Ethyleneamines Market Report Scope & Overview:

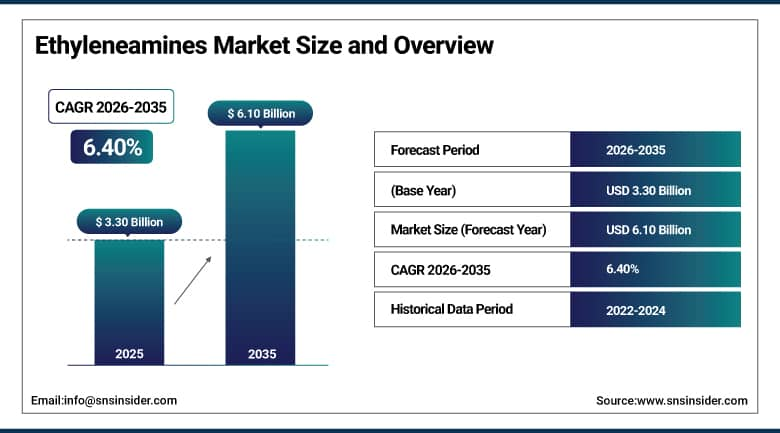

The Ethyleneamines Market was valued at USD 3.30 Billion in 2025 and is expected to reach USD 6.10 Billion by 2035, growing at a CAGR of 6.40% from 2026 to 2035.

Ethyleneamines are a commercially important family of polyamine compounds synthesized primarily by reacting ethylene dichloride with ammonia in a continuous reactor system or by the catalytic amination of monoethanolamine, yielding a series of homologous compounds whose chain length, branching, and number of amine functional groups vary systematically across the product family. Ethylenediamine, the simplest diamine in the series, serves as both the primary commercial product and the chemical precursor from which longer-chain ethyleneamines including diethylenetriamine, triethylenetetramine, tetraethylenepentamine, piperazine, aminoethylpiperazine, and pentaethylenehexamine are derived through controlled transamination reactions. The commercial significance of ethyleneamines across diverse industrial sectors reflects the unique combination of properties that their amino-functional molecular architecture provides.

Huntsman Corporation and Zamil Group completed commissioning of a 27,000 tonne per year ethyleneamines production facility at Jubail, Saudi Arabia in March 2025 through their Arabian Amines Company joint venture. The Jubail plant represents a strategically positioned manufacturing asset serving the growing Middle East and South Asian ethyleneamines demand. The facility's MEA amination production route provides a production cost structure aligned with the feedstock cost environment of the Middle East petrochemical sector.

Market Size and Forecast

-

Market Size in 2026E: USD 3.51 Billion

-

Market Size by 2035: USD 6.10 Billion

-

CAGR: 6.40% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Ethyleneamines Market - Request Free Sample Report

Ethyleneamines Market Trends

-

Wind energy expansion is increasing demand for ethyleneamine-based epoxy curing agents used in high-performance wind turbine blade manufacturing.

-

Bio-based ethyleneamine production is gaining momentum as manufacturers invest in sustainable feedstocks to meet evolving environmental and regulatory requirements.

-

Electric vehicle production is driving demand for high-purity ethyleneamine-based epoxy systems used in battery encapsulation and structural adhesives.

-

Rising investments in water treatment infrastructure are supporting ethyleneamine consumption in chelating agents and polyamine-based water treatment chemicals.

-

Growth in oil and gas processing is increasing demand for ethyleneamine derivatives used in natural gas sweetening and acid gas removal applications.

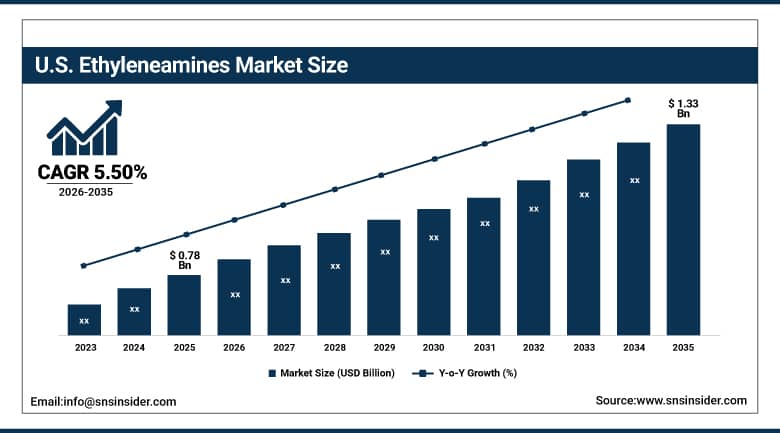

The U.S. Ethyleneamines Market Outlook

The U.S. ethyleneamines market was valued at approximately USD 0.78 Billion in 2025 and is expected to reach approximately USD 1.33 Billion by 2035, growing at a CAGR of approximately 5.50%.

The United States is the world's largest single-country ethyleneamine producer and a major consumer market, anchored by the domestic manufacturing operations of Dow Chemical whose Texas-based ethyleneamine production complex represents the world's largest single-site ethyleneamine manufacturing facility, and by Huntsman Corporation whose Port Neches, Texas facility contributes additional domestic production capacity. U.S. domestic ethyleneamine consumption is dominated by epoxy curing agent production for the U.S. coatings, adhesives, and composites industries, agrochemical manufacture for the world's largest agricultural chemical market, and oilfield chemical production for the U.S. shale gas sector's acid gas treatment operations.

In 2024, Dow Chemical Company announced continued investment into process optimization at its ethyleneamine manufacturing plant in Freeport, Texas, for better selectivity of ethyleneamines favored by the market, such as EDA and DETA, using catalysts and optimal conditions for reaction that limit the production of higher homologues less desired by the market than linear amines.

Ethyleneamines Market Segment Analysis

-

By Product Type, the ethylenediamine (EDA) segment dominated the Ethyleneamines market with 36.00% share in 2025, while the triethylenetetramine (TETA) segment is the fastest growing product during 2026 to 2035.

-

By Grade, the industrial grade segment dominated the Ethyleneamines market in 2025, while the high-purity grade segment is the fastest growing grade during 2026 to 2035.

-

By Manufacturing Process, the EDC/Ammonia Route segment dominated the Ethyleneamines Market with a 68.4% share in 2025, while the MEA Amination Route segment is the fastest growing manufacturing process during 2026 to 2035.

-

By Application, the epoxy curing agents segment dominated the Ethyleneamines market with 22.60% share in 2025, while the water treatment chemicals segment is the fastest growing application during 2026 to 2035.

-

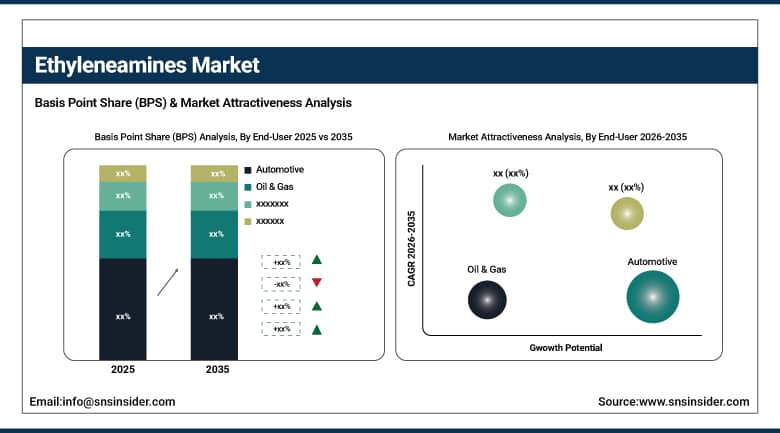

By End Use Industry, the automotive segment dominated the Ethyleneamines market with 19.30% share in 2025, while the oil & gas segment is among the fastest growing end use industries during 2026 to 2035.

By End Use Industry, automotive dominates, oil & gas grows alongside water treatment

The automotive segment generated 19.30% of Ethyleneamines market revenue in 2025 through structural adhesives for body panel bonding requiring ethyleneamine-cured epoxy systems, lubricating oil additive packages incorporating ashless dispersants and corrosion inhibitors, and fuel additive formulations where TEPA-based components improve combustion stability.

Oil and gas have started showing promise in being an important end-use application of ethyleneamines due to rising natural gas extraction and building up of infrastructure for gas processing plants. The derivatives of ethyleneamines, such as piperazine and AEP (aminoethylpiperazine), find many applications in acid gas capture and natural gas sweetening processes to capture CO2 and H2S effectively. Rising adoption of carbon capture technology, stringent emission norms, and retrofitting of CO2 capture are expected to boost demand for ethyleneamines in the oil & gas industry.

By Product Type, EDA dominates, TETA grows fastest

Ethylenediamine retained 36.00% of Ethyleneamines market revenue in 2025 through its broad reactivity profile across chelating agent production, epoxy curing, agrochemical synthesis, and pharmaceutical intermediate manufacture that diversifies its demand base across more end use categories than any individual downstream amine derivative. EDA serves as the precursor for EDTA synthesis, the most widely used industrial chelating agent, whose water treatment, detergent, and medical imaging applications create stable recurring consumption. Diethylenetriamine retains approximately 22 to 24 percent market share through performance advantages in slower-cure epoxy systems and DTPA synthesis for pulp bleaching.

Triethylenetetramine (TETA) is predicted to be the highest revenue generator among products of ethylene amines market in the period 2026-2035 owing to its moderate reactivity, curing capacity and chelation characteristics that make it an ideal chemical intermediate for preparing epoxy resins, coatings, adhesives and sealants of high performance. Growing application of TETA in composites of wind turbine blades is due to the reason that TETA imparts mechanical strength and durability to the blades. Growing investments in renewable energy, infrastructure, industrial coatings, and increasing demand for water treatment chemicals and corrosion inhibitors will drive TETA consumption.

By Application, epoxy curing agents dominate, water treatment grows fastest

Epoxy curing agents generated 22.60% of Ethyleneamines market revenue in 2025, reflecting demand across marine and protective coatings, civil engineering adhesives, electronic encapsulants, composites, and wind turbine blade infusion resins. Epoxy-amine systems cure at room temperature without external catalysts, offering strong substrate adhesion and solvent-free formulation compatibility with VOC regulations.

The water treatment chemicals segment is projected to be the fastest-growing application in the ethyleneamines market during the forecast period. Growth is driven by increasing urbanization, expanding municipal and industrial water treatment infrastructure, and rising investments in agricultural water management. Due to the excellent reactivity associated with their amine functionalities, ethyleneamines find extensive use as ingredients in polyamine coagulants, chelating agents, scale inhibitors, and corrosion control chemicals. Increasing worldwide focus on the recycling and efficient utilization of water is set to boost the demand for ethyleneamines.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

42.84% |

|

Middle East & Africa |

Saudi Arabia |

27.84% |

|

Latin America |

Brazil |

43.84% |

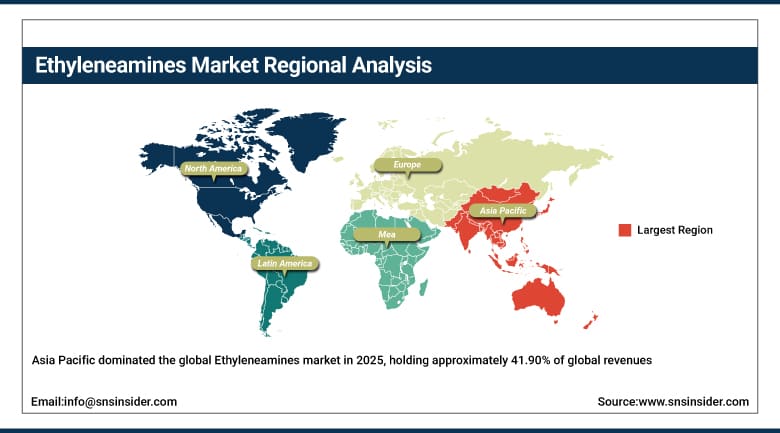

Asia Pacific Ethyleneamines Market Insights

Asia Pacific dominated the global Ethyleneamines market in 2025, holding approximately 41.90% of global revenues, and is projected to remain the largest and fastest-growing regional market through 2035. China accounts for approximately 42.84% of Asia Pacific revenues through its domestic ethyleneamine production capacity expansion at major petrochemical complexes, its world-leading agrochemical manufacturing industry creating large EDA consumption for herbicide and pesticide active ingredient synthesis, and its rapidly growing epoxy resin and wind turbine composite manufacturing sectors.

India is growing fastest within Asia Pacific through its expanding pharmaceutical API manufacturing sector whose high-purity EDA consumption is growing with domestic medicine production, and its water treatment chemical industry serving urban infrastructure investment across its rapidly urbanising population. Shandong Lianmeng Chemical and other Chinese producers are expanding capacity to serve both domestic demand growth and price-competitive export markets across the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Ethyleneamines Market Insights

North America held approximately 28% of global Ethyleneamines revenues in 2025. The United States accounts for approximately 84.73% of regional revenue through the domestic manufacturing of Dow Chemical and Huntsman Corporation, the world's largest agrochemical market creating sustained EDA demand for herbicide synthesis, and the U.S. shale gas industry's piperazine and AEP consumption in natural gas processing.

Ethyleneamines production capacity is higher than its consumption needs in North America, where the United States exports these products to Latin America and Asia-Pacific regions. Canada adds to the demand for ethyleneamines products through its need for chemicals used in oil sands processing, pulps and paper industry, and increased consumption of water treatment chemicals.

Europe Ethyleneamines Market Insights

In 2025, Europe was a prominent player in terms of global revenues of Ethyleneamines, due to robust consumption of ethyleneamines for use in the specialty chemicals, coatings, adhesives, water treatment, and advanced manufacturing segments and strict environment rules that favor high-quality chemical products. Germany holds around 28.47% of European revenues, thanks to BASF SE's integrated ethyleneamine production plant and chemical transformation processes in Ludwigshafen, which is the consumption of EDA by Germany for manufacturing specialty chemicals and its presence in the global supply chain of coatings, adhesives, and composites requiring epoxy curing agents using ethyleneamines.

The Nouryon (formerly Akzo Nobel) manufacturing plant at Delfzijl, the Netherlands, which operates via Delamine BV joint venture, is a significant source of European ethyleneamine supply. The European Union’s regulations governing the chemical industry, such as REACH substance evaluations for ethyleneamines and their derivatives, involve compliance costs that affect European market supply chain integration trends.

MEA & Latin America Ethyleneamines Market Insights

Middle East and Latin America are growing Ethyleneamines markets where new production capacity investment and downstream chemical industry development are creating expanding supply and demand dynamics. Saudi Arabia leads MEA revenues at approximately 27.84% of the regional total through the Huntsman-Zamil Arabian Amines Company joint venture facility commissioned at Jubail in 2025, whose 27,000 tonne per year capacity serves regional water treatment, oilfield chemical, and agricultural markets with MEA amination route ethyleneamine production.

The UAE, Qatar, and Egypt contribute secondary MEA demand through their oilfield chemical, water treatment, and personal care industries. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large agricultural sector whose herbicide and crop protection chemical formulation requires EDA-derived active ingredients at volumes commensurate with Brazil's position as one of the world's top three agricultural producers.

Market Dynamics

Growth Drivers: Expanding epoxy resins and water treatment infrastructure demand.

Growth in the use of renewable energy sources across the world will bring about immense growth potential for the ethyleneamines market, especially because of the rising demand for epoxy curing agents in the production of wind turbine blades. Ethyleneamines such as DETA and TETA are vital ingredients in superior epoxy resins that give wind turbine blades the necessary strength and chemical resistance. With the ongoing governmental investments in offshore and onshore wind energy generation projects, there will be an increase in the demand for these curing agents.

Furthermore, the fast-growing electric vehicle industry is driving up the demand for ethyleneamines in battery module encapsulation, adhesives, and power electronics potting compounds. This makes these materials more thermally stable and more electrically insulated. Hence, investment in renewable energy infrastructure and vehicle electrification is generating new growth prospects for ethyleneamine producers in the industrial sector.

Restraints: Volatile feedstock prices and stringent environmental regulations.

Ethyleneamine production economics are directly linked to ethylene dichloride and ammonia commodity prices in the EDC/ammonia production route, and to monoethanolamine pricing in the MEA amination route. EDC is itself derived from ethylene and chlorine whose individual market dynamics create layered price volatility exposure for integrated ethyleneamine producers whose feedstock cost management requires either vertical integration into EDC production or sophisticated commodity price hedging strategies.

REACH regulation in the European Union has placed several ethyleneamine products including ethylenediamine, diethylenetriamine, and triethylenetetramine on substances of very high concern candidate lists and substance evaluation programmes, imposing risk assessment obligations and potential use restriction processes that create regulatory uncertainty for European downstream users whose formulation practices must be documented and defended in regulatory submissions.

Opportunities: Pharmaceutical-grade ethyleneamines and carbon capture solvent applications.

High-purity pharmaceutical-grade ethyleneamines present a significant growth opportunity as pharmaceutical manufacturing and active pharmaceutical ingredient (API) production continue to expand globally, particularly across Asia Pacific. Pharmaceutical grade ethylenediamine (EDA), synthesized under extremely strict conditions, is being used increasingly in pharmaceutical products along with specialty chemicals, and this has increased its value due to the high purification process involved in its production. Another key application area for EDA derivatives is carbon capture.

The use of piperazine-based absorption solvents is prevalent in carbon dioxide capture systems after combustion due to their high capacity for absorption and regeneration. Increased investments in CCUS projects on account of stringent emission regulations and net-zero emissions targets are likely to boost the demand for ethyleneamines across the projection period.

Recent Developments:

-

2025: Huntsman Corporation and Zamil Group completed commissioning of the 27,000 tonne per year Arabian Amines Company ethyleneamines plant at Jubail, Saudi Arabia, with Huntsman holding exclusive global sales and technical rights for production output that serves Middle East and South Asian water treatment, oilfield chemical, and agricultural market demand.

-

2025: BASF SE advanced its bio-based ethyleneamine production research programme exploring fermentation-derived monoethanolamine and bio-attributed ethylene oxide feedstocks to enable renewable carbon content claims for ethyleneamine products targeting European sustainable chemistry procurement requirements in coatings and adhesives applications.

-

2024: Nouryon (Delamine BV) completed a capacity utilisation optimisation programme at its Delfzijl, Netherlands ethyleneamine production facility, improving yield toward higher-value DETA and TETA product grades whose epoxy curing agent and chelating agent applications command premium pricing relative to the EDA commodity market.

Ethyleneamines Market key players are:

-

The Dow Chemical Company

-

BASF SE

-

Huntsman Corporation

-

Nouryon

-

Tosoh Corporation

-

Delamine B.V.

-

Arabian Amines Company (Huntsman–Zamil JV)

-

Diamines and Chemicals Limited (DACL)

-

Alkyl Amines Chemicals Ltd.

-

DuPont de Nemours, Inc.

-

Shandong Lianmeng Chemical Group Co. Ltd.

-

INEOS Group Holdings S.A.

-

Sinopec Yangzi Petrochemical Co. Ltd.

-

Saudi Basic Industries Corporation (SABIC)

-

KPX Chemical Co. Ltd.

-

Balaji Amines Limited

-

Oriental Union Chemical Corporation (OUCC)

-

Nippon Shokubai Co., Ltd.

-

Mitsubishi Gas Chemical Company, Inc.

-

Celanese Corporation

Ethyleneamines Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.30 Billion |

| Market Size by 2035 | USD 6.10 Billion |

| CAGR | CAGR of 6.40% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Ethylenediamine (EDA), Diethylenetriamine (DETA), Triethylenetetramine (TETA), Tetraethylenepentamine (TEPA), Piperazine (PIP), Aminoethylpiperazine (AEP), Others) • By Grade (Commercial Grade, Industrial Grade, High-Purity Grade) • By Manufacturing Process (EDC/Ammonia Route, MEA Amination Route) • By Application (Epoxy Curing Agents, Agrochemicals, Fuel & Lubricant Additives, Water Treatment Chemicals, Pharmaceutical Intermediates, Paper & Textile Auxiliaries, Others) • By End Use Industry (Automotive, Chemical Processing, Agriculture, Oil & Gas, Pharmaceuticals, Water Treatment, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | The Dow Chemical Company, BASF SE, Huntsman Corporation, Nouryon, Tosoh Corporation, Delamine B.V., Arabian Amines Company (Huntsman–Zamil JV), Diamines and Chemicals Limited (DACL), Alkyl Amines Chemicals Ltd., DuPont de Nemours, Inc., Shandong Lianmeng Chemical Group Co. Ltd., INEOS Group Holdings S.A., Sinopec Yangzi Petrochemical Co. Ltd., Saudi Basic Industries Corporation (SABIC), KPX Chemical Co. Ltd., Balaji Amines Limited, Oriental Union Chemical Corporation (OUCC), Nippon Shokubai Co., Ltd., Mitsubishi Gas Chemical Company, Inc., Celanese Corporation |

Frequently Asked Questions

The primary growth factors are renewable energy infrastructure expansion creating growing demand for ethyleneamine-based epoxy curing agents, electric vehicle manufacturing increasing epoxy adhesive and encapsulant consumption.

The Ethyleneamines Market was valued at USD 3.30 Billion in 2025.

The Ethyleneamines Market is expected to grow at a CAGR of 6.40% from 2026 to 2035.

Asia Pacific dominated the Ethyleneamines Market in 2025, holding approximately 41.90% of global revenues.

The ethylenediamine (EDA) segment dominated the Ethyleneamines Market with 36.00% share in 2025.

Get in Touch