Automatic Dependent Surveillance-Broadcast (ADS-B) Market Report Scope & Overview:

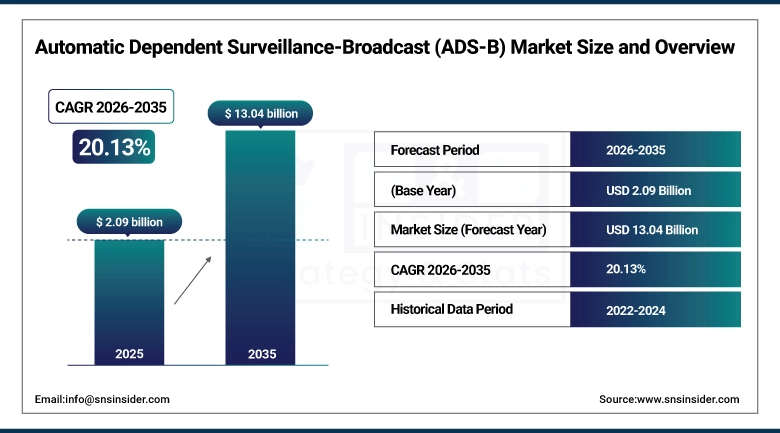

The Automatic Dependent Surveillance-Broadcast (ADS-B) Market size was valued at USD 2.09 Billion in 2025 and is projected to reach USD 13.04 Billion by 2035, growing at a CAGR of 20.13% during 2026-2035.

The market is driven by the growing need to track aircraft in real-time, the need to enhance the efficiency of air traffic management, and the need to ensure the safety of aircraft. Aviation authorities' mandates are driving the growth of the ADS-B market, especially in commercial and military aviation. The growth of the air passenger market, the modernization of airport infrastructure, and the inclusion of the next generation air navigation system are also driving the growth of the market.

Market Size and Forecast:

-

Market Size in 2025: USD 2.09 Billion

-

Market Size by 2035: USD 13.04 Billion

-

CAGR of 20.13% From 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Automatic Dependent Surveillance-Broadcast (ADS-B) Market - Request Free Sample Report

Key Automatic Dependent Surveillance-Broadcast (ADS-B) Market Trends:

-

Regulatory mandates for ADS-B Out compliance in the United States, Europe, Australia, and Singapore have driven near-universal equipage among commercial operators, shifting the primary investment focus toward ADS-B In capability upgrades that enable airborne traffic situational awareness for pilots and flight management systems.

-

Space-based ADS-B through Aireon's LEO constellation, operating on the Iridium NEXT satellite network, has achieved global coverage including oceanic and polar routes, fundamentally changing the economics of surveillance for airlines operating long-haul transoceanic flights where secondary radar coverage has never existed.

-

UAV traffic management programs under the FAA's UTM framework and equivalent EASA U-Space regulations are requiring ADS-B-compatible positioning broadcasts for drone operations in controlled and shared airspace, opening an entirely new and rapidly expanding segment for miniaturized ADS-B transponder technology.

-

Software-defined ADS-B receivers and open-architecture ground station solutions are lowering infrastructure deployment costs for smaller air navigation service providers and enabling developing nations to build surveillance coverage without high-capital investment in traditional secondary surveillance radar networks.

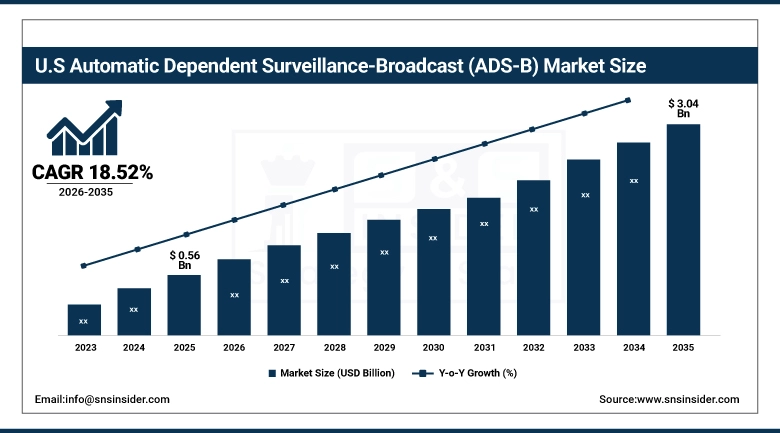

The U.S. ADS-B Market size was valued at USD 0.56 Billion in 2025 and is projected to reach USD 3.04 Billion by 2035, growing at a CAGR of 18.52% during 2026-2035. The U.S. holds a 76.42% share within the North America region and remains the single largest national market for ADS-B technology globally, underpinned by the world's busiest commercial and general aviation fleet, ongoing FAA NextGen air traffic modernization investment, and an expanding UAV industry whose traffic management requirements are driving fresh demand for low-cost ADS-B broadcast solutions.

Automatic Dependent Surveillance-Broadcast (ADS-B) Market Growth Drivers:

-

ADS-B Market Expands Rapidly Driven by Global Regulatory Mandates, NextGen Air Traffic Modernization, UAV Integration, and Space-Based Surveillance Infrastructure Investment

The dominant commercial driver for the ADS-B market is the cascade of regulatory mandates that have moved from aspiration to enforceable law across the world's major aviation jurisdictions. The FAA's January 2020 rule requiring ADS-B Out in Class A, B, C, and E airspace brought more than 160,000 aircraft in the U.S. into compliance and established a permanent baseline of equipped aircraft that feeds ongoing receiver, software, and ground infrastructure spending. Europe followed a similar trajectory under EASA's airspace modernization rules, and Australia, Japan, Singapore, and Canada have implemented comparable mandates that collectively cover the majority of international commercial traffic. Beyond the initial compliance wave, second-order investment is accelerating ADS-B In cockpit displays, which allow pilots to receive traffic and weather data broadcast over the ADS-B datalink, are being rolled out across commercial and business aviation fleets as operators recognize the operational and safety value delivered at relatively modest incremental cost.

Automatic Dependent Surveillance-Broadcast (ADS-B) Market Market Restraints:

-

ADS-B Market Growth Constrained by High Retrofit Costs for Aging Fleets, Cybersecurity Vulnerabilities in Broadcast Protocols, and Regulatory Inconsistencies Across Developing Market Jurisdictions

The global ADS-B market has a series of significant limitations, which, while driving adoption in some areas, have slowed adoption in other areas. The cost factor, particularly in the case of general aviation, has been a major limitation, given that avionics’ upgrades are required, which, depending upon existing avionics compatibility, could cost anywhere between several thousands and several tens of thousands of dollars per aircraft. The more technically challenging limitation, however, relates to the inherent cybersecurity risk associated with the ADS-B transmission protocol.

Automatic Dependent Surveillance-Broadcast (ADS-B) Market Opportunities:

-

UAV Traffic Management Expansion, Urban Air Mobility Infrastructure, and Developing Region Fleet Growth Offer Significant ADS-B Market Opportunities Through 2035

Several large and structurally durable growth opportunities exist across the ADS-B market through the forecast period. The most immediate and volume-driven opportunity is the UAV and unmanned traffic management segment, where BVLOS operations require verified position broadcasts compatible with manned aircraft surveillance systems. FAA BEYOND and UAS Integration Pilot Programs, along with EASA's U-Space regulatory framework adopted across EU member states, are creating enforceable technical requirements for ADS-B-compatible position reporting that manufacturers of miniaturized transponders and software-defined broadcast modules are positioned to address. Urban air mobility developers including Joby Aviation, Archer, and Wisk, all of which received FAA certification milestone approvals in 2024-2025, are designing ADS-B connectivity into their aircraft from the ground up, creating a forward pipeline of equipped platforms.

Automatic Dependent Surveillance-Broadcast (ADS-B) Market Segment Analysis

-

By Type / System, ADS-B Out dominated with 56.48% in 2025, and ADS-B In is expected to grow at the fastest CAGR of 21.99% from 2026 to 2035.

-

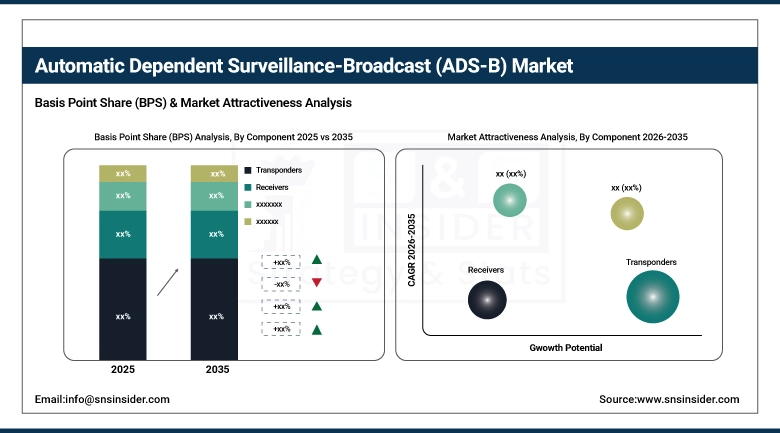

By Component, Transponders dominated with 42.37% in 2025, and Receivers are expected to grow at the fastest CAGR of 21.30% from 2026 to 2035.

-

By Application, Airborne Surveillance dominated with 41.26% in 2025, and Airport Surface Surveillance is expected to grow at the fastest CAGR of 21.14% from 2026 to 2035.

-

By Platform / End-Use, Commercial Aviation dominated with 49.68% in 2025, and Unmanned Aerial Vehicles (UAVs) are expected to grow at the fastest CAGR of 22.59% from 2026 to 2035.

By Type / System, ADS-B Out Leads the Market While ADS-B In Set for Fastest Growth 2026 to 2035

In 2025, ADS-B Out dominated the market in the Type/System segment, driven by the high number of ADS-B Out-compliant aircraft in the commercial and general aviation fleets, as they completed the FAA and EASA-mandated equipage programs in the previous years. ADS-B Out transponders, which transmit the aircraft's position, altitude, velocity, and ID, are the first and most important part of the compliance solution that regulators mandated, creating the initial growth spike that set the market's scale. ADS-B In is expected to have the highest CAGR growth and expand in 2025. ADS-B In, which enables an aircraft to receive and display traffic and weather information transmitted over the ADS-B system, is moving from an optional upgrade to the standard equipment list for new commercial aircraft as the value of the solution becomes more appreciated by the airlines.

By Component, Transponders Lead ADS-B Market While Receivers and Software See Rapid Growth Through 2035

The largest share of the transponders market segment in 2025 can be attributed to the commanded share, considering the fitment mandate for regulated aviation platforms for ADS-B Out transponders. Transponders from approved manufacturers are subjected to strict aviation technical standard orders, including frequency accuracy, output power, message encoding, and environmental conditions, thereby presenting a technically demanding market with strict certification hurdles, favoring established avionics manufacturers. For the period from 2026 to 2035, the Receivers segment is likely to record the highest CAGR, considering the expansion of ADS-B In among commercial and business aviation, and UAV fleet managers requiring compatible receivers for traffic awareness in shared airspace.

By Application, Airborne Surveillance Dominates While Airport Surface Surveillance Poised for Fastest Growth in ADS-B Market 2026 to 2035

Airborne Surveillance led the application segment in 2025, driven by the need to equip all commercial and general aviation aircraft in controlled airspaces across the globe with ADS-B technology. The constant need to update the avionics in newly delivered aircraft, as well as those in the middle of their life cycles, ensures the segment maintains its position as the largest market value segment from 2026 to 2035. Airport Surface Surveillance will experience the highest CAGR from 2026 to 2035, driven by the need to install ADS-B technology on the ground to prevent runway incursions in low-visibility conditions at international airports worldwide.

By Platform / End-Use, Commercial Aviation Leads ADS-B Market While UAVs Set for Fastest Growth 2026 to 2035

Commercial Aviation led the market in the Platform / End-Use segment in 2025, owing to the universal ADS-B Mandate Compliance status of global commercial airline fleets and the regular aircraft delivery pipeline from Airbus and Boeing, adding ADS-B enabled aircraft to the global commercial aviation fleet at the rate of hundreds per month. Unmanned Aerial Vehicles (UAVs) are expected to have the highest CAGR from 2026 to 2035.

Automatic Dependent Surveillance-Broadcast (ADS-B) Market Regional Analysis:

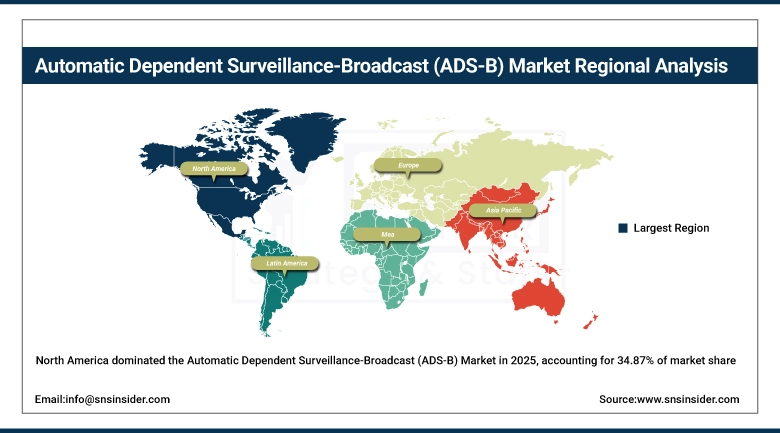

North America ADS-B Market Insights

In 2025, North America dominated the global ADS-B market with a 34.87% share valued at USD 0.73 Billion, growing at a CAGR of 18.87% through 2035. The region's market leadership reflects its position as the world's largest single-country aviation market by aircraft count, the maturity of the FAA's ADS-B mandate enforcement, and the ongoing NextGen air traffic modernization program that continues to integrate ADS-B surveillance data into the full operational backbone of the U.S. national airspace system. Sustained investment in FAA automation infrastructure, including the Automatic Terminal Information Service replacement and next-generation STARS terminal automation platforms, generates recurring demand for ADS-B data interfaces and ground station upgrades.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. ADS-B Market Insights

In North America, the United States dominated the ADS-B market in 2025, supported by the world's largest general aviation fleet, the highest commercial service frequency of any national airspace, and the FAA's role as the primary global benchmark-setter for ADS-B mandate design and technical standards.

Europe ADS-B Market Insights

In 2025, Europe held a 21.76% share of the global ADS-B market at USD 0.45 Billion, growing at a CAGR of 19.19% through 2035. EASA's Single European Sky ATM Research (SESAR) program, which designated ADS-B as a core enabling technology for the unified European airspace architecture, continues to drive ground infrastructure investment across Eurocontrol member states and national ANSP upgrade programs. The adoption of U-Space regulations across EU member states from 2023 onward established a formal regulatory framework for drone operations that incorporates ADS-B connectivity requirements, accelerating miniaturized transponder procurement by commercial drone operators. Avinor in Norway, DFS in Germany, NATS in the UK, and DSNA in France have all published multi-year capital investment plans that include ADS-B ground station expansion components through 2030.

Germany ADS-B Market Insights

In Europe, Germany was the leading market in terms of ADS-B in 2025 due to the significant influence of DFS Deutsche Flugsicherung, one of the busiest and most technologically advanced air navigation services in Europe, the high commercial air traffic density in German airspace, being an important gateway between Eastern and Western Europe, and the significant contribution to the development programs of SESAR Joint Undertaking.

Asia Pacific ADS-B Market Insights

Asia Pacific is expected to grow at the fastest CAGR of 22.47% from 2026 to 2035 in the global ADS-B market, with the region valued at USD 0.51 Billion in 2025. The region's growth trajectory is driven by the fastest-expanding commercial aviation fleet globally, where Airbus and Boeing forecasts project Asia Pacific will require over 17,000 new commercial aircraft through 2042, each delivered with ADS-B avionics as standard equipment. India's civil aviation boom, with domestic passenger traffic recovering beyond pre-pandemic levels in 2024 and the AAI pursuing comprehensive ATC modernization including ADS-B ground network rollout across all major and secondary airports, represents one of the largest single-country infrastructure opportunities in the segment.

China ADS-B Market Insights

In Asia Pacific, China dominated the ADS-B market from 2025 onward, backed by the CAAC's nationwide ADS-B mandate covering commercial operations across one of the world's fastest-growing air traffic environments, the scale of China's domestic avionics manufacturing base, and the government's sustained investment in civil aviation infrastructure under its 14th and forthcoming Five-Year Plans.

Latin America (LATAM) and Middle East & Africa (MEA) ADS-B Market Insights

In 2025, Latin America and the Middle East & Africa together exhibited consistent growth in the global ADS-B market. Latin America held a 10.18% share at USD 0.21 Billion with a CAGR of 20.96% through 2035, led by Brazil's DECEA and ANAC modernization programs and Mexico's SENEAM ATC infrastructure upgrades that include ADS-B ground receiver expansion across major and regional airports. The Middle East & Africa held an 8.86% share at USD 0.19 Billion with a CAGR of 18.85%, driven by the rapid growth of Gulf carrier fleets operating out of Dubai, Abu Dhabi, and Doha, which serve as the world's busiest international transit hubs, and the corresponding GCAA and GACA investments in ATC infrastructure to handle expanding traffic volumes. South Africa's ATNS and Kenya's KCAA represent the most active ADS-B ground infrastructure procurement programs in sub-Saharan Africa, where ADS-B is increasingly seen as the primary path to surveillance coverage given the prohibitive cost of radar installation across the continent's vast and sparsely monitored airspace.

Competitive Landscape for Automatic Dependent Surveillance-Broadcast (ADS-B) Market:

Garmin Ltd. is a global leader in aviation navigation and communication devices, with headquarters in Olathe, Kansas, and one of the widest certified product offerings in the global aviation industry, including transponders, receivers, cockpit displays, and integrated avionics products for commercial, business, and general aviation aircraft.

-

In 2024, Garmin received FAA TSO and STC approval for its GNX 375 GPS/ADS-B navigator with integrated ADS-B In and Out, enabling single-box compliance for general aviation operators and expanding its position in the growing retrofit market for aircraft requiring both GPS upgrading and ADS-B mandate compliance.

Honeywell International Inc., with headquarters in Charlotte, North Carolina, is one of the major suppliers of integrated avionics and ADS-B transponder products, including integrated avionics suites, such as Primus Epic and Anthem, which offer certified ADS-B In and Out functionality as standard.

- In 2025, Honeywell announced certification progress on its next-generation Compact Multi-Mode Receiver with integrated ADS-B In processing, targeting business jet and regional turboprop operators seeking a cost-optimized upgrade path to full ADS-B In situational awareness without a full flight deck replacement.

Automatic Dependent Surveillance-Broadcast (ADS-B) Market Key Players:

Some of the ADS-B Market Companies are:

-

Garmin Ltd.

- Honeywell International Inc.

- L3Harris Technologies Inc.

- Thales Group

- Collins Aerospace

- Indra Sistemas S.A.

- Aireon LLC

- Saab AB

- Aspen Avionics Inc.

- Avidyne Corporation

- Trig Avionics Limited

- FreeFlight Systems

- uAvionix Corporation

- Becker Avionics GmbH

- ACSS (Aviation Communication & Surveillance Systems)

- Leonardo S.p.A.

- Raytheon Technologies Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- Intelcan Technosystems Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.09 Billion |

| Market Size by 2035 | USD 13.04 Million |

| CAGR | CAGR of 20.13% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type / System (ADS-B Out, ADS-B In, and Ground-Based ADS-B Systems) • By Component (Transponders, Receivers, Antennas, and Software & Ground Infrastructure) • By Application (Airborne Surveillance, Terminal Maneuvering Area (TMA) Surveillance, Airport Surface Surveillance, and Air Traffic Control (ATC) Surveillance) • By Platform / End-Use (Commercial Aviation, Military Aviation, General Aviation, and Unmanned Aerial Vehicles (UAVs)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Garmin Ltd., Honeywell International Inc., L3Harris Technologies Inc., Thales Group, Collins Aerospace, Indra Sistemas S.A., Aireon LLC, Saab AB, Aspen Avionics Inc., Avidyne Corporation, Trig Avionics Limited, FreeFlight Systems, uAvionix Corporation, Becker Avionics GmbH, ACSS (Aviation Communication & Surveillance Systems), Leonardo S.p.A., Raytheon Technologies Corporation, Northrop Grumman Corporation, BAE Systems plc, Intelcan Technosystems Inc. |

Frequently Asked Questions

Airport Surface Surveillance is the fastest-growing application segment with a CAGR of 21.14% from 2026 to 2035.

North America dominated the ADS-B Market in 2025 with a 34.87% share.

ADS-B Out dominated the ADS-B Market with a 56.48% share in 2025.

The key drivers of the ADS-B market are global regulatory mandates for ADS-B Out equipage, FAA and EASA NextGen and SESAR air traffic modernization programs, rising adoption of ADS-B In for cockpit traffic situational awareness, rapid growth of UAV operations requiring UTM-compatible surveillance broadcasts, and space-based ADS-B infrastructure enabling oceanic and polar route surveillance.

The ADS-B Market size was USD 2.09 Billion in 2025 and is expected to reach USD 13.04 Billion by 2035.

Get in Touch