Post-Harvest Treatment Market Report Scope & Overview:

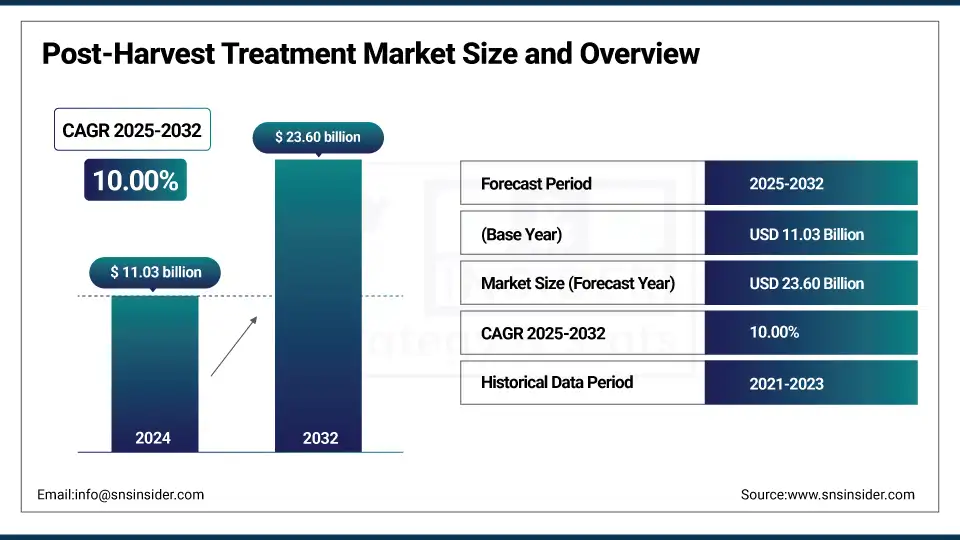

The Post-Harvest Treatment market size was valued at USD 11.03 billion in 2024 and is expected to reach USD 23.60 billion by 2032, growing at a CAGR of 10.00% over the forecast period of 2025-2032.

One key factor driving the market growth is the growing global focus on food loss post-harvest treatment, with FAO estimating that more than 14 million tonnes of food are lost for every 1% in loss between harvest and sale post-harvest treatment market trends which are driving the demand of hot water treatment, ethylene inhibitors, and biological control amongst others proves notable in sustaining shelf life of produce. AgroFresh, Pace International, and a few other companies have introduced the new generation coatings along with decay control products for meeting stringent global MRL standards. In 2024, USDA initiated numerous funding programs catering to the development of cold storage infrastructure, strengthening the post-harvest treatment market.

To Get more information On Post-Harvest Treatment Market - Request Free Sample Report

Advancements in supply chain logistics and smart packaging have been affecting the division of the post-harvest treatment market share. These post-harvest treatment companies are looking for AI-enabled quality monitoring systems to create synthetic datasets. According to the 2023 USDA announcement, $300 million of funding has been set aside for improving food preservation techniques. This detailed post-harvest treatment research report not only helps you in increasing revenue but also helps you build a model to grow your business, ultimately gaining traction globally.

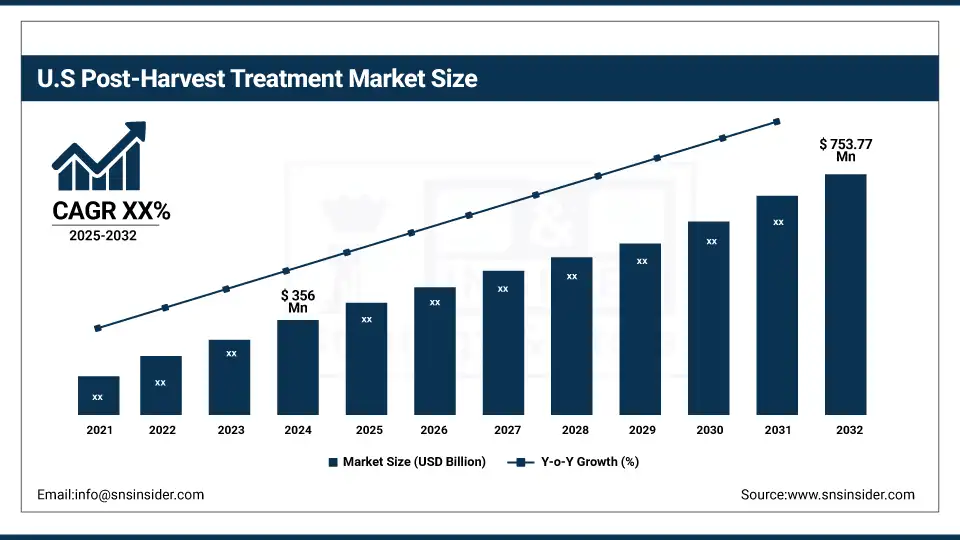

U.S USD 356 million in 2024 and is projected to reach a value of USD 753.77 million by 2032, buoyed by USDA funding and packhouse innovation, with Canada trailing behind as BC and Alberta receive strong provincial support for cold chain. Continuing demand from key apple, citrus, and berry supply chains for disease-control sprays, coatings, as well as ethylene inhibitors drives high consumer uptake.

Market Dynamics:

Drivers:

-

Rising Consumer Preference for Plant-Based Preservation Elevates Innovation Incentive

The post-harvest treatment market growth is attributed to the increasing demand for residue-free freshness from consumers, which has risen amid the growing preference for plant-based coatings and ethylene blockers. Agtech startups are collaborating with academic institutions to utilize natural antimicrobials. The nation's food safety benchmarks that government agencies are beginning to see a greater number of biological treatments being registered. This adoption trajectory is encouraging post‑harvest treatments companies, both established and emerging, to market bio-based solutions that not only enhance shelf life but also support sustainability and food safety mandates.

-

Increasing Cold‑Chain Integration Reduces Spoilage and Enhances Quality Retention

Increasing temperature-controlled logistics in different regions is helping to reduce post-harvest loss by reducing spoilage during transit. Dynamic trends Smart sensor-equipped cold storage for perishables, which is used in the health care sector. Upgraded infrastructure resulted in a reduction of more than 15% of spoilage, according to development agencies. The rapid technological evolution has given impetus to cold storage solutions providers and farming cooperatives to integrate new cooling and monitoring systems that ensure the freshness from harvest to retail.

Restraints:

-

Crop-Specific Physiological Differences Challenge Treatment Standardization Across Varieties

Non-uniform deployment of Food Security Solutions is due to the different traits such as respiration rate, skin porosity, and moisture levels. Crop-specific treatment protocols make scaling difficult and increase complexity. Research has shown that this varies significantly with the species; for example, tender fruits need to be prepped in a way so they do not get infected. This crop‑specific adjustment necessity increases the research and development costs, time to test, especially for post‑harvest suppliers targeting multi-crop exporters, and places operational limitations on rapid implementation.

Segmentation Analysis:

By Origin

Synthetic held a dominant post-harvest treatment market share of 63.2% in 2024, due to increasing demand for synthetic as it is more efficient compared to natural hormones and used across large-scale commercial applications with consistent performance against microbial spoilage/decay or pest activities. Synthetic pesticides are convenient to formulate, have a longer shelf life, and are approved in all major regions for fruits and vegetables. While organic production for store sweetening is increasing among consumers, the economies of scale of high-output agricultural economies have maintained synthetics as the lingua franca following harvest.

Natural treatments are the fastest growing with the highest CAGR of 9.2% during the forecast period from 2025 to 2032, on account of surging consumer demand for residue-free produce, growing trend towards organic farming practices, and extensive laws regarding synthetic residues. Such desires are met by bio-based coatings, plant-derived fungicides, and edible waxes. The growing government subsidies and R&D investments have also supported the adoption, particularly among small-scale growers and organic packhouses in the Asia Pacific and North America.

By Product

Coatings held a dominant post-harvest treatment market share of 37.6% in 2024, as they help extend shelf-life by reducing moisture-loss, respiration, and microbial growth. These edible films and waxes are rinse-less and are used on citrus, apples, and tropical fruits. Further, the preference for multifunctional coatings, combining both fungicidal and ripening inhibition properties, is increasing with advancing technologies across the supply chain. Apart from preserving the texture over long storage periods, coatings also prevent visual contamination.

Ethylene blockers are the fastest growing with the highest CAGR of 9.7% during the forecast period from 2025 to 2032, largely led by their effectiveness in prolonging ripening and senescence in climacteric fruits like bananas, avocados, tomatoes, etc. They interfere with ethylene receptors and are developed to prevent post-harvest losses incurred in export markets. Increasing trade volumes, consumer demand for fruits & vegetables, and new formulations of 1-MCP are fueling demand, with APAC and Latin America accounting for the highest consumption.

By Crop Type

Fruits and vegetables held a dominant post-harvest treatment market share of 56.8% in 2024, as they are highly perishable and prone to microbial spoilage, moisture loss, and physiological disorders. These also include coatings, fungicides, and sanitizers to extend the shelf-life, export quality, and meet the phytosanitary regulations. This dominance is also facilitated through demand for fresh produce, shelf-life requirements in retail, and post-harvest activation investments that horticultural supply chains promote.

Flowers and ornamentals are the fastest-growing with the highest CAGR of 8.6% during the forecast period from 2025 to 2032, as there is an increase in global demand for fresh-cut flowers, mainly for roses, chrysanthemums, and lilies. Efforts for post-harvest handling through ethylene control, microbial contamination, and moisture retention treatment are increasing export preparedness and vase life. Prosperous e-commerce floral sales, widespread access to flower auctions, and innovations in preservative solutions are further accelerating the growth of this lucrative market.

By Application

Disease control held a dominant post-harvest treatment market share of 48.9% in 2024, on account of the extensive use of fungicides and disinfectants, which prevent decay due to molds & bacteria during storage and transit. They are crucial for such high-revenue crops as citrus, apples, and potatoes. The increasingly large volume of produce being traded globally and longer supply chains associated with this escalating trade make it more important to address disease control in a manner that minimizes economic losses and regulatory rejections.

Ripening inhibition is the fastest growing with the highest CAGR of 9.1% during the forecast period from 2025 to 2032, due to the growing demand for longer shelf-life produce quality in transit. Suppression of ethylene blockers and temperature-controlled logistics allow businesses to defer ripening of fruits such as mangoes and bananas until they are brought on the shelves of the point-of-retail. In addition, the growing consumer inclination towards convenient, ready-to-eat fresh fruits is accelerating innovation in this category across the globe.

By Mode of Application

Spraying held a dominant post-harvest treatment market share of 51.3% in 2024, owing to its effective and uniform application of coatings, sanitizers, nutrient solutions, and fungicides for large produce volumes. This method is affordable, works with a variety of formulations, and can be used on both manual and automated systems. This is widely used in the fruit, vegetable, and grain packing facilities. Low-drift nozzles and the like are increasing efficacy by reducing drift and waste.

Coating is the fastest-growing segment with the highest CAGR of 8.9% during the forecast period from 2025 to 2032, driven by the dual feature of edible coatings for maintaining moisture and microbial control. They work particularly well for apples, citrus, and tropical fruits. Organic growers and exporters are increasingly turning to the bio-based and biodegradable versions. The possibility of transporting products by coating them makes the coatings useful for those regions in which cold storage is limited, but where demand is also increasing.

By End User

The Packers held a dominant post-harvest treatment market share of 41.2% in 2024, as they maintain a central position for massive processing volume, segregation, and packaging of produce prior to distribution. Their manufacturing expertise in industrial-grade infrastructure, integration with cold chain logistics, and compliance with export quality standards are key players who stand to expand the shelf life of fresh produce. As part of overall compliance and efficiency, Packers continue to use synthetic/next-level coating technologies.

Growers are the fastest growing with the highest CAGR of 8.6% during the forecast period from 2025 to 2032, owing to growing understanding about post-harvest losses, direct farm-level usage of treatments, and government initiatives supporting sustainable agriculture. This prompts producers to turn to on-farm, natural, and eco-friendly post-harvest solutions, making supply chain players a major driver in emerging markets.

Regional Analysis:

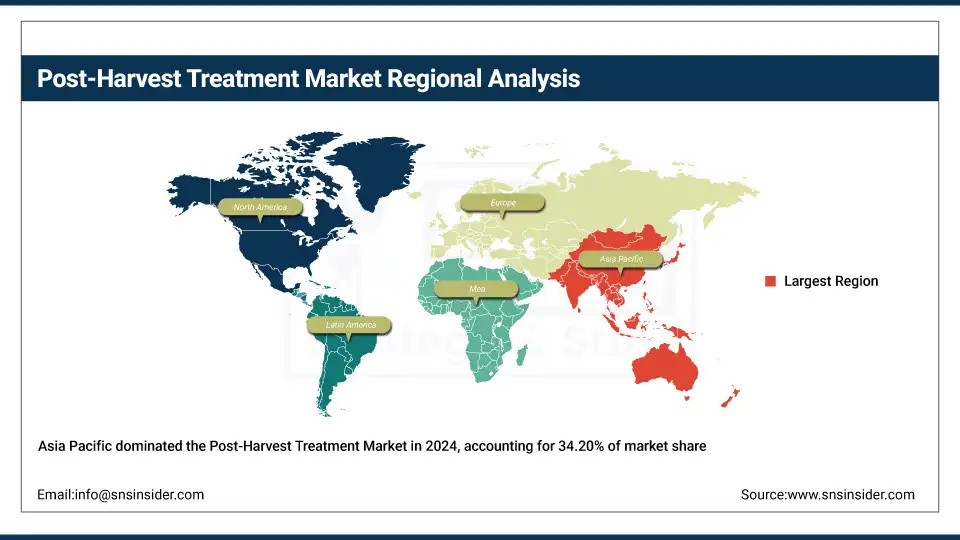

Asia Pacific dominates with a 34.20% share and is the fastest-growing region with the highest CAGR of 10.28% between 2025 and 2032, owing to the growing agricultural export business and investments in technologies for storing agricultural produce. Temperature-control logistics are increasingly being adopted, with coatings, ethylene blockers, and government programs like India's post-harvest loss reduction initiative well-established in countries like China, India, Thailand, and Vietnam. Growth driven by fast modernization in both smallholder-commercial systems

Get Customized Report as per Your Business Requirement - Enquiry Now

North America holds the second-dominating position with a market share of 26.40%, due to its strong post-harvest management system and product standards. The U.S. is the leader in the region, holding a market share of about 73% with a market size of U.S USD 356 million in 2024 and is projected to reach a value of USD 753.77 million by 2032, buoyed by USDA funding and packhouse innovation, with Canada trailing behind as BC and Alberta receive strong provincial support for cold chain. Continuing demand from key apple, citrus, and berry supply chains for disease-control sprays, coatings, as well as ethylene inhibitors drives high consumer uptake.

Europe holds third place, accounting for 21.70% of the market, with crop protection legislation and sustainability trends underpinning further growth. The requirement to export horticultural produce has been the key driver behind its implementation by Germany, Spain, and the Netherlands due to restrictive post‑harvest residue limit requirements of the EU. The major national initiatives in cold storage modernization in Germany and grants for post‑harvest quality projects in Spain both have the same effect of increasing potential to invest. It is in this dynamic regulatory focus area and significant export to fresh plant produce that Europe resides, supported globally by the Asia Pacific, but from a position of being able to grow its capability only within limits.

Key Players:

The major post-harvest treatment market competitors include AgroFresh Solutions, Inc., Citrosol, Hazel Technologies Inc., JBT Corporation, Lytone Enterprise Inc., Xeda International S.A.S., Colin Campbell Chemicals Pty Ltd., Fomesa Fruitech, PostHarvest Technologies, Post Harvest Solution Ltd., Fine Chemicals Inc., Apeel Sciences, Sufresca Ltd., KitoZyme, LLC, Ceradis B.V., Jingold S.p.A., Symbiotech Research Pvt. Ltd., NTC Agri, Agrosta SARL, and Decco Ibérica Postcosecha S.A.U.

Recent Developments:

-

In May 2025, JBT Marel showcased its new ozone-based sanitization equipment for fruits and vegetables at IFFA 2025 in Frankfurt, highlighting enhanced microbial control and reduced chemical residues

-

In January 2025, Citrosol unveiled its CATsystem automatic control platform and GREENFOG-AS fumigant system at Fruit Logistica 2025 in Berlin

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 11.03 billion |

| Market Size by 2032 | USD 23.60 billion |

| CAGR | CAGR of 10.00% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Origin (Natural, and Synthetic) •By Product (Coatings, Cleaners, Fungicides, Insecticides, Ethylene Blockers, Sanitizers, and Others) •By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables, Flowers & Ornamentals, and Others) •By Application (Disease Control, Ripening Inhibition, Moisture Retention, Disinfection, and Others) •By Mode of Application (Spraying, Dipping, Fumigation, and Coating) •By End User (Growers, Packers, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | AgroFresh Solutions, Inc., Citrosol, Hazel Technologies Inc., JBT Corporation, Lytone Enterprise Inc., Xeda International S.A.S., Colin Campbell Chemicals Pty Ltd., Fomesa Fruitech, PostHarvest Technologies, Post Harvest Solution Ltd., Fine Chemicals Inc., Apeel Sciences, Sufresca Ltd., KitoZyme, LLC, Ceradis B.V., Jingold S.p.A., Symbiotech Research Pvt. Ltd., NTC Agri, Agrosta SARL, and Decco Ibérica Postcosecha S.A.U. |

Frequently Asked Questions

Asia Pacific leads in growth due to rising exports, government support, and rapid adoption of advanced post-harvest treatment solutions across emerging economies.

The market enhances food security by enabling agricultural produce preservation, reducing spoilage, and improving quality through effective post-harvest management practices.

Major post-harvest treatments companies include AgroFresh, Citrosol, JBT Corporation, Apeel Sciences, and Hazel Technologies, known for innovations in bio-based solutions.

Growth is driven by demand for sustainable crop protection, cold-chain expansion, and adoption of smart post-harvest technology, reducing spoilage and extending shelf life.

The post-harvest treatment market is projected to grow at a CAGR of 10.00% from 2025 to 2032, driven by rising global food loss concerns.

Get in Touch