Veterinary Parasiticides Market Report Scope & Overview:

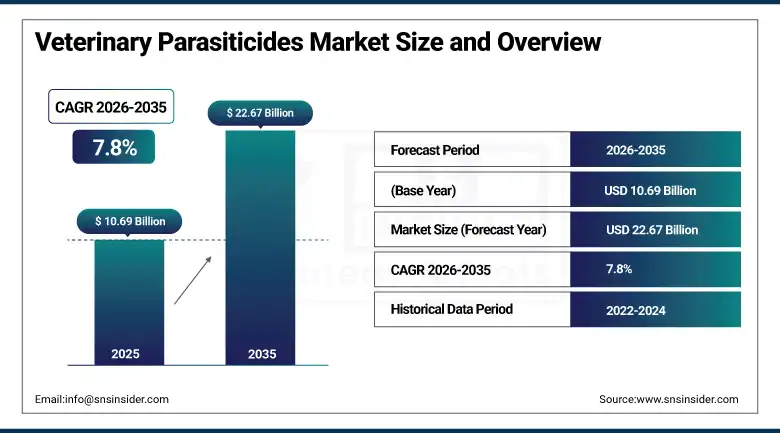

The Veterinary Parasiticides Market size was USD 10.69 Billion in 2025 and is expected to reach USD 22.67 Billion by 2035, growing at a CAGR of 7.8% from 2026–2035.

Veterinary parasiticides provide companion animals and livestock protection from ticks, fleas, worms, and other types of parasites. Market dynamics cover the frequency of diseases among both companion animal and livestock populations around the world. It also evaluates the prescribing behavior regarding anthelmintics, ectoparasiticides, and endectocides. Both production and consumption statistics can be used to measure demand dynamics. Information on healthcare expenditures covers the share contributed by governments, health insurance organizations, and pet owners. Long-acting formulations and combination treatments become increasingly common. Regulatory approval trends also influence the speed at which new products enter the market. There is a growing number of cases involving zoonotic diseases. Therefore, there is an increasing need for better protective measures among pet owners and livestock producers.

In October 2024, the FDA approved Elanco’s Credelio Quattro. It is a monthly chewable tablet for dogs eight weeks and older. The drug treats fleas, ticks, roundworms, hookworms, tapeworms, and heartworms in a single dose. Elanco plans to launch the product in early 2025. This kind of all-in-one chewable reflects a clear industry shift. Pet owners want fewer pills and broader parasite coverage from a single, convenient treatment.

Market Size and Forecast

-

Market Size in 2026E: USD 11.53 Billion

-

Market Size by 2035: USD 22.67 Billion

-

CAGR: 7.8% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Veterinary Parasiticides Market - Request Free Sample Report

Veterinary Parasiticides Market Trends

-

Long-acting chewable tablets like NexGard and Bravecto are replacing older monthly topical treatments fast.

-

Combination therapies covering multiple parasite types in one dose are gaining strong pet owner preference.

-

Rising pet humanization is pushing owners to spend more on premium parasite prevention products.

-

Antiparasitic drug resistance is forcing companies to develop new active ingredients and combination formulas.

-

E-commerce platforms are becoming a bigger sales channel for over-the-counter parasiticide products.

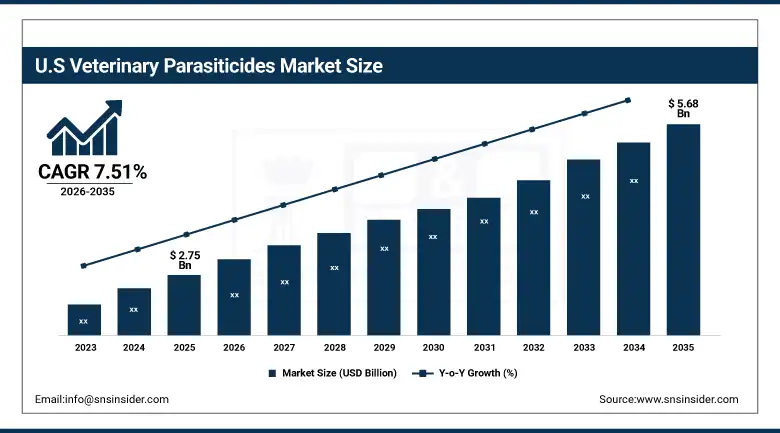

The U.S. Veterinary Parasiticides Market Outlook

The U.S. Veterinary Parasiticides Market was valued at approximately USD 2.75 Billion in 2025. It is expected to reach approximately USD 5.68 Billion by 2035. The market is growing at a CAGR of approximately 7.51%.

Pet owners in America reportedly spend about USD 151 billion on their pets per year. Pets are becoming family members in America at an increasing pace. Humanization trends continue to push pet health care products sales, which includes parasiticides, among others. Such companies as Freshpet have established themselves as multi-billion dollar corporations due to the same trend. The presence of sound veterinary care systems and accessible clinics adds to this equation. Increasing disposable income and increasing pet ownership also ensure further growth.

In November 2024, Merck Animal Health received European approval for BRAVECTO TriUNO. It is a single chewable tablet for dogs that treats both internal and external parasites. The drug covers fleas, ticks, gastrointestinal worms, and heartworm prevention together. This kind of broad-spectrum, single-dose product is becoming the new industry standard. It simplifies treatment for pet owners while improving compliance and reducing missed doses.

Veterinary Parasiticides Market Segment Analysis

-

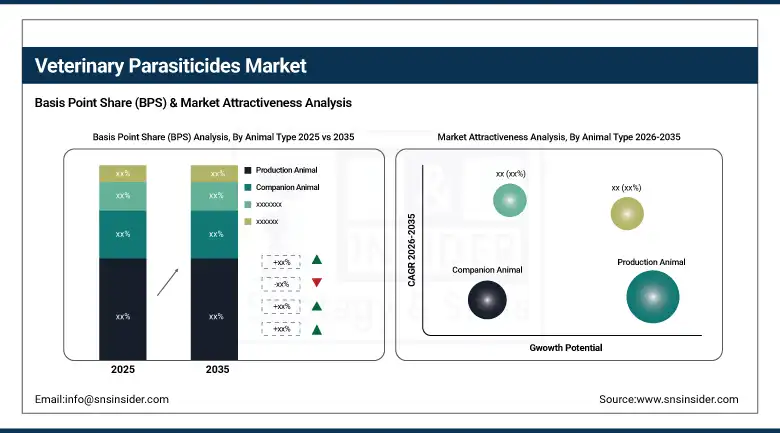

By Animal Type, production animal segment dominated the veterinary parasiticides market with approximately 57% share in 2025. The companion animal segment is growing fastest, driven by rising pet ownership worldwide.

-

By Product, the ectoparasiticides segment dominated the veterinary parasiticides market with approximately 49% share in 2025. The endectocides segment is growing fastest, driven by demand for combination treatments.

-

By Route of Administration, the topical segment dominated the veterinary parasiticides market with approximately 39% share in 2025. The oral segment is growing fastest, driven by chewable tablet convenience.

-

By Distribution Channel, the hospital/clinic pharmacy segment dominated the veterinary parasiticides market with the largest share in 2025. The e-commerce segment is growing fastest.

By Animal Type, production animal dominates, companion animal grows fastest

Production animals held the largest share of the market in 2025, at about 57%. Rising global demand for meat and dairy products drives this dominance. Effective parasite control is essential for healthy, productive livestock. Governments worldwide are investing heavily in agricultural disease prevention programs. The USDA has promoted sustainable farming practices that include parasiticide use. Livestock health directly affects food safety and supply for a growing population. The economic stakes are high too, since livestock is a major part of many national economies. In North America, the U.S. holds a substantial share of this segment. Advanced veterinary care and supportive regulatory frameworks both help sustain this lead. These factors keep production animal parasiticides as the largest category overall.

Companion animals are now the fastest-growing segment in this market. Rising pet ownership worldwide is the clear driver behind this trend. Nearly 56% of people globally now identify as pet parents. Almost half of these are first-time pet owners, especially among younger generations. This emotional connection between pets and owners keeps driving health spending higher. People increasingly view pets as full family members rather than just animals. This shift pushes demand for premium, effective parasite prevention products. As global pet adoption keeps climbing, this segment should keep outpacing the broader market.

By Product, ectoparasiticides dominate, endectocides grow fastest

Ectoparasiticides held the largest product share in 2025, at about 49%. Ticks and fleas pose a serious health threat to both livestock and companion animals. Governments have supported research into more effective ectoparasiticide formulas. Oral chewable tablets like NexGard and Bravecto have seen especially strong adoption. The EPA plays a key regulatory role here. It ensures these products stay safe and effective for widespread use. Consumer preference for easy, convenient treatments adds further momentum to this segment. As pet ownership keeps rising globally, more owners want simple solutions for tick and flea control. This consumer demand keeps driving innovation across the entire ectoparasiticide category.

Endectocides are growing the fastest among all product types. These products combine ectoparasite and endoparasite protection into a single treatment. Pet owners increasingly prefer fewer products that cover broader parasite ranges. This convenience factor is a major reason behind the segment’s rapid growth. Newer combination formulas also improve treatment compliance significantly. Missed doses become less of a concern when one product handles multiple parasite types. As veterinary medicine keeps innovating, more combination products should reach the market soon. This trend should keep pushing endectocide growth well above the category average.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

42.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

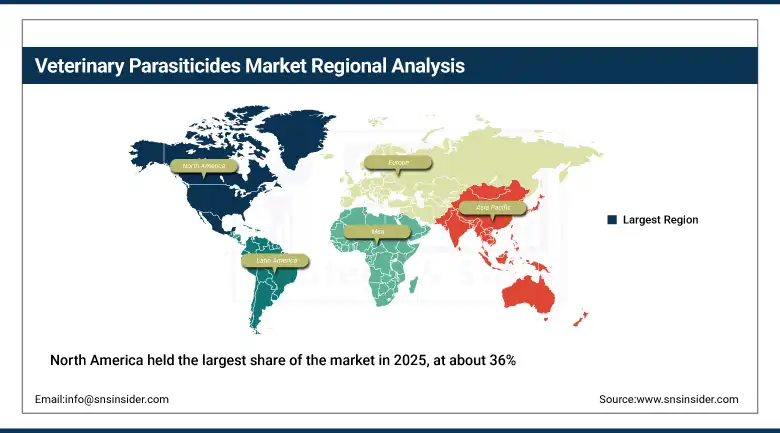

North America Veterinary Parasiticides Market Insights

North America held the largest share of the market in 2025, at about 36%. Rising pet adoption and well-developed veterinary care systems both drive this lead. The United States holds a large share within this region. A big animal population combined with strong health infrastructure supports this position. Canada also contributes meaningful demand through its growing companion animal sector.

The United States accounts for approximately 82.5% of North American revenue. Strong animal health awareness and strict disease control rules help maintain this lead. Companies like Zoetis and Elanco run major operations across the country. This regional dominance should continue through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Veterinary Parasiticides Market Insights

Europe is also a key market for veterinary parasiticides. Rising pet adoption and growing animal healthcare spending both support this position. Strong R&D investment in veterinary medicine keeps the region competitive globally. Germany accounts for approximately 24.6% of European revenue. France and the United Kingdom also contribute substantial demand across the continent.

Regulatory challenges vary across European countries and can slow product approvals somewhat. Boehringer Ingelheim and Bayer AG both run significant operations across the continent. Growing concern about environmental impact from certain chemicals is also shaping product development. This pushes companies toward safer, more targeted formulas. Several national veterinary associations are also updating treatment guidelines to reduce overuse.

Asia Pacific Veterinary Parasiticides Market Insights

Asia Pacific is the fastest-growing veterinary parasiticides market today. Rising livestock production and growing pet adoption both drive this rapid growth. China and India are leading this regional expansion. Government initiatives to improve animal health infrastructure are also helping.

China accounts for approximately 42.8% of Asia Pacific revenue. Rising disposable income and changing attitudes toward pet ownership both fuel demand. India’s pet care market is also expanding quickly. This regional growth should keep outpacing the global average through the forecast period.

MEA & Latin America Veterinary Parasiticides Market Insights

The UAE leads MEA revenue. Growing veterinary infrastructure and rising pet ownership both support this position. Saudi Arabia’s agricultural modernization efforts are also adding to regional demand. South Africa contributes additional volume through its established livestock sector.

Brazil leads Latin American revenue. A large livestock sector and growing companion animal population both drive this lead. Mexico and Argentina contribute secondary demand through their own expanding veterinary markets. Rising urbanization across the region is also boosting pet ownership rates steadily.

Market Dynamics

Growth Drivers: Rising pet ownership and growing concern about zoonotic disease driving stronger parasite control demand

Rising pet ownership worldwide is a major growth driver. Younger generations are adopting pets at record rates. Nearly 56% of people globally now identify as pet parents. Almost half of these are first-time owners, especially among Gen Z and Millennials. This wave of new pet ownership strengthens the emotional bond between owners and animals. People increasingly view pets as central to their lives and daily routines. This drives higher spending on veterinary services and parasite prevention products. American pet owners alone spent roughly USD 151 billion on pet care in 2024.

Zoonotic disease concerns add another important growth layer. These diseases can spread from animals to humans, raising public health stakes. Government health agencies report tens of thousands of zoonotic cases every year. This keeps pressure on pet owners and farmers to maintain strict parasite control. China’s pet care spending has also surged, reaching roughly USD 42 billion recently. Rising urbanization and easing pet ownership rules are both fueling this growth. Veterinary clinics worldwide are reporting steady increases in parasite-prevention product sales. Together, these factors keep demand for parasiticides climbing steadily worldwide.

Restraints: Strict regulatory approval processes and environmental safety concerns slowing new product launches

Stringent regulatory challenges represent one of the key factors that limit the growth potential of this market. Both the FDA and the European Medicines Agency apply very strict product approval process. This can result in significant delays in releasing any new products onto the market. Concerns related to environmental safety have been growing recently. Scientists at the University of Sussex have found flea treatment chemicals in UK rivers. Such substances as imidacloprid and fipronil can pose risks to river ecology and wildlife. British veterinarians are now advised to minimize preventive treatments.

This poses another challenge for manufacturers as authorities might consider imposing stricter rules when it comes to some specific active ingredients. This will result in longer product approval periods and additional limitations to using such products. Smaller manufacturers will find it increasingly difficult to cope with higher compliance requirements. At the same time, big companies with larger research budgets will be able to manage this problem successfully.

Opportunities: Rapid pet care growth across Asia Pacific creating substantial untapped market potential

Asia Pacific presents a lucrative growth area, particularly in China and India. There is an increase in urban population and disposable income, resulting in more pet adoptions in the region. Over half of the pet owners in China see their pet as their child. This humanization creates a demand for quality pet-related products and healthcare services. In South Korea, sales of pet strollers exceed those of baby strollers. India is home to another rapidly growing market for pets with approximately 31 million dogs owned in the country.

The Indian veterinary healthcare segment, valued at roughly $169 million, continues to grow due to increased accessibility. All these suggest considerable growth potential in the region. Businesses that can set up their own channels will be able to secure a sizable market share. Local manufacturing arrangements can be useful in combating regional pricing pressures too. With increasing focus on pet health in the Asia Pacific, there will continue to be a consistent demand for parasiticides.

Recent Developments:

-

2024: The FDA approved Elanco’s Credelio Quattro, a monthly chewable tablet treating fleas, ticks, roundworms, hookworms, tapeworms, and heartworms in dogs eight weeks and older.

-

2024: Merck Animal Health received European approval for BRAVECTO TriUNO, a single chewable tablet treating both internal and external parasites in dogs.

-

2024: University of Queensland research found nearly 70% of dog hookworm samples carried genetic mutations linked to dewormer resistance, highlighting a growing industry challenge.

Veterinary Parasiticides Market Key Players are:

-

Zoetis Inc.

-

Boehringer Ingelheim

-

Merck Animal Health

-

Elanco Animal Health

-

Bayer AG

-

Virbac

-

Ceva Santé Animale

-

Vetoquinol S.A.

-

Dechra Pharmaceuticals

-

Bimeda Animal Health

-

Norbrook

-

Phibro Animal Health Corporation

-

PetIQ Inc.

-

ECO Animal Health Group plc

-

Chanelle Pharma

-

Krka Group

-

SmartVet Holdings

-

Neogen Corporation

-

AdvaCare Pharma

Veterinary Parasiticides Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.69 Billion |

| Market Size by 2035 | USD 22.67 Billion |

| CAGR | CAGR of 7.8% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Ectoparasiticides, Endoparasiticides, Endectocides) • By Animal Type (Production Animal, Companion Animal) • By Distribution Channel (E-Commerce, Retail, Hospital/Clinic Pharmacy, Others) • By Route of Administration (Oral, Injectable, Topical) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Zoetis Inc., Boehringer Ingelheim, Merck Animal Health, Elanco Animal Health, Bayer AG, Virbac, Ceva Santé Animale, Vetoquinol S.A., Dechra Pharmaceuticals, Bimeda Animal Health, Norbrook, Phibro Animal Health Corporation, PetIQ Inc., ECO Animal Health Group plc, Chanelle Pharma, Krka Group, SmartVet Holdings, Neogen Corporation, and AdvaCare Pharma |

Frequently Asked Questions

The Veterinary Parasiticides Market is expected to grow at a CAGR of 7.8% from 2026 to 2035.

The Veterinary Parasiticides Market was valued at USD 10.69 Billion in 2025.

Rising pet ownership worldwide, growing zoonotic disease concern, and rapid pet care growth across Asia Pacific are the primary growth factors.

The Production Animal segment dominated the Veterinary Parasiticides Market with approximately 57% share in 2025.

North America dominated the Veterinary Parasiticides Market with approximately 36% revenue share in 2025.

Get in Touch