Anti-Corrosive Packaging Market Report Scope & Overview:

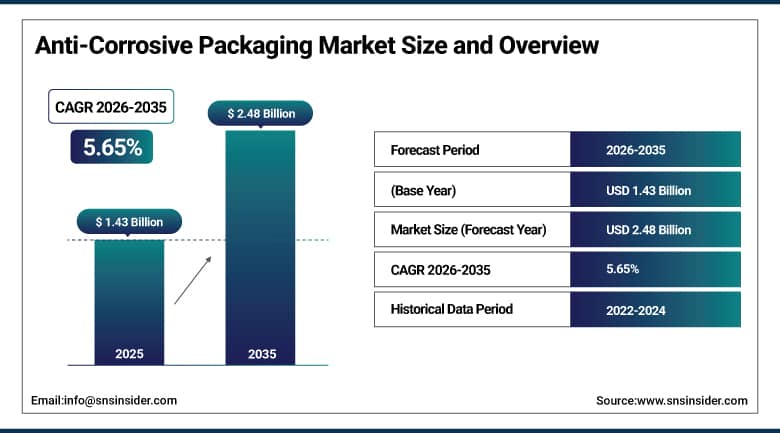

The Anti-Corrosive Packaging Market was valued at USD 1.43 Billion in 2025 and is projected to reach USD 2.48 Billion by 2035, expanding at a CAGR of 5.65% during the forecast period 2026–2035.

The anti-corrosive packaging market is growing steadily because of the need to protect metal pieces, machinery, car parts, and electronics during transport and storage. Companies that rely on exports are using new corrosion-resistant materials with special barriers and VCI to stop product damage and save on upkeep. As more factories get automated and global trade expands, there's more demand for high-tech protective packaging in production areas worldwide.

By 2026, several packaging makers boosted their recyclable VCI-based material output. They did this to back up higher export needs from auto and industrial gear producers.

Market Size and Forecast:

-

Market Size 2026E: USD 1.51 Billion

-

Market Size 2035: USD 2.48 Billion

-

CAGR: 5.65% from 2026 to 2035

-

Fastest Growing Region: Latin America

-

Largest Region: North America

To Get More Information On Anti-Corrosive Packaging Market - Request Free Sample Report

Anti-Corrosive Packaging Market Trends:

-

Rising adoption of recyclable VCI-based industrial packaging materials.

-

Expansion of RFID-enabled logistics and warehouse traceability systems.

-

Increasing integration of humidity-monitoring smart packaging technologies.

-

Growth in cloud-connected industrial inventory monitoring platforms.

-

Rising deployment of sustainable multilayer corrosion protection films.

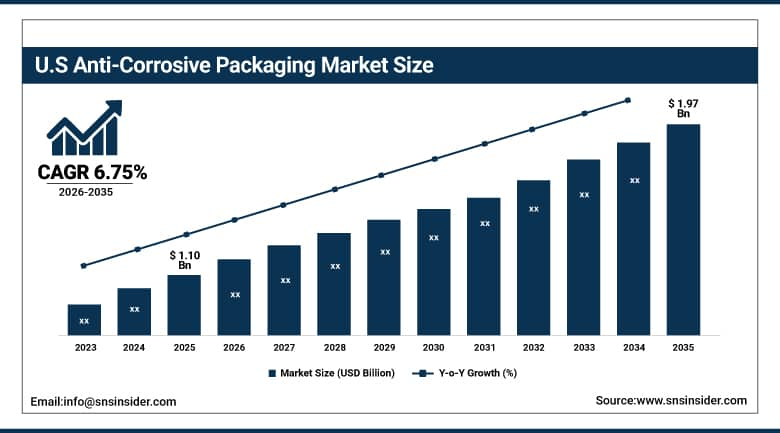

U.S. Anti-Corrosive Packaging Market Size Outlook:

The U.S. Anti-Corrosive Packaging Market was valued at USD 1.10 billion in 2025 and is expected to reach approximately USD 1.97 billion by 2035, expanding at a CAGR of 6.75% during 2026–2035.

The United States leads the North American anti-corrosive packaging market because of its strong automotive exports, advanced manufacturing, and tech needs in aerospace and electronics. Companies there quickly took on RFID packaging with cloud-logistics, boosting warehouse views and shipping accuracy. Plus, more funds in eco-friendly materials are spurring business growth in US plants.

In 2025, several U.S.-based industrial packaging suppliers introduced recyclable anti-corrosion PE packaging systems integrated with digital warehouse monitoring technologies for industrial export applications.

Anti-Corrosive Packaging Market Segment Analysis:

-

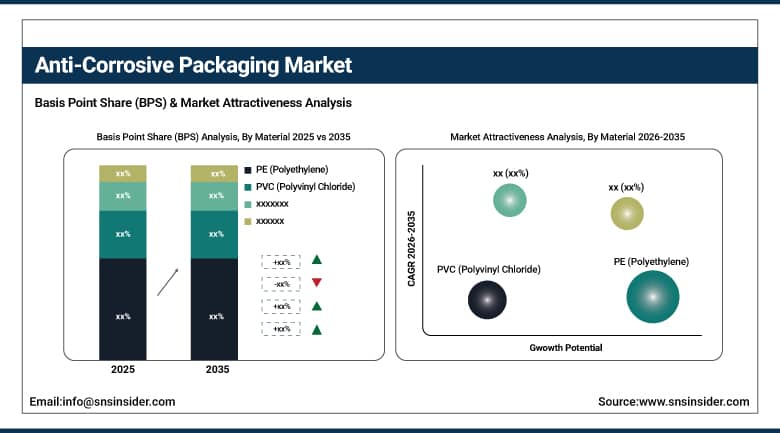

By Material, the PE (Polyethylene) segment dominated the market with 68.30% share in 2025, while the others segment is projected to register the fastest CAGR of 6.45% during the forecast period.

-

By Product Type, the Bags segment dominated the market with 46.00% share in 2025, and is the fastest growing product category.

-

By Application, the automotive segment dominated the market with 31.00% share in 2025, while the Industrial Goods segment is projected to witness the fastest growth during the forecast period.

By Material, PE (Polyethylene) segment dominated, while others segment is fastest-growing.

The PE (Polyethylene) segment accounted for approximately USD 0.98 billion in 2025 and held a dominant market share of 68.30% owing to its high moisture resistance, cost efficiency, flexibility, and strong applicability across industrial transportation and export packaging operations. Polyethylene-based anti-corrosion packaging solutions are extensively used for automotive components, industrial spare parts, and electronic equipment due to superior durability and operational convenience. The Others segment is projected to register the fastest CAGR of 6.45% during the forecast period driven by increasing commercialization of biodegradable and multi-layer corrosion-resistant materials.

In 2026, several industrial packaging manufacturers introduced advanced recyclable anti-corrosion films using hybrid barrier materials integrated with smart warehouse traceability systems for export-oriented industrial applications.

By Product Type, Bags segment dominated the market and is projected to remain the fastest-growing segment.

The Bags segment contributed nearly USD 0.66 billion in 2025 and accounted for 46.00% of total market revenue owing to rising adoption across automotive component transportation, industrial machinery storage, and electronics export logistics. Anti-corrosive bags offer operational flexibility, cost-effective deployment, and efficient contamination protection for metal-based industrial products during domestic and international shipment cycles. The segment continues to gain commercial traction due to growing investments in automated industrial packaging infrastructure and smart inventory handling technologies.

In 2025, several industrial exporters increased procurement of VCI-based anti-corrosion bags integrated with RFID shipment tracking labels and cloud-based logistics management systems to improve supply chain visibility and reduce corrosion-related operational losses.

By Application, Automotive segment dominated, while Industrial Goods segment is fastest-growth.

The Automotive segment generated approximately USD 0.44 billion in 2025 and captured 31.00% market share due to increasing exports of automotive components, engines, transmission systems, and precision metal assemblies requiring corrosion-resistant protective packaging solutions. Automotive manufacturers are increasingly implementing advanced anti-corrosion packaging technologies to reduce replacement costs, improve inventory preservation, and enhance export quality compliance standards. The Industrial Goods segment is projected to witness the fastest growth during the forecast period owing to increasing global industrialization and expansion of heavy equipment manufacturing operations.

During 2026, multiple automotive component suppliers implemented AI-enabled packaging inspection systems integrated with humidity analytics and cloud-based inventory monitoring platforms to improve anti-corrosion packaging efficiency across export operations.

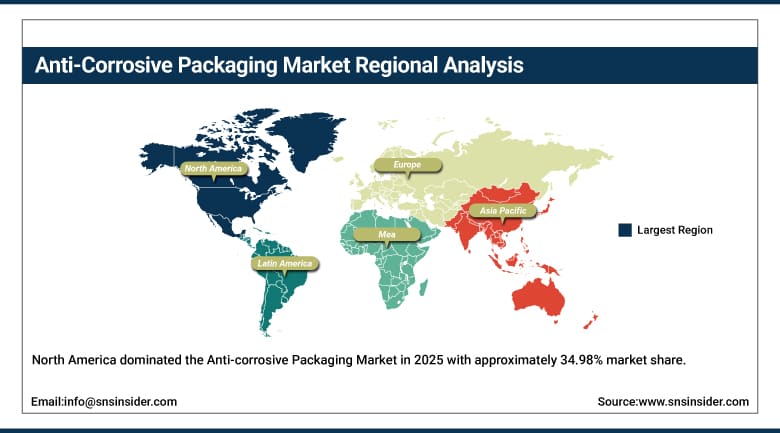

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

34.98% |

|

Europe |

Germany |

25.00% |

|

Asia Pacific |

China |

34.00% |

|

Middle East & Africa |

UAE |

0.02% |

|

Latin America |

Brazil |

6.00% |

North America Anti-Corrosive Packaging Market Insights

North America dominated the Anti-corrosive Packaging Market in 2025 with approximately 34.98% market share owing to strong industrial manufacturing infrastructure, rising export activities, and increasing investments in advanced industrial packaging systems. The presence of large automotive manufacturers, electronics exporters, and heavy machinery producers continues to support regional demand for corrosion-prevention packaging solutions. Increasing implementation of automated warehouse systems and RFID-enabled logistics infrastructure is further accelerating adoption across industrial supply chains.

In 2025, several North American industrial packaging providers expanded production capacity for recyclable VCI packaging materials integrated with smart logistics monitoring technologies for automotive and industrial export applications.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Anti-corrosive Packaging Market Insights

Europe accounted for nearly 22.30% of the global anti-corrosive packaging market in 2025 due to stringent industrial quality regulations, increasing focus on sustainable packaging materials, and strong export-oriented manufacturing industries. Germany, France, Italy, and the United Kingdom continue to invest in advanced industrial packaging technologies supporting automotive and precision engineering sectors. Regional emphasis on recyclable materials and environmentally compliant industrial packaging solutions is driving commercialization of lightweight anti-corrosion films and barrier materials.

In 2026, multiple European industrial packaging manufacturers launched recyclable VCI packaging solutions designed for export-oriented automotive component transportation and industrial warehouse applications.

Asia Pacific Anti-corrosive Packaging Market Insights

Asia Pacific held approximately 34.00% revenue share in 2025 owing to expanding industrial manufacturing activities, rapid electronics production growth, and increasing automotive exports from China, India, Japan, and South Korea. The region is witnessing strong investments in industrial logistics modernization, automated packaging facilities, and smart warehousing infrastructure. Industrial manufacturers are increasingly adopting cost-efficient anti-corrosion packaging solutions integrated with digital logistics management systems to reduce product damage during international transportation.

During 2025–2026, several Asia Pacific-based industrial exporters implemented RFID-integrated anti-corrosion packaging systems with cloud-based shipment visibility solutions to improve operational efficiency and export product protection.

Middle East & Africa and Latin America Anti-corrosive Packaging Market Insights

The Middle East & Africa region is projected to register a CAGR of 0.08% during the forecast period owing to rising industrial diversification projects, expanding manufacturing infrastructure, and increasing investments in export logistics modernization. Latin America is steadily emerging as a growth market due to increasing automotive component exports and expansion of industrial manufacturing operations across Brazil and Mexico.

In 2026, multiple industrial logistics providers across the Middle East expanded deployment of smart warehouse monitoring technologies integrated with anti-corrosion packaging analytics systems to improve industrial export efficiency.

Market Dynamics:

Growth Drivers: Expansion of industrial exports and smart logistics infrastructure accelerating adoption.

Increasing international trade activities involving automotive parts, industrial machinery, and electronic equipment are significantly driving demand for anti-corrosive packaging solutions globally. Manufacturers are focusing on reducing corrosion-related product losses during storage and transportation through adoption of advanced VCI films, moisture barrier bags, and smart packaging systems. Integration of RFID tracking technologies and cloud-based shipment monitoring platforms is improving operational visibility while enabling predictive inventory protection strategies across industrial supply chains.

In 2025, several industrial exporters implemented AI-supported warehouse analytics integrated with anti-corrosion packaging inspection systems to improve inventory preservation and export quality management.

Restraints: Volatility in raw material prices and sustainability compliance challenges.

The anti-corrosive packaging market continues to face operational challenges associated with fluctuating raw material prices, environmental regulations on plastic usage, and high transition costs toward recyclable industrial packaging materials. Industrial packaging manufacturers are under pressure to balance corrosion protection efficiency with sustainability compliance and cost optimization requirements. Smaller packaging suppliers also face challenges associated with modernization of manufacturing infrastructure and adoption of advanced smart packaging technologies.

During 2026, several industrial packaging manufacturers announced investments in sustainable material innovation programs to address regulatory pressure surrounding conventional plastic-based packaging products.

Opportunities: AI-enabled packaging analytics and recyclable protective materials creating long-term commercial potential .

Growing investments in smart warehouses, industrial automation, and connected logistics ecosystems are creating long-term growth opportunities for anti-corrosive packaging solution providers. Industrial manufacturers are increasingly deploying AI-enabled packaging inspection systems capable of monitoring environmental exposure risks and optimizing packaging performance during shipment cycles. Commercial expansion of recyclable barrier materials and advanced biodegradable anti-corrosion films is expected to strengthen future market competitiveness across global industrial supply chains.

In 2025, multiple industrial packaging companies expanded development of AI-integrated anti-corrosion packaging analytics platforms supporting predictive inventory protection and cloud-based export logistics monitoring systems.

Recent Developments:

-

2026: Several industrial packaging companies launched recyclable anti-corrosion packaging films integrated with RFID-enabled shipment visibility technologies.

-

2026: Multiple automotive exporters expanded implementation of AI-based warehouse monitoring systems supporting predictive corrosion prevention analytics.

-

2025: Industrial packaging manufacturers increased commercialization of moisture-resistant VCI packaging solutions for electronics and heavy machinery exports.

-

2025: Multiple smart warehouse operators implemented cloud-based industrial inventory monitoring platforms integrated with anti-corrosion packaging analytics systems.

Anti-corrosive Packaging Market Key Players are:

-

Cortec Corporation

-

Daubert Cromwell Inc.

-

Branopac GmbH

-

Armor Protective Packaging

-

Zerust Excor

-

Transcendia Inc.

-

Aicello Corporation

-

Intertape Polymer Group Inc.

-

Protective Packaging Corporation

-

RustX USA

-

Green Packaging Inc.

-

Nefab Group

-

Smurfit Westrock plc

-

Pregis LLC

-

CGP Coating Innovation

-

MetPro Group

-

Technology Packaging Ltd.

-

Polyplus Packaging

-

Shanghai Jinglin Packaging Products Co. Ltd.

-

CVC Packaging India Pvt. Ltd.

Anti-Corrosive Packaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.43 Billion |

| Market Size by 2035 | USD 2.48 Billion |

| CAGR | CAGR of 5.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Packaging Material Assessment, Corrosion Protection Technology Trends, Supply Chain Evaluation, Industrial Packaging Demand Analysis, Sustainability Assessment, DROC & SWOT Analysis, Regulatory Framework Analysis, Innovation Benchmarking, and Future Market Opportunity Evaluation |

| Key Segments | • By Material (PE (Polyethylene), PVC (Polyvinyl Chloride), Others) • By Product Type (Bags, Foils, Others) • By Application (Electrical & Electronics, Automotive, Consumer Goods, Industrial Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cortec Corporation, Daubert Cromwell Inc., Branopac GmbH, Armor Protective Packaging, Zerust Excor, Transcendia Inc., Aicello Corporation, Intertape Polymer Group Inc., Protective Packaging Corporation, RustX USA, Green Packaging Inc., Nefab Group, Smurfit Westrock plc, Pregis LLC, CGP Coating Innovation, MetPro Group, Technology Packaging Ltd., Polyplus Packaging, Shanghai Jinglin Packaging Products Co. Ltd., and CVC Packaging India Pvt. Ltd. |

Frequently Asked Questions

The Anti-corrosive Packaging Market was valued at USD 1.43 billion in 2025.

The market is projected to reach USD 2.48 billion by 2035.

The market is expected to expand at a CAGR of 5.65% during the forecast period.

North America dominated the global market owing to strong industrial manufacturing infrastructure and increasing adoption of advanced export-grade protective packaging solutions.

PE (Polyethylene) accounted for the largest revenue share that is 68.30% in 2025.

Get in Touch