Architectural Services Market Report Scope & Overview:

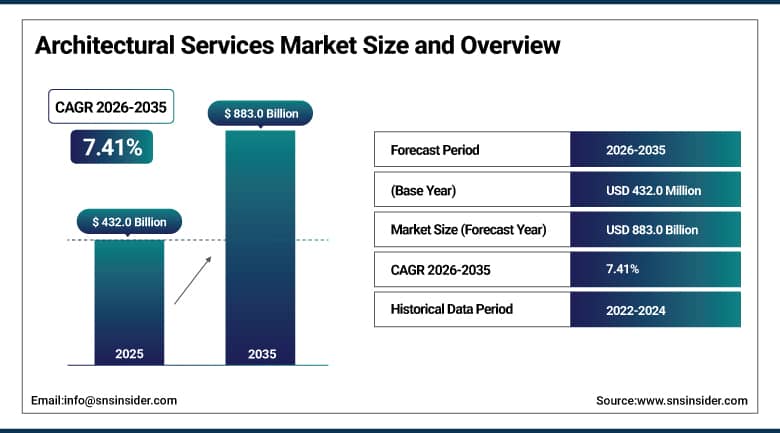

The Architectural Services Market was valued at USD 432.0 Billion in 2025 and is expected to reach USD 883.0 Billion by 2035, growing at a CAGR of 7.41% from 2026–2035.

The Architectural Services Market is growing due to several factors such as urbanization, increase in global population, demand for residential, commercial, and infrastructure construction projects. Rising initiatives by the government to develop sustainable infrastructure and smart cities have increased demand for architecture and engineering design services. The use of technologies like Building Information Modeling, 3D modeling, and digital twins is enhancing efficiency and accuracy of designs. Moreover, growing emphasis on building environmentally friendly structures and energy-efficient designs is increasing demand for architectural design services.

According to the United Nations Department of Economic and Social Affairs (UN DESA), approximately 68% of the global population is expected to live in urban areas by 2050, up from about 55% today, significantly increasing demand for urban planning and architectural services. The United Nations also projects that the global population will reach around 9.7 billion by 2050, intensifying pressure on housing, infrastructure, and built environment development, thereby supporting long-term growth in architectural services.

Architectural Services Market Size and Forecast:

-

Market Size in 2026E: USD 464.0 Billion

-

Market Size by 2035: USD 883.0 Billion

-

CAGR: 7.41% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Architectural Services Market - Request Free Sample Report

Architectural Services Market Trends:

-

Rising investment in urban infrastructure development and smart city projects driving strong demand for advanced architectural planning and design services

-

Growing adoption of sustainable and green building designs, with emphasis on energy efficiency, eco-friendly materials, and regulatory compliance

-

Increasing use of digital design tools such as BIM (Building Information Modeling) to enhance project visualization, accuracy, and collaboration

-

Expanding renovation and retrofitting activities in commercial and residential sectors to upgrade aging infrastructure and improve space utilization

-

Rising demand for integrated architectural services combining design, engineering, and project management to deliver cost-efficient and time-optimized construction outcomes

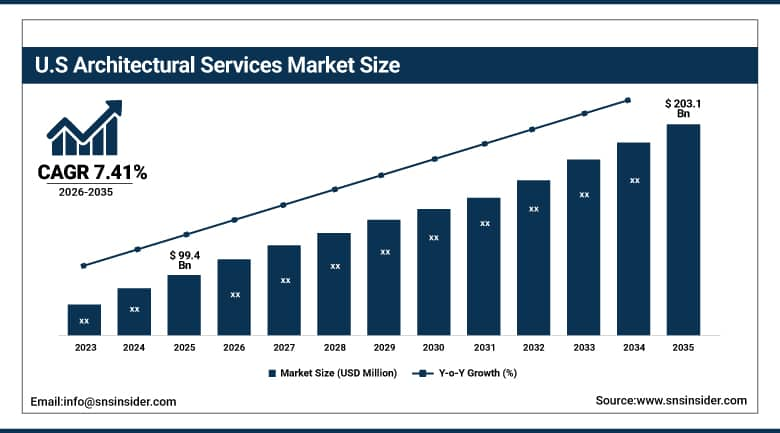

U.S. Architectural Services Market Outlook:

The U.S. Architectural Services Market was valued at approximately USD 99.4 Billion in 2025 and is expected to reach approximately USD 203.1 Billion by 2035, growing at a CAGR of approximately 7.41%.

The United States leads North American architectural services revenues through the world’s most commercially sophisticated architecture market, the highest concentration of global architecture firm headquarters, and the largest construction industry whose annual spend exceeds USD 2 trillion creating proportional professional design services procurement. Gensler, HOK, Perkins and Will, HKS, and NBBJ sustain U.S. market leadership through their integrated global design platform capabilities and deep sector expertise across healthcare, workplace, higher education, and mixed-use project typologies whose project complexity and client expectations drive above-average professional service content.

The U.S. Bureau of Labor Statistics (BLS) projects employment for architects to grow by 5% from 2023 to 2033, driven by sustained demand from commercial and residential construction activity.

Architectural Services Market Segment Analysis:

-

By Type, Construction and Project Management Services segment dominated the Architectural Services Market in 2025 with 29% share; Urban Planning Services segment is the fastest growing segment.

-

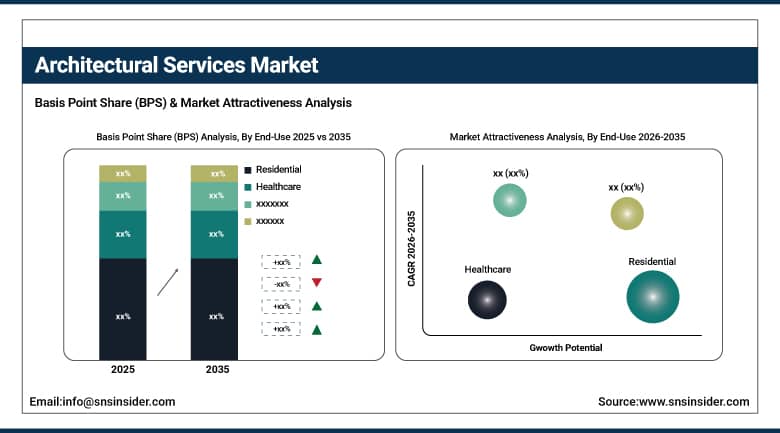

By End-Use, Residential segment dominated the market in 2025 with 34% share; Healthcare segment is the fastest growing segment.

By End-Use, residential segment dominates the architectural services market, while healthcare segment is the fastest-growing segment.

The Residential segment dominated the Architectural Services Market due to high demand for housing caused by fast-growing population. Increasing investments in housing constructions, redevelopments of urban areas, and preference for modern living standards have contributed to this dominance. The architects were actively involved in the creation of effective, aesthetically pleasing, and affordable houses. Moreover, various housing programs initiated by governments and expansion of real estate in the private sector would continue driving demand in residential architectural services.

The Healthcare segment is the fastest growing due to increasing investments in construction and improvement of hospitals, clinics, and other medical infrastructures all over the world. High demand for the construction of effective medical facilities driven by aging population and higher demand for better healthcare services was contributing to that trend. Healthcare architecture required not only aesthetics but also ensured safety and efficiency of work along with integration of advanced medical technologies.

By Type, construction and project management services segment dominates the market, while urban planning services segment is the fastest-growing segment

The Construction and Project Management Services segment dominated the Architectural Services Market owing to its critical importance in ensuring proper coordination, cost optimization, and timely completion of projects. Increased urban construction, increased infrastructural spending, and complicated construction process have led to the higher requirement for an all-inclusive project management service. Moreover, increasing trends of smart cities, along with huge investment in commercial buildings, have contributed to the dominant position of this sub-segment across the globe.

The Urban Planning Services segment is the fastest growing primarily because of the rapid pace of urbanization as well as increasing urban planning requirements across the world. Increased focus on efficient utilization of lands, better transportation networks, and smart infrastructure plans have added further fuel to the growth of this sub-segment. Moreover, increasing focus on green cities, climate-resilient infrastructures, and smart cities has increased the need for professional services in this sub-segment across the globe.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

52.4% |

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

43.8% |

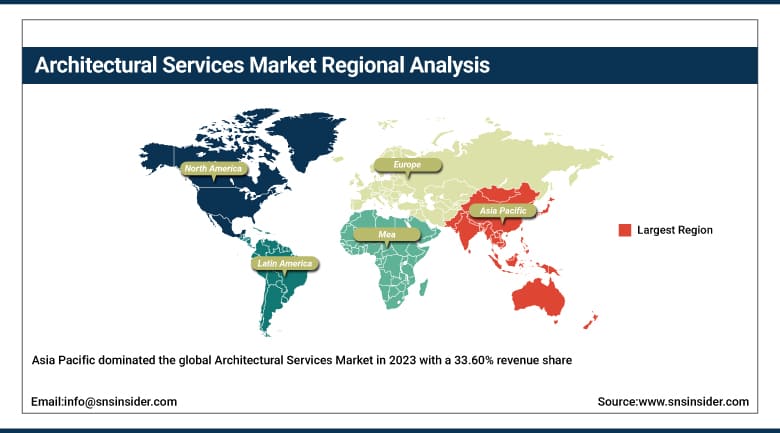

Asia Pacific Architectural Services Market Insights

Asia Pacific dominated the global Architectural Services Market in 2023 with a 33.60% revenue share, driven by rapid urbanisation across China, India, Indonesia, and Vietnam creating unprecedented housing, commercial, and infrastructure design demand. China accounts for approximately 52.4% of Asia Pacific revenues through its extraordinary urban construction scale whose annual new building floor space creation requires proportional architectural design services from both domestic firms and international architecture practices engaged for premium projects.

According to the United Nations Department of Economic and Social Affairs (UN DESA), Asia is expected to account for over 50% of the world’s urban population by 2050, making it the largest global hub for urban development and architectural demand.

The World Bank reports that East Asia already has urbanization levels exceeding 60%, with continued rapid infrastructure expansion supporting sustained construction and planning activity.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Architectural Services Market Insights

North America sustains a significant architectural services market through the United States’ premium project complexity, the world’s highest architecture firm billing rates, and the progressive integration of advanced design technology creating above-average revenue per project. The U.S. accounts for approximately 82.5% of North American revenues through Gensler, HOK, Perkins and Will, and HKS’ commercial design leadership across the office, healthcare, education, and mixed-use project typologies.

According to the U.S. Census Bureau, the U.S. population exceeded 335 million in 2024, with continued urban migration increasing demand for housing and infrastructure development, thereby supporting architectural service requirements.

Canada contributes supplementary North American revenues through its growing transit-oriented development programmes, healthcare campus redevelopment investment, and commercial real estate sector’s growing sustainable design requirements. Canadian government infrastructure investment under national housing and transit programmes creates consistent public sector architectural procurement above commercial development cycles.

Europe Architectural Services Market Insights

Europe is a technically advanced architectural services market where the European Green Deal’s building renovation requirement, EU taxonomy sustainability classification for real estate investment, and national net-zero carbon building regulations create structured demand for integrated sustainable design expertise. Germany accounts for approximately 22.4% of European revenues through its large commercial, industrial, and residential construction markets and the global reputation of German architecture firms for engineering precision.

According to Eurostat, approximately 75% of Europe’s population lives in urban areas, one of the highest urbanization rates globally, driving continuous demand for architectural and urban planning services.

The European Commission estimates that buildings account for around 40% of total energy consumption in the EU, supporting large-scale renovation and green building design initiatives. The European Environment Agency (EEA) reports that over 85% of EU citizens live in urban or peri-urban areas, further reinforcing demand for city planning, infrastructure development, and architectural services.

MEA & Latin America Architectural Services Market Insights

The UAE leads MEA revenues at approximately 38.4% through its world-class development programme, NEOM’s transformative architecture investment, and the Dubai and Abu Dhabi construction market’s premium hospitality, residential, and commercial project pipeline. Saudi Arabia’s Vision 2030 giga-project investments create the world’s most commercially active architecture procurement market per capita in the megaproject category.

Brazil leads Latin American revenues at approximately 43.8% through its large construction industry, growing commercial real estate sector’s sustainability requirements, and government infrastructure investment. Mexico and Colombia contribute growing secondary demand through commercial real estate development and government infrastructure programmes.

Market Dynamics:

Growth Drivers: Global urbanisation creating structural housing and infrastructure demand and sustainability mandates driving integrated net-zero building design investment

The architectural services market’s consistent growth is driven by urbanisation’s structural demand creation, where the United Nations’ projection of 2.5 billion additional urban residents by 2050 requiring approximately 3 billion square metres of new urban infrastructure annually creates non-cyclical professional design service demand. Each new urban resident requires housing, workplace, healthcare, education, and commercial infrastructure whose design creates architectural service procurement across the complete project typology range sustaining market growth through demographic trends that transcend economic cycles.

Building sustainability mandates create a growing premium design service tier whose integrated passive design, energy modelling, carbon accounting, and certification documentation expertise creates billable service scope above conventional design deliverables. Each new building energy code upgrade, net-zero carbon target, and sustainability certification requirement whose compliance demands specialist expertise creates architectural service engagement above baseline scope, sustaining above-inflation professional fee rate growth for firms with demonstrated sustainability design capability.

Restraints: Skills shortage in advanced digital design tools and fee compression from design-build procurement limiting revenue growth

Architecture firm skills shortages in BIM coordination, computational design, energy modelling, and AI-assisted design tools, documented as unfilled at 96% of design firms creating project delivery capacity constraints, limit revenue growth below market demand levels. Each architecture firm declining new commissions due to insufficient qualified staffing represents foregone revenue whose aggregate across the profession creates below-demand professional service supply, extending project timelines and creating client dissatisfaction that reinforces talent investment pressure.

Design-build and integrated project delivery procurement models’ progressive replacement of traditional design-bid-build in institutional and commercial client procurement, where architectural design services are bundled within contractor-led delivery contracts whose fee structures compress professional service margins relative to traditional owner-direct engagement, reduces architectural service revenue per project and creates competitive pressure that constrains average fee rate growth.

Opportunities: AI generative design commercial deployment and modular construction design services creating new professional service categories

Generative AI’s commercial deployment in architectural design, where AI-powered parametric design tools autonomously generate building configuration options, evaluate performance criteria, and optimise design parameters enabling architects to deliver client-responsive designs at a fraction of manual iteration time, creates a professional service value proposition whose speed and quality advantage over conventional practice creates competitive differentiation for firms investing in AI design platform capability.

Modular and prefabricated construction’s market share growth, driven by developer demand for schedule certainty, quality control consistency, and construction labour shortage mitigation, creates growing architectural design service demand for specialised module design, manufacturing interface coordination, and site assembly documentation. The technical barriers of modular design expertise sustain above-average professional fee rates for firms with established off-site construction design capability.

Recent Developments:

-

2024: Gensler expanded its AI-driven design platform integrating parametric design generation and energy performance simulation within a unified workflow, enabling simultaneous evaluation of hundreds of design variants against programme requirements and sustainability targets.

-

2024: HOK Group launched an enhanced sustainable design toolkit integrating carbon accounting, embodied carbon material selection, and operational energy modelling into its standard project delivery process, targeting net-zero operational carbon for all new projects by 2030.

-

2023: Perkins and Will launched a computational design studio integrating machine learning-assisted space optimisation and daylighting analysis into its healthcare and education project process, reducing iterative design cycle time and improving measurable building performance outcomes.

Architectural Services Market Key Players are:

-

AECOM

-

Jacobs Solutions Inc.

-

HDR, Inc.

-

Gensler

-

Perkins&Will

-

Foster + Partners

-

Sweco AB

-

Arup Group

-

Stantec Inc.

-

HDR Architecture Associates

-

HOK (Hellmuth, Obata + Kassabaum)

-

Nikken Sekkei Ltd.

-

SOM (Skidmore, Owings & Merrill)

-

Perkins Eastman

-

CannonDesign

-

Woods Bagot

-

BDP (Building Design Partnership)

-

CallisonRTKL (Arcadis)

-

NBBJ

-

Corgan Associates

Architectural Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 432.0 Billion |

| Market Size by 2035 | USD 883.0 Billion |

| CAGR | CAGR of 7.41% from 2026–2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Architectural Advisory Services, Construction and Project Management Services, Engineering Services, Interior Design Services, Urban Planning Services, Building Code Counseling and Interpretation Consulting Services, Legal Technical Requirement Compliance Counseling Services, Others) • By End-Use (Education, Government, Healthcare, Hospitality, Residential, Industrial, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AECOM, Jacobs Solutions Inc, HDR Inc, Gensler, Perkins Will, Foster + Partners, Sweco AB, Arup Group, Stantec Inc, HDR Architecture Associates, HOK (Hellmuth Obata + Kassabaum), Nikken Sekkei Ltd, SOM (Skidmore Owings & Merrill), Perkins Eastman, CannonDesign, Woods Bagot, BDP (Building Design Partnership), CallisonRTKL (Arcadis), NBBJ, Corgan Associates |

Frequently Asked Questions

The Architectural Services Market is expected to grow at a CAGR of 7.41% from 2026 to 2035.

The Architectural Services Market was valued at USD 432.0 Billion in 2025.

Global urbanisation creating structural housing and infrastructure demand, sustainability mandates driving integrated net-zero building design, and AI and BIM technology advancing architectural service delivery quality and efficiency are the primary growth factors.

The Residential segment dominated the Architectural Services Market with approximately 34.21% share in 2025.

Asia Pacific dominated the Architectural Services Market in 2025.

Get in Touch