Aqueous-based Metal Cleaners Market Report Scope & Overview:

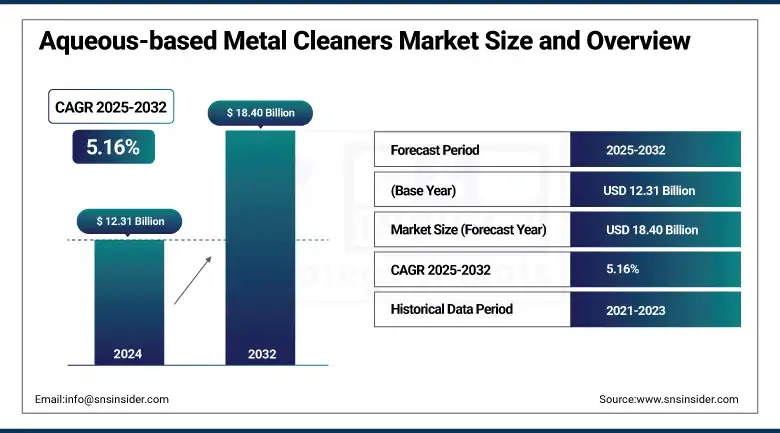

The Aqueous-based Metal Cleaners market size was valued at USD 12.31 billion in 2024 and is expected to reach USD 18.40 billion by 2032, growing at a CAGR of 5.16% over the forecast period of 2025-2032.

The Aqueous-based Metal Cleaners Market is propelled by environmental legislation and demand for 24/7 Water-based Metal Cleaning Agents in green manufacturing. Industrial Aqueous Metal Cleaners are increasingly industry 4.0 integrated with digital performance monitoring and hybrid ultrasonic-spray systems that add to the efficiency of the washer. Aqueous-based Metal Cleaners Market Trends. Some key trends that we have witnessed in the aqueous-based metal cleaners’ market are enzyme-enhanced biodegradable surfactants and two-stage alkaline-acid cleaning, especially in the automotive and electronics industries.

To Get more information On Aqueous-based Metal Cleaners Market - Request Free Sample Report

Metal products & machinery effluent guidelines apply to more than 2,400 facilities, including due with oily wastewater according to the US EPA. Trichloroethylene Broadcast Drain Pollution Prevention case studies show that as much as 90% less trichloroethylene waste is generated once an aqueous system is in place. Further, the U.S. cleaning products industry contributed approximately $200 billion to the economy and supported an estimated 700,000 jobs in 2019, demonstrating the strength of the Metal Cleaning Chemical market and Aqueous-based Metal Cleaners Market Growth and adding value to innovation by leading Aqueous-based Metal Cleaners companies.

Market Dynamics

Drivers

-

Adoption of Industry 4.0 Digital Monitoring Optimizes Cleaning Efficiency and Resource Utilization

The prominence of IoT-enabled sensors and cloud-based analytics in the aqueous-based metal cleaners market is facilitating a real-time monitoring of bath composition, pH, and conductivity, which in turn helps in improving bath life and reducing chemical consumption. Companies using the ultrasonic/spray hybrid system are lowering water consumption by 20–30% and detergent costs by 15–25% with the help of predictive maintenance schedules. One such major U.S.-based automotive OEM reported how, installation of inline conductivity probes reduced rinse-water drag-out losses by 22%, increasing the market share and reliability of aqueous-based metal cleaners. These digital innovations also enable on-the-go compliance documentation, which is important for metal cleaning chemical market players in attaining their net-zero carbon ambitions.

-

Growing Demand for Biodegradable Enzyme-Enhanced Formulations Aligns with Corporate Net-Zero Goals

Corporate sustainability initiatives are driving the advancement of enzyme-boosted, 100% biodegradable industrial aqueous metal cleaners, allowing customers to minimize lifecycle emissions and wastewater treatment costs. Britemor 921 from Chemetall has an extremely low COD/BOD ratio that reduces the number of rinse-water contaminants by more than 40% compared to traditional products. Likewise, top formulators are adding protease- and lipase-based concentrates that offer the same level of soil removal, but at levels up to 30% lower, a response to end-user needs for eco-friendly solutions in the electronics, healthcare, and fine machining fields. This momentum highlights the crucial role of green innovation in generating sustained aqueous-based metal cleaners market expansion and in maintaining market leadership for the aqueous-based metal cleaners.

Restraints

-

Complex Wastewater Discharge Regulations Increase Compliance Burden for Users

The administrative burden of complying with multiple overlapping federal, state, and local discharge standards for TSS, oil and grease, and pH (as established by the EPA effluent guidelines) is material. According to National Pollutant Discharge Elimination System permits, facilities are required to monitor a range of factors and to periodically submit discharge monitoring reports, which, when including the costs of laboratory and reporting annually, can range from $50,000 to $100,000. This complexity disproportionately affects small manufacturers without in-house environmental expertise, leading to a reluctance to fully accept Industrial aqueous metal cleaners despite obvious environmental advantages. Consequently, some processes do not invest in advanced treatment technology, and those bottlenecks obstruct the general aqueous metal cleaners market sustainability trends.

Segmentation Analysis

By Cleaning Chemical

Sequestrants and inhibitors dominated the aqueous-based metal cleaners market through 2024, with zeolite-based chemistries dominating due to the phenomenal scale and corrosion control in industrial washers. More than 2,400 facilities are required by the EPA to control the levels of oil, grease, and suspended solids that can be discharged from point sources under the Metal Products & Machinery Effluent Guidelines, leading to a trend in the adoption of sequestrant blends, which can extend bath life and reduce rinse cycles. This transition is aligned with its sustainability; Users have reported 30–40% savings in chemical replenishment, with easier documentation for compliance, enhancing the metal cleaning chemical market transition towards sustainable phosphor-free solutions.

On the other hand, the surfactants emerged as the fastest growing segment with the highest CAGR of 5.86%, driven by non-ionic glycol ether blends that enhance the oil emulsification at lower temperatures as well as reducing the drag-out of the deposit into the wastewater. For example, Pollution Prevention case studies indicate that those plants which converted to advanced surfactant systems reduced their use of trichloroethylene by 90% and saved over $170,000 annually in compliance costs. The trend also supports the Water-based Metal Cleaning Solutions' focus on low-VOC, biodegradable ingredients as a means of meeting tightening effluent limits while improving or equaling cleaning performance.

By Technology

Ultrasonic cleaning dominated the aqueous-based metal cleaners market with 40.5% market share in 2024. The dominance is fueled by cavitation tank systems that can strip soils without harsh chemicals. Based on work sponsored by the U.S. Department of Energy, these systems have a volumetric throughput of more than 92% water, which equates to substantially less solvent usage, which accommodates both federal sustainability objectives and local wastewater control regulations. Ultrasonic baths have been adopted by major automotive OEMs to clean complex engine parts, providing cycle times that are up 25% faster and energy consumption that is 20% less than traditional cleaning techniques.

Spray cleaning is projected to be the fastest growing segment and registered a CAGR of 6.10%, propelled by air-atomized nozzle sub-systems that provide finer misting and decrease the water usage up to 15%. Spray-rinse rigs reduce bath drag-out by 25% according to EPA Pollution Prevention reviews, both minimizing chemical loss and wastewater generation. This ability is particularly appreciated in aerospace component cleaning, where precise, automated spray cycles are used to effectively remove contamination, ensuring repeatable residue removal and repeatability to the ±5% maximum residue limits mandated by the most stringent military and FAA surface-treatment specifications.

By Form

Liquid forms led the aqueous-based metal cleaners market with a market share of 58.9% in 2024, with the technology being helped by low-viscosity alkali concentrates that penetrate soils rapidly in conveyorized wash lines. the American Cleaning Institute's Cold Water Saves campaign: Liquid formulas had the potential to save up to 36% water over gels and powders, supporting the shift to Industrial Aqueous Metal Cleaners in environmentally conscious plants. The leading electronics manufacturers have found that liquid concentrates make bath monitoring and addition easier, minimize downtime, and help decrease the aqueous-based metal cleaners market growth by allowing them to work more efficiently at lower life-cycle costs.

Paste forms are projected to be the fastest growing segment with a CAGR of 6.44%, and thixotropic sodium silicate-based pastes are the sub-segment sales leader. These high-viscosity pastes adhere to vertical surfaces to reduce run-off and chemical use by 18% in precision electronics cleaning, according to Pollution Prevention recording. This is in line with continued aqueous-based metal cleaners market trends for pinpoint application to increase contact time, minimize waste, and sit within stringent wastewater discharge regulations whilst not negatively impacting cleaning performance.

By End-use Industry

In 2024, manufacturing was the leading application, accounting for 52.5%, especially automotive OEM lines, where enzyme-boosted chemistries in inline spray-rinse systems are used to meet NPDES permit limits. Two-stage alkaline-acid cleaning adoption has been spurred by EPA requirements for the metal products & machinery segment, which has trimmed rinse-water chemical load by 40% while delivering uniform surface preparation for painting, plating. This performance solidifies manufacturing’s grip on the aqueous-based metal cleaners market report and demonstrates how the metal cleaning chemical market has transitioned towards powerhouse, modular cleaning solutions.

Healthcare emerged as the fastest-growing application for ultrasonic-spray hybrid systems, with a CAGR of 6.67%, as of 2018. According to data from Infection Control, CDC guidelines require debridement involving thorough cleaning before sterilization, and pulp-dissolving, enzyme-enhanced aqueous cleaners deliver more than 90% bioburden reduction. According to hospitals, these systems reduce the time required for manual scrubbing by up to 35%, provide a validated, traceable record, and support patient-safety initiatives, driving rapid adoption in the aqueous-based metal cleaners market.

Regional Analysis

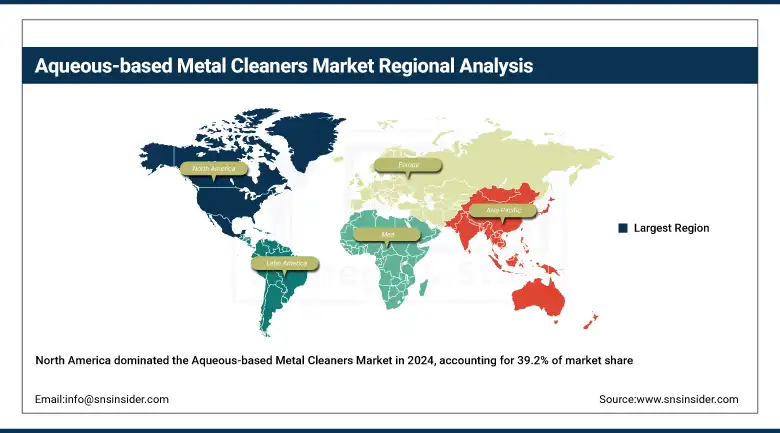

North America dominated and held the largest share of about 39.2% in the aqueous-based metal cleaners market in 2024, with growth in the region driven mainly by the U.S., as the EPA’s Metal Products & Machinery Effluent Guidelines (40 CFR Part 438) necessitate aqueous cleaning for over 2,400 facilities in the U.S., forcing Ultrasonics and new Spray-Rinse hybrids to comply while saving money. Canada lags, under Environment Canada’s Pollution Prevention Planning Handbook, calling up steel mills and mining plants to recondition wash baths and cut chemical loads. Mexico is beginning to apply pressure to the import of toxic materials in such a way that they have installed local aqueous system installations to slow down the movement of hazardous waste across borders.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe accounted for a 30.4% share of the aqueous-based metal cleaners market in 2024. Mechanisms to reduce Wastewater contaminants have moved to the forefront in Germany, with strict REACH heavy‐metal directives and the Industrial Emissions Directive fueling enzyme‐enhanced ultrasonics in automotive and precision engineering plants. In France Water Reuse Regulation (EU 2020/741) is used to treat rinse water, in Italy, the circularity incentives of the Clean Industry Deal for IoT-monitored spray-rinse lines acted to fund the deployment of industrial aqueous metal cleaners.

Asia Pacific dominated and accounted for a market share of 22.1% of the aqueous-based metal cleaners market in 2024, headed by China, where MEE's "GB 8978" wastewater regulations and 34 heavy‐metal emission regulations require sophisticated aqueous treatments, speeding ultrasonic‐spray uptake in steel and electronics clusters. India employs Zero Liquid Discharge according to CPCB standards in car clusters, propelling enzyme‐enhanced concentrates, while Japan applies Industry 4.0 bath‐monitoring sensors to maximize Water-based Metal Cleaning Solutions and minimize drag‐out losses.

Key Players

The major competitors in the aqueous-based metal cleaners market include BASF SE, Dow Inc., Stepan Company, Evonik Industries AG, Eastman Chemical Company, Clariant AG, Nouryon, Henkel AG & Co. KGaA, Chemetall (a BASF subsidiary), and Quaker Houghton

Recent Developments

-

April 2025: BASF launched Trilon G, a sustainable chelating agent for cleaning applications, offering improved performance, cost efficiency, and biodegradability, meeting sustainability goals in industrial and home care.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 12.31 billion |

| Market Size by 2032 | USD 18.40 billion |

| CAGR | CAGR of 5.16% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Cleaning Chemical (Builders, Sequestrants and inhibitors, Surfactants, Others) •By Technology (Ultrasonic, Rinse, Dip, Spray) •By Form (Liquid, Paste, Gel, Powder) •By End-use Industry (Manufacturing, Automotive & Aerospace, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Dow Inc., Stepan Company, Evonik Industries AG, Eastman Chemical Company, Clariant AG, Nouryon, Henkel AG & Co. KGaA, Chemetall (a BASF subsidiary), Quaker Houghton |

Frequently Asked Questions

The Aqueous-based Metal Cleaners market is expected to grow at a CAGR of 5.16% from 2025 to 2032, reaching USD 18.40 billion by 2032.

Industry 4.0 enhances cleaning efficiency by integrating IoT sensors and digital monitoring systems, optimizing resource utilization in the Aqueous-based Metal Cleaners market.

Key trends include the use of enzyme-enhanced biodegradable surfactants and two-stage alkaline-acid cleaning, especially in the automotive and electronics industries.

Spray cleaning is the fastest-growing segment, with a CAGR of 6.10%, driven by air-atomized nozzle sub-systems that reduce water usage in the Aqueous-based Metal Cleaners market.

North America holds the largest market share, with the U.S. contributing significantly due to strict environmental regulations and the adoption of advanced aqueous cleaning systems in the Aqueous-based Metal Cleaners market.

Get in Touch