Full Flight Simulator Market Report Scope & Overview:

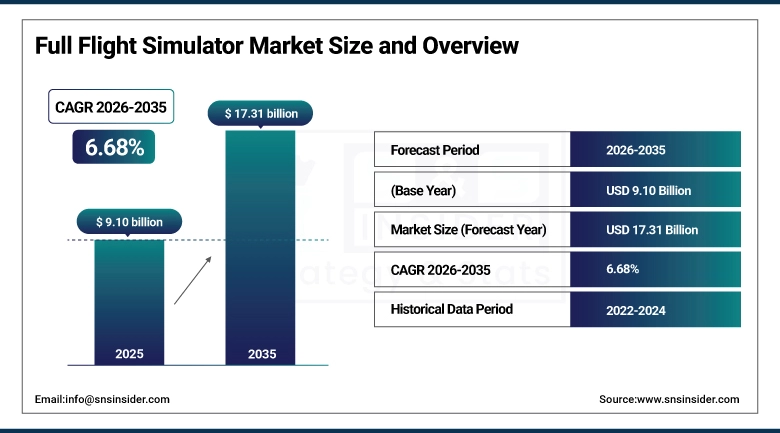

The Full Flight Simulator Market size is valued at USD 9.10 Billion in 2025 and is projected to reach USD 17.31 Billion by 2035, growing at a CAGR of 6.68% during the forecast period 2026–2035.

The Full Flight Simulator (FFS) Market analysis report includes a detailed analysis of the market dynamics, technological developments, and training applications. Increasing global air travel, growing need for certified pilots, increased adoption of advanced simulation technologies, and expanding airline training infrastructure are some of the factors propelling the Full Flight Simulator Market growth during the forecast period of 2026-2035. Full Flight Simulator usage exceeded hundreds of thousands of pilot training sessions annually in 2025, fueled by growing airline fleet expansions and regulatory requirements for Level D simulators.

Market Size and Forecast:

-

Market Size in 2025: USD 9.10 Billion

-

Market Size by 2035: USD 17.31 Billion

-

CAGR: 6.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Full Flight Simulator Market - Request Free Sample Report

Full Flight Simulator Market Trends:

-

Regulatory bodies like FAA, EASA, and ICAO are demanding Level D simulators for type rating and recurrent training.

-

Advancement in modern technologies like AI-based adaptive training, virtual and augmented reality-based simulators, and portable modular simulators.

-

Increasing acceptance of simulators in military aviation for cost-effective and mission-ready training.

-

Trend toward airline-owned training centers and regional academies to address pilot shortages.

-

Advancements in simulators in terms of motion systems, visual fidelity, and analytics.

-

Growth in demand for helicopter and business aircraft simulators for specialized markets.

-

Emergence of new business models based on a hybrid approach using full-flight simulators and virtual and augmented reality-based simulators.

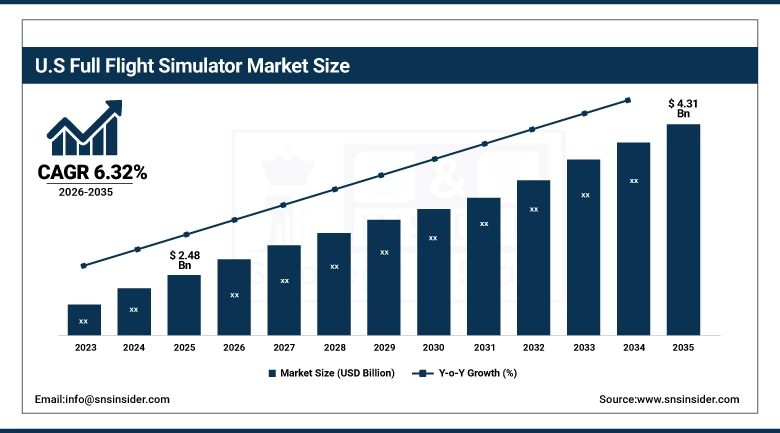

U.S. Full Flight Simulator Market Insights:

The U.S. Full Flight Simulator Market is projected to grow from USD 2.48 Billion in 2025 to USD 4.31 Billion by 2035, at a CAGR of 6.32%. The growth of the U.S. Full Flight Simulator Market can be attributed to the growing need for certified pilots, increased airline fleet expansions, high acceptance rates for advanced simulator technologies, and investments in innovative motion simulators, visual simulators, and VR/AR simulators by airline training centers and military academies.

Full Flight Simulator Market Growth Drivers:

- Rising airline fleet expansions and pilot shortages are driving demand for advanced Full Flight Simulators.

Airlines, training academies, and military organizations are using high fidelity Level D simulators to fulfill regulatory demands and ensure pilot competency. Investments in motion simulators, visual simulators, and VR/AR-enabled simulators are further driving the adoption of simulators to ensure efficient training, safety, and accuracy, thereby boosting pilot performance and driving the market growth.

Over 58% of airlines, training centers, and military academies utilized advanced Full Flight Simulators in 2025 to meet certification standards and address growing pilot demand.

Full Flight Simulator Market Restraints:

- High initial investment costs and ongoing maintenance requirements are restraining adoption of Full Flight Simulators.

Airlines, academies, and military forces have to incur high capital costs for procuring Level D simulators. In addition, there are recurring costs associated with software upgrades, hardware maintenance, and regulatory compliance. These are barriers to entry, especially for emerging nations. The limited availability of skilled instructors and technical staff, which reduces training efficiency and makes it difficult to fully utilize advanced simulator capabilities.

More than 42% of smaller regional airlines and academies faced delays in procuring simulators in 2025 due to budget constraints and high infrastructure costs.

Full Flight Simulator Market Opportunities:

- Expansion of advanced training technologies and digital ecosystems is creating strong opportunities for Full Flight Simulator growth.

Airlines, academies, and defense forces are increasingly incorporating simulators with AI-driven analytics, cloud-based training solutions, and real-time performance monitoring tools to improve the competency level of pilots and lower the operational costs. The development of blended learning solutions, incorporating simulators with VR/AR and desktop simulators, is also expected to drive the simulator market with its increasing adoption, thus fueling the growth of the simulator market.

In 2025, more than 61% of airlines, training facilities, and military academies anticipate either updating their current simulator systems or integrating new, more sophisticated ones.

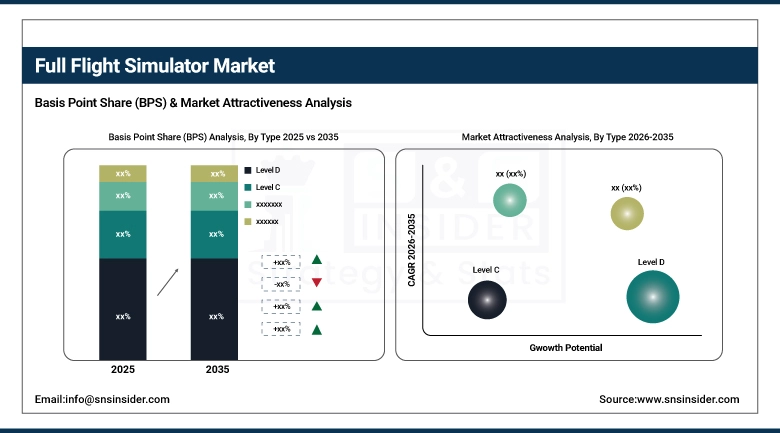

Full Flight Simulator Market Segmentation Analysis:

-

By Type, Level D held the largest market share of 59.38% in 2025, while they are also expected to grow at the fastest CAGR of 5.81% during 2026–2035.

-

By Aircraft Type, Commercial Aircraft dominated with 68.54% market share in 2025, whereas they are also projected to record the fastest CAGR of 5.98% through 2026–2035.

-

By Technology, Motion-enabled FFS accounted for the highest market share of 72.82% in 2025, while Non-motion FFS are expected to grow at the fastest CAGR of 5.89% during the forecast period.

-

By Provider Type, Original Equipment Manufacturers (OEMs) dominated with a 67.71% share in 2025, while Military Training Providers are anticipated to expand at the fastest CAGR of 5.31% through 2026–2035.

By Type, Level D Dominates as Both the Largest and Fastest‑Growing Segment:

The Level D simulators dominate the market share with the highest fidelity simulators available, with the highest level of realism. Their dominance can be attributed to the fact that regulatory requirements are very strict, requiring Level D certification for type rating and recurrent training. This has ensured that Level D simulators are the preferred choice for all airlines, academies, and defense forces around the world.

In the year 2025, Level D simulators are fastest growing and most widely used training systems, indicating high levels of confidence within the industry. The high growth rate of Level D simulators can be attributed to the high levels of innovation in artificial intelligence-based adaptive learning, as well as the integration of virtual and augmented reality.

By Aircraft Type, Commercial Aircraft Dominates as Both the Largest and Fastest‑Growing Segment:

Commercial Aircraft simulators are dominated with market share and it is a the most popular type of training system used by the airline industry. This can be attributed to the increase in global passengers traveling by air, the growth of the number of aircraft used by airlines, and the need for strict compliance with regulations by pilots. This can be attributed to the high demand by airlines and academies for these simulators.

Also, Commercial Aircraft simulators have emerged as the fastest growing first choice for training pilots, thereby highlighting their importance. The growth of Commercial Aircraft simulators can be attributed to the high level of investment going into these simulators, which provide realistic training for pilots.

By Technology, Motion‑enabled FFS Leads While Non‑motion Systems Gain Traction:

Full Flight Simulators with motion is emerged as a dominated share with the most prevalent simulators due to the realistic simulation of the aircraft’s dynamics, which are made possible with the use of sophisticated motion simulators. Their popularity can also be attributed to the regulatory body’s preference for them and the operators’ confidence in the realistic simulation experience they provide.

The popularity of Non-motion Simulators is on the rise at a fastest rate, driven by the cost-effectiveness and flexibility they offer, particularly for regional academies, helicopter training, and initial pilot training. Their popularity is also driven by the portability of the simulators, making them ideal for emerging markets.

By Provider Type, Original Equipment Manufacturers (OEMs) Leads While Military Training Providers Gain Traction:

Original Equipment Manufacturers (OEMs) segment dominates the Full Flight Simulator market, owing to their capacity to provide certified high-fidelity solutions that match the specifications of the aircraft. Their strong associations with aircraft manufacturers and authorities enable the widespread adoption of Full Flight Simulators by airlines, academies, and defense forces, thereby making OEMs the preferred choice for advanced pilot training solutions.

Military Training Providers, on the other hand, are fastest growing segment, supported by increasing defense expenditures, the need for mission-ready pilots, and the use of simulators for fighter, transport, and rotorcraft aircraft. Their growth is a strategic move to improve operational readiness and reduce training costs while maintaining high safety standards.

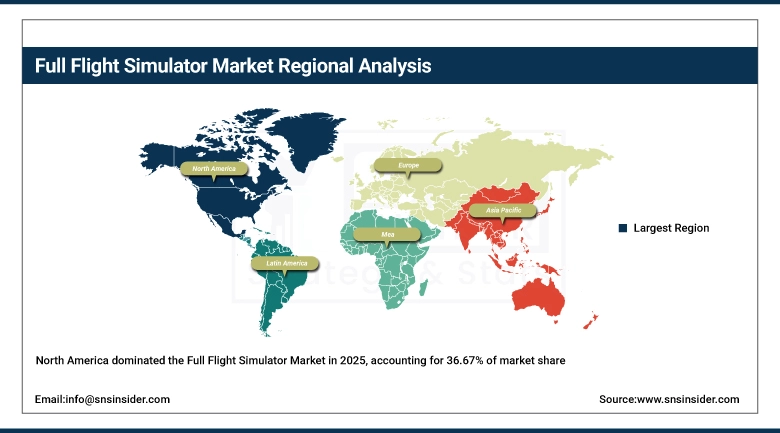

Full Flight Simulator Market Regional Analysis:

North America Full Flight Simulator Market Insights:

The market for the North American Full Flight Simulator market is dominated by the segment, holding a significant market share of 36.67%. The growth of the market is attributed to the increase in the number of fleet expansion programs by airlines, the scarcity of pilots, and the increasing number of Level D simulators. The innovations in the simulator’s motion, visual, and artificial intelligence-based adaptive training are also contributing to the growth of the market, which is considered mature.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Full Flight Simulator Market Insights:

The U.S. Full Flight Simulator Market is driven by a large commercial aviation market, extensive defense training needs, and strong regulatory requirements from the FAA. Airlines, academies, and military organizations are investing heavily in sophisticated simulators to meet regulatory requirements and address pilot staffing needs. Technology advancements, including analytics integration, portable modular simulators, and improved motion and visual simulation, are key growth drivers.

Asia‑Pacific Full Flight Simulator Market Insights:

Asia Pacific is the fastest-growing market and has a CAGR of 8.30%. This is due to the growing aviation markets in China, India, and Southeast Asia. Passenger traffic is increasing rapidly in the region. Airline fleets are expanding rapidly in the region. Severe pilot shortages are also driving the need for Level D simulators. Government support and infrastructure development are also adding to the growth in the region. The region is growing rapidly and is the most dynamic market for future growth.

China Full Flight Simulator Market Insights:

China’s Full Flight Simulator market is in an expansion phase due to the high growth of civil aviation, increased passenger traffic, and large fleet orders by local airlines. Government initiatives in developing infrastructure and establishing new academies are driving the Full Flight Simulator market in China. Level D simulators are being adopted to solve the acute pilot shortage problem in China; in addition, VR/AR-enabled simulators and modular simulators are also gaining popularity in China as cost-effective solutions.

Europe Full Flight Simulator Market Insights:

The market in Europe is driven by EASA regulations, airline presence, and training infrastructure in countries like Germany, France, and the U.K. The region is also driven by increasing demand for commercial pilot training services, growing defense contracts, and adoption of advanced simulators for business aviation. Ongoing investments in environmentally friendly and cost-effective training solutions, along with the adoption of VR and AR technologies, further emphasize Europe as a significant hub for simulator innovation.

Germany Full Flight Simulator Market Insights:

The Full Flight Simulator market in Germany is fueled by EASA’s stringent rules, major airlines, and established training academies. The nation’s aviation infrastructure is highly developed, and there is strong need for Level D simulators. Growth is fueled by ongoing technological advancements in motion simulators, realistic visuals, and AI-enabled adaptive learning capabilities.

Latin America Full Flight Simulator Market Insights:

Latin American market is expanding steadily with an increase in air operations in Brazil and Mexico. The region is witnessing an increase in demand for cost-effective pilot training solutions. Adoption of simulator solutions is encouraged through academies and partnerships with international companies. Infrastructure is still an issue for Latin America, but investments in modular and VR-enabled solutions are on the rise.

Middle East & Africa Full Flight Simulator Market Insights:

The Middle East & Africa region is gaining momentum due to its high investment in aviation hubs like the UAE, Saudi Arabia, and South Africa. The growing need for pilot training in commercial and military aircraft, and the increase in the number of aircraft in operation, are boosting the adoption of simulators. Strategic alliances with OEMs and government support to enhance aviation infrastructure are adding to the growth story of the region, making it an emerging market.

Full Flight Simulator Market Competitive Landscape:

CAE Inc. is a Canadian multinational company that focuses on providing simulation technologies and training services. The company is a leader in providing Full Flight Simulator services. CAE Inc. provides various services in commercial aviation, business aviation, and defense markets. The company focuses on providing Level D simulators that meet international regulatory requirements. CAE Inc. invests heavily in R&D in virtual technology, AI-based training programs, and portable simulators. CAE Inc. is a leader in providing training services globally in association with various major airlines and defense forces.

-

In 2025, CAE expanded its training partnerships with multiple Asia-Pacific airlines, enhancing pilot access to advanced simulators and strengthening its footprint in the fastest-growing aviation region.

FlightSafety International is a US-based leader in the aviation industry, specifically in the training and simulation segment, with a reputation for its large fleet of Full Flight Simulators for the commercial, business, and military aviation sectors. The organization prides itself on its commitment to safety, regulatory compliance, and operational excellence, with its Full Flight Simulators being certified at the highest level of fidelity. The organization’s partnerships with the world’s leading aircraft manufacturers and operators drive the demand for its services, especially in North America and Europe.

-

In 2025, FlightSafety introduced upgraded visual systems in its simulators, improving pilot situational awareness and enhancing training outcomes for both commercial and military clients.

L3Harris Technologies (L3 Simulation & Training) is a defense and aerospace company based in the U.S. that plays a vital role in the Full Flight Simulator industry. L3Harris specializes in military and commercial pilot training. L3 simulators have gained popularity for their avionics integration capabilities and modularity. L3Harris Technologies has expertise in the defense industry and provides cost-effective and mission-ready simulators. It has also expanded its services to the commercial aviation industry. L3Harris has expertise in innovation in terms of motion platforms and adaptive training and virtual reality/augmented reality.

-

In 2025, L3Harris broadened its military training contracts across Europe. They rolled out sophisticated simulators, designed for both fighter aircraft and transport planes. This move underscored the company's strengths in both the defense and commercial sectors.

Full Flight Simulator Market Key Players:

Some of the Full Flight Simulator Market Companies are:

-

CAE Inc.

-

FlightSafety International

-

L3Harris Technologies

-

Thales Group

-

Indra Sistemas S.A.

-

Rockwell Collins (Collins Aerospace)

-

TRU Simulation + Training (Textron)

-

Reiser Simulation and Training GmbH

-

AXIS Flight Simulation

-

HAVELSAN A.S.

-

Quantum3D Inc.

-

Pacific Simulators

-

Frasca International Inc.

-

Aerosim Technologies Inc.

-

Sim-Industries (Lockheed Martin subsidiary)

-

STS (Specialized Training Systems)

-

ALSIM Simulators

-

Avion Group

-

Entrol Flight Simulation

-

ECA Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.10 Billion |

| Market Size by 2035 | USD 17.31 Billion |

| CAGR | CAGR of 6.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Level D, Level C, Level B & A, Fixed Base FFS, Others), • By Aircraft Type (Commercial Aircraft, Military Aircraft, Heicopters, General Aviation, Others), • By Technology (Motion-enabled FFS, Non-motion FFS, Others), • By Provider Type (Original Equipment Manufacturers (OEMs) , Airline-Owned Training Centers, Independent Training Academies, Military Training Providers, Technology Integrators / VR/AR Providers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CAE Inc., FlightSafety International, L3Harris Technologies, Thales Group, Indra Sistemas S.A., Rockwell Collins (Collins Aerospace), TRU Simulation + Training (Textron), Reiser Simulation and Training GmbH, AXIS Flight Simulation, HAVELSAN A.S., Quantum3D Inc., Pacific Simulators, Frasca International Inc., Aerosim Technologies Inc., Sim-Industries (Lockheed Martin subsidiary), STS (Specialized Training Systems), ALSIM Simulators, Avion Group, Entrol Flight Simulation, ECA Group. |

Frequently Asked Questions

Advances in motion systems, AI-driven adaptive training, integrated analytics, and VR/AR immersion are enhancing realism, reducing pilot fatigue, and expanding simulator applications beyond traditional training.

Key opportunities include Expansion of airline-owned training centers, Adoption of VR/AR-enabled simulators for cost-effective training, Rising demand for military and helicopter simulators, etc.

Asia-Pacific is the fastest-growing region, with a CAGR above 8.30%, fueled by booming aviation markets in China, India, and Southeast Asia, alongside increasing pilot shortages.

North America currently leads, accounting for 36.67 of the global market, due to FAA regulations, strong airline presence, and established training infrastructure.

The market is projected to grow at a compound annual growth rate (CAGR) of around 6.68%, driven by rising demand for pilot training, regulatory mandates, and technological innovation.

Get in Touch