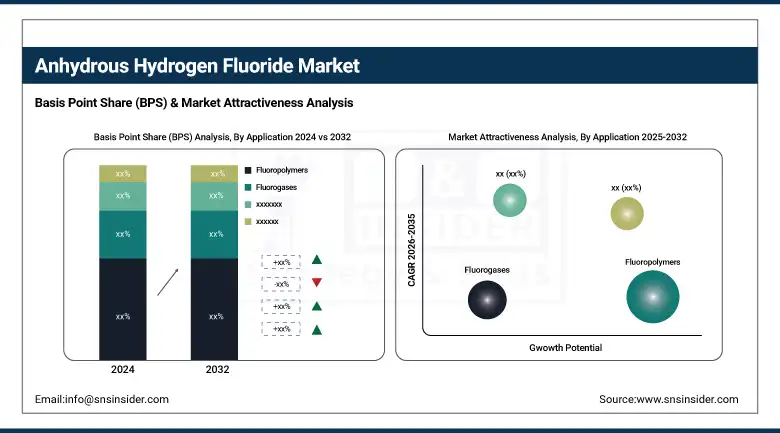

By Application

The fluorogases sector led the anhydrous hydrogen fluoride market in 2024 and is projected to have a consensus market offering of about 37.4%. Demand is fueled by evolving refrigeration rules, particularly the U.S. EPA's phase-down schedules under the Clean Air Act for low-global-warming-potential hydrofluorocarbons. Honeywell and Chemours increased the output of HFC-134a by 10% in 2023 for use in air conditioning and refrigeration. Fluorogases’ long-term supply agreements with leading OEMs exemplify its importance as the elite anhydrous hydrogen fluoride trendsetter toward eco-safe refrigerants and strong partnerships across the globe.

The fluoropolymers segment is the fastest growing amongst the anhydrous hydrogen fluoride market, which is projected to have a CAGR of 6.29%. Its growth prospects are supported by the increasing use of polytetrafluoroethylene and other high-performance polymers in segments, such as medical devices and electronics. According to the world-leading U.S. Chemical Safety Board, there was a 12% increase in output of fluoropolymer plants utilizing ultra-high purity hydrogen fluoride lines in 2023. Companies, such as DuPont and 3M are introducing new polymerization reactors in what is eying the important anhydrous hydrogen fluoride industry trends for specialty polymer applications.

By End Use

The chemical industry was the leading application area in 2024, accounting for revenue worth 35.6%, owing to its prominent usage in manufacturing fluorosilicic acid and aluminum fluorides. Hydrogen fluoride consumption by chemical makers in 2023 would increase 9% over current U.S. Geological Survey data, with growth in catalyst synthesis for petroleum refining. Leading players, including Solvay and Arkema, provide hydrogen fluoride grades for acid treatment in this regard, pointing toward steady, robust global demand, and the responsibility of the chemical industry.

Semiconductor is the fastest-growing segment in the anhydrous hydrogen fluoride market and is expected to grow at a CAGR of 5.44%. Rise in advanced node fabrication and packaging techniques has led to an increase in demand for ultra-pure hydrogen fluoride for etching and chamber cleaning. 2 US wafer fab investments are up 22% for 2023, with notable players including Intel and TSMC building new lines that will need hydrogen fluoride, according to the U.S. Department of Commerce. This fad marks the expansion of the anhydrous hydrogen fluoride market due to the semiconductor end-user advancement.

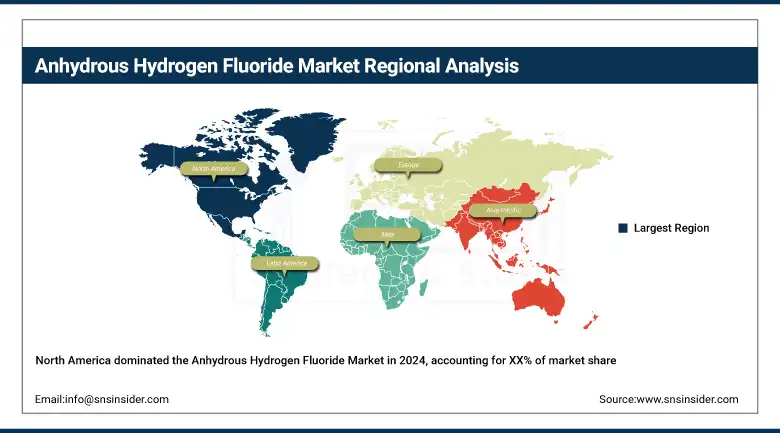

Regional Analysis:

North America is expected to be the fastest-growing region with a CAGR of 6.43% during the forecast period of 2025 to 2032. The growth of the anhydrous hydrogen fluoride market is gaining traction, owing to the increasing investments in the semiconductor manufacturing and refinery upgradation activities. The U.S. Department of Commerce stated that wafer starts needing ultra-high-purity anhydrous hydrogen fluoride in 2023 would rise by 22%, fueling demand for sub-5 ppm acid among Arizona and New Mexico fabs. In the meantime, upgrades to Gulf Coast alkylation units have contributed to an 8% year-on-year gain in hydrofluoric acid use, the U.S. Energy Information Administration says. Major anhydrous hydrogen fluoride suppliers including Solvay and DuPont have established long-term contracts and increased their purification capacities amid robust market growth, consolidating North America’s position as the fastest-growing regional market.

Get Customized Report as per Your Business Requirement - Enquiry Now

The anhydrous hydrogen fluoride market in Europe is the second largest and is driven by regulations on environmental policies as well as capacity additions in major chemical clusters. In Germany, the Marl and Schkopau locations expanded their hydrogen fluoride production capacities by 10% in 2023 to meet European Chemicals Agency emission standards and to feed downstream fluorosilicate and aluminum fluoride production. The Netherlands achieved logistics efficiency with new state-of-the-art double-walled tanker terminals meeting ECHA transport standards, resulting in a reliable supply for France’s industrial parks (where recycled hydrofluoric acid from Chemours’ EU pilot program is provided). This momentum, driven by regulation, reflects the strong European market share and shift to sustainable hydrogen fluoride usage.

Asia Pacific leads the anhydrous hydrogen fluoride market with 34.2% share due to the large refinery and petrochemical projects in China, and semiconductor node transitions in South Korea. According to China’s National Bureau of Statistics, new hydrogen fluoride production for alkylation units in 2023 will increase by 15% to comply with more stringent domestic fuel standards. The trend has been confirmed by the South Korea Ministry of Trade, which reported a 20% increase in the import of ultra-high purity hydrogen fluoride used for advanced etching at Samsung and SK Hynix fabs in recent years, a testament to the technological precedence of the region. This dual activity illustrates dynamic market dynamics and reinforces the dominance of Asia Pacific.

Anhydrous hydrogen fluoride demand in Latin America is growing as a consequence of Brazil refinery alkylation capacity expansions and Mexico chemical park additions. Brazil’s ANP had projected 7% growth in hydrogen fluoride alkylation capacity in 2023 to assist compliance with biofuel blending requirements. In Mexico, the new Veracruz chemical parks each finalized their long-term offtakes with Solvay for sub-99. 90% anhydrous hydrogen fluoride to supply the petrochemical and metal finishing industries. These strategic actions highlight Latin America’s increasing market share and trajectory towards local hydrogen fluoride supply.

The Middle East & Africa anhydrous hydrogen fluoride market is projected to be propelled by the refinery investments in the Gulf and growth in the industrial applications. Saudi Aramco’s new HYDROGEN FLUORIDE alkylation units in the Duqm refinery began operation in late 2023, increasing acid demand for high-octane gasoline production, according to Aramco’s annual review. Meanwhile, South Africa’s Department of Mineral Resources registered a 5% rise in imports for use in specialty chemicals in 2023, suggestive of early demand in the mining and industrial sectors. These are evidence of the region’s growth potential and important sectoral collaboration.

Key Players:

The major anhydrous hydrogen fluoride market competitors include Honeywell International Inc., Solvay S.A., Linde plc, Arkema S.A., Lanxess AG, Navin Fluorine International Limited (NFIL), Daikin Industries, Ltd., Mexichem S.A.B. de C.V. (Orbia/Koura), GFL Limited (Gujarat Fluorochemicals Ltd.), and Foosung Co., Ltd.

Recent Developments:

-

In September 2024, the EPA issued an alert against illegal hydrofluorocarbon imports, downstream products of anhydrous hydrogen fluoride, leading to stricter customs enforcement and boosting demand for domestically sourced feedstock in the fluorogases supply chain.

-

In December 2024, Solvay launched a large biodigester at its Ciudad Juarez anhydrous hydrogen fluoride facility, improving waste management and supporting steady regional supply for refinery alkylation and high-purity applications in semiconductor etching.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.21 billion |

| Market Size by 2032 | USD 4.99 billion |

| CAGR | CAGR of 5.66% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Purity (>99.90%, <99.90%) •By Application (Fluoropolymers, Fluorogases, Pesticides, Others) •By End Use (Chemical industry, Semiconductor industry, Electronics industry, Automotive industry, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Honeywell International Inc., Solvay S.A., Linde plc, Arkema S.A., Lanxess AG, Navin Fluorine International Limited (NFIL), Daikin Industries, Ltd., Mexichem S.A.B. de C.V. (Orbia/Koura), GFL Limited (Gujarat Fluorochemicals Ltd.), and Foosung Co., Ltd. |

Frequently Asked Questions

Asia Pacific leads with 34.2% share, supported by China’s refinery projects and South Korea’s semiconductor growth.

Strict environmental regulations and capacity expansions in Germany and the Netherlands drive Europe’s stable market share.

North America leads growth due to refinery upgrades and semiconductor fabrication investments boosting hydrogen fluoride consumption.

The <99.90% purity segment led the market with 63.3% share in 2024 due to widespread industrial applications.

The anhydrous hydrogen fluoride market was valued at USD 3.21 billion in 2024 and is projected to reach USD 4.99 billion by 2032.

Get in Touch