Animal Disinfectant Market Report Scope & Overview:

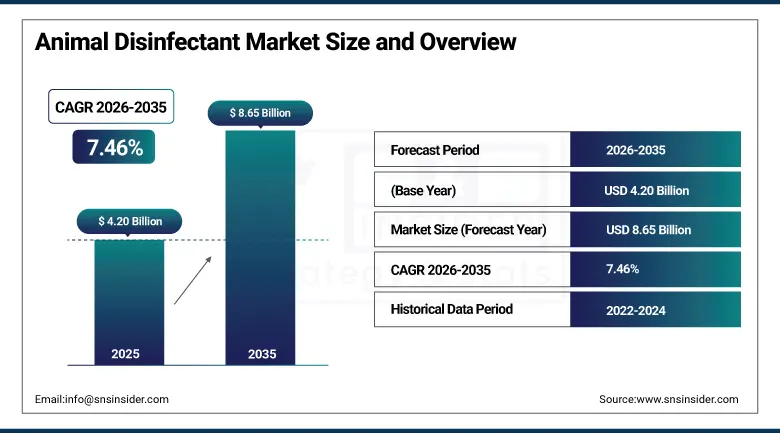

The Animal Disinfectant Market was valued at USD 4.20 Billion in 2025 and is expected to reach USD 8.65 Billion by 2035, growing at a CAGR of 7.46% from 2026 to 2035.

The global animal disinfectant market continues to demonstrate steady and sustainable growth owing to the increased frequency of infectious diseases among animals, higher intensification of livestock production worldwide, and tougher regulatory biosecurity policies mandating the use of approved disinfectant products at farms, veterinary facilities, and slaughterhouses. Animal disinfectants include diverse formulations such as iodophors, quaternary ammonium compounds, aldehydes, alcohols, peroxides, and lactic acid disinfectants used in livestock premises, dairy cattle milking facilities, poultry facilities, aquaculture systems, pig farms, and companion animal veterinary practices as a measure to reduce the microbial load and prevent its transmission.

The market is supported by the increased global frequency of pathogens of zoonotic and specific to livestock nature such as bird flu, African swine fever, foot and mouth disease, and bovine respiratory disease which trigger emergency procurement of biosecurity measures, the introduction of the EU Animal Health Law making comprehensive biosecurity management mandatory at all animal farms and slaughterhouses, and growing consumer demand for antibiotic-free and sustainable animal protein.

In April 2024, Virox Technologies launched Rescue Refill Wipe pouches containing eco-preferred disinfectant chemistries that use 90% less plastic than conventional canisters, designed to fit into existing wipe canisters for reuse in veterinary clinics and animal hospitals where large daily wipe consumption creates significant single-use plastic waste

Animal Disinfectant Market Size and Forecast

-

Market Size in 2026E: USD 4.51 Billion

-

Market Size by 2035: USD 8.65 Billion

-

CAGR: 7.46% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Animal Disinfectant Market - Request Free Sample Report

Animal Disinfectant Market Trends

-

Eco-friendly and biodegradable disinfectants are gaining popularity due to environmental regulations and sustainability goals.

-

Automated and robotic disinfection systems are being increasingly adopted in large-scale poultry and swine farms to improve biosecurity efficiency.

-

Lactic acid-based disinfectants are witnessing higher demand in dairy farming because of their residue-safe and food-safe properties.

-

Ready-to-use and concentrate formulations are simplifying disinfectant application and improving protocol compliance among livestock operators.

-

Digital biosecurity platforms integrating disinfectant tracking and compliance monitoring are emerging as value-added solutions in animal health management.

U.S. Animal Disinfectant Market Outlook

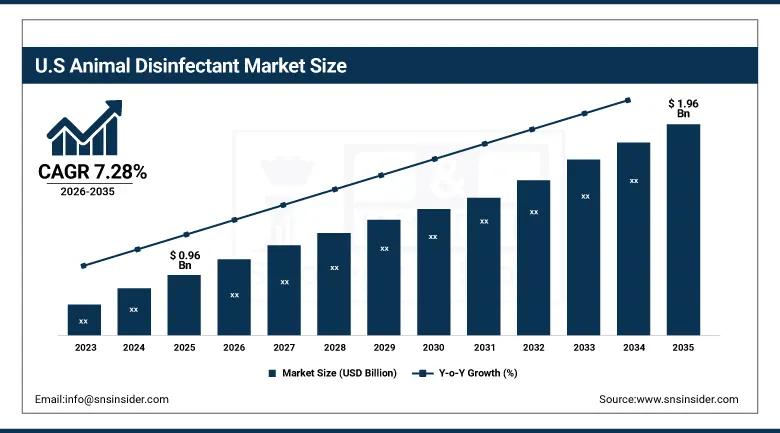

The U.S. Animal Disinfectant Market was valued at approximately USD 0.96 Billion in 2025 and is expected to reach approximately USD 1.96 Billion by 2035, growing at a CAGR of approximately 7.28%.

The United States is the largest single country market for animal disinfectants in the world, based on the vastness of American livestock production, which involves systematic biosecurity purchases by the large commercial poultry, swine, beef cattle, and dairy production facilities in the country. This results from the disease surveillance and response regulations of USDA APHIS, animal food facility sanitation inspections and enforcement policies of the FDA, and the registration and efficacy evaluation of animal facility disinfectants at the EPA to create a regulatory regime for structuring investment in disinfectants in all commercial animal production facilities.

The presence of a heavy avian influenza outbreak problem in the United States, where repeated outbreaks of high-pathogenicity avian influenza in commercial poultry lead to systematic depopulation and disinfection of facilities using vast quantities of disinfectants, drives above-normal emergency purchases.

In 2024, the World Organization for Animal Health reported avian influenza outbreaks in multiple countries affecting domestic poultry and wild birds, underscoring the strategic importance of effective disinfection protocols in commercial poultry facilities whose all-in all-out production management requires complete microbial load reduction between placement cycles to prevent pathogen carryover between successive flocks.

Animal Disinfectant Market Segment Analysis

-

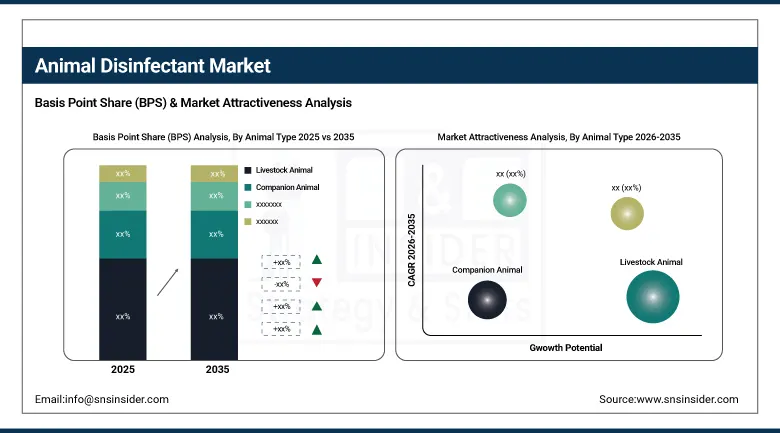

By Animal Type, the Livestock Animal segment dominated the animal disinfectant market with the largest share in 2025, while the Companion Animal segment is the fastest growing as rising pet ownership globally.

-

By Product, the Iodine-containing Disinfectant segment dominated the animal disinfectant market with approximately 22% share in 2025, while the Quaternary Ammonium Compounds segment is the fastest growing as QAC formulations' residual surface activity, low corrosivity on equipment and housing materials.

-

By Form, the Liquid segment dominated the animal disinfectant market with the largest share in 2025, while the Powder segment is the fastest growing as concentrated powder formulations' superior stability during storage.

-

By Application, the Poultry Farm segment dominated the animal disinfectant market with the largest share in 2025, while the Aquaculture segment is the fastest growing as the expanding global aquaculture industry's intensification of production density in land-based recirculating aquaculture systems.

By Animal Type, livestock dominates, companion animal grows fastest

Livestock animals were the leading category of animals in terms of market share in the animal disinfectant market during 2025. This is because the commercial concentration of spending on animal disinfectants for livestock production arises from the necessity of managing the biosecurity of the facility in any operation that involves animal husbandry due to the need for maintaining hygiene.

The segment with companion animals’ experiences rapid growth due to the remarkable rise in pet keeping around the world, especially in emerging countries and post-COVID pet adoption. This has led to the establishment of facilities like veterinary clinics and pet grooming services which require routine disinfection. Every clinic, boarding facility, and grooming saloon needs disinfectant products which contributes to above-average segment growth.

By Product, iodine-containing dominates, quaternary ammonium compounds grow fastest

Iodine disinfectants continued to lead all other animal disinfectant products with a market share of about 22% in 2025. This was owing to the very wide spectrum of pathogen control offered by iodine covering all pathogens such as bacteria, fungi, viruses including hard to kill non-enveloped varieties and mycobacteria that need to be controlled as part of the biosecurity measures for livestock operations. Iodine teat dipping products have been one of the largest applications within animal disinfectants due to the regular use of these disinfectants in dairy farming during pre- and post-milking.

Quaternary Ammonium Compounds have been the fastest growing product segments due to the residual bactericidal properties of quaternary ammonium compounds even after the treatment, lack of odor which makes these disinfectants acceptable to users in closed animal housing spaces, and compatibility with fogging/misting delivery systems used in commercial poultry and swine houses.

By Form, liquid dominates, powder grows fastest

Liquid forms continued to enjoy the top form position in the animal disinfectants market in 2025. The inherent suitability of ready-to-use and concentrated liquid forms to knapsack sprayers, pressure washers, automatic dosing machines, and footbath tank dispensing systems means that they can be applied without any further equipment and preparation for the entire process of facility disinfection in livestock and companion animals without the need for additional preparation equipment or staff.

Powder has the fastest growing form due to the excellent stability properties of concentrated powder forms which increase shelf-life under tough tropical/subtropical conditions, the reduction in weight and volume in packaging of the products which reduces logistical costs to transport them to remote areas in the livestock sector of operation, and their suitability for on-farm concentration mixing machines in commercial livestock operations in APAC and LATAM emerging markets experiencing growth in livestock industries which ensures above average demand growth.

By Application, poultry farm dominates, aquaculture grows fastest

Poultry farms maintained their dominance as the primary application category in the animal disinfectant market in 2025. The requirement for full facility disinfection at every placement interval for all-in all-out commercial broiler, breeder, and layer farms ensures that this application category sees the most predictable and voluminous disinfectant purchases in the livestock applications. In the case of a commercial broiler farm with six to eight production intervals per year, there will be six to eight full disinfection intervals each year, each utilizing hundreds of liters of concentrated disinfectant.

The aquaculture application segment is the fastest-growing as the rapid growth of the global aquaculture sector due to increased seafood consumption and reduced capacity in wild fisheries increases the need for disinfectants as biosecurity management grows within the sector.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Animal Disinfectant Market Insights

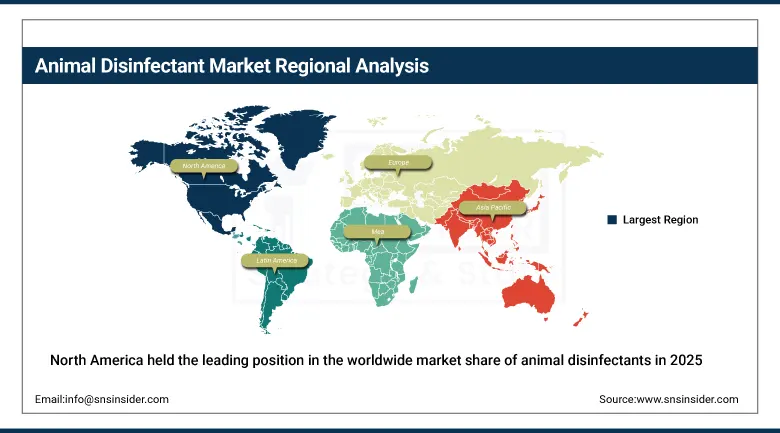

North America held the leading position in the worldwide market share of animal disinfectants in 2025 due to its exceptional commercial livestock production capacity, most advanced biosecurity regulations of any market, and home presence of companies such as Zoetis, Phibro Animal Health, and Neogen Corporation which offer the widest range of animal disinfectant products. The USA provides for approximately 87.4% of North American revenue due to its integrated production of poultry, swine, and dairy animals and biosecurity programme investment, which ensures systematic purchases of animal disinfectants.

Canada provides for approximately 12.6% of North American revenue due to its commercial poultry and swine production, Canadian Food Inspection Agency's biosecurity standards for animal health, and companion animal veterinary practices disinfections through purchases made from the growing domestic pet ownership market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Animal Disinfectant Market Insights

Europe is a compliance-oriented animal disinfectant market due to the mandatory biosecurity management requirements in all animal farms under EU Animal Health Law, the stringent approval process of disinfectants under EU Biocidal Products Regulation that leads to an organized approved products list, and the animal welfare and food safety standards of the European Food Safety Authority which form a regulatory procurement framework. The country earns about 22.3% of Europe's revenue through its commercial animal productions such as pigs, poultry, and dairies, the strict veterinary disinfectant approval standards of BVL, and the commercial operations of companies like Schülke & Mayr and Diversey whose animal facility disinfectants cater to Europe's needs.

The Netherlands, France, Denmark, and Spain are other secondary markets that generate above-average disinfectant procurements per the number of their livestock units due to intensive livestock production in enclosed animal houses. The contribution of Ecolab in Europe and veterinary disinfectant portfolio of Lanxess forms the competitive supply.

Asia Pacific Animal Disinfectant Market Insights

Asia-Pacific is the fastest growing regional market for animal disinfectants due to the extraordinary production scale of commercial poultry and swine in China, the increasing rate of modernization of the livestock industry that employs formal biosecurity programs in Asia-Pacific, and the long-lasting effect of the African swine fever epidemic on biosecurity investments in Chinese swine production. China generates around 44.8% of the Asia-Pacific revenue thanks to its extraordinary production scale, mandatory biosecurity enhancement programs, and the biosecurity investments after the ASF.

Vietnam, Indonesia, Thailand, and India are considered the most dynamic emerging markets of Asia-Pacific due to the fast-growing livestock industry, increased integration of commercial biosecurity programs by integrated poultry and swine producers, and intensification of the aquaculture industry.

MEA & Latin America Animal Disinfectant Market Insights

In the MEA region, South Africa dominates the revenue share with around 31.2%, thanks to its large-scale commercial poultry production, animal health biosecurity guidelines by the National Department of Agriculture, and growing companion animal veterinary services in urban areas. The large investments made in the region for poultry production by Saudi Arabia and UAE increase the revenue in this market. Brazil leads the Latin America market with approximately 44.2%, thanks to its large-scale commercial poultry and cattle production, animal health biosecurity compliance by MAPA, and growth in the aquaculture segment in the northern and northeastern regions.

Market Dynamics

Growth Drivers: Rising animal disease incidence creating emergency and precautionary biosecurity procurement and stringent regulatory mandates

The increasing worldwide prevalence of highly infectious diseases such as Highly Pathogenic Avian Influenza, African Swine Fever, Foot and Mouth Disease, and other animal diseases causing huge economic damages to the livestock industry has become the most commercially relevant structural growth driver for the animal disinfectant industry. Every outbreak causes emergency purchases of disinfectants on a large scale as the outbreak protocol demands complete facility disinfection, enhanced biosecurity around the perimeter, and decontamination of the transportation vehicles due to their widespread presence in large geographical locations of the affected production operations.

Strict biosecurity regulations create mandatory investment in the purchase of disinfectants, thus driving the industry growth regardless of any disease situation. Biosecurity management requirements stipulated by the EU Animal Health Law for all animal farms, biosecurity programme requirements stipulated by the USDA APHIS for commercial poultry and swine farms, and emerging biosecurity laws in Asian Pacific and Latin American livestock producing countries collectively provide obligatory compliance measures demanding usage of approved disinfectants.

Restraints: Antimicrobial resistance concerns and high regulatory approval costs

The growing community concern over the possible impact on the development of antibiotic resistance by the abuse of disinfectants and their sub-lethal exposure is bringing increasing attention towards the practice of the use of disinfectants in intensive livestock farming. The studies that link the repeated application of quaternary ammonium compounds and the emergence of bacteria that are resistant to disinfectants and can be cross-resistant to clinically relevant antibiotics have led to regulatory oversight that may limit the use of products in markets were AMR monitoring leads to restrictive policies for products.

The high cost and long approval time under the EU Biocidal Products Regulation and EPA pesticide registration requirements constitute high barriers to market entry for new disinfectants that lead to innovation inertia and the dominance of existing disinfectants. Disinfectant manufacturers that lack the means to bear the millions of euros necessary to gain approval under the BPR regime through the evaluation process are at a competitive disadvantage compared to multinational companies.

Opportunities: Sustainable formulation development and automated disinfection system integration

The creation of sustainable and environmentally friendly disinfectant formulations that meet both biosecurity efficacy needs and the environmental responsibilities aims to provide a more commercially differentiated innovation opportunity in the short term. Every organic acid, natural source, or biotechnology-based disinfectant formulation that gets approval through regulatory requirements and proves broad-spectrum efficacy offers a premium value position in the market compared to traditional chemical disinfectants with an adverse effect on the environment and aquatic life due to their persistence in the environment.

Integration of a disinfection system provides a higher value service and equipment market layer that provides additional sources of income through the provision of equipment and consumables that exceeds that provided by simply supplying the basic disinfectant products. Disinfection robots for poultry house terminal disinfection, automated foggers for biosecurity in swine facilities, and automated milking parlors disinfection equipment whose integration into disinfectant dosing creates precise application according to protocol offer equipment and consumable purchases from livestock clients in biosecurity investments.

Recent Developments:

-

2024: Phibro Animal Health expanded its animal health portfolio in 2024 with new biosecurity product formulations targeting enhanced broad-spectrum disinfection performance across swine and poultry facilities, reflecting the sustained commercial demand for effective disinfectant solutions following ongoing avian influenza and swine disease challenges globally.

-

2024: Zoetis strengthened its animal health diagnostics and biosecurity service offerings in 2024, supporting integrated disease prevention programmes that combine surveillance testing with disinfection protocol optimization for large commercial livestock producers seeking comprehensive pathogen management beyond individual product procurement.

-

2023: Virox Technologies launched Rescue Refill Wipe pouches in April 2023 containing eco-preferred disinfectant chemistries using 90% less plastic than standard canisters, designed for veterinary clinics and animal hospitals seeking to reduce single-use plastic waste while maintaining effective surface disinfection.

Animal Disinfectant Market Key Players

-

Zoetis Inc.

-

Phibro Animal Health Corporation

-

Neogen Corporation

-

Virox Technologies Inc.

-

Ecolab Inc.

-

Diversey Holdings Ltd.

-

Lanxess AG

-

Schülke & Mayr GmbH

-

Thymox Technology Inc.

-

GEA Group AG

-

Vetoquinol SA

-

Elanco Animal Health Inc.

-

Evans Vanodine International PLC

-

Solvay SA

-

Biomérieux SA

-

Virbac SA

-

Ceva Santé Animale

-

Huvepharma NV

-

M-Tech Diagnostics Ltd.

-

Kilco International Ltd.

Animal Disinfectant Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.20 Billion |

| Market Size by 2035 | USD 8.65 Billion |

| CAGR | CAGR of 7.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Animal Type (Livestock Animal, Companion Animal) • By Product (Alcohol-based Disinfectant, Aldehyde Disinfectant, Iodine-containing Disinfectant, Quaternary Ammonium Compounds, Peroxide Disinfectant, Lactic Acid Disinfectant, Other Disinfectant) • By Form (Powder, Liquid, Others) • By Application (Dairy Farming, Aquaculture, Poultry Farm, Swine, Equine, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zoetis Inc., Phibro Animal Health Corporation, Neogen Corporation, Virox Technologies Inc., Ecolab Inc., Diversey Holdings Ltd., Lanxess AG, Schülke & Mayr GmbH, Thymox Technology Inc., GEA Group AG, Vetoquinol SA, Elanco Animal Health Inc., Evans Vanodine International PLC, Solvay SA, Biomérieux SA, Virbac SA, Ceva Santé Animale, Huvepharma NV, M-Tech Diagnostics Ltd., and Kilco International Ltd. |

Frequently Asked Questions

The Animal Disinfectant Market is expected to grow at a CAGR of 7.46% from 2026 to 2035.

The Animal Disinfectant Market was valued at USD 4.20 Billion in 2025.

Rising global incidence of highly pathogenic avian influenza, African swine fever, and other devastating livestock pathogens creating emergency biosecurity procurement, combined with stringent regulatory mandates under the EU Animal Health Law, USDA APHIS biosecurity standards, and expanding national biosecurity legislation across Asia Pacific creating non-discretionary disinfectant investment.

Iodine-containing Disinfectant dominated the Animal Disinfectant Market with approximately 22% share in 2025, while Quaternary Ammonium Compounds is the fastest growing segment.

North America dominated the Animal Disinfectant Market in 2025, driven by the U.S. commercial livestock production scale and comprehensive regulatory biosecurity framework, while Asia Pacific is the fastest growing region driven by China and Southeast Asia livestock industry modernization.

Get in Touch