Transplant Diagnostics Market Report Scope & Overview:

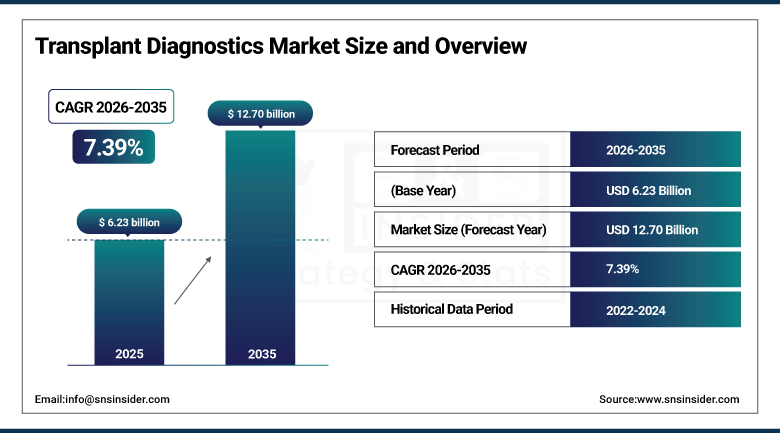

The Transplant Diagnostics Market was estimated at USD 6.23 billion in 2025 and is expected to reach USD 12.70 billion by 2035 and grow at a CAGR of 7.39% over the forecast period of 2026-2035.

Reasons for Growth of Global Transplant Diagnostics Market include rising organ transplant operations, increased incidence of chronic diseases, and increasing demand for early detection of rejection. Technological advancements in molecular diagnostics, HLA typing, and non-invasive monitoring techniques have been enhancing the success rate of transplantation procedures. Growing healthcare infrastructure and awareness about organ donation are additional driving factors of market expansion across the world.

The International Society for Heart and Lung Transplantation's registry documents that global heart and lung transplant volumes have grown 15% over the past five years driven by improved mechanical circulatory support enabling more bridging of patients to transplant and expanded donor utilization criteria.

Market Size and Forecast

-

Market Size in 2025: USD 6.23 Billion

-

Market Size by 2035: USD 12.70 Billion

-

CAGR: 7.39% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Transplant Diagnostics Market - Request Free Sample Report

Transplant Diagnostics Market Trends

-

Next-generation sequencing HLA typing providing single nucleotide resolution genetic characterization of HLA alleles that traditional sequence-specific oligonucleotide methods miss is replacing low-resolution HLA typing in programs whose improved matching accuracy is documented to improve graft outcomes.

-

Donor-derived cell-free DNA monitoring where circulating fragments of donor DNA in the recipient's blood are quantified as a rejection biomarker that rises before conventional creatinine elevation in kidney rejection is creating a new post-transplant monitoring assay category whose liquid biopsy approach avoids the invasive tissue biopsy that traditional rejection confirmation requires.

-

AI-powered compatibility prediction where machine learning models trained on millions of donor-recipient HLA pairs and outcomes predict rejection risk more accurately than traditional algorithm-based matching is enabling virtual crossmatch predictions that reduce the time-to-transplant for urgent recipients.

-

Multiplexed flow cytometry crossmatch assays providing simultaneous T-cell and B-cell crossmatch results alongside donor-specific antibody specificity identification in a single workflow are reducing pre-transplant evaluation turnaround time whose urgency for deceased donor transplants creates pressure for faster diagnostic results.

-

Luminex solid-phase antibody testing evolution toward next-generation platforms with improved resolution and quantification accuracy is sustaining reagent procurement growth above transplant volume growth.

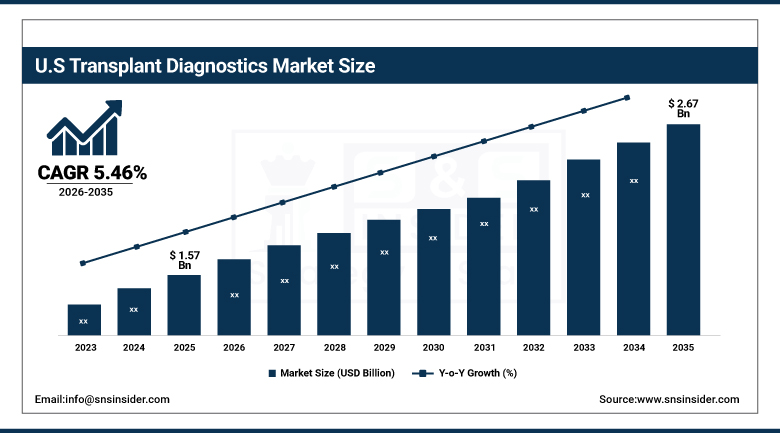

U.S. Transplant Diagnostics Market was valued at USD 1.57 billion in 2025 and is expected to reach USD 2.67 billion by 2035, growing at a CAGR of 5.46%.

Factors Driving the Expansion of U.S. Transplant Diagnostics Market include increasing organ transplant procedures, growing incidence of kidney and liver diseases, and high adoption rate of molecular diagnostics technologies. Precision medicine and early rejection monitoring are some other important factors contributing towards demand generation within the country.

The Organ Procurement and Transplantation Network's annual data documents that U.S. organ transplant volumes grew 6% in the most recently reported year with deceased donor kidneys, livers, and hearts each achieving record procurement volumes through expanded utilization criteria including normalized donation after circulatory death protocols.

Transplant Diagnostics Market Segment Analysis

-

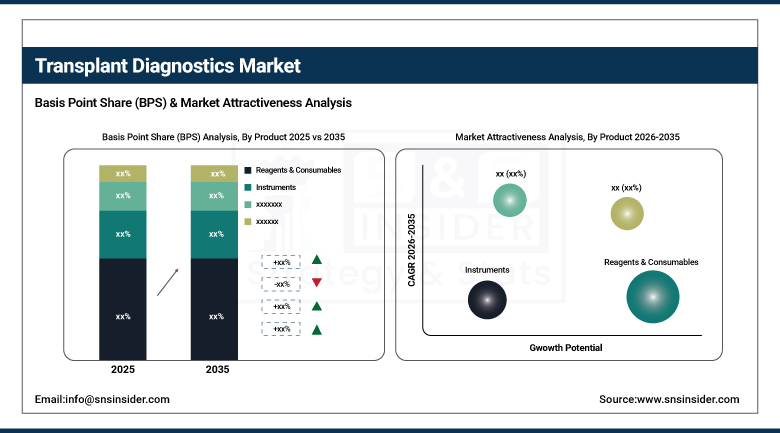

By Product, Reagents & Consumables dominated with the largest share in 2025; Software & Services growing at fastest CAGR.

-

By Technique, Molecular Assay dominated the Transplant Diagnostics Market; Non-Molecular growing in developing market programs.

-

By Transplant Type, Solid Organ Transplant (Kidney largest) dominated; Stem Cell/Bone Marrow significant and growing.

By Product: Reagents & Consumables dominant, Software growing fastest

Reagents and Consumables held the dominant product position in the Transplant Diagnostics Market in 2025, reflecting the recurring procurement model that diagnostic assay kits, HLA typing reagents, solid-phase bead arrays for antibody testing, and dd-cfDNA assay consumables create where each transplant recipient generates ongoing post-transplant monitoring reagent consumption that extends the commercial relationship between diagnostic manufacturer and transplant program for years beyond the initial transplant event. Luminex's SAB (Single Antigen Bead) kits the gold standard for donor-specific antibody identification globally sustain high reagent consumption at every transplant program that performs antibody monitoring, creating recurring revenue whose predictability sustains manufacturer investment in assay innovation. Software and Services are growing at the fastest CAGR, driven by AI-powered compatibility prediction platforms, dd-cfDNA interpretation algorithms, and HLA database subscription services whose software value proposition increases with each improvement in predictive algorithm accuracy.

By Transplant Type: Kidney transplant largest, all types growing

Solid Organ Transplantation held the dominant transplant type position, with kidney transplantation as the largest individual procedure category reflecting kidney's position as the world's most commonly transplanted solid organ, with over 90,000 kidney transplants annually, and the most developed diagnostic infrastructure for pre- and post-transplant kidney monitoring. Liver, heart, and lung transplantation each sustain significant and growing diagnostic market shares as diagnostic sophistication in each transplant type increases toward the comprehensive HLA typing, crossmatch testing, and monitoring protocols that kidney transplantation has established as the clinical standard. Stem Cell and Bone Marrow Transplantation creates distinct diagnostic requirements high-resolution HLA typing for donor-recipient matching across the full HLA locus set, chimerism monitoring to assess engraftment success, and graft-versus-host disease prediction algorithms that sustain a specialized diagnostic sub-market growing alongside the expanding indications for allogeneic stem cell transplantation.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

China |

38% |

|

Middle East & Africa |

Israel |

42% |

|

Latin America |

Brazil |

52% |

North America Transplant Diagnostics Market Insights

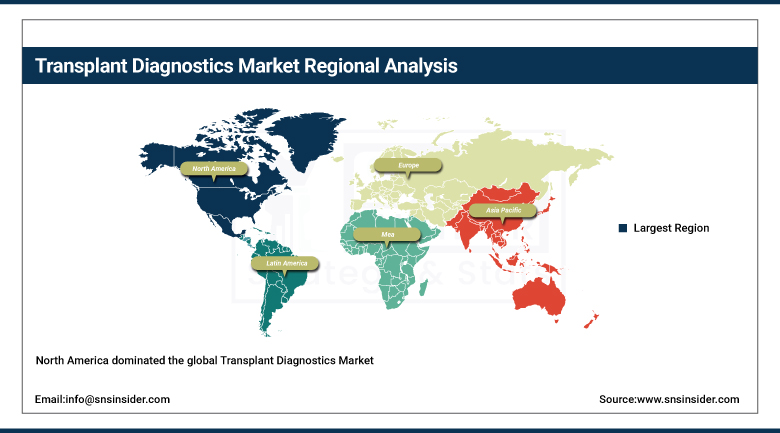

North America dominated the global Transplant Diagnostics Market, led by the United States' comprehensive transplant infrastructure, the world's most sophisticated commercial transplant diagnostic laboratory ecosystem, and the progressive CMS reimbursement expansion for novel transplant monitoring assays including dd-cfDNA. The U.S. transplant diagnostic market's commercial sophistication reflects the deep clinical engagement between diagnostic manufacturers and transplant programs where CareDx, Thermo Fisher Scientific's transplant division, and Immucor support clinical data generation programs alongside commercial product development creating the evidence base that sustains clinical adoption and regulatory reimbursement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Transplant Diagnostics Market Insights

Europe's Transplant Diagnostics Market is growing with the EU's comprehensive deceased donor transplant infrastructure whose Eurotrans plant (serving 8 European countries) and UK Transplant coordination programs sustain high-volume transplant activities requiring systematic diagnostic support and the region's adoption of NGS HLA typing across major transplant centers. Germany, France, UK, and the Netherlands lead European transplant volumes and diagnostic sophistication, with European manufacturers Hannover-based DKMS Life Science Lab and Munich's Helmholtz Zentrum München sustaining local HLA typing research alongside commercial diagnostic laboratories.

Asia Pacific Transplant Diagnostics Market Insights

Asia Pacific is the fastest-growing regional Transplant Diagnostics Market, driven by China's rapidly expanding organ transplant program which performed over 22,000 transplants in the most recently reported year and is growing volume as transplant infrastructure investment expands beyond major coastal medical centers India's growing transplant program, and Japan and South Korea's sophisticated academic transplant centers that adopt advanced diagnostic approaches rapidly. China's transplant diagnostic market is served by domestic manufacturers including Lifotronic Technology and BioMedica alongside international brands, with government investment in transplant infrastructure sustaining diagnostic procurement growth.

MEA and Latin America Transplant Diagnostics Market Insights

Israel's transplant diagnostics market is commercially active relative to its size with Hadassah Medical Center and Sheba Medical Center running sophisticated transplant programs that adopt novel diagnostic approaches including dd-cfDNA monitoring ahead of regional peers. Latin America's market concentrates in Brazil where the Brazilian organ transplant system performs the highest transplant volumes in Latin America and Argentina, whose transplant infrastructure represents Latin America's most advanced diagnostic adoption environment.

Transplant Diagnostics Market Growth Drivers:

-

Rising organ transplant volumes and dd-cfDNA monitoring adoption driving sustained transplant diagnostics market growth globally

The Transplant Diagnostics Market is growing steadily because of growing rates of organ transplantations across the world and increased use of donor derived cell free DNA (dd-cfDNA) test systems. Increasing use of highly sophisticated molecular diagnostic tests in the identification of organ rejection, better organ compatibility testing and improved clinical outcomes among others will drive the growth of the market. The incidence of chronic diseases such as kidney disease, liver disease, heart disease, and lung disease among other diseases that require organ transplantation is also on the rise.

Transplant Diagnostics Market Restraints:

-

Organ shortage constraints and high diagnostic costs creating transplant diagnostics market challenges globally

The transplant diagnostics market's growth is ultimately constrained by organ availability where the global shortage of deceased donor organs limits transplant volumes below the demand that the waitlisted patient population represents. Approximately 100,000 patients are on the U.S. transplant waitlist at any given time, with over 6,000 dying annually while waiting for organs creating a transplant volume ceiling that diagnostic market growth must work within. The high cost of comprehensive pre-transplant evaluation where full HLA typing, crossmatch testing, and antibody characterization adds USD 2,000-5,000 to the pre-transplant evaluation cost creates coverage discussion at programs whose reimbursement environments are constrained.

Transplant Diagnostics Market Opportunities:

-

NGS HLA typing adoption and liquid biopsy rejection monitoring creating transformative transplant diagnostics market growth globally

NGS-based HLA typing's progressive replacement of conventional sequence-specific oligonucleotide and sequence-specific primer methods represents the transplant diagnostics market's most clinically impactful technology transition where single nucleotide resolution HLA allele identification improves matching accuracy in ways whose graft survival improvement has been documented in large registry analyses. As NGS HLA typing costs decline through automation and reagent commoditization, adoption will expand from the leading academic centers where it is already standard toward community transplant programs whose testing budgets have historically constrained adoption to conventional lower-resolution methods. Liquid biopsy transplant monitoring expansion from kidney surveillance toward heart, lung, and liver transplant monitoring creates new reimbursable test categories whose introduction compounds the per-patient monitoring revenue that sustains transplant diagnostic market growth above transplant volume growth.

Recent Developments:

-

2026: CareDx launched AlloSeq cfDNA 2.0 an expanded donor-derived cell-free DNA monitoring panel simultaneously quantifying dd-cfDNA fraction, HLA antibody status, and viral infection markers (BK virus, CMV, EBV) from a single blood draw providing comprehensive post-transplant health status assessment in a single sample collection event that reduces patient phlebotomy burden while expanding clinical information available to transplant physicians managing the complex post-transplant patient whose immunosuppression creates vulnerability to both rejection and opportunistic infection simultaneously.

-

2025: Thermo Fisher Scientific launched the VeriFlex HLA Typing System a fully automated NGS HLA typing platform completing 96-sample HLA typing in 18 hours with single nucleotide resolution across HLA-A, B, C, DRB1, DQB1, and DPB1 loci reducing the labor input for high-resolution HLA typing by 65% versus manual NGS library preparation protocols and enabling community hospital transplant laboratories to perform in-house high-resolution typing that previously required sending samples to specialized commercial reference laboratories.

Transplant Diagnostics Market Key Players

-

CareDx Inc.

-

Thermo Fisher Scientific Inc. (One Lambda)

-

Bio-Rad Laboratories Inc.

-

Immucor Inc. (Werfen)

-

Luminex Corporation (DiaSorin)

-

Bio-Techne Corporation

-

F. Hoffmann-La Roche AG

-

Abbott Laboratories

-

Illumina Inc.

-

Pacific Biosciences (PacBio)

-

GenDx BV

-

Inno-Train Diagnostik GmbH

-

Grifols SA

-

Transmedics Group Inc.

-

Beckman Coulter Life Sciences

-

QIAGEN NV

-

Miltenyi Biotec GmbH

-

Hemacare Corporation

-

Hologic Inc.

-

Agena Bioscience Inc.

Transplant Diagnostics Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.23 Billion |

| Market Size by 2035 | USD 12.70 Billion |

| CAGR | CAGR of 7.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Reagents & Consumables, Instruments, Software & Services) • By Technique (Molecular Assay, Non-Molecular Assay) • By Transplant Type (Solid Organ Transplant [Kidney, Liver, Heart, Lung], Stem Cell/Bone Marrow Transplant) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CareDx Inc., Thermo Fisher Scientific Inc., Bio-Rad Laboratories Inc., Immucor Inc., Luminex Corporation, Bio-Techne Corporation, F. Hoffmann-La Roche AG, Abbott Laboratories, Illumina Inc., Pacific Biosciences (PacBio), GenDx BV, Inno-Train Diagnostik GmbH, Grifols SA, Transmedics Group Inc., Beckman Coulter Life Sciences, QIAGEN NV, Miltenyi Biotec GmbH, Hemacare Corporation, Hologic Inc., Agena Bioscience Inc. |

Frequently Asked Questions

The Transplant Diagnostics Market was valued at USD 6.23 billion in 2025.

North America dominated; Asia Pacific is the fastest growing regional market.

Molecular Assay dominated; Non-Molecular growing in developing market transplant programs.

Reagents & Consumables dominated; Software & Services growing at the fastest CAGR.

The Transplant Diagnostics Market is expected to grow at a CAGR of 7.39% from 2026 to 2035.

Get in Touch