Anti-Biofilm Wound Dressing Market Report Scope & Overview:

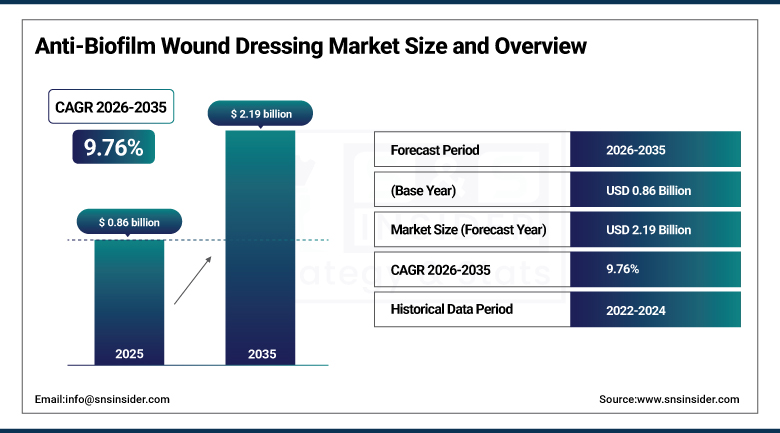

The Anti-Biofilm Wound Dressing Market was valued at USD 0.86 Billion in 2025 and is expected to reach USD 2.19 Billion by 2035, growing at a CAGR of 9.76% from 2026–2035.

The Anti-Biofilm Wound Dressing Market is expanding owing to the increasing rate of chronic wounds, including diabetic foot ulcers, pressure ulcers, and venous leg ulcers that need better solutions for infection control. Antimicrobial resistance and biofilm-related infections are contributing to the growth of the market. Growing number of aged population and diabetes cases are adding to the growth of the market. The development of technologies such as bioactive wound dressings and antimicrobial dressings and nanotechnology-based wound care technologies is contributing to the growth of the market. Rising healthcare costs and awareness about advanced wound care technologies are driving market growth.

For instance, in March 2024, the CDC reported USD 2.8 million antibiotic-resistant infections and over 35,000 deaths in the U.S., highlighting the urgent need for alternative infection-control solutions. According to the World Health Organization (WHO), diabetes affects over 830 million people globally (2024 estimate), significantly increasing the risk of chronic wound complications such as diabetic foot ulcers and delayed healing. WHO further notes that chronic wounds affect an estimated 1–2% of the global population at any given time, with prevalence rising sharply among elderly and diabetic populations.

Anti-Biofilm Wound Dressing Market Size and Forecast

-

Market Size in 2026E: USD 0.95 Billion

-

Market Size by 2035: USD 2.19 Billion

-

CAGR: 9.76% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Anti-Biofilm Wound Dressing Market - Request Free Sample Report

Anti-Biofilm Wound Dressing Market Trends

-

MRSA and multidrug-resistant organism prevalence in chronic wounds is driving specification preference for anti-biofilm dressings over conventional antimicrobial wound products.

-

Honey-based anti-biofilm dressings leveraging methylglyoxal’s biofilm disruption mechanism are gaining clinical adoption as evidence accumulates for efficacy against resistant organisms.

-

Nanoparticle-embedded wound dressings incorporating silver, zinc oxide, and copper nanoparticles are delivering enhanced biofilm penetration versus conventional ionic silver dressings.

-

Home care wound management programmes are expanding the anti-biofilm dressing distribution channel beyond institutional settings to community and patient-self-care contexts.

-

Point-of-care biofilm detection tools are enabling clinical identification of biofilm presence that optimises anti-biofilm dressing selection and treatment monitoring accuracy.

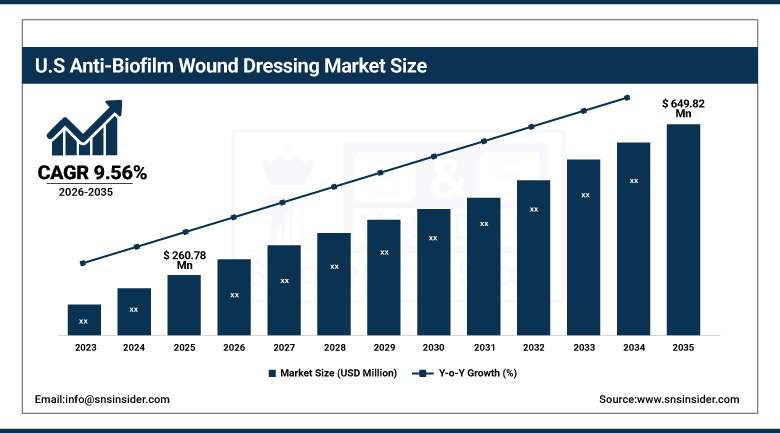

The U.S. Anti-Biofilm Wound Dressing Market Outlook

The U.S. Anti-Biofilm Wound Dressing Market was valued at USD 260.78 million in 2025 and is expected to reach USD 649.82 million by 2035, growing at a CAGR of 9.56% from 2026-2035.

The United States leads North American revenues through its advanced wound care infrastructure, strong CMS and Medicare reimbursement frameworks for advanced wound dressings in hospital outpatient and home health settings, and the world’s largest diabetic wound population whose 37 million diabetes patients create the highest national chronic wound burden. Convatec, Smith & Nephew, and 3M (Solventum)’s AQUACEL Ag and Tegaderm antimicrobial silver dressings sustain U.S. market leadership through established clinical evidence, formulary positioning, and established clinical education programmes.

In February 2025, U.S. healthcare spending reached USD 4.8 trillion, with rising investment in advanced wound care and home health supporting anti-biofilm dressing market growth. Furthermore, about 17% of the U.S. population is aged 65 or older, contributing to a higher prevalence of chronic conditions and prolonged wound recovery times. These factors collectively drive strong demand for anti-biofilm wound dressings across healthcare settings.

Anti-Biofilm Wound Dressing Market Segment Analysis

-

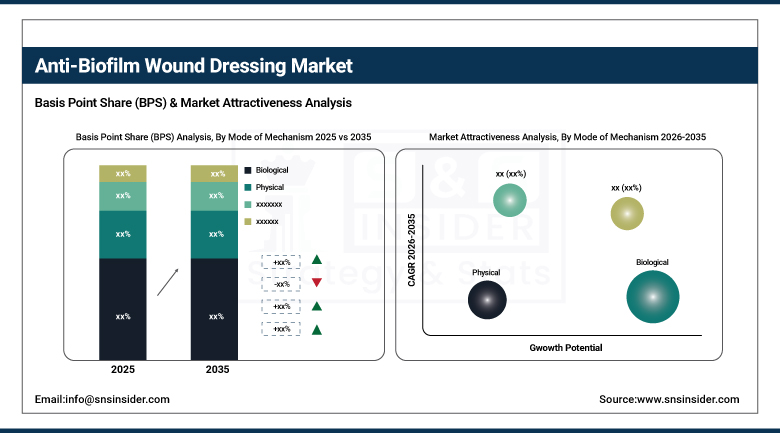

By Mode of Mechanism, Biological segment dominated the Anti-Biofilm Wound Dressing Market in 2025 with 46.8% share; Chemical segment is the fastest growing segment.

-

By Wound Type, Chronic Wounds segment dominated the market in 2025 with 58.2% share; Acute Wounds segment is the fastest growing segment.

-

By End-user, Hospitals segment dominated the market in 2025 with 49.5% share; Home Healthcare segment is the fastest growing segment.

By Mode of Mechanism, biological segment dominates the anti-biofilm wound dressing market, while chemical segment is the fastest-growing segment

The biological segment dominated the Anti-Biofilm Wound Dressing Market because of its robust potential to facilitate natural healing mechanisms and at the same time prevent the emergence of microbial resistance. This type of dressing is made from biological materials that accelerate the growth of tissues, eliminate any infection, and contribute to efficient wound recovery. The increase in chronic wounds and the increasing preference for high-tech wound treatment solutions in the clinical setting also boost its popularity. Compatibility with human biology makes this product popular in the market.

The chemical segment is the fastest-growing owing to the rise in demand for fast-acting and efficient anti-bacterial products for the elimination of biofilms. This kind of dressings includes antibacterial and anti-septic substances that work on disrupting the bacterial colonies and reducing the severity of the infection. Increasing cases of antibiotic-resistant infections and complicated wounds are propelling the demand for this kind of dressings.

By Wound Type, chronic wounds dominate the anti-biofilm wound dressing market, while acute wounds is the fastest-growing segment

Chronic wounds dominated the Anti-Biofilm Wound Dressing Market owing to their slow healing process and high vulnerability to infection and biofilm formation. Conditions like diabetic foot ulcers, pressure ulcers, and venous leg ulcers need continuous advanced wound care. Increased occurrences of diseases like diabetes, obesity, and growing elderly populations are other factors that have driven the demand for anti-biofilm wound dressings. Chronic wounds are currently the most dominant segment in the global market for these dressings.

Acute wounds are the fastest-growing segment owing to an increased number of injuries, surgery procedures, and emergencies across the globe. The demand for anti-biofilm dressing is rising due to the growing use of advanced wound care products in post-surgery operations and emergencies. Anti-biofilm dressings aid in avoiding infections, decreasing risks of complications, and accelerating the healing process.

By End-user, hospitals dominate the anti-biofilm wound dressing market, while home healthcare is the fastest-growing segment

Hospitals dominated the Anti-Biofilm Wound Dressing Market due to having a highly developed health care infrastructure, high patient traffic, and presence of skilled health professionals. They handle large numbers of patients with chronic and acute wounds that require specialized management. The adoption of such devices is supported by the presence of advanced wound care technologies and clinical protocols. The dominance of hospitals in the wound care space is expected to persist due to their capability in handling difficult cases.

Home healthcare is the fastest-growing segment owing to the increasing need for convenient and cost-effective management of complicated wounds. The growth drivers include an increased number of aging individuals and chronic diseases, which contribute to wound formation. Individuals have a preference for being treated from the comfort of their homes as it enables them to save time, cost, and travel expenses. Innovation and developments in portable wound care technologies are anticipated to boost the growth of this segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

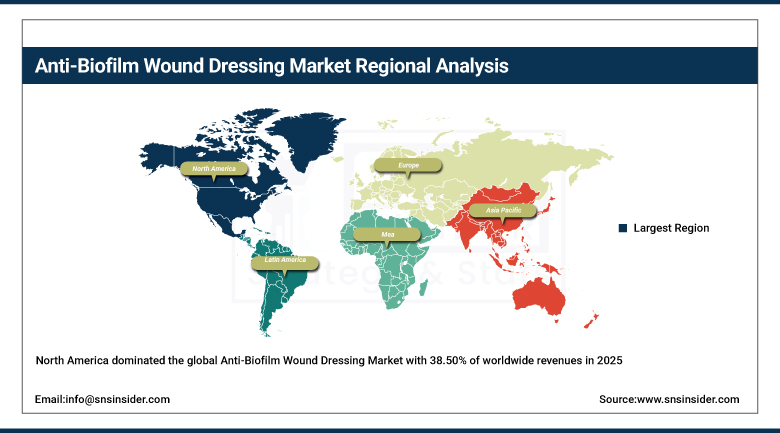

North America Anti-Biofilm Wound Dressing Market Insights

North America dominated the global Anti-Biofilm Wound Dressing Market with 38.50% of worldwide revenues in 2025, driven by its advanced wound care infrastructure, strong CMS Medicare and Medicaid reimbursement for advanced wound dressings, and the world’s highest healthcare expenditure creating procurement access for premium wound care products. The United States accounts for approximately 82.5% of North American revenues through Convatec, Smith & Nephew, and 3M Solventum’s AQUACEL, ALLEVYN, and Tegaderm antimicrobial wound dressing market leadership.

As per reports of CDC in the U.S., there are 38 million people who are diabetic in the United States. These people constitute about 11% of the total population, thereby making them more prone to infections due to chronic wounds and delay in their healing process. Additionally, each year there are around 6.5 million chronic wound cases in the United States.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Anti-Biofilm Wound Dressing Market Insights

Europe is a technically sophisticated anti-biofilm wound dressing market where universal healthcare system procurement, advanced wound care clinical guidelines, and the commercial presence of Mölnlycke Health Care, Urgo Medical, and Convatec’s European operations sustain consistent demand. Germany accounts for approximately 24.6% of European revenues through its large hospital and outpatient wound care infrastructure, the comprehensive wound management coverage within statutory health insurance, and the German Wound Healing Society’s evidence-based guideline development that progressively formalises anti-biofilm dressing standard of care.

According to Eurostat, around 21% of the European Union population is aged 65 or older, significantly increasing the prevalence of chronic wounds and age-related complications that require advanced care and prolonged treatment. Diabetes affects over 61 million adults in Europe, according to the International Diabetes Federation, further contributing to a high-risk patient pool for chronic wound development.

Additionally, hospital-acquired pressure ulcers impact up to 10–20% of hospitalized elderly patients in some European healthcare systems, highlighting the clinical burden and reinforcing the need for effective anti-biofilm wound care solutions to prevent infections and improve healing outcomes.

Asia Pacific Anti-Biofilm Wound Dressing Market Insights

Asia Pacific is the fastest-growing regional Anti-Biofilm Wound Dressing Market with a CAGR of approximately 10.33%, driven by the world’s largest and fastest-growing diabetic population, rising surgical volume in expanding hospital infrastructure, and increasing awareness of advanced wound care solutions among healthcare providers. China accounts for approximately 38.5% of Asia Pacific revenues through its growing wound care market’s progressive adoption of advanced dressings above traditional gauze-based wound management, the expanding hospital-acquired infection prevention investment, and the domestic diabetic population’s world-leading scale creating the largest chronic wound burden globally.

According to the International Diabetes Federation (IDF), Asia accounts for over 50% of global diabetes cases, making it the largest contributor to diabetes-related complications such as diabetic foot ulcers and other chronic wounds.

China alone has over 140 million people living with diabetes, one of the highest national burdens globally, significantly increasing demand for advanced wound care solutions. Similarly, India has more than 77 million diabetes patients, further contributing to the rising incidence of chronic wounds and infections.

These factors collectively drive strong demand for anti-biofilm wound dressings across the Asia Pacific region due to the growing patient pool and associated wound management needs.

MEA & Latin America Anti-Biofilm Wound Dressing Market Insights

The UAE leads MEA revenues at approximately 22.8% through its world-class hospital infrastructure’s adoption of premium wound care products, the large diabetic patient population among its Gulf Cooperation Council neighbours creating regional wound care demand, and Vision 2030 healthcare quality investment creating procurement capacity for advanced wound management solutions. Saudi Arabia’s large diabetic population and expanding hospital infrastructure create growing anti-biofilm dressing market development.

Brazil leads Latin American revenues at approximately 43.8% through its large diabetic and obese population creating the region’s highest chronic wound burden, the SUS public health system’s progressive adoption of advanced wound care in complex wound management protocols, and the growing private health sector’s wound care specialty clinic network. Mexico and Colombia are growing secondary markets whose expanding hospital infrastructure and increasing chronic disease burden create developing anti-biofilm dressing procurement.

Market Dynamics

Growth Drivers: Escalating antibiotic resistance is making biofilm-infected wounds harder to treat, increasing demand for advanced wound dressings.

The anti-biofilm wound dressing market’s growth is structurally driven by the intersection of two independently compounding health crises: the antibiotic resistance crisis whose WHO-designated critical priority pathogens including MRSA and Pseudomonas aeruginosa are progressively rendering systemic antibiotic therapy ineffective in biofilm-infected wounds, and the chronic disease pandemic whose global diabetes prevalence of 537 million adults creating diabetic foot ulcer risk and the obesity epidemic creating pressure injury susceptibility collectively sustain the world’s growing chronic wound patient population. Each percentage point increase in global diabetes prevalence creates proportional growth in the diabetic foot ulcer incidence pool that generates anti-biofilm wound dressing demand, creating a non-discretionary market growth driver whose clinical urgency and healthcare system treatment obligation creates procurement independent of economic cycle variability.

Restraints: High product cost relative to conventional wound dressings and reimbursement complexity limiting adoption in cost-constrained healthcare systems

Anti-biofilm wound dressings’ premium pricing relative to conventional antimicrobial or non-antimicrobial wound care alternatives, where per-dressing costs of USD 8 to USD 35 for advanced anti-biofilm products compare unfavourably with USD 0.50 to USD 3 for standard gauze or simple foam dressings, creates formulary adoption barriers in cost-constrained healthcare systems whose procurement decisions require health economic evidence demonstrating wound healing acceleration or complication reduction that offsets the higher per-dressing cost.

Reimbursement pathway complexity for novel anti-biofilm dressings in national healthcare systems whose product coverage determination processes require country-specific health technology assessment submissions creates market access delays and regulatory investment that smaller innovative anti-biofilm product manufacturers cannot efficiently fund.

Opportunities: Rising chronic wounds and innovations like Manuka honey and bacteriophage dressings are driving strong market expansion.

Medical-grade Manuka honey’s methylglyoxal-mediated biofilm disruption mechanism whose physical sugar osmolality, acidic pH, and hydrogen peroxide generation collectively address multiple biofilm vulnerability points without the resistance development risk associated with conventional chemical antimicrobials creates growing commercial opportunity for honey-based anti-biofilm dressing products. Each new randomised controlled trial demonstrating superior biofilm-infected wound healing outcomes from Manuka honey dressings versus silver or iodine alternatives creates prescriber conversion events that expand the addressable market for honey-based products.

Emerging market diabetic wound care infrastructure investment, where India, China, and Southeast Asian markets are progressively establishing wound care speciality clinics and home care programmes, creates distribution expansion opportunities for anti-biofilm dressing manufacturers whose market penetration in these high-chronic-wound-burden territories remains substantially below their developed market penetration levels.

Recent Developments:

-

2024: Coloplast initiated a clinical trial for Biatain Silicone Ag Xtra in Canada targeting MRSA-colonised burn wound biofilm management, evaluating multimodal anti-biofilm efficacy combining silver ion release with superabsorbent silicone foam in the demanding burn wound environment.

-

2024: Mölnlycke Health Care expanded its Mepilex Border Ag antimicrobial wound dressing portfolio with extended sizes and configurations for surgical site infection prevention, providing anti-biofilm silver-containing wound closure capability across a broader range of surgical incision dimensions and anatomical locations.

-

2024: Aroa Biosurgery expanded distribution of its Endoform anti-biofilm extracellular matrix dressing through its WOW Nurses programme partnership with HCAH in India, providing community wound care nurse training and clinical support infrastructure for complex wound management in home and subacute care settings.

Anti-Biofilm Wound Dressing Market Key Players are:

-

Smith & Nephew plc

-

Mölnlycke Health Care AB

-

ConvaTec Group PLC

-

3M Health Care

-

Coloplast A/S

-

Lohmann & Rauscher GmbH & Co. KG

-

Braun Melsungen AG

-

Medline Industries LP

-

Urgo Medical

-

Next Science Limited

-

Imbed Biosciences Inc.

-

Medtronic plc

-

Integra LifeSciences Holdings Corporation

-

Hartmann Group

-

Argentum Medical

-

KCI (Acelity)

-

DermaRite Industries

-

Genadyne Biotechnologies

-

Kerecis

-

Covalon Technologies

Anti-Biofilm Wound Dressing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.86 Billion |

| Market Size by 2035 | USD 2.19 Billion |

| CAGR | CAGR of 9.76% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Mode of Mechanism (Physical, Chemical, Biological) • By Wound Type (Chronic Wounds, Acute Wounds) • By End-user (Hospitals, Specialty Clinics, Home Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Smith & Nephew plc, Mölnlycke Health Care AB, ConvaTec Group PLC, 3M Health Care, Coloplast A/S, Lohmann & Rauscher GmbH & Co. KG, B. Braun Melsungen AG, Medline Industries, LP, Urgo Medical, Next Science Limited, Imbed Biosciences Inc., Medtronic plc, Integra LifeSciences Holdings Corporation, Hartmann Group, Argentum Medical, KCI (Acelity), DermaRite Industries, Genadyne Biotechnologies, Kerecis, Covalon Technologies. |

Frequently Asked Questions

The Anti-Biofilm Wound Dressing Market is expected to grow at a CAGR of 9.76% from 2026 to 2035.

Escalating antibiotic resistance, rising chronic wounds, surgical infection prevention investment, and biofilm awareness are driving strong anti-biofilm wound dressing demand.

The Chronic Wounds segment dominated the Anti-Biofilm Wound Dressing Market with the largest share in 2025.

North America dominated the Anti-Biofilm Wound Dressing Market with 38.50% of global revenues in 2025.

Get in Touch