Wood Coatings Market Report Scope & Overview:

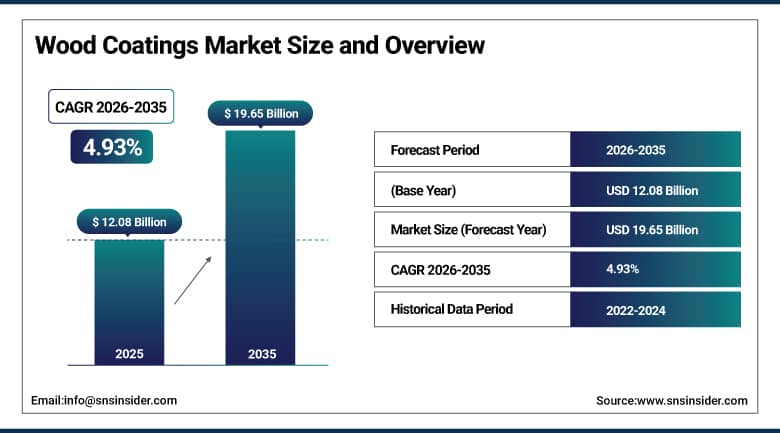

Wood Coatings Market was valued at USD 12.08 billion in 2025 and is expected to reach USD 19.65 billion by 2035, growing at a CAGR of 4.93% from 2026-2035.

Wood surfaces in furniture, flooring, cabinetry, architectural millwork, and exterior cladding represent one of the most commercially demanding coating substrates in the finishing industry dimensionally unstable with seasonal moisture cycling, naturally porous with species-specific absorption variability, aesthetically evaluable at a level that consumers apply more scrutiny to than painted metal or concrete, and required to perform under conditions ranging from kitchen heat and humidity through exterior UV and rain exposure. Wood coatings must simultaneously provide protective performance moisture exclusion, abrasion resistance, UV stability, chemical resistance and aesthetic enhancement colour depth, grain clarification, gloss or sheen level control in formulations that apply efficiently in high-volume industrial spray finishing environments and that remain stable long-term through the expansion and contraction that wood's hygroscopic character imposes. The demand from global furniture manufacturing where Asia-Pacific furniture production for export creates the world's largest wood coating consumption base alongside the growing renovation and home improvement markets in developed economies and the progressive transition from solvent-based to waterborne coating formulations driven by environmental regulation.

The China National Furniture Association documents that China accounts for over 40% of global furniture exports creating the world's largest single national wood coating consumption market whose production volumes for the global furniture trade dwarf any other national furniture industry. The American Hardwood Export Council's 2024 market report documents that residential renovation spending in the U.S. exceeded USD 500 billion sustaining floor refinishing, cabinet repainting, and interior millwork coating demand that sustains U.S. wood coating retail and professional markets.

Wood Coatings Market Size and Forecast

- Market Size in 2025: USD 12.08 Billion

- Market Size by 2035: USD 19.65 Billion

- CAGR: 4.93% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026-2035

- Historical Data: 2022-2024

To Get More Information On Wood Coatings Market - Request Free Sample Report

Wood Coatings Market Trends

- UV-curable waterborne coatings combining the zero-solvent environmental benefits of waterborne formulations with UV cure's instantaneous cross-linking speed are replacing both conventional waterborne and UV-cured solventborne coatings in the furniture manufacturing segment where production line speed and VOC compliance are simultaneously required.

- Bio-based wood coating resins derived from natural oils (linseed, tung, soybean), bio-based polyols, and plant-derived monomers are creating commercially viable sustainable coating alternatives whose renewable content credentials are becoming differentiating factors in the premium furniture and flooring markets.

- Nano-technology enhanced wood coatings incorporating nano-silica, nano-clay, or nano-TiO2 particles into coating formulations are delivering hardness, scratch resistance, and UV protection properties that traditional organic coating chemistry cannot achieve at equivalent film thickness.

- Anti-fingerprint and easy-clean coating treatments providing hydrophobic or oleophobic surface properties that prevent fingerprint and food residue adhesion on kitchen furniture and cabinetry are growing as consumer preference for low-maintenance premium finishes drives product development investment at major coating brands.

- Digital printing on wood where inkjet printing systems deposit wood-grain images, decorative patterns, or custom colors on MDF and wood substrates before topcoat application is creating new premium finishing aesthetics that sustain coating demand even as printing replaces conventional staining in some decorative wood applications.

- Waterborne 2K polyurethane coatings two-component systems whose isocyanate crosslinkers deliver solventborne performance levels in waterborne formulations are capturing the professional wood finishing market's most demanding durability applications where single-component waterborne coatings cannot provide equivalent chemical and abrasion resistance.

- Smart wood coatings providing color-changing or photoluminescent functionality finding application in luxury furniture and architectural accents represent an emerging premium market segment whose novelty sustains price premiums above standard decorative coating categories.

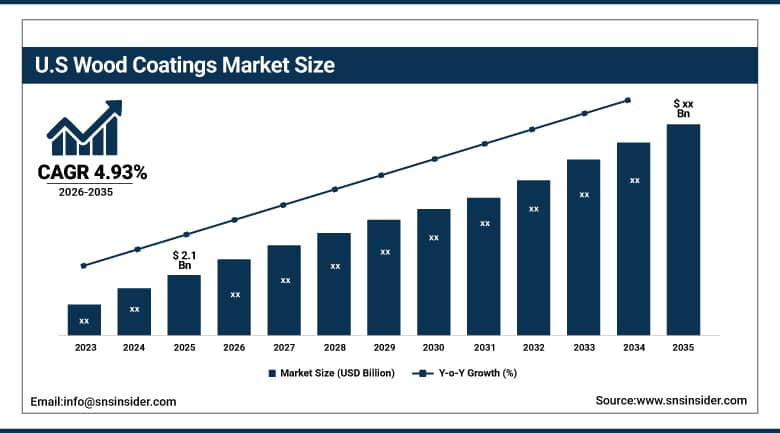

U.S. Wood Coatings Market was valued at approximately USD 2.1 billion in 2025 and is expected to grow at a CAGR of 4.93% from 2026-2035.

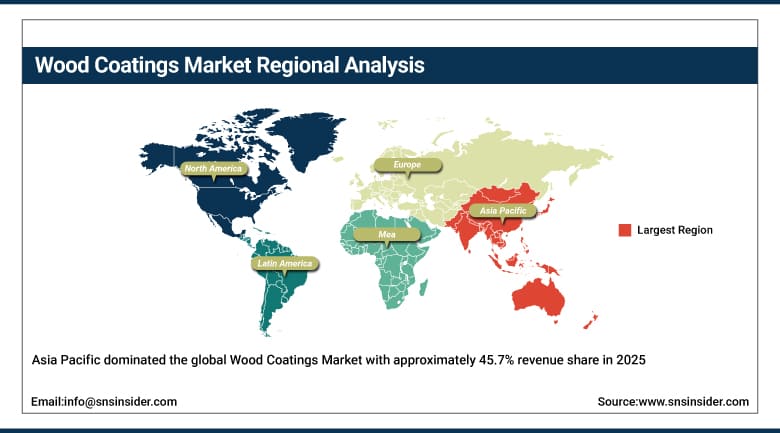

Asia Pacific dominated the global Wood Coatings Market with approximately 45.7% revenue share in 2025, driven by China's enormous furniture manufacturing export industry which produces furniture for global markets including IKEA, Walmart, and hundreds of European and North American retailers and the domestic furniture markets of India, Vietnam, Indonesia, and South Korea that collectively create the world's highest concentration of wood coating consumption. China's furniture manufacturing cluster concentrated in Guangdong, Zhejiang, and Fujian provinces applies wood coatings at production volumes whose aggregate demand sustains the global operations of coating majors including Sherwin-Williams, AkzoNobel, Nippon Paint, and domestic Chinese coating companies including Guangdong Huarun and Carpoly. Vietnam's furniture manufacturing sector which has grown to become the world's second-largest furniture exporter as global supply chains diversified away from exclusive China dependence creates additional APAC wood coating demand whose growth rate exceeds China's more mature market.

Vietnam's General Statistics Office documents that Vietnam's furniture export revenue reached USD 14.8 billion in 2023 making Vietnam the world's second-largest furniture exporter after China sustaining a wood coating import and domestic production market whose growth rate of 12-15% annually consistently exceeds the global wood coatings market average. India's furniture market projected by the Indian Furniture & Fixtures Manufacturers' Association to grow from USD 20 billion to USD 37 billion by 2028 creates rapidly expanding wood coating demand from both organized furniture manufacturing and the vast unorganized carpentry and joinery sector.

Wood Coatings Market Segment Analysis

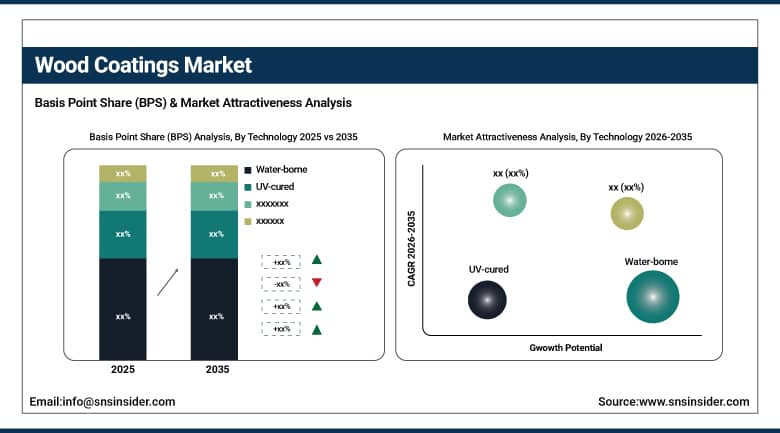

- By Technology , Waterborne dominated the Wood Coatings Market in 2025 driven by environmental regulations; UV-Cured growing fastest.

- By Resin Type, Polyurethane dominated the Wood Coatings Market in 2025 due to superior durability and abrasion resistance; Acrylic growing fastest driven by low-VOC and waterborne coating demand.

- By Product Type, Stains & Varnishes dominated the Wood Coatings Market in 2025 owing to extensive furniture and interior wood finishing applications; Wood Preservatives significant due to rising outdoor wood protection demand.

- By Application, Furniture dominated the Wood Coatings Market; Flooring and Cabinetry & Joinery significant.

By Technology: Waterborne dominant, UV-Cured growing fastest

Waterborne wood coatings held the dominant type position in the Wood Coatings Market in 2025, reflecting the structural market transition from solvent borne to waterborne formulations that tightening VOC regulations particularly the EU's Directive and state-level regulations in the U.S. have driven progressively. Modern waterborne acrylic, polyurethane, and polyurethane-acrylic dispersion coatings have achieved performance levels in adhesion, hardness, and abrasion resistance that have narrowed the performance gap with solvent borne alternatives to the point where the majority of furniture and flooring applications previously reserved for solvent borne are now served by waterborne formulations. Waterborne coatings' additional advantages lower toxicological risk for manufacturing workers, simplified storage and transportation without flammable solvent regulations, and water cleanup sustain their market dominance regardless of the performance convergence arguments alone.

UV-Cured coatings are growing at the fastest type CAGR, driven by the furniture manufacturing industry's need for coating systems whose instantaneous UV cure enables continuous coating line production rates that thermal-cure waterborne and systems cannot match. UV-cured coatings applied to flat panels and profiled furniture components chair backs, tabletops, cabinet doors cure in fractions of a second under UV or electron beam irradiation, enabling automated finishing lines that coat, cure, and inspect furniture components at 50+ meters per minute production rates. The technology is expanding beyond traditional 2D flat panel applications into 3D object coating through the development of UV-LED systems whose wavelength flexibility enables curing of complex geometries.

By Resin Type: Polyurethane dominant, Acrylic growing fastest

Polyurethane held the dominant resin type position in the Wood Coatings Market in 2025, reflecting its superior durability, abrasion resistance, chemical protection, and long-term finish retention across furniture, flooring, cabinetry, and architectural wood applications. Polyurethane-based wood coatings are extensively utilized in both residential and commercial environments where high mechanical performance, scratch resistance, and moisture protection are critical operational requirements. The segment’s dominance is additionally supported by its compatibility with, waterborne, and high-solid coating systems that enable manufacturers to serve a broad range of industrial and decorative wood finishing applications. Polyurethane coatings remain particularly preferred for premium furniture and hardwood flooring due to their ability to provide long-lasting gloss retention and surface toughness under heavy wear conditions.

Acrylic coatings are growing at the fastest CAGR, driven by increasing global demand for low-VOC, environmentally compliant, and waterborne coating technologies. Acrylic resin systems provide excellent colour retention, UV stability, weather resistance, and low Odor characteristics, making them increasingly suitable for eco-friendly furniture coatings and interior decorative wood applications. The rapid expansion of sustainable construction materials, stricter environmental regulations, and growing consumer preference for waterborne coatings are accelerating acrylic resin adoption across both residential and industrial wood finishing markets.

By Product Type: Stains & Varnishes dominant, Wood Preservatives significant

Stains & Varnishes held the dominant product type position in the Wood Coatings Market in 2025, driven by their widespread use in furniture finishing, cabinetry, decorative interiors, flooring, and architectural wood enhancement applications. These coatings provide both aesthetic enhancement and surface protection by improving wood grain visibility, gloss appearance, scratch resistance, and moisture durability. The segment’s dominance reflects the strong demand for premium decorative wood finishes across residential, hospitality, office, and commercial infrastructure projects globally. Stains and varnishes remain essential in both industrial-scale furniture manufacturing and consumer DIY wood finishing applications where appearance quality and long-term surface protection are critical purchasing factors.

Wood Preservatives sustain significant market demand due to increasing focus on extending wood lifespan in outdoor, marine, agricultural, and structural applications exposed to moisture, insects, fungi, and environmental degradation. Preservative coatings are extensively applied in decks, fences, utility poles, outdoor furniture, and construction timber where biological and weather-related deterioration risks are high. Rising investments in outdoor infrastructure, landscaping, and weather-resistant wood protection solutions continue to support strong preservative segment growth globally.

By Application: Furniture dominant, Flooring and Cabinetry growing

Furniture held the dominant application position in the Wood Coatings Market in 2025, reflecting the furniture manufacturing industry's position as the largest single wood coating consumption segment globally. Furniture production requires coating application across multiple stages sanding sealer, stain, base coat, and topcoat creating per-piece coating material consumption that multiplied by global furniture production volumes generates aggregate wood coating demand that flooring and cabinetry markets cannot match by unit count.

Flooring represents a significant and premium application segment, where hardwood, engineered wood, and laminate flooring require coatings polyurethane and polyacrylic topcoats whose durability and abrasion resistance specifications are the most demanding of any wood coating application given residential and commercial floor traffic loads.

Wood Coatings Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

60% |

|

Europe |

Germany |

28% |

|

North America |

United States |

85% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

48% |

Asia Pacific Wood Coatings Market Insights

Asia Pacific dominated the global Wood Coatings Market with approximately 45.7% revenue share in 2025, a position driven by China's furniture manufacturing export scale, Vietnam's rapidly growing furniture sector, and the large and growing domestic furniture markets of India, Indonesia, and Southeast Asian economies. The region's wood coating market serves both export-oriented furniture manufacturing whose coating quality must meet the standards of international retail customers and domestic furniture markets whose quality expectations are rising with incomes. Chinese coating companies including Carpoly, Guangdong Huarun, and Zhanchen have established competitive domestic positions in mid-market coating categories while international brands maintain leadership in premium and UV-cure coatings for export-quality furniture.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Wood Coatings Market Insights

Europe is the fastest-growing regional Wood Coatings Market, driven by stringent environmental regulations accelerating the conversion from solvent-based to waterborne and UV-cure formulations, growing home renovation activities, and the EU's sustainable construction mandates creating demand for low-VOC and bio-based coating options. Germany leads the European wood coatings market with BASF Coatings, Brillux, and Adler Lacke sustaining domestic coating development alongside the UK's significant home improvement market and France and Scandinavia's sustainable construction coating specifications.

North America Wood Coatings Market Insights

North America's Wood Coatings Market is driven by the U.S.'s large residential renovation market where kitchen cabinet repainting, hardwood floor refinishing, and interior trim recoating create consistent professional and DIY wood coating demand and the domestic furniture manufacturing market whose production serves both the premium custom furniture segment and the assembled furniture retail category. The U.S. EPA's Architectural and Industrial Maintenance Coating regulations whose VOC content limits have progressively tightened sustain the waterborne conversion trend in the U.S. professional wood finishing market.

MEA and Latin America Wood Coatings Market Insights

The Middle East's Wood Coatings Market is growing with the Gulf states' interior design culture where premium wood finishes in luxury residential, hospitality, and retail environments create demand for high-quality furniture and architectural millwork coatings and the region's construction activity sustaining joinery and cabinetry coating demand. Latin America's market concentrates in Brazil's significant furniture manufacturing industry which produces both for domestic consumption and export to regional markets and the growing residential construction markets of Brazil, Mexico, and Colombia.

Wood Coatings Market Growth Drivers:

- Rising furniture demand and environmental regulation driving sustained wood coatings market growth globally

The Wood Coatings Market is driven by the compounding of global furniture demand growth sustained by urbanization, rising incomes in emerging markets, and the renovation culture in developed markets and the product innovation cycle that environmental regulation is driving within the coatings industry. Furniture demand growth is directly correlated with household formation, income growth, and housing activity each of which is growing across the developing world in ways that sustain wood coating demand above GDP growth rates in the markets where furniture production is concentrated. Environmental regulation creates a technology investment cycle whose innovation output bio-based resins, waterborne 2K systems, UV-waterborne hybrids sustains market growth through premium product development that maintains or improves wood coating value per liter above pure volume growth.

Wood Coatings Market Restraints:

- Raw material price volatility and waterborne performance perception creating wood coatings market challenges globally

Wood coatings manufacturers face persistent raw material price volatility where acrylic monomer, polyol, isocyanate, and titanium dioxide prices fluctuate with petrochemical feedstock costs and supply chain dynamics creating margin pressure that complicates pricing strategy in competitive coating markets where customers resist rapid price adjustments. In some industrial and professional wood finishing applications, solventborne coating performance perceptions that solventborne provides superior flow, leveling, and penetration compared to waterborne sustain demand for solventborne products in technically conservative markets despite waterborne chemistry's documented performance improvements.

Wood Coatings Market Opportunities:

- Bio-based formulations and UV-LED curing technology creating significant wood coatings market growth opportunities globally

Bio-based wood coating resins derived from plant oils, bio-based polyols, and recycled content materials represent the wood coatings market's most strategically aligned development direction for the growing market segment of environmentally committed buyers in premium furniture and building material markets. As LEED v5, BREEAM, and product-specific environmental declarations (EPDs) increasingly specify bio-based or recycled content in interior finishes, wood coating manufacturers who achieve credible bio-based content claims at competitive pricing access a premium market segment whose growth rate exceeds the broader market. UV-LED curing technology whose narrow-band UV-A emission enables curing of photo initiator systems tuned to LED wavelengths with 70% lower energy consumption and 20-year LED lamp life versus conventional UV mercury arc lamps is expanding UV-cure adoption economics into lower-volume wood finishing applications that conventional UV cure's high equipment cost and mercury lamp management deterred.

Recent Developments:

- 2026: BASF SE launched its Acronal Eco waterborne acrylic dispersion for wood coatings incorporating 35% renewable bio-based monomer content while maintaining identical film hardness, water resistance, and adhesion performance to the petroleum-based predecessor achieving ISCC PLUS sustainability certification and serving as the raw material for Sherwin-Williams, AkzoNobel, and Sherwin-Williams Industrial's bio-based wood coating product line extensions.

- 2025: AkzoNobel Industrial Coatings launched its Interpon WoodFusion UV-waterborne topcoat a dual-cure system completing initial cure through UV irradiation and final cure through ambient moisture enabling application to profiled furniture components that conventional flat-panel UV cure systems cannot process, expanding UV technology's reach into chair backs, table edges, and cabinet door profiles that represent 40% of furniture component volume by area.

- 2025: Nippon Paint Holdings expanded its wood coatings capacity in Vietnam by 60,000 metric tons the largest single capacity expansion in Southeast Asian wood coatings history targeting Vietnam's rapidly growing furniture export manufacturing sector whose coating demand is growing at 15%+ annually and whose current reliance on Chinese coating imports represents a supply chain vulnerability that Vietnamese coating manufacturing investment addresses.

Wood Coatings Market Key Players

Some of the Wood Coatings Market Companies

- Sherwin-Williams Company

- AkzoNobel NV

- BASF SE

- PPG Industries Inc.

- Nippon Paint Holdings Co. Ltd.

- Kansai Paint Co. Ltd.

- Axalta Coating Systems Ltd.

- Hempel A/S

- Jotun Group

- RPM International Inc.

- Valspar Corporation (Sherwin-Williams)

- Brillux GmbH & Co. KG

- Adler Lacke AG

- Bona AB

- Loba GmbH & Co. KG

- Carpoly Chemical Group Co. Ltd.

- Guangdong Huarun Paints Co. Ltd.

- Zhanchen Chemical Co. Ltd.

- Teknos Group

- ICA Group SpA

Wood Coatings Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.08 Billion |

| Market Size by 2035 | USD 19.65 Billion |

| CAGR | CAGR of 4.93% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Resin Type (Polyurethane, Acrylic, Nitrocellulose, Melamine Formaldehyde, Others) •By Product Type (Stains & varnishes, Shellac coating, Wood preservatives, Water repellents, Others) •By Technology (Water-borne, Solven-borne, UV-cured, Powder Coatings, Others) •By Application (Furniture, Cabinets, Flooring & Decking, Sidings, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sherwin-Williams Company, AkzoNobel NV, BASF SE, PPG Industries Inc., Nippon Paint Holdings Co. Ltd., Kansai Paint Co. Ltd., Axalta Coating Systems Ltd., Hempel A/S, Jotun Group, RPM International Inc., Valspar Corporation (Sherwin-Williams), Brillux GmbH & Co. KG, Adler Lacke AG, Bona AB, Loba GmbH & Co. KG, Carpoly Chemical Group Co. Ltd., Guangdong Huarun Paints Co. Ltd., Zhanchen Chemical Co. Ltd., Teknos Group, ICA Group SpA |

Frequently Asked Questions

Furniture dominated; Flooring and Cabinetry & Joinery are also significant growing segments.

The Wood Coatings Market was valued at USD 12.08 billion in 2025.

Asia Pacific dominated with approximately 45.7% share; Europe is the fastest growing region.

Waterborne coatings dominated; UV-Cured coatings are growing fastest.

The Wood Coatings Market is expected to grow at a CAGR of 4.93% from 2026 to 2035.

Get in Touch